Your analysis of Harita seating is very informative and insightful.Can the information in attached article be incorporated in your analysis and find a more accurate price for the stock.

That’s a very good article, Amit. This will probably be useful for someone trying to use a Multiples Valuation method. I don’t see how it can be used in an Intrinsic Value method.

Thanks for your appreciation. Your analysis made me look into Hartia seating more carefully. You seem to follow Benjamin’s graham margin of safety in both letter and spirit. However,regarding Harita seating I came across an article that said the fall in price is mainly due to SEBI’s guidelines on P-Notes by Indians based abroad. Once I get hold of that article I will share it here. Also,I feel that since we do not life in a perfect world,some give and take on the margin of safety may be there…

what is you r call on that? is it ±5% or +=10%…that makes quite a lot of difference.

We don’t and it’s not that easy, even in real life. Say, you’d like to buy groceries for the week. You already know how much you’ll consume every day. But don’t you always end up buying a little extra, “just in case”? The truth is, we apply Margin of Safety to several things in life unwittingly. So it only makes sense to apply it to investing as well.

Of course, there could be leniency. For instance, I personally use a baseline MoS of 30%. But if it’s a company with a long history of good cash flows and if I understand the source of those cash flows I might demand only 20% by way of a MoS. But I’ve never gone below 20%. If I cheat myself into thinking “18% is fine”, soon enough, I’d be willing to let go of MoS entirely, which is not a place I’d like to get to. Alternatively, if I feel like the cash flows are fickle and I only have a basic understanding of the source of cash flows, I will demand upwards of 40% by way of MoS.

Warren Buffet put it more eloquently than me:

“If you understood a business perfectly and the future of the business, you would need very little in the way of a margin of safety. So, the more vulnerable the business is, assuming you still want to invest in it, the larger margin of safety you’d need. If you’re driving a truck across a bridge that says it holds 10,000 pounds and you’ve got a 9,800 pound vehicle, if the bridge is 6 inches above the crevice it covers, you may feel okay; but if it’s over the Grand Canyon, you may feel you want a little larger margin of safety.”

Hello @dineshssairam, exception analysis as always. I have few queries on this valulation analysis,

Why did you consider cost of Debt as 9%, isnt it very low? I tried to compute the cost of Debt and I found it to be very low too. Is there a specific reason?

I was analyzing the commercial vehcile sale vs the growth of this company YoY - not using CAGR. I found that since the industry is cyclical , Harita sales also has its ups and downs. Is there a way to factor such cyclical changes in your model? By logic, average growth expectation should take care of such cyclical perfromance, however I am not sure of the impact if its aproven fact. Do you have some inputs?

The Cost of Debt used in the model isn’t the Book Cost of Debt (Interest Expenses / Total Debt). It’s the Market Cost of Debt. The ideal practice is to find a few companies with the same Credit Risk as Harita and then see what the yields are on their Corporate Debts. Unfortunately, India’s Corporate Debt Market is still at a very nascent stage. So we’ll have to settle for an approximation. AAA Rate Corporate Debt is trading at 8.5% in the Indian markets today (Refer to NSE Bond Trading Data). Considering Haritha’s Credit Rating at A+ and a very strong parent in TVS, I judged it to have a 9% Cost of Debt. Regarding your question about the Book Cost of Debt being so low, I would again guess it has something to do with TVS being the promoter. Having a parent with high credit rating helps the subsidiaries as well with their loans.

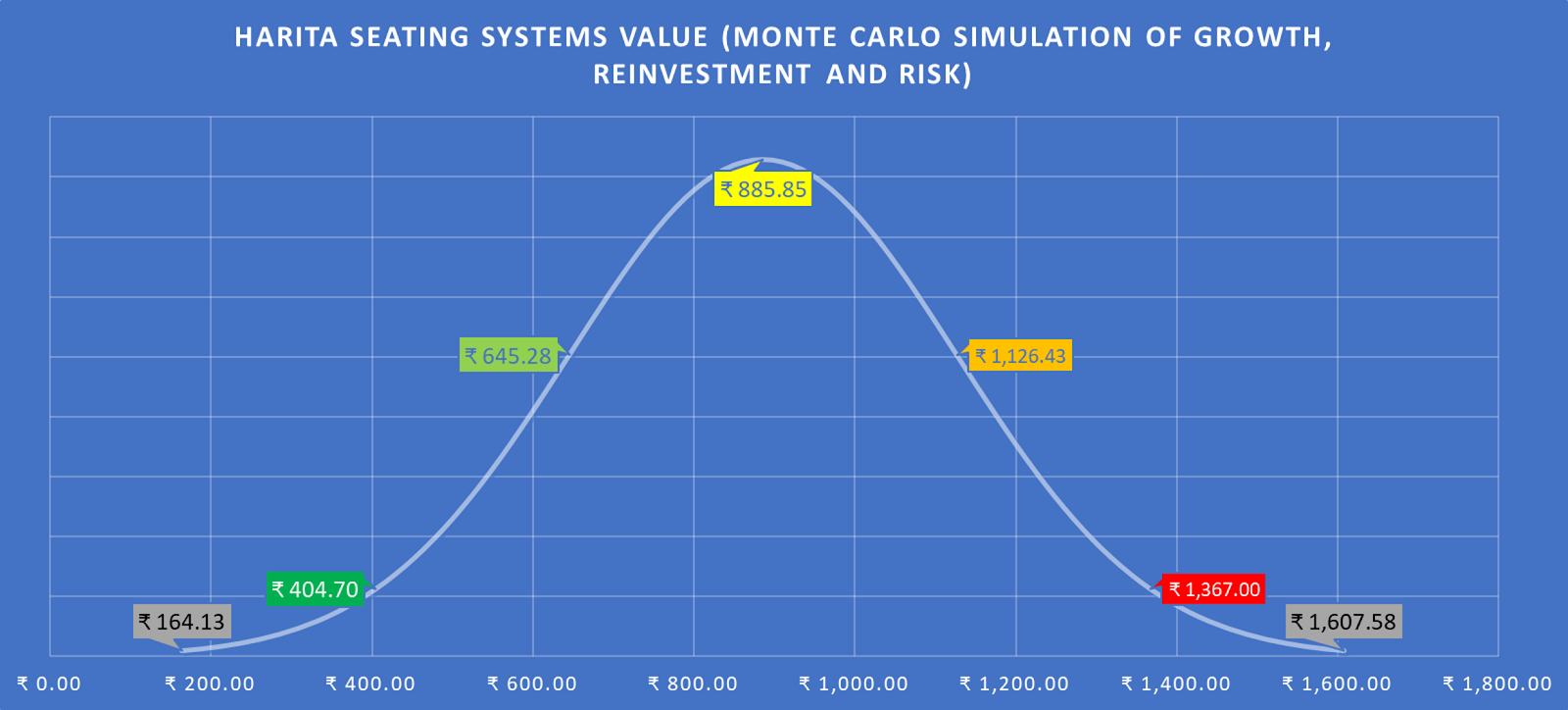

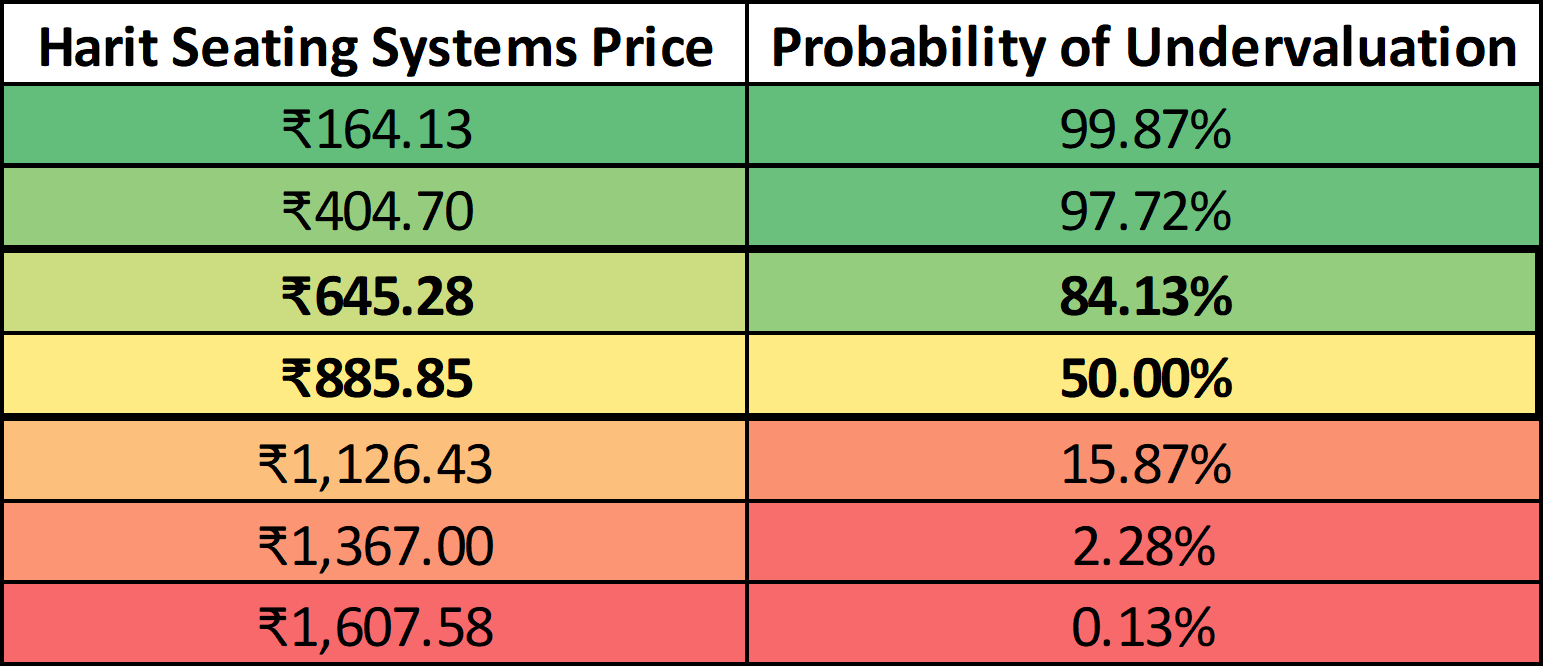

If you have insights into the industry, you may try to increase and decrease Sales Growth / Margins as required. But in my opinion, these things are impossible to do accurately. Remember, all we’re doing in a Valuation is an attempt at approximation, not an attempt at accurate calculation. In fact, the tendency for assumptions to be inaccurate is why I always perform a “stress test” of sorts and represent the value of a company as a range of probabilities (Of course, value is always a range of probabilities. If someone says he’s 100% sure a stock is valued at X, feel free to consider him crazy). Here are the results from my blog for Harita:

Just making a note. Harita’s local business is kind of weak. Their export unit based on Chennai is the strongest one. So take Standalone results with a pinch of salt.

One negative, a noteworthy one, I see in Harita Seating is that, its Debtor days are high; now crossing 100. and increasing every year. Combining this fact with OPM % as low as 7, paints a dull picture.

A good business with some kind of moat, must at least have the power to get their customers to pay-up, preferably advance. Why should the customer have the supplier bear its working capital requirement! and more importantly why should the supplier agree? To keep the sales graph pointing northward? Does it not have a market otherwise?

Somewhat better would be, if the supplier must give handsome credit, then at least it should be in a position to extract a hefty margin. If the supplier cannot do both, then where is the moat.

Harita is one such candidate, with high debtor days and low OPM.

The debtor days are increasing with each passing year. Jumped to 104 in 2018, where it was 66 in 2016. Bad times are likely to continue for next couple of more years.

@dineshssairam

pls shed some light. tia.

A question. From the company’s AR, how do I find out if the management has faced non-payment of receivables. Bad-debts.

1st - Reduce Account Receivables with the amount of bad debt from Asset side of the balance-sheet.

2nd - Treat bad debt amount as expense and reduce your profit in P&L statement. Generally, you will find bad debt under heading “other expenses” in P&L.

Things become little complex if the provision for bad debt was made before. In that case you reduce the provision without impacting P&L.

It would be important to find out, the exact entities who are owing payments. What are the chances of them shutting shop, would result in a loss for Harita. The AR does not give those details.

Only in the AR of 2018-19, will be know if this 180 days limit is crossed.

Regarding the merger of Harita Seating with Minda Inds, the board of directors of Harita Seating have approved the following exchange ratio.

Share exchange ratio to the shareholders of the Company

Option - 1

152 (One Hundred and Fifty Two) fully paid equity shares of INR 2/- (Rupees two) each of Transferee Company for every 100 ( One Hundred) fully paid up equity share(s) of INR 10/— (Rupees ten) each held in the Company by the Eligible Members; OR

Option - 2

4 (Four) fully paid up 0.01% NonConvertible Redeemable Preference Shares of INR 100 (Rupees hundred) each at price of INR 121.25/— per NonConvertible Redeemable Preference Share of Transferee Company with a yield of 7.5% per annum on the issued price, for every 1 (One) fully paid equity share of INR 10/— (Rupees ten) held in the Company by the Eligible Members.

Would be glad if someone could explain how option 2 would work and how it compares to option 1. In short, should we choose option 1 or option 2?

by choosing option 1 ur return wud depend on d performance of minda industries. By choosing option 2 u would get a return of 7.5% per annum. Which option to choose depends on ur risk appetite and ur return expectations

Option 2 is effectively a deferred cash option, where Minda (acquirer) pays the Harita shareholder 4 X 121.25 = Rs 485 per share worth of zero-coupon debt, which is effectively worth 4 X 100 = Rs 400 today. The present value of the zero coupon paper is at a steep discount to the market value at time of announcement and hence the crash in stock price. Option 2 is a sub optimal option all around - if somebody wants cash upfront, they are better selling off in the market (and harvest some capital losses simultaneously as tax shields in all probability). If they believe in the Minda story, swapping into Minda shares with option 1 makes sense. Option 2 is for the miniscule minority who think that lending to Minda at 7.5% pa (less than most bank FDs) makes sense for them.

Option 1 is fractionally more attractive as at least as of date the 1.52x Minda shares are valued at Rs 422 (higher than HSSL CMP post announcement)

Caveat: lets wait for the formal shareholder communication as the press release is not sufficiently clear.

Let me vent here that I am very disappointed at the governance and communication here. EVen today, there is no IR / communication on the Company website. There is no attempt to explain rationale for transaction or to demonstrate to minority investors that they have not been shortchanged by giving the favourable swap ratios to the 4 unlisted promoter entities also involved in the transaction. SO much for all the hype about governance and transparency in TVS Group. I will not be surprised if other listed group companies suffer a governance discount in valuations if this sorry state of affairs persists.

Disclosure: hold the stock - deeply out of the money (and deeply unhappy)!

Can anything be done to stop the merger at this ratio ?

Can the report of the independent valuer be challenged ?

I believe HSSL has a far deeper value then it is being shown.

Moreover, it seems the OPM margins has been purposely brought down by the management from 12% in Q4 FY 17-18 to mere 5% in FY 18-19, just to bring down the valuations.

Apologies Kushal, don’t have an answer to your question. I do completely agree that HSSL was a deep value play and that is why I was holding it despite recent bad quarters (all standalone BTW; consol picture which they do not report quarterly may have been much better).

My understanding is that this transaction will require only a special resolution, ie., approval of 74% of shareholders present and voting. If this had been a related party transaction, then a majority of the non-promoter votes would have been required for the transaction to go ahead. We will have to wait and see what the formal shareholder communication says.

If the swap ratios for 100% promoter owned companies are significantly more favourable to Promoters, then there may be a case to seek SEBI intervention. I am hoping to check on this when formal papers become available.

Any idea how to get a copy of the independent valuation report?

HSSL is in an almost perfect duopoly with Bharat Seats. They have good systems built around them and have a marquee list of customers to service. While Minda might have its own capabilities, I don’t think the merger will create any additional value to anyone, except let the shareholders of HSSL get muddled up in the larger Auto Parts industry, which is decidedly more competitive. The only logical explanation I can think of is perhaps the parent, TVS Group, needs more funds to fight for survival in the Two-wheeler space.

But of course, these are just baseline views. I haven’t done any deep dive into this. So, take my views with a pinch of salt.