Harita Seating is a TVS Group company and is the leading manufacturer of seating systems in India. Harita specialises in manufacture & supply of safe, ergonomic and reliable driver seats and bus passenger seats. Harita seats are used in the automotive segments of: Commercial vehicles, Tractors, Off-road vehicles and Buses. Company has 5 Plants: Hosur (Tamil Nadu), Chennai (TN), Ranjangaon (MH), Dhadwad (KTK), Pantnagar (Uttarakhand). Harita has a subsidiary company (51% share of Harita Seating), Harita Fehrer Limited (HFRL) which is a joint venture between Harita Seating Systems Limited , and F.S Fehrer Automotive GmbH , one of the market leaders in automotive foam business in Germany, Europe. Company has a good client base and supplies to almost all the major players in the industry.

HFRL is a material un-listed Indian subsidiary. During the year, HFRL achieved a turnover of Rs. 506.37 cr and PAT of Rs.23.45 Cr. HFRL contribute majorly to the consolidated revenue and profits. JV was formed in 2009 and in 2010 Harita Seating transferred it’s the two wheeler seats, Long Fibre Injection (LFI) & Micro Cellular Urethane (MCU) products and the foaming businesses to HFRL for a sale consideration of Rs. 46.50 Cr which was settled partly by way of allotment of 1,02,00,000 equity shares of Rs.10/- each at a premium of Rs.17/- per share amounting to Rs.27.54 Cr in the equity capital of HFRL and the balance consideration of Rs.18.96 Cr by way of cash, both aggregating to Rs.46.50 Cr. HFRL allotted 68,33,364 equity shares of Rs.10/- each for cash at a price of Rs.101.54 per share (including a premium of Rs.91.54 per share) aggregating to Rs.69.39 Cr to its foreign collaborators, namely Fehrer on 8th February 2010.

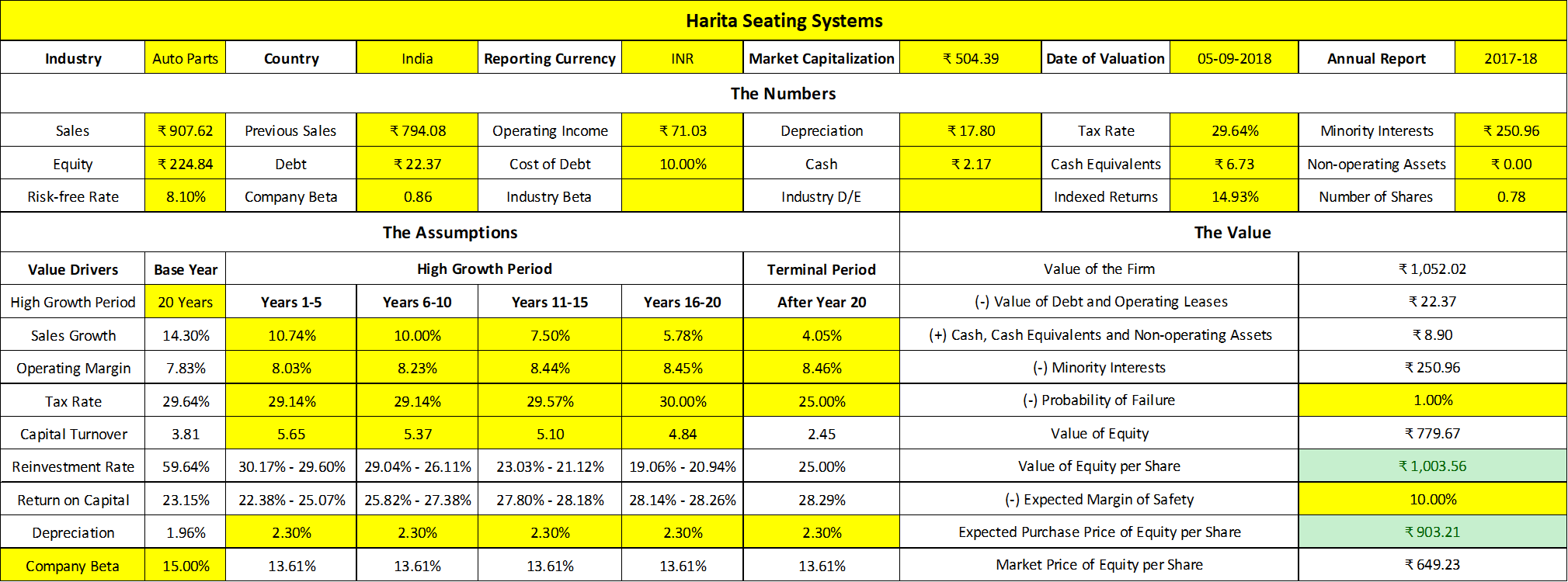

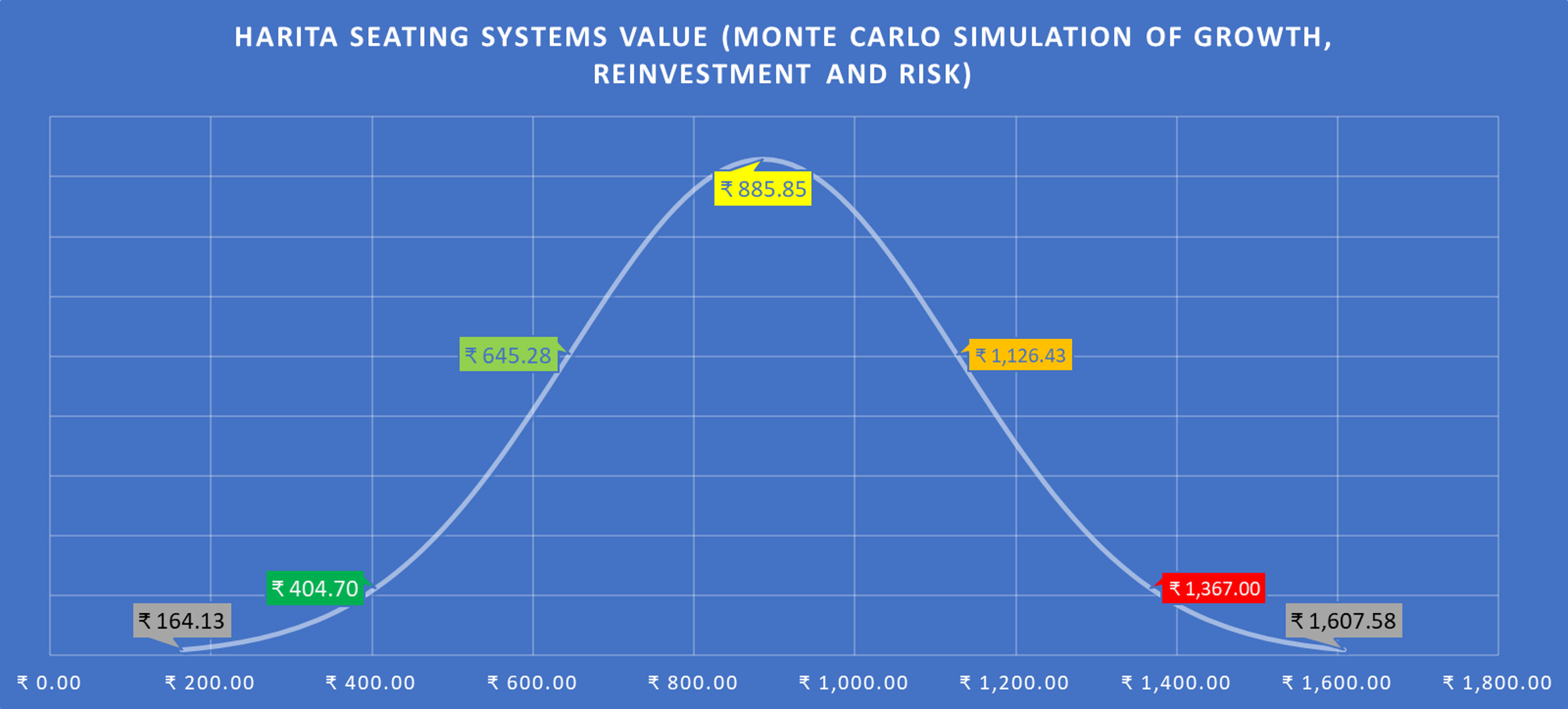

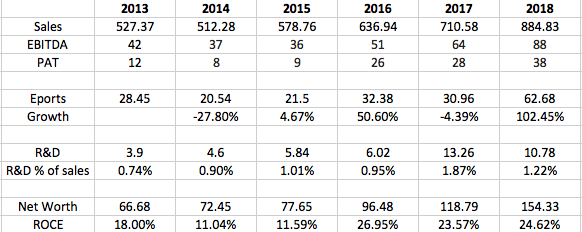

Financials & Valuation

During FY18, the Company posted a growth of 26% in overall sales. Company’s sales grew in the commercial vehicle segment and in the bus passenger seats better than the market growth. From 2013 to 2018 Sales have grown at 10.90% cagr, EBITDA growth at 15.94% and Net Profit at 25.93% cagr. At CMP of Rs. 640 company has a Market Cap of Rs. 510 cr and Enterprise Value (EV) of Rs. 525 cr. On the basis of FY18 numbers company is available at PE of 13.42 times and EV/EBITDA of 8.46 times which is quite reasonable in comparison to other auto ancillary companies.

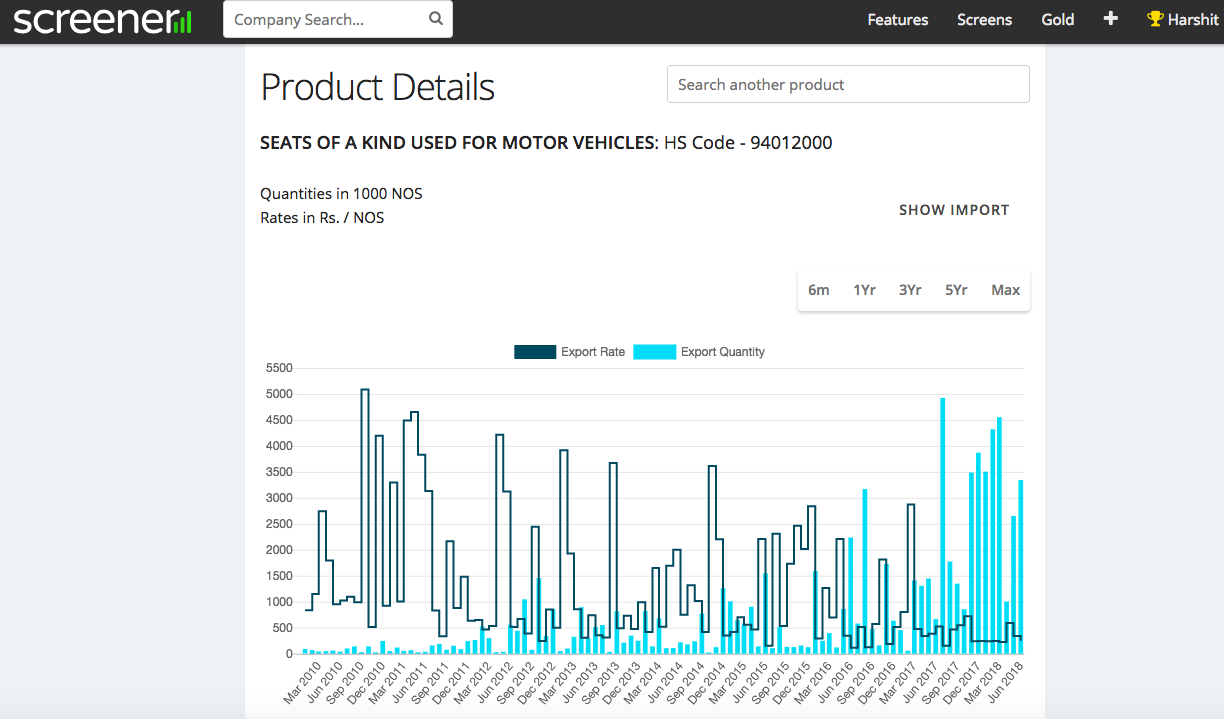

Company has seen good growth in exports in recent times and it is hopeful of continuing this growth in the future. Export sales grew by 105% in current products and new products customers. The Company has been continuing its efforts to increase the current volume of export of tractor seats to USA and Germany.The Company continues to strengthen its position in export markets and has won significant new orders from overseas customer. The supplies are scheduled in 2018-19. In the case of domestic tractor segment, the Company catered to the existing base of customers and experienced 32% growth. What’s also impressive to see is the company’s increasing expenditure on R&D from Rs. 3.9 cr in FY13 to Rs. 10.78 cr in FY18.

Company has done capex of Rs. 75 cr in the past two years which is quite substantial in context of the company’s total assets. This will help in maintaining the current sales growth in the near future. Company’s ROCE has improved substantially in the past 3 years. Increased capex and improved ROCE are very good signs.

Risks

- Chairman of the company is Mr. H Lakshmanan and he is 85 years old, so succession risk is there. This risk is mitigated by the fact that the company belongs to the TVS Group and also in FY15 company appointed a full time CEO, Mr. A. G. Giridharan is the CEO of the company since 2015.

- Company’s performance is dependent on the automotive sector, it’s cyclical in that sense. Company suffered losses after the economic meltdown in 2008 and took considerable time to recover.

Few Important Questions.

- What is the market size? Who are the other players in the market?

- Capacity of Harita Seating in various segments?

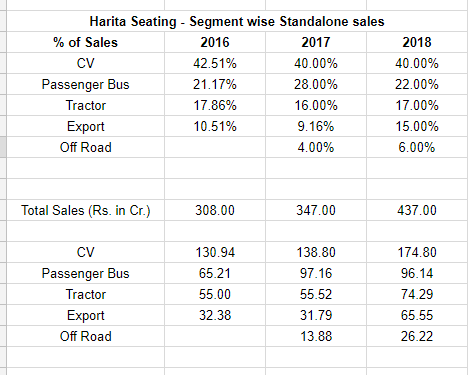

- Segment wise sale in Passenger Bus Segment, Driving Seats, Two Wheelers and Tractor segment?

- Nature of sale contracts company does. Are these long term supply contracts or Order based?

Regards

Harshit

Disclosure: Invested (Invested in last one month)