Hello Fellow Members

This is my first post (i have been silent reader all these years ) and i post my portfolio here

This was supposed to “Fail safe ” Portfolio but now its “ Ticking Time Bomb ” given the nauseating valuation

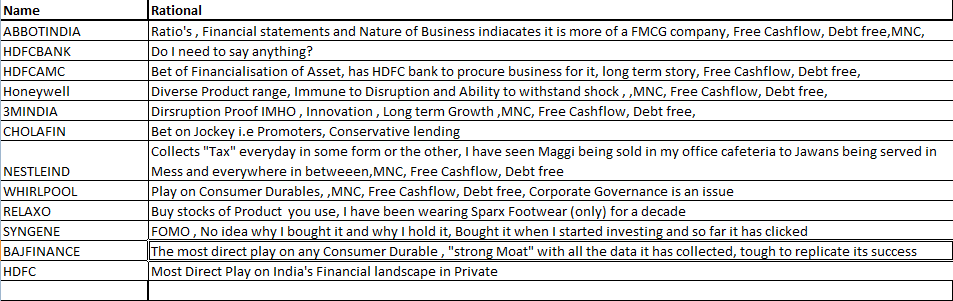

Rational

This portfolio i have started constructing in mid 2018 and have sipped from then on as i am salaried guy

A little about my investing journey, Like typical upstart i was fascinated by Warren Buffett and read all his books everything i could lay my hands on.

My First Picks (as you might have already guessed) were typical Low P/E and high dividend yield PSU stocks. I thought myself of true Graham disciple when i first bought REC below “Book Value “ (i was so excited that i thought i had the best bargain deal of the century.)

However one good thing emerged from it, i came out unscathed from Mid and Small Cap Meltdown as i didn’t have any of them in my Portfolio

Buy-and -Hold comes naturally to me and holding “Coffee can Portfolio“ suits me in temperament wise

The current Portfolio is still Work in Progress and i would like to add more stocks when the valuation froth in “Quality” stocks cools down

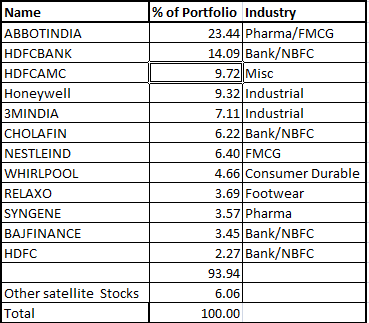

Common Theme across Portfolio is

My NAV on 1/1/2019 was 1000 and as of today i.e 27/10/2019 its 1243 implying 24.13%, In IRR terms it would have been even greater . The short term returns means nothing and it might be gone in one trading session . The Portfolio has been greatly aided by “Flight to Quality” and “Quality-at-any-Price” style currently in vogue. i had no foresight then and am lucky to be holding “Right” stocks in Bull market

Looking for your valuable feedback

Harsh