Hello @Investor_No_1, @Himanshu_Nigam , @ranjan_r ,

Thank you guys for dropping in and keeping me engaged.

First let me start with disclaimer. I am no authority on Abbott or for that matter any company. It just happened to me and was lucky break. I didnt unearth it and it is not a product of any system or process at my end. And when i bought it i didnt have foresight either that it would become this big , just like i dont know where Abbott or any of my investee companies will go in future

Many , if numbers were to tell the story, the increase in Sales and Operating margin every year indicate either new products, or pricing power , volume growth or better sales mix, The Annual report does keep mentioning of new products, but being from non pharma background I dont understand it.

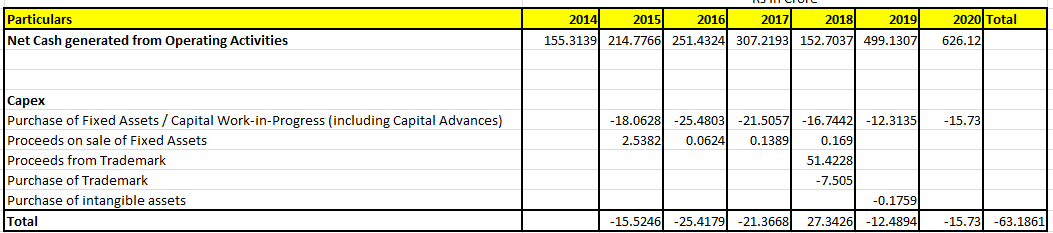

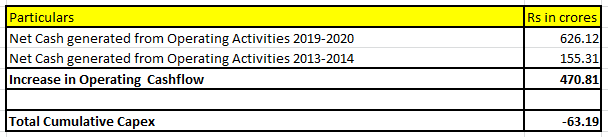

The screener has data from 2007 and i have gone through annual report from 2014. There has been never huge Capex. And even the Capex is purchase of Intangible like Trade name and all. Its primarily a trading company (selling products either sourced from related party or other companies under its brand name) in my opinion.

True

The business from what i understand doesn’t require huge Capex in Fixed Assets (you can refer numbers and discussion in above posts), though every year it does automatically invest in working capital (increase in debtors and inventory).

Now you dont have much room for reinvestment , but where Abbot scores is increasing Pre Tax ROCE by wide margin on existing capital base and minuscule new investment in Fixed Asset and working capital. Last year the Pre Tax ROCE from Core Business was 83% and these year its 150%

I subtract Interest income from EBIT for calculation of ROCE from core business because whether you or i or Abbott does Fixed Deposit, we get the same interest rate and has no meaning at all as the income aint business related

To sum it up , the reinvestment rate aint great, but ROCE is too great and increasing

Its not only Abbott but all MNC’s. There is change in Dividend Tax laws. Earlier there was DDT Tax regime (Dividend Distribution Tax Regime) where the tax on dividend was directly paid by company. so Foreign Holding companies couldn’t claim Tax credit in their home countries and has to pay tax on Dividend too. leading to multiple Tax of same income. So the MNC’s kept cash on their books. Now from this year, its recipient who has to pay tax on dividend and Foreign holding companies can claim credit of Tax paid in India in their home countries. And i hope this trend to continue and its time to load up Cash Rich MNC’s

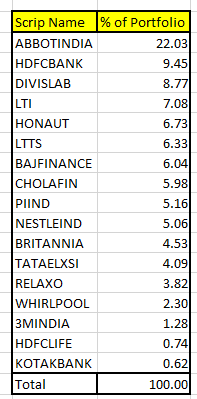

Its difficult for me too and it already forms a large part of my portfolio too. I am loading up on VST Industries and Procter and Gamble Health to shoulder some weight of portfolio for now. And hopefully they will do the heavy lifting in future

I am not good on valuation but have basic valuation tool in my mind (which may not make sense to you at all). If you see i like and have companies which may in all possibility become dividend plays in future when growth comes off (like Abbott, Sanofi, VST, Nestle, HDFC AMC) and some companies only and only for Growth(Like HDFC Bank, Relaxo, Bajaj Finance, WhirlPool, 3M, Honeywell). That way i can have best of both world of Dividend and Growth Investing. On my First Abbot share which i bought at 4k i am currently having 5.5 % dividend yield (ofcourse there is special Dividend in it).

For Future Dividend play i run a mental calculation at what price the Dividend Yield on original cost will be near or exceed Risk Free Rate in next 4-5 years. Current Risk Free rate is around 6% , and there are lot of if’s and but’s in calculation (more of a optimist assumptions)

Say Vst Industry is around 3% yield as of today, do i see it getting at 6 % in next 4-5 years?

Overall I have a aim of generating 12% return (3% from Dividend and 9% from Capital Gains )post Tax and without much Churning and being engaged from a decent portfolio of Dividend Growth Stocks and Growth Stocks in next decade. The GDP growth rate even in Pre Covid world for India was 4% and that too was doubtfull. Overall it looks difficult, but lets see

Thank @Investor_No_1

Thanks @Himanshu_Nigam

Its my pleasure to engage in discussion as it made me to think clearly and as they say you cant be great investor untill you think clearly

Thank you all

Harsh