Sorry for late reply, Twin tragedies struck my family.

Sir , Appreciation coming from you means a lot for me. Its like a life long worshiper is being acknowledged by worshipped. I have “grown up” reading your portfolio thread multiple times. In fact one of my daily activities checklist is to read new discussion to your thread. What would have taken me and any rookie atleast 2 cycles and expensive Tuition fees to learn is served on platter by you. Now that you are there in this thread i have think 10 times more both while adding stocks to portfolio and when i write here and other threads. Nonetheless it motivates me further.

I would certainly add Divis lab to my collection when valuation froth cools down a bit .

Thanks for your appreciation. Hopefully ill live upto your expectation and yes i want be more contributing member to this forum.

I havent studied Pidilite , bandhan bank or Credit access Gramin so far. Pidilite has always been too expensive for my taste but someday i will make peace with it and finally buy it.

If you would like to read my thoughts on Banks and NBFCs in general , for whatever its worth then here it is.

I am generally averse to looking into Bank/NBFC in general for 2 reason, my inability to understand them completely and not holding the Accounting principles and Reporting in high regard.

The basic premise of preparation of Financial Statement for Banks and NBFC’s are not the best if not faulty. The Major head of revenue for this institution’s are “Interest Earned or Accrued” and not “Interest Received” Therein lies the catch . How much of "Interest Earned"comprises of Interest actually recieved and/or would be recieved is anybody’s guess. Yes Bank was very aggressive in accounting fees for loan advanced upfront.

Whats inside the books, whats the composition of loan book and whether the Loan book would stay performing matters more then the number’s. Banks and NBFC are purest proof where Return of capital is more important then Return on capital.

Of course RBI and other Regulatory bodies are tightening the grip with regards to Reporting. On Side note , Kotak bank avoids heavily leveraged and capital intensive sectors like Infra, Power and Airlines like plague. This explains the premium valuation and ability to stay clear of NPA mess

The RBI has more strict rules for Asset Reconstruction Companies which are not as levereged as Banks, and not of that"Public Interest", whats stopping it from applying the same rules for Bank’s and NBFC’s.

ARC can recognize profits only once its cost is realised and that too only on Cash received basis. No building of castles in air

Say a ARC buys a distressed asset for 100 rs, the first time it can recognize revenue is when it actually receives (major emphasis on receives) any money over and above 100 rs. If the same rule is applied to Lending institution then , on a loan of 100 rs given, the 1st revenue should be recognised only when 100 rs of loan is recovered and not embedding of Interest in to it. This would clear lot of Misreporting. This would have certainly halted theIL&FS , DHFL and Yes Bank fiascos

Overall in my limited wisdom, Investing in Bank’s and NBFC is ALL-or-Nothing game.

My own Portfolio consists of many names like HDFC Bank and Chola and Bajaj, where to be honest i have bet on Jockey’s and not Horse. its based more on faith(to be taken with pinch of salt) and Credit underwriting culture then on crunching numbers.

Next time when we meet, ill hopefully have more specific answer the general gyan

Indeed mature way of looking at finance stocks. Can u pls let us know since when you are holding your finance stocks like hdfc, hdfc bank, chola and Bajaj finance?

Also would really be great to know your thoughts on the risk profile and long term investment in insurance stocks like life and general and AMC companies.

Lastly, are these sectors better bets, risk reward bets than banks/NBFCs? Thanks

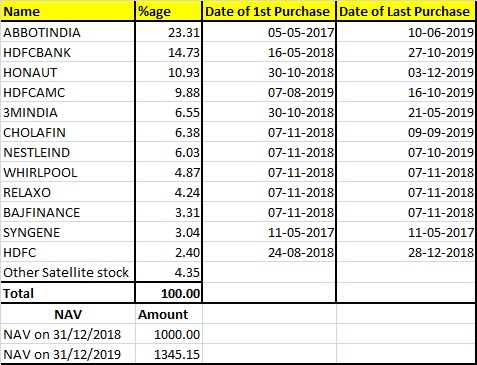

Please find the working below, i just made the working

As can be seen , i started constructing Coffee can Portfolio around Nov-2018. Before that i used to hold craps like Indiabulls Housing Finance , REC and PFC and Yes Bank in Banks and NBFC . I was lucky to come out without any bruises and Scars. I am adding HDFC Bank every few/alternate months and it just came out with great results yesterday. Maybe the Big-getting-Bigger theory is playing out in Financial Space.

I dont know much about Insurance companies , maybe that explains absence of Insurance Companies currently. But Insurance made Buffett and Berkshire what it is today, So it goes without saying that i am bullish on it. To compensate for my ignorance, I’d play Insurance theme with Holding Companies like HDFC , Bajaj Finserv or Chola Holding.

Now Comes the best part , AMC

As a Fund Accountant who computes Management Fees manually day in day out, I can tell you that Asset management is the best business in town. Perhaps that explains heavy weightage to HDFC AMC . I jumped after waiting endlessly for valuation to cool down.

Few things about AMC that makes it great holding-

1- Toll Bridge/Tax collecting Agency- The AMC imposes Asset Management “Tax” everyday regardless the investor makes money or not. Whether or not Inverstor makes money , AMC will always make money. I’d rather want to be Asset Manager then Investor.

2- Little Capital Stuck in Fixed Asset or Working Capital- AMC makes money hand over fist, Scaling up doesnt require much additional investment and management fees is deducted automatically so no recievables.

Overall the AMCs Belong to rare breed of Companies which focuses on core business , doesnt require much capital and continues to spit cash

Overall I am bullish on financial sector as a whole and for me it covers the Sub Sectors like Insurance and AMC because in my limited wisdom i believe Financialisation of Saving theme will play out (if already not playing out)

Now there are not many “Tax Collecting Agencies” (company which enjoys repeated purchases, doesnt require much capital to grow, Money received upfront, little money stuck in receivables/Inventory, Spits cash) other then FMCG, select Pharma companies (mostly India focused MNC’s) , Good Bank/NBFC and AMC and Tobbaco Companies . we have extremely limited number of them, and they are at Atrocious Valuation.

Sure, XIRR is superior to NAV, If i were to cherry pick the date from Nov 18 when i liquidated my old portfolio and bought the current one, then in IRR terms i will probably end at north of 50 % which will give me Swollen head. However Next time i will add IRR returns as well

I strongly beleive in the Maths of Coffee Can, but have few doubts:

Stock price return = ROCE%* Retention Ratio + P/E expansion (or contraction)

(1) In the above, most of the coffee can companies have ROCE% avg of 25% and retention ratio of around 50% over last few years (eg: Asian Paints, berger paints)…this makes the first part only 13%…

Second part is going to be negative in next ten years as current valuation is high…so suppose there is a fall of 7%…then the 10 years return is less than 10%…how do you cater for it?

(2) How many previous years avg is being taken to calclate the roce and ret ratio. Any other modicifcations to project the roce or ret ratio for next ten years?

(3) As the coffee can concept depends on companies retaining more money…that means dividend paying stocks are not good compounders? I am a bit confused in this part. So we should not be investing in companies distributing dividends?

Request if youll can clarify based on your concepts

Please find my responses below.

I am still learning the ropes of the trade and as such my answer has to be taken in that way

Let me combine your 1st and 3rd question

While I agree with your equation for stock price return , My suggestion would be to focus more on “Process” of buying good quality business at sensible valuation and not worry about Return

Without Sounding Preachy, its my firm belief and experience that if 1step (i.e buying part ) is done somewhat correctly and you are able to sit patiently then phenomenal returm will follow

I more then agree that the currently “Quality” and “Compounder” stocks are at nosebleeding valuation and I wont be buying Relaxo or likes at current Valuation. But there are still few Stocks like VST which are currentlly in buying range (for me)

2 Examples

1st Example

My uncle bought 7 or 8 stocks somewhere in late 90’s and just sat over it (and is still sitting over it). His annual dividend is many times more then the price he paid for Total investment and since then he hasn’t added or sold any stocks

2 Stocks of the Portfolio are HUL and Reliance and he still holds spinoffs like RCOM and likes

2nd Example

I know another senior person who has simple process. He applies for IPO , never bought shares from secondary market and never sold any of his shares. He has the Extremely rare ability to see his stocks going down to Zero and yet sticks to his guns

1 stock turned out to be Motherson Sumi. (both Motherson and Infosys IPO came at sametime and he didn’t have money for Infy) and dividends alone from Motherson every year is more then his total investment

ROCE and P/E (expansion or contraction) depends on lot of factor like business model, size of market, Management Competence and Integrity , Economy of Country etc etc , for P/E major driver apart from healthy ROCE and Free cashflow and Interest rate (my understanding). I dont spend much time on Future P/E multiple

Coming to 3rd question of Dividend paying stocks not being decent compounders.

1st - You need to flush out excess cash on books (i.e paying dividends) or the ROCE/ROE/ROA takes hit if cash is not employed in business.

2nd- What you do with retained earnings is more imortant then what you flush out. Ultimately it’s the Incremental ROCE on Retained earning that will decide investment returns.

ITC deploys its retained earning suboptimally while VST pays them out and keep things simple and the difference in their returns over a period is quite visible. In addition Companies like HDFC bank have a policy of paying 20-25% of earnings every year

Both VST and HDFC Bank have been terrific compounders , the market cap has grown 15X and has dividend yield greater then that of FD’s

Have followed your posts on this thread for a while, and it helped a lot with understanding about some of the companies which I also have in common.

Wanted to check what are your plans in the current scenario, in terms of what prices you are looking to add on to current positions or if you have already added at some price points.

Just would like to add here that in 90’s, the IPO pricing was controlled by CCI and it used to be very conservative.Now a days most of the groups with the exception of <10% , price the issue keeping the next few years earning potential in price.To give an example ,one of the airlines even held suppliers payment and distributed huge dividends to shareholders pre IPO and the issue was debated by the media channels.

Therefore the situation of 1990 is quite different from the current one.

I just graduated from Class of 2020 (read Crash of 2020) and please find my scorecard below.

I always used to ask Senior Investors what 2008 was like and they would say no amount of reading books and articles would help as much as navigating through one. They say experience is best Teacher

Few learnings/observation from COVID-19 Crash

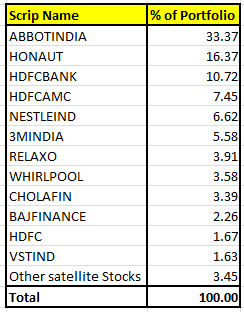

1- Portfolio becoming like Classic Coffee Can where 1 or 2 position dominate major part of portfolio and loser becoming lesser and lesser to the point of Immaterial, Abbott and Honeywell forms major part while Chola and Bajaj Finance and HDFC have been reduced to nothing.

2- Financials should be restricted to 15-20 % of Portfolio, they amplify results both way. Chola and Bajaj I think will become insignificant unless i add them

3- I’d be lying if i say that that i had lower volatility/beta in my mind while constructing the portfolio, it just happened . The fall has been less sharper then that of Index while recovery has been faster then that of Index. I am not taking credit for it , just am thankful for it.

4- Focus on Debt free companies which throws growing Free CashFlow, you understand their importance in times like this. The Price destruction is contained and is not that severe…

5- Psychologically It really helps to have 1 or 2 stock firing in a portfolio, it gives courage to hold on other Stocks and not to Jump off the ship . Abbott and Nestle hitting All Time High evens out the Chola and Bajaj Finance losing half of their Market cap in no time

Thanks for checking out ,here is my activity update

1- Didnt sell single share throughout. (dont know if i am being crazy or smart, only time will tell)

2- Added Honeywell Automation, Started nibbling VST Industries and bit of ITC as dividend play

3- Want to add Honeywell more and more.

True that. I think you are referring to Indigo Airlines

Also many dont know that the Listed MNC’s were forced to list by Goverment with twin objectives of Sharing of wealth with Indians and prevent flow of all the money outside as dividend (they had adverse impact on Foreign Exchange Price and Reserves ). Coca Cola and IBM had left India then because Coke didnt want to share secret syrup formula with company over which they might not have control. Now we dont have that rule and hence no new MNC company is getting listed.

Like you said the situation of 90’s is different from current one

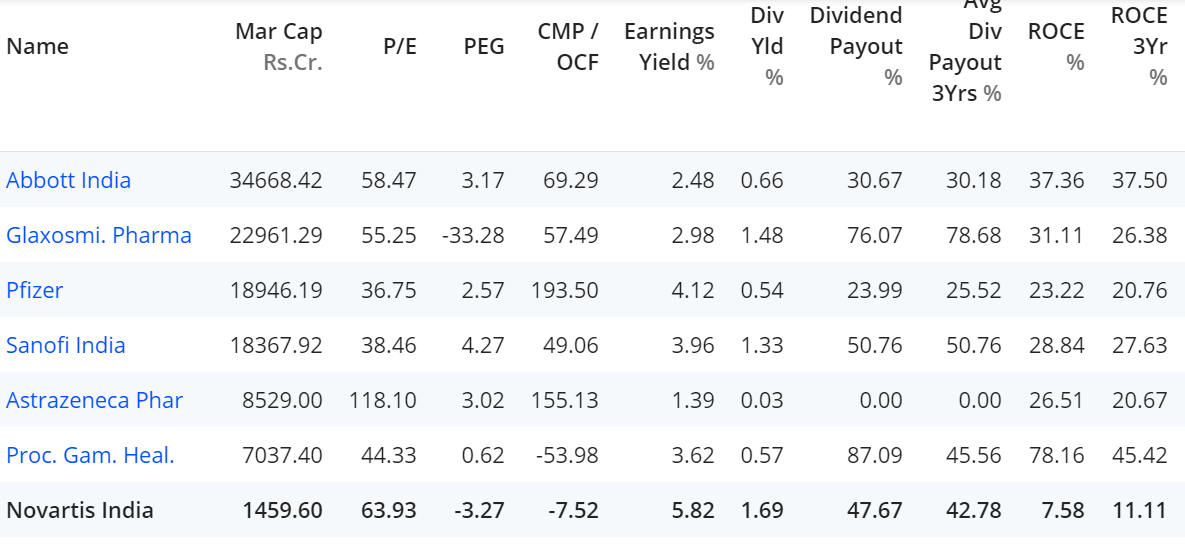

I have enjoyed the discussions here. Could someone explain to me why are we paying so much for Abbotindia (PE 58.47; for fair comparison only 1.5% revenue is from outside India, and the remaining 98.5% from India) when the domestic market share is so small?

MNC’c in general have higher PE for perceived better Corporate Governance. (In reality Unlisted subsidiaries and related party transactions and transfer of better business/products to Unlisted subsidiary and persistent efforts to delist prove it otherwise)

Coming to Pharma MNC’s , They trade at siginificant premium for following reasons

1- Mostly they are Trading/marketing agent(i.e they get product manufactured from other companies and sell it under their brand name ) and hence Fixed Asset Light

2- Brand Leader in their segment and Pricing Power ( Major risk is pricing control by Government as they did in stents)

3- Better Distribution network

4- Liquid Balance Sheet stuffed with cash and Debt Free

5- Better Operating Margin then Indian Peers

6-Since they are India focused , they don’t have the FDA risk and Indian firms selling in US market have presence in Generic drugs which are very price competitive

These are broad points and actual reality might be different from my understanding because I don’t know much about Pharma and most of the things

Coming to Abbott , its different beast altogether

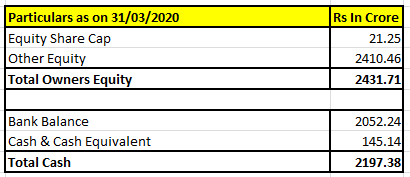

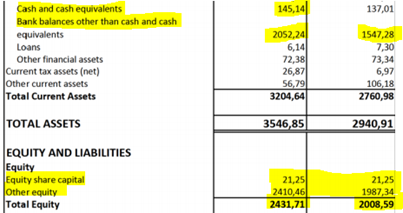

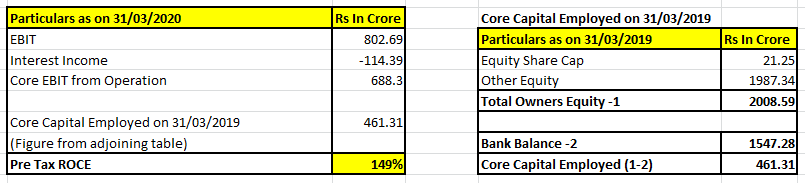

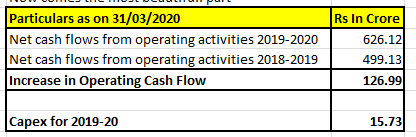

Few Interesting Points from 31/03/2020 results

If you see then almost all of Owner’s Equity is held in Raw Cash.Theoretically if Abbott wants to pay off the Equity Share holder on what it owes to them on books then it actually can and yet the business will continue spitting cash forever.

Extract from Results for attesting my workings

Abbott just declared Rs 250/share as dividend ( the Declaration of special dividend was mostly due to change in Tax Laws where it’s the recepient who is liable to pay tax on Dividend

Hi Harsh,

I am trying to understand your analysis ,though I am not v conversant with balance sheets. Company is keeping such a huge amount as bank balance and not using it productively.Is it not negative in long term?

Not sure since when you would be holding Abbott, but I am amused by fact that many investors, including myself, have realized the prowess of this beast in last 2-3 years or so. I am bit curious why is that so? Is it because of domestic pharma facing FDA issue or overall market paying for quality or Abbott doing some things right which it was not doing earlier or just that these investors following price action (What goes up and has been going up is a beast as long as it is going up) - Pls note nothing against your thoughts, I am also attracted to Abbott since couple years though have not managed an entry yet. I also do not like the fact that they have unlisted entity with which they have many attractive products in market.

Now regarding Honeywell, can you mention why are you so upbeat that you want to further increase allocation when you have significant already? I am aware some investors had concerns on sister unlisted companies of Honeywell.

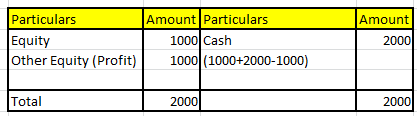

Say you are a Commission Agent for a particular Commodity. In morning you have 1000 rs in your wallet for business

your Balance Sheet will be

You receive a call from buyer asking for price of commodity . You ask him for 5 minutes to get back to him.you call seller and he quotes 1000 rs and you call your buyer and quote him 2000 Rs. The deal is agreed.Buyer deposits 2000 rs via Google pay and you deposit 1000 to seller

Your balance sheet will look like

Now at the end of the day , your Capital of 2000 rs (starting capital of 1000 rs and Profit of 1000 rs ) is not tied/stuck anywhere . You can withdraw if you want without affecting your business next day

Abbott Balance sheet is one such. Its Liquid

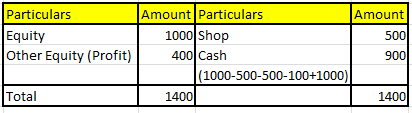

Lets say you are into Manufacturing, your starting capital is 1000 Rs , invest 500 rs in Shop , get goods worth 500 rs and process them for 100 and sell them for 1000 rs

Your Balance sheet will look like

At the end of the day, there is little amount of cash you can pull out because 500 rs is stuck in shop and other you need to carry out business next day.Manufacturing company like steel and Textile etc come in these category

Coming to your question

There is only so much of Amount of money you can invest in business. If it continues spitting cash without major capital reinvestment then its sign of great business.

Abbott has been prudent and has not engaged in Unnecessary diversification so far and hasn’t let lent it to related party. I am happy if it doesn’t pay dividend and keeps it in FD as it is.

Abbott has around 1000 rs / Share as cash outstanding

Consider 2 scenario

If It doesn’t pay dividend

At 6% Interest in FD , the money in Abbots books will be 1060 at the end of the year

If It pays Dividend

In earlier Tax regime of 18% DDT or current Tax regime at depending slab rate, lets say 20 %, I get 800 rs and for me to reach 1060 I have to earn around around 32% return (which is impossible and Revenue leakage to Government is biggest enemy of compounding)