This video may be beneficial reading on the different type of pipes being manufactured by hari om(patra raw material) and sambhv(narrow width hr coil) , quality of pipe is better in case of manufactured with narrow width hr coil

This video may be beneficial reading on the different type of pipes being manufactured by hari om(patra raw material) and sambhv(narrow width hr coil) , quality of pipe is better in case of manufactured with narrow width hr coil

You forgot ROE & ROCE of Sambhv is way above Hariom also working capital cycle is shorter as compared to Hariom and Sambhv has done some capex which is yet to get utilized & greenfield project is going to commence in coming years which can provide growth runway as compared to Hariom

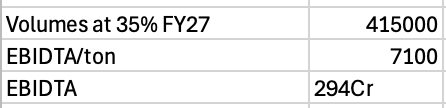

I did some back-of-the-envelope analysis for FY27. It looks very cheap at current levels. According to my estimates, it can do 160Cr+ PAT in FY27. It’s trading at 7-8*FY27 earnings. This year, they had very good cash flow, which was a confidence booster.

Only 137KMT capacity is backward integrated and presently at 75% of capacity utilisation and blended EBIDTA is Rs.7147. GP lines are not backward integrated and CU is 17.2 %. So the volume growth will come from GP Coils..so how did you come to Rs 7100/- EBIDTA

It’s in the last concall, there were a lot of questions about it, but they reiterated, it will be around this level.

Hello. Thank you for the opportunity. My first question was that, to make galvanised pipes, the raw material, which you mentioned, HRC, that is currently available in the market at INR 45 per kg. So, what is the blended cost of manufacturing including the raw material and conversion cost, just for this galvanised pipelines? And what would be the average realisations currently?

Amitabha Bhattacharya: So basically, madam, in short, all of your question, I can give you

that around 6,600 to 6,800, that much of blended EBITDA, that much of per-tonne EBITDA, we are earning from the galvanised pipe and coil, this product.

Now comes to volume

Amitabha Bhattacharya: So as of today, we are on track to achieve around 14% volume growth in Q1 compared to the last quarter.

Amitabha Bhattacharya: 33,380 metric tonnes, which is almost on 40% of our Q1 FY '26 target.

and

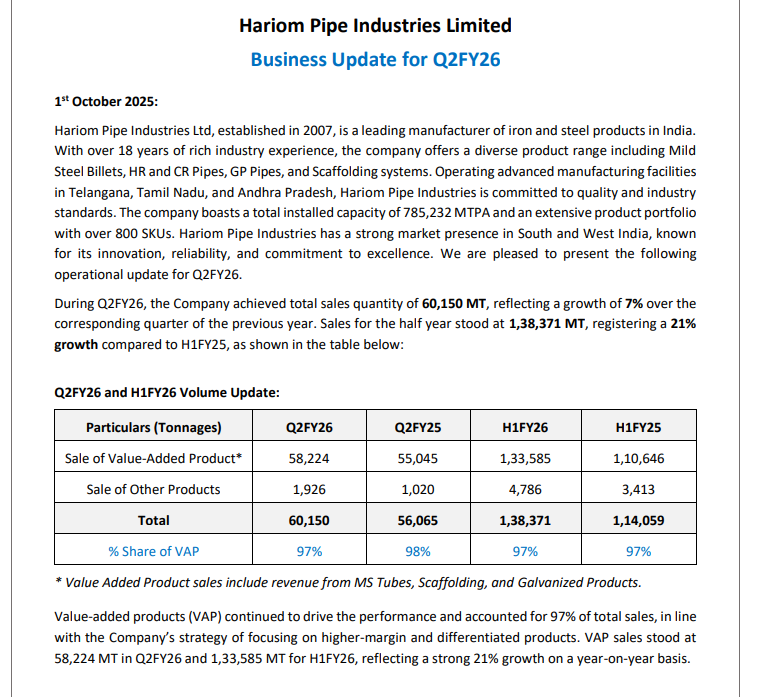

ended up with Total Sales Volume for the Quarter - Growth of 35% YoY & 5% QoQ

Flagging post for using AI for self promotion.

There is no value added to the trhead by the user. Request moderator to ban.

Hariom Pipe Results

V Good set ![]()

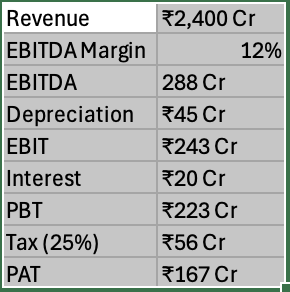

Rev Growth of 34% YoY n 15% QoQ

EBITDA Growth of 31% YoY n 20% QoQ

Margins up at 12.8% vs 13% YoY n 11.8% QoQ

PAT Growth of 35% YoY n 37% QoQ

Finance cost & Dep Stable ![]()

Finally after 2 years; they had started delivering on Numbers

EBITDA/Ton also started inching upward from 6,583 to 7,360 QoQ

Targeting 30% Volume Growth CAGR for next 2 years

Overall V Good set

No Reco

I am a bit disappointed the way depre and interest costing is increasing (or stable but not reducing) despite management promising few times earlier that they will get it reduced. This is the reason the PAT margin is not improving despite leading EBITDA in industry. The industry leading EBITDA of Hariom is getting wasted due to depre and inter cost as they are not able to convert it to bottomline.

ALso, do we know what is this “enabling the Company to borrow up to INR 2000 Crore including present borrowings, and Creation of Charge on the movable and immovable properties of the Company”. Why do they need to raise so much money while having sizable amt of debt at the moment?

Capacity utilization is at ~45% currently. if the volume growth of 30% CAGR is indeed achieved (as mentioned in ppt) leading to better utilization ~60-70%, that will help for better fixed cost absorption.. which in turn should help EPS growth substantially..

Just sharing the latest announcement

My personal opinion is that for a market cap of 1700cr company to invest more than 3000cr for an integrated steel plant is slightly MORE AMBITUOUS.

Please share your opinions.

Invested but considering selling after this announcement.

I sometimes dont get the promoters … things are looking good, operating leverage is playing out and suddenly now they want to invest almost double their mcap … obviously a lot of dilution will need to happen for this and debt is not great too

Even I am little confused after this announcement

My opinion:

Need to see validation going forward or Q2 concall might answer it

PS: Biased & Invested but if it turns real then can be a dent to thesis

Since they haven’t mentioned any timeline, this ₹3,300 cr MoU could be a phased investment over a longer horizon. In the Q1 call, management had spoken about a greenfield project in Maharashtra, which might unfold over a prolonged timeline, not something immediate.

Let’s wait till Q2 concall for conclusion.

Q2 appears to be disappointing, especially compared to Q1. Q1 was a solid set of numbers with 40% growth QoQ. Agreed that Q2 was affected by monsoon. But Q2 of last year had monsoon also. So Q3 has to be watched closely .

Seems South India had a rougher 2025 monsoon than 2024. Could be a reason. Though lets see what other pipe manufacturers come up with

Every year each quarter something happens that dampens the sales growth. This company seems to have become a quarter se quarter tak company. Q2 will be yoy 10% growth and qoq degrowth.

Bought before Q1 result and sold around 480. Seems like it was a good decision.