This is an unrelated venture to its core business or am I missing the link?

Seems co is venturing into renewable energy space. I am assuming so looking at the earlier announcement of the renewable energy order and the below announcement of amendment of company association.

However it is very surprising move given that:

1/ Company has never talked earlier about this plan.

2/ Co had unfulfilled vision with the existing steel/pipes business, where they have lot to do.

3/ Co do not have / may not have required expertise and mature plan in renewable business where the space is quite crowded.

Not sure what is company trying to do overall and seems to be going in all directions without proper investor comms / plan.

Looks like the scrip is getting rerated due to this kind of quality of management.

Can guys / @SwapanBansal who has done study of this business throw some light?

To be honest; Even I was confused when I seen those press release. Rather than focusing on their core business they are diversifying to unrelated areas like Renewables and telling it their growth strategy…

Last call also they hadn’t guided anything about such shift… will wait for Q4 Results & management commentry about same

Can’t say whether this is good or bad without management commentry… but this sudden shift is concerning as they had aspiration plan in Pipe Business.

No Reco; Invested, Biased & Holding

Renewable is an entire different business and is not related to pipes in the slightest way

They should focus on pipes by forward/backward integrating and growing that business as big as they can and then diversify

As a shareholder i can simply buy a renewable energy company and diversify my portfolio

Why do i need a management that has zero experience in an already competitive field

Looks like a future CG issue is on the cards

The latest move by the company to RE sector appears to be a red flag. Though details of expansion is not shared by the company. I am not an expert on RE sector. So only experts can throw light. It is also surprising to see order wins. How can a company without any expertise/ prior experience can win orders from Govt Sector?

Whatever may be the fact, seeing the cutthroat competition in RE sector, I am not willing to back the company for success. I am certain that like it happened in telecom sectors, many companies in RE sector will bite the dust. Are we not aware of RCOM episode?

I am also sort of amused, about this venture , since they never communicated or hinted such aspect. That’s the problem.

However , I won’t see it as a redflag, unless it’s not hurting the company"s OPM or botomline.

If the move is revenue accrual and contributes to the numbers, I don’t see the venture a problem, since they are into pipes, they might already have some input raw material manufacturing capabilities inhouse, like panel mounting structures etc.

P.S: I could be wrong, and biased, since holding.

Latest Investor Presentation:

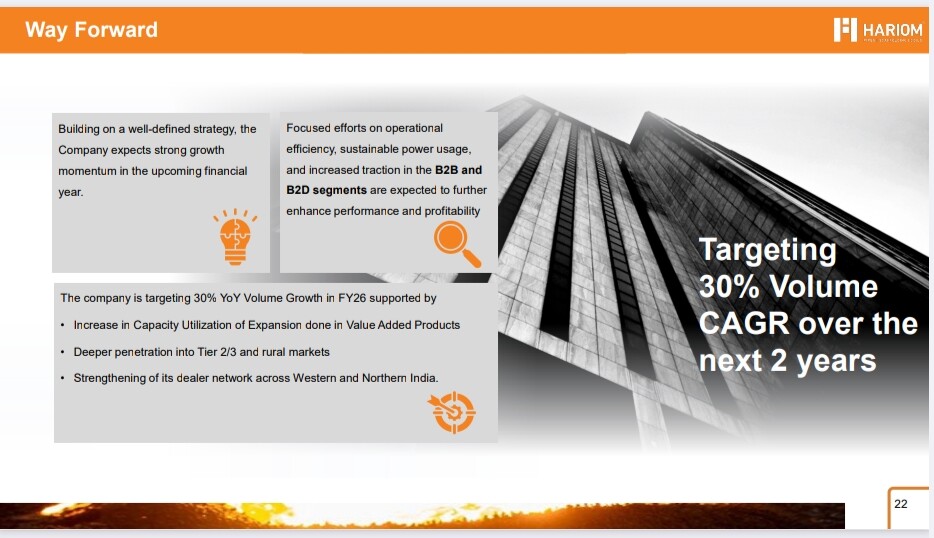

50% Growth has been lowered to 30%

Now Hariom is targeting 30% Volume Growth for Next 2 years (this can be achievable, but management failed to achieve last Target. So take this guidance also with pinch of salt)

Growth will be achieve through

- Strengthening of Dealer network

- Expansion in VAP Products

- Penetrating more in Tier 1/2 markets

If they can achieve 30% this time then their would be lot of value today, but again take this guidance with pinch of salt & don’t blindly follow management

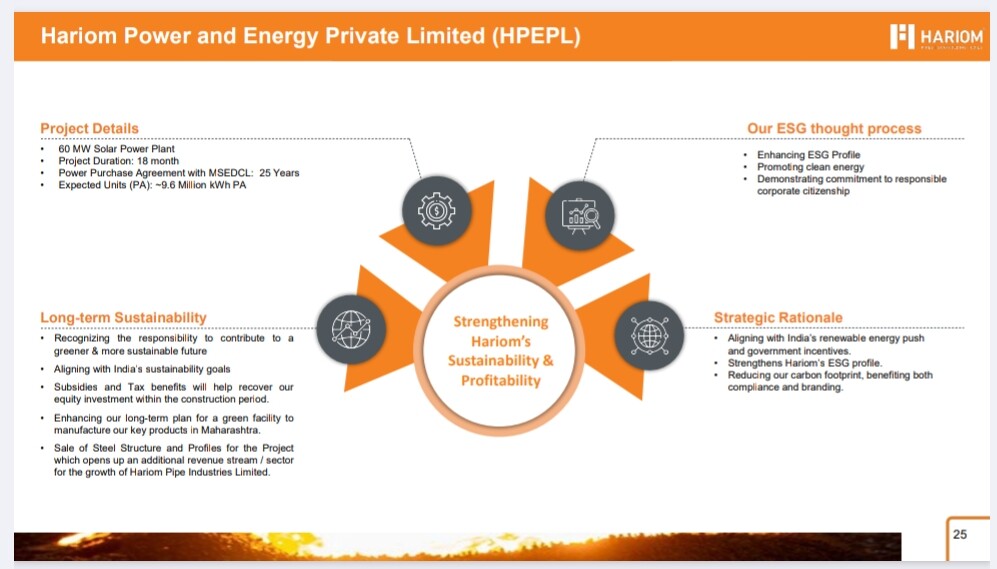

On Hariom entering Renewable space:

Might be this is done to further lowering the Power cost + for enhancing ESG profile (can be wrong but Next call can only answer this)

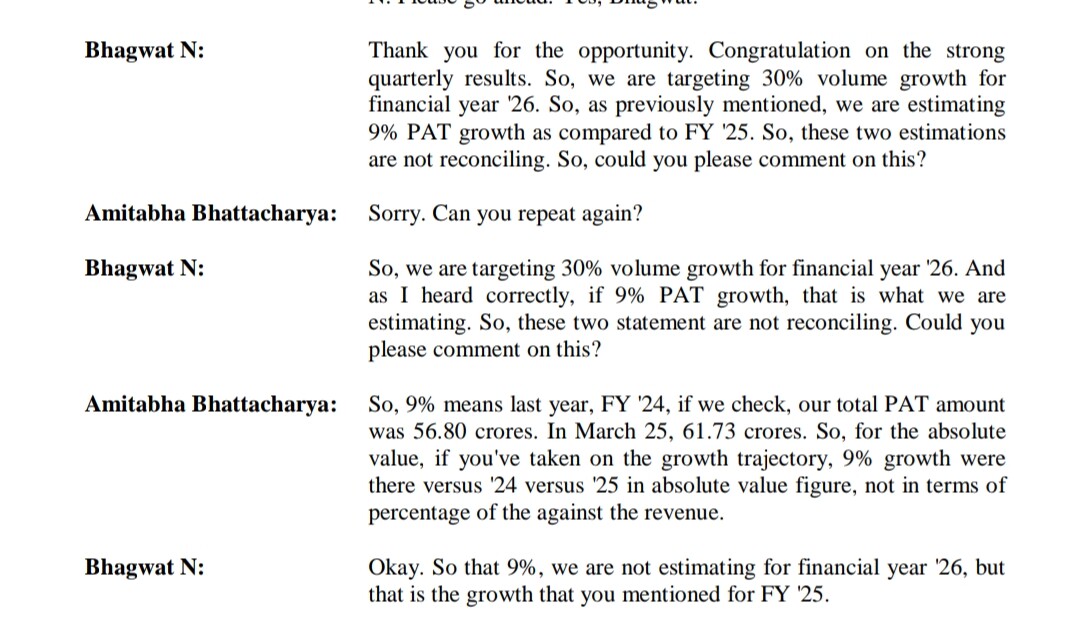

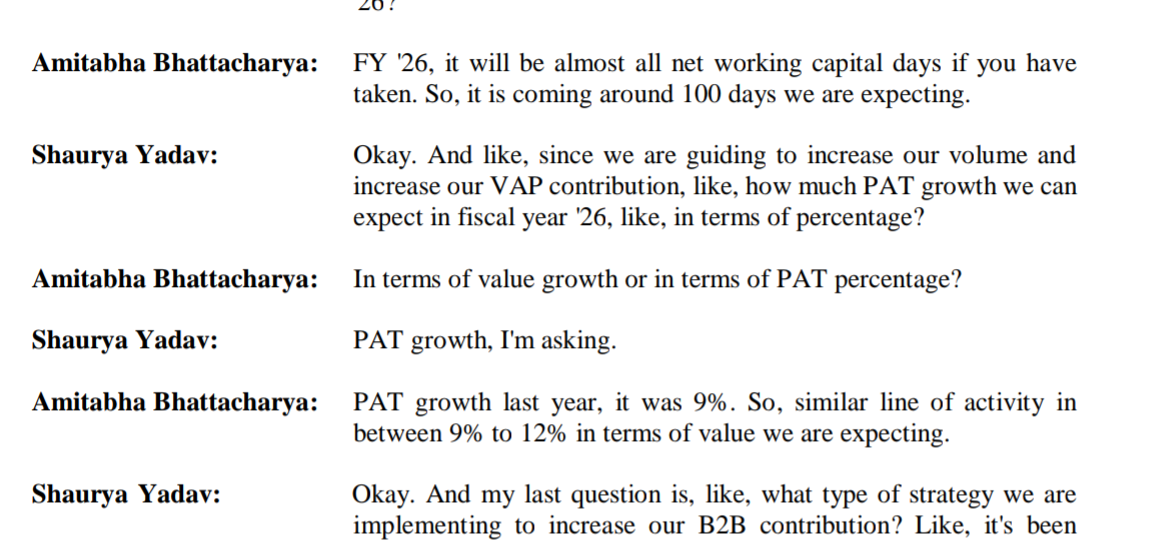

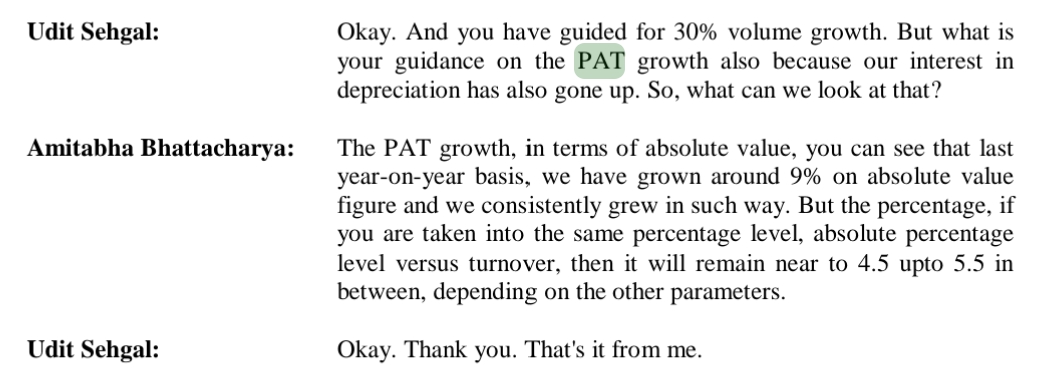

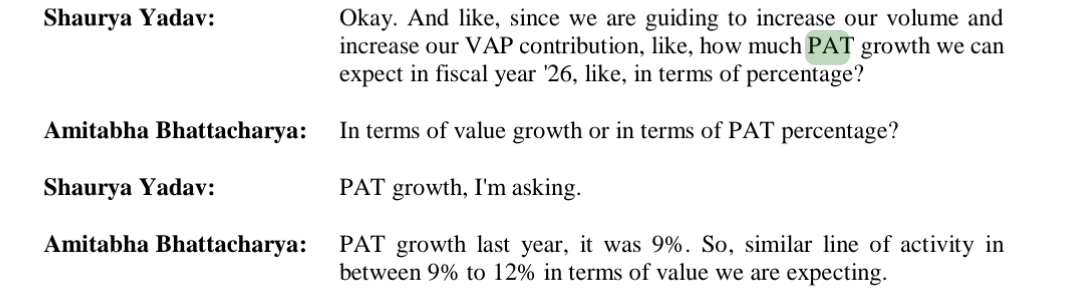

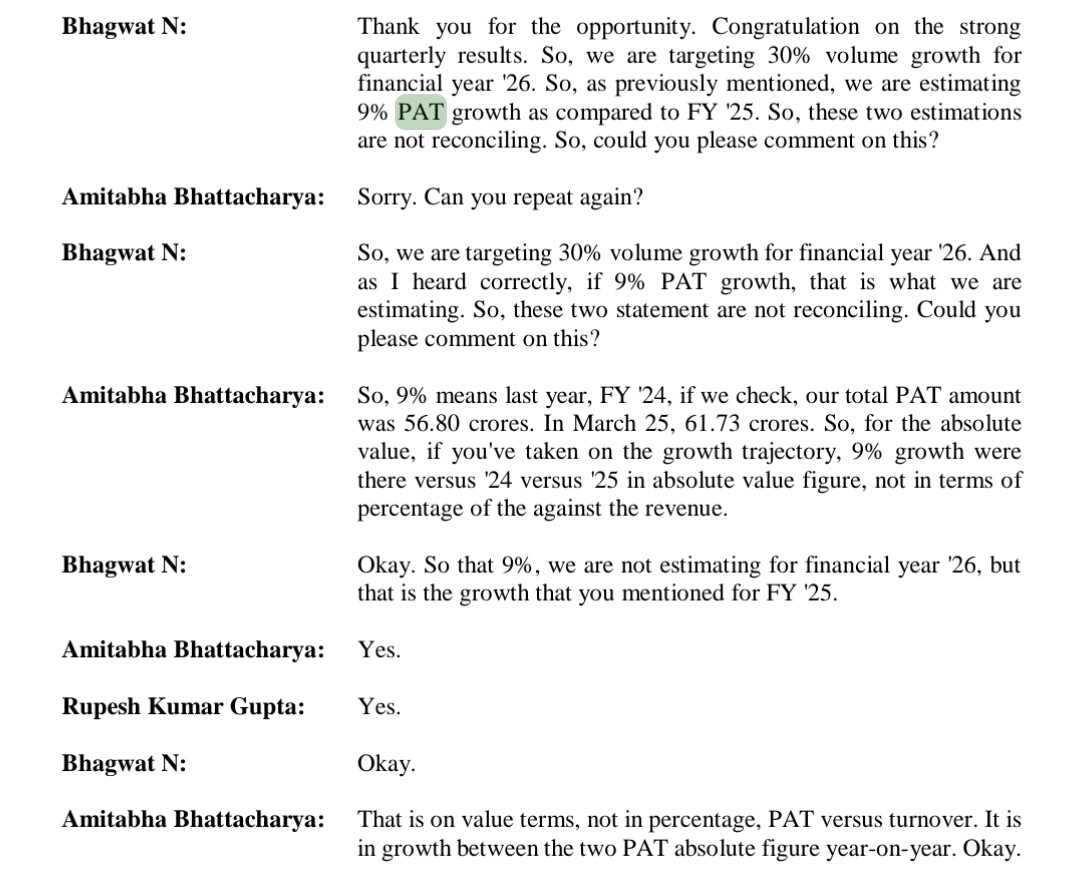

Why are they projecting 9-12% of PAT growth eventhough targeting 30% volume growth? I have gone through concall, the answer I couldn’t understand..

I see there is still the confusion.

- Volume growth for FY-25 vs 24 is 30%

- Revenue growth is around 20%

- PAT growth is around 9%

Now the disconnect is between volume growth being hight while pat growth being low, understandingly due to price correction in steel prices.

But they are stating if they grow volumes in same line, they will achieve around 9% pat growth.

I still don’t understand what are they guiding for volume growth, revenue growth and pat growth for FY27?

As per Q3 concall 10% of revenue was from Coils and ORs, as per q4 ppt 31KMT was coil and ORs production out a capacity of 180KMTPA, means only 17.2% capacity utilisation. It is not backward integrated hence realisation is less compared to MS Tubes.. So even though vol increases by 30%, revenue and EBIDTA may not increase proportionately. Dep and lease liabilities also to kick in from Ultra Pipes. Other exp may increase because of HPEPL, Interest may also increase of higher term loan on account of higher inv. Hence thought PAT is likely to increase by 9-12% only.. Kindly share your views..

For such comodity company, they can able to guide for volume growth only. Revenue and profit are not in their hand. Same is observed for SG Mart and other comodity players.

Gone through their concall, found weird that they ask questioner to meet them atleast 3-5 times. This seems not normal, if they need anything to disclose, it should be done in boarder call vs individual. May not be that big issue but…

Disc: Invested and intent to remain same untill next Q result.

Have they stated anything about their renewable business, I see they had updated about the order win in renewable energy business.

What’s the thought process or foraying into renewable energy business. If any?

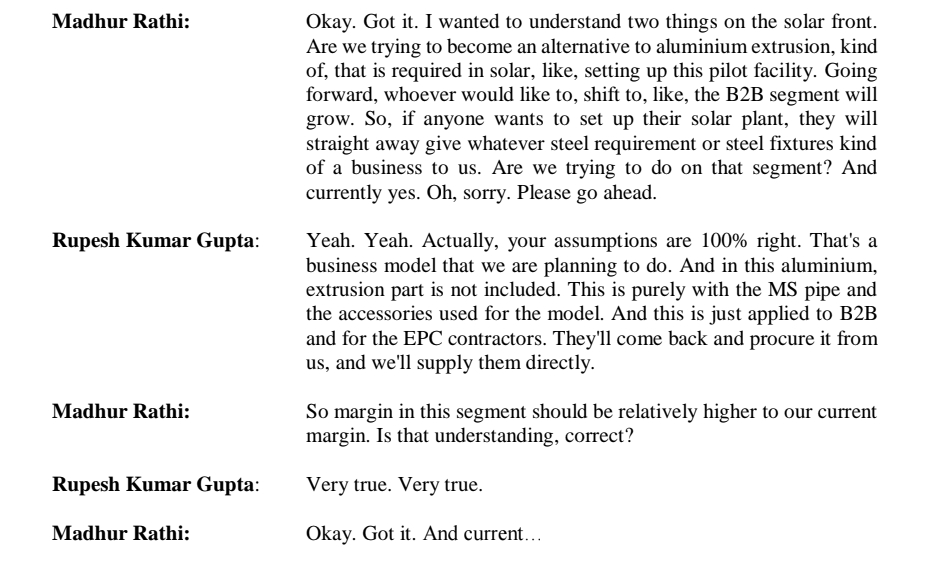

Read this 2 page.. u will get complete understanding of starting solar vertical

After reading this.. I feel they will try to do something unique in solar space to capture growth momentum sector has

My assumptions are if they succeed in such things then they can partner with Rooftop solar companies like Waarre, Adani or tatas for supply of spares in total

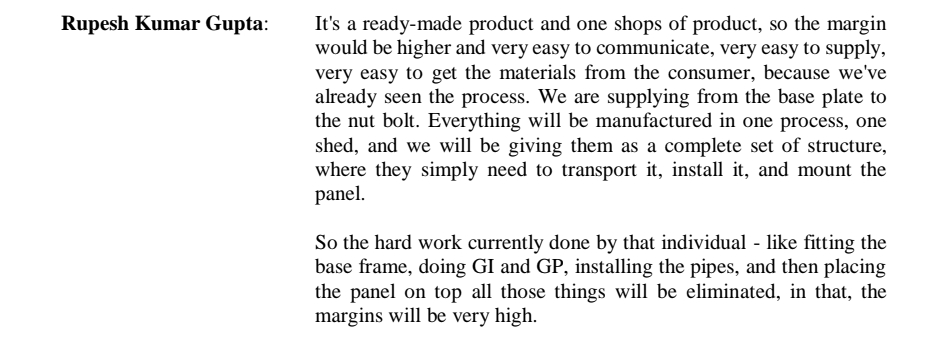

++ As management said this thing has higher margin, can be cherry on cake if succeed

No Reco.. just my assumptions

Why they are installing 60MW solar plant in maharashtra is still a question.. but about starting supply of solar accessories can be a welcoming move

There might be some confusion here due to the reply to Shaurya Yadav’s question. Which management clarified in a follow up question .

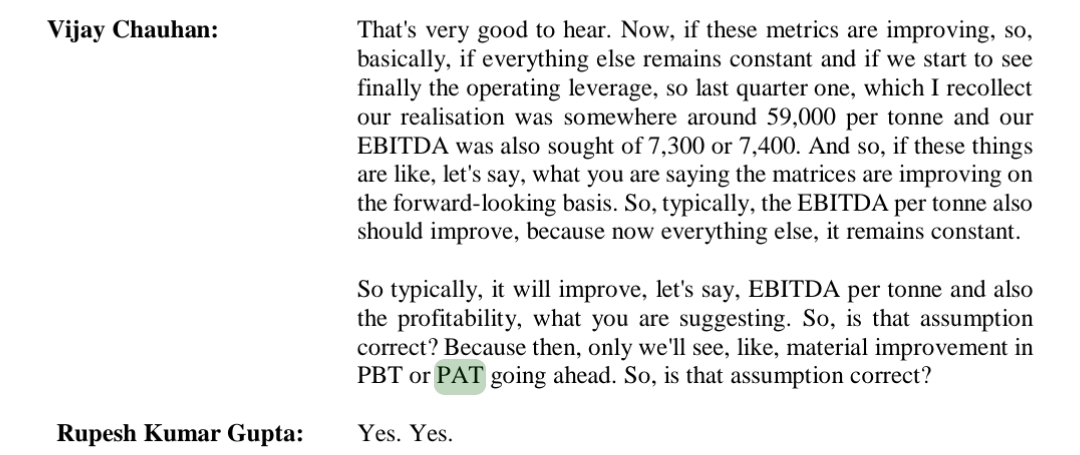

However my take is that since Steel prices might have bottomed out PAT growth should mirror that of topline growth here if Finance costs and depreciation remain constant.

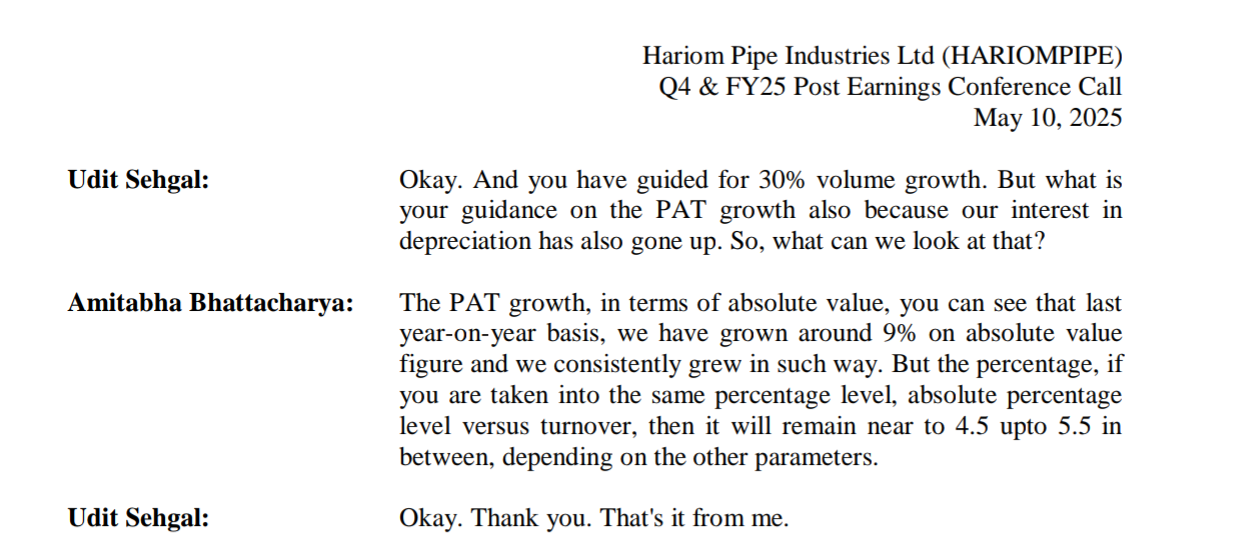

In one answer they mentioned that PAT margin was around 4.5% in Fy25, and that future margin will remain 4.5-5.5% range.

Another point was around current Q1 realization which they said were up 5-6%.

But at the very end they were wary of giving a clear guidance.

Here is a chronological sequence from concall:

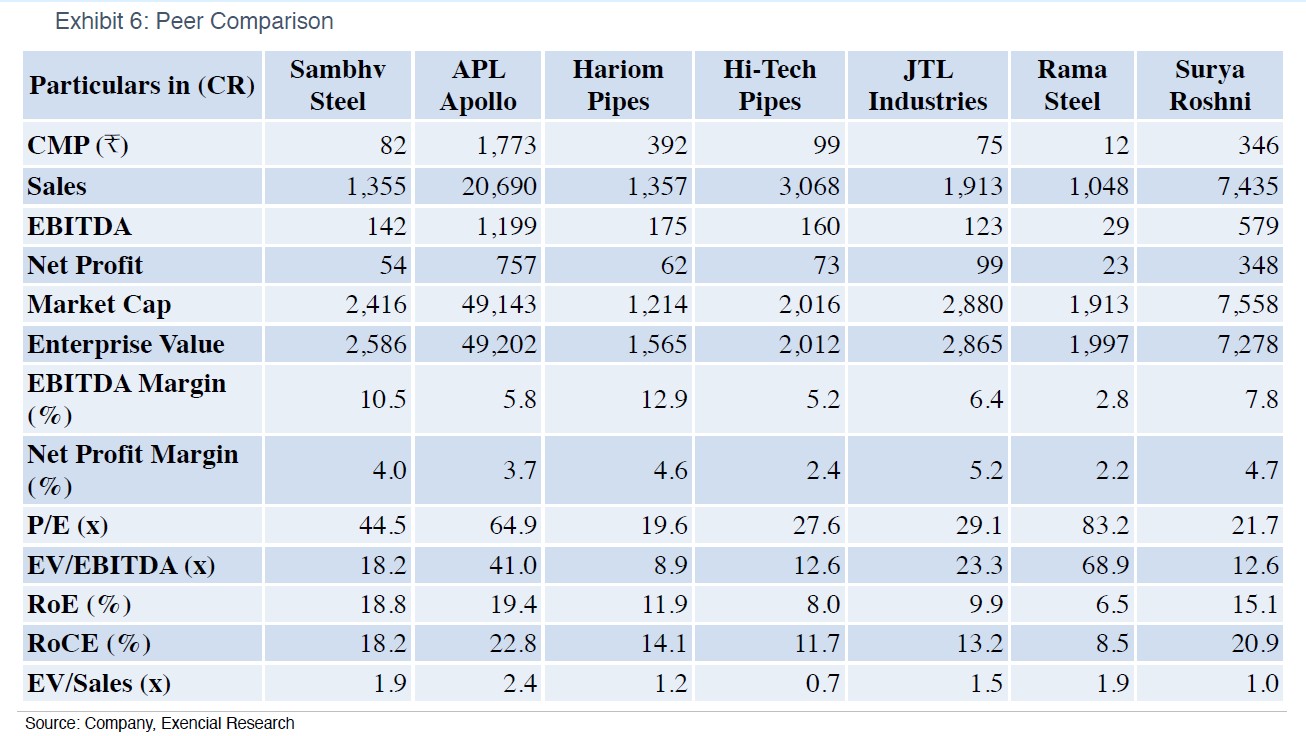

Sambhv vs Hariom (Source - Exencial Research Partners)

Seems bahut na insafi hai with Hariom, jokes apart - Hariom seems beat sambhv in all parameters (except PE ![]() ).

).

Disc: Invested in Hariom and views are biased.

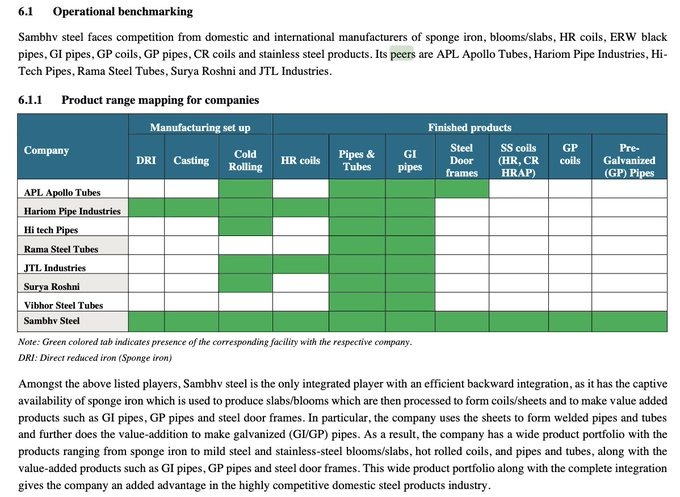

I think Hariom Pipes is the only company where they have integrated plant for pipes