Detailed Analysis of Hariom Pipe Industries Ltd.

Market Cap: 1600 Cr.

5 year Sales CAGR: 44%

5 year Profit CAGR: 48%

ROE: 20%

ROCE: 17%

Let’s, deep dive into it

Business Overview:

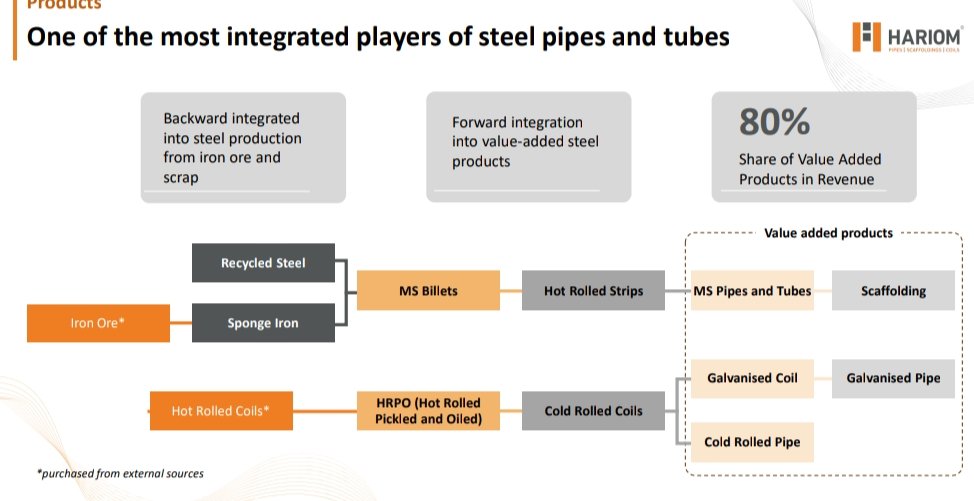

Hariom Pipe Industries Limited is an integrated manufacturer of multiple industrial pipes & tubes

With a diverse product portfolio consisting of Mild Steel (MS) Billets, MS, GP, GI Pipes and Tubes, HR, CR, GI Coils, Scaffolding Systems, Metal Crash Barriers

Product Profile:

Sponge Iron: Raw material for making Pipes; It’s an alternative to Scrap/Patra (Better quality than Patra)

MS Billets: It’s pure steel (Metal Bar)/Semi-finished steel

HR strips: Again a semi-finished iron or steel

Both of these are used for making Pipes or tubes

MS/HR Pipes: Co. manufacture square, rectangular, circular and D-shaped sections pipes

HR pipes up-to a maximum size of 250x250mm for square sections, 300x200mm for rectangular

sections and 300mm NB (nominal bore) for circular sections. The thickness can vary from 2mm to 6mm

GI Pipes: Galvanized pipes are steel pipes that have been dipped in a protective zinc coating to prevent corrosion and rust. These pipes are used earlier for water supply in home; it is made from GI Stripe, which are again made inhouse

GI Pipes are high margin pipes

Scaffolding, Tube Accessories and Fittings:

Scaffolding is used in construction activity, both buildings and other infrastructure construction. Scaffolding is used for variety

of purposes including ease of construction process and safety of workers

Catering to wide Industries like:

-Housing

-Infrastructure

-Agriculture

-Power

-Cement

-Mining

-Solar Power

-Engineering

-Steel Industry

-Railways

Scaffolding is used in construction activities

This makes end-users diversified in nature & reduce concentration risk

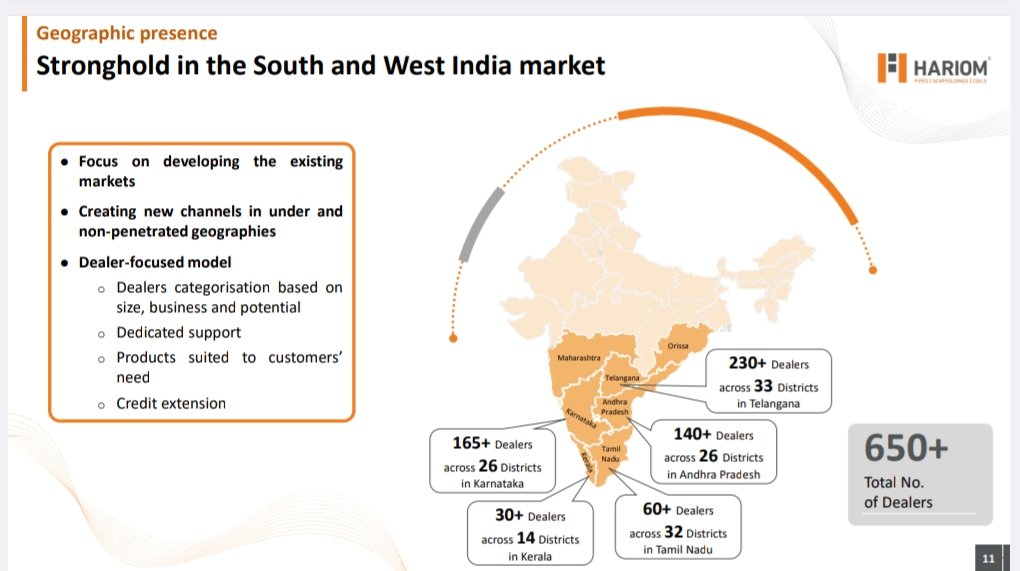

Distribution Network:

Hariom Pipe has a strong distribution network of 1,400 distributors and 1,500 point of sales in:

Telangana

o Andhra Pradesh

o Karnataka

o Tamil Nadu

o Kerala

o Maharashtra

o Dadra & Nagar Haveli & Puducherry

Mainly catering to South & Western India

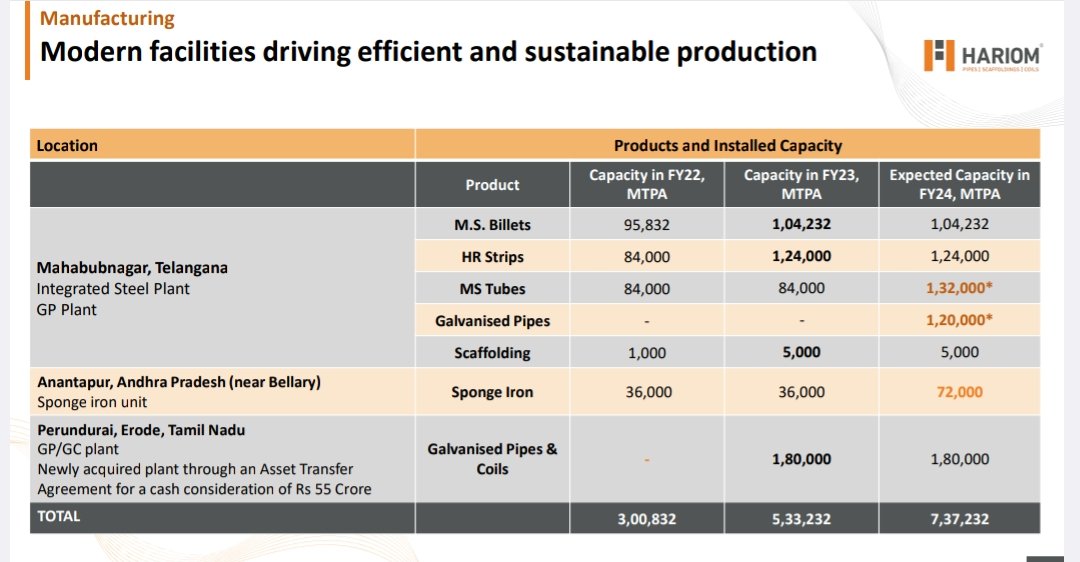

Production Process:

Hariom is Vertically & Backward integrated in manufacturing Pipe & Tubes Process

-Major raw material for this process comprises MS scrap, sponge iron and pig iron

-Through sponge iron & scrap, HR Stripes are made and from HR Stripes, Pipes & tubes are made

MS Steel Pipes are manufactured by using the process called Electric Resistance Welding (E.R.W).

As the company is Vertically integrated it makes sponge iron internally

Sponge iron is made from Iron Ore, which company procure through E-Auction

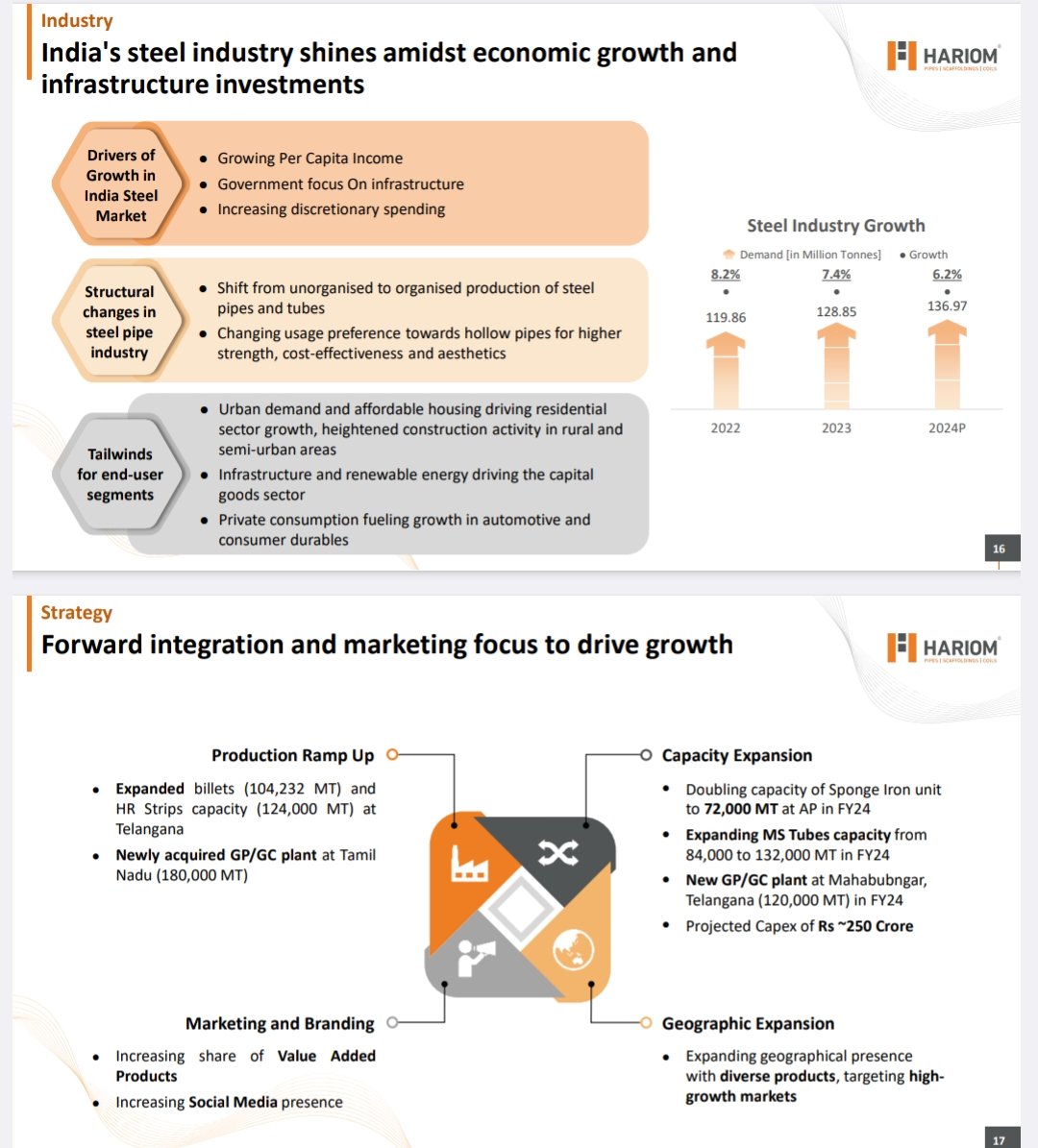

Industry Overview:

-After Europe and China, India is amongst the top-3 steel pipe manufacturers in the world with

capabilities to manufacture crude steel to value-added steel products, including pipes & tubes

-Availability of raw material, cheap labor & ability to produce steel at low cost have supported India’s

progress in the steel pipes & tubes industry. In terms of steel consumption, India stands amongst the top-3 countries in the world

Per Capita Cons. of steel is still very low

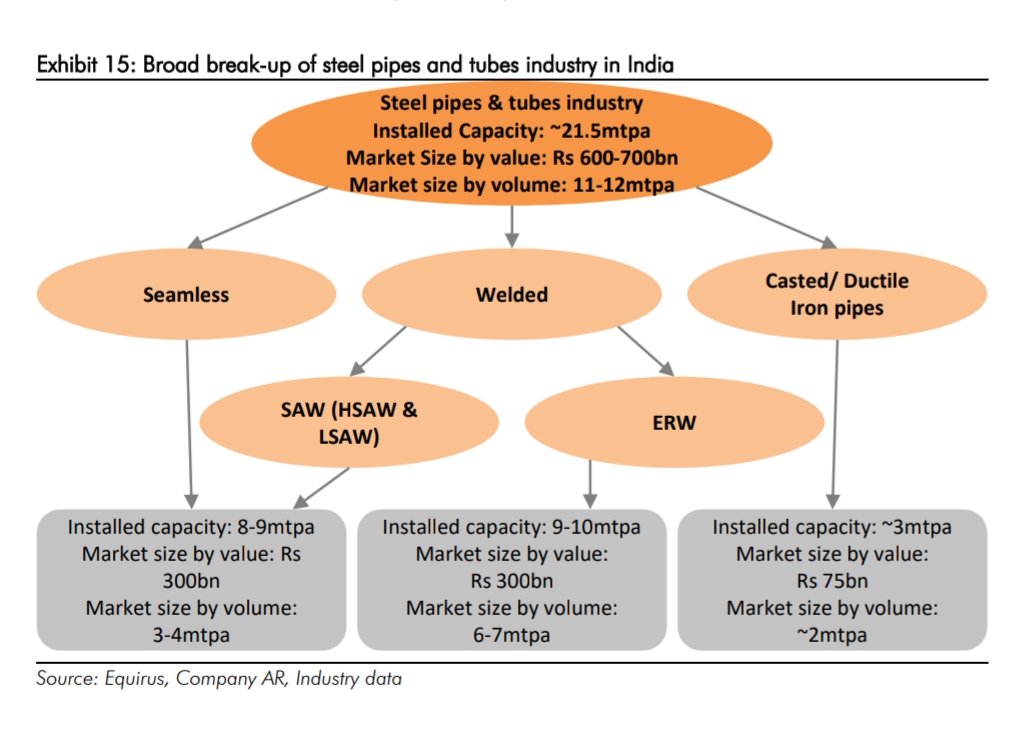

Indian Steel Pipes & Tube Industry:

India’s steel pipes & tubes market is currently estimated at ~Rs 600-700bn in value and ~11-12mtpa

in volume terms

It is expected that Indian Steel industry will grow at 7-8% CAGR for next 5 year

Hariom manufactures ERW & HSAW Pipes:

Types of Steel Pipes & their key features:

-DI Pipes are commodity Pipes

-ERW Pipes have wide usage & are little value additive in nature compared to DI Pipes (ERW Pipe market is expected to grow at 8-10% in future) aka Future growth driver for Pipe Industry

Key Competitive Advantage of Hariom Pipe:

- Vertically+Backward integrated manufacturing process:

-This insures margin safety in bad times & also can face high competition

-Dependence on external sources of RM reduce

-Better quality maintain

-Efficiency of production increases - Qualify chemist & engineers, which help in maintaining quality standards as per Industry standard

- High Number of SKUs/Customised products as per customer (Maintain customer stickiness)

- Strategic location of Units, which help in maintaining logistics cost

- Experience Promoter over three decades experience

- Competitive pricing of product as it’s product are in between Industry specialist & Patra base pipe products, which enable to capture price sensitive clients

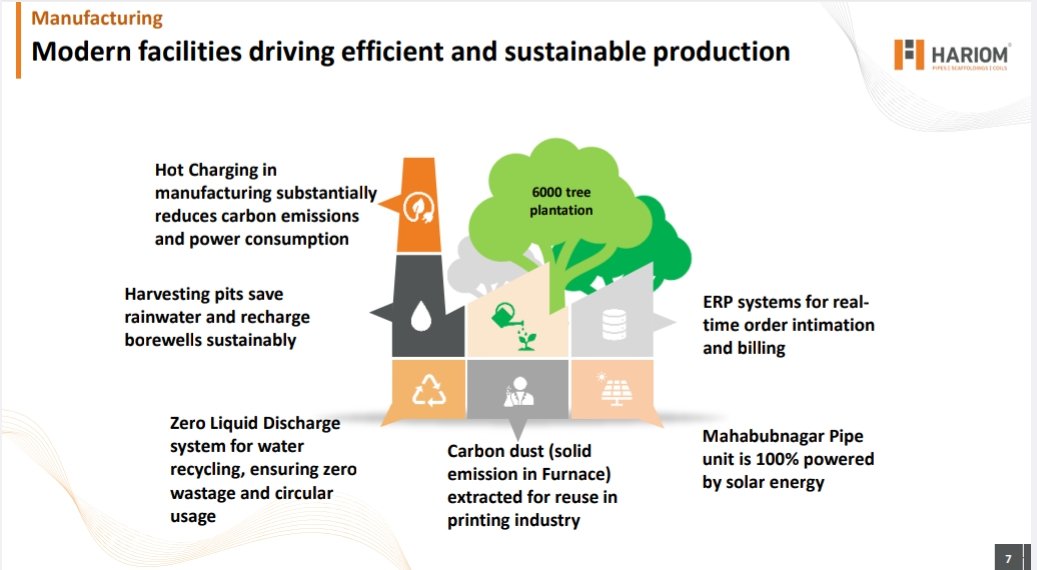

- Sustainable steel producing method

Key Variant Perception playing out:

- Margin Expansion in Future: -Through introducing VAP: GI Pipes

-Cost Reduction: Reducing waste through automation & Reducing Power cost (through establishing solar plant) - Industry Cycle: Industry is growing at low single digit

- Capex led growth: Hariom has increased MS & HR Capacity in the current plant (Up by more than 55%) + Introducing GI Pipes through IPO money, Debt & fund raising

- Operating Leverage to be played in future as sales increase

- Stable operating margin

- Acquisition of R.P Metals (But it’s products are commodity & low margin in nature)

- Additional Capex for cold rolled strips would cater demand to Asia’s largest hub of fan manufacturers in Hyderabad

Sources of Future Earning Growth:

- New Product Introduction (GI Pipes)

- Geographical Expansion through entering new states & Export contribution & Expanding distribution network

- Growth in the End User Industry(Capex cycle is going in India)

- M&A & Capex led growth

Peer Comparison:

-Indian Steel Pipe Industry is highly fragmented & dominated by large organised steel pipe players like APL Apollo & various unorganised Patra based manufacturers

-Its closest competitors are APL Apollo, Hi-tech Pipes, JTL Industries & Surya Roshni

Anti-thesis/Risk:

-Highly competitive & Cyclical Industry

-All players are doing Capex this can impact industry profitability

-Low margin Acquisition of R.P Metals

-Last year Cash flow turn -ve (need to track the CFO conversion)

-Debt has increased for WC needs

-Finance cost & Dep increase as Debt & Capex rises(this can impact margins & PAT in short term)

-Contribution from low margin product impacting margins

-Concentration risk: Top 10 customer contributes over 50% of sales

-China dumping low price pipes in India & other countries

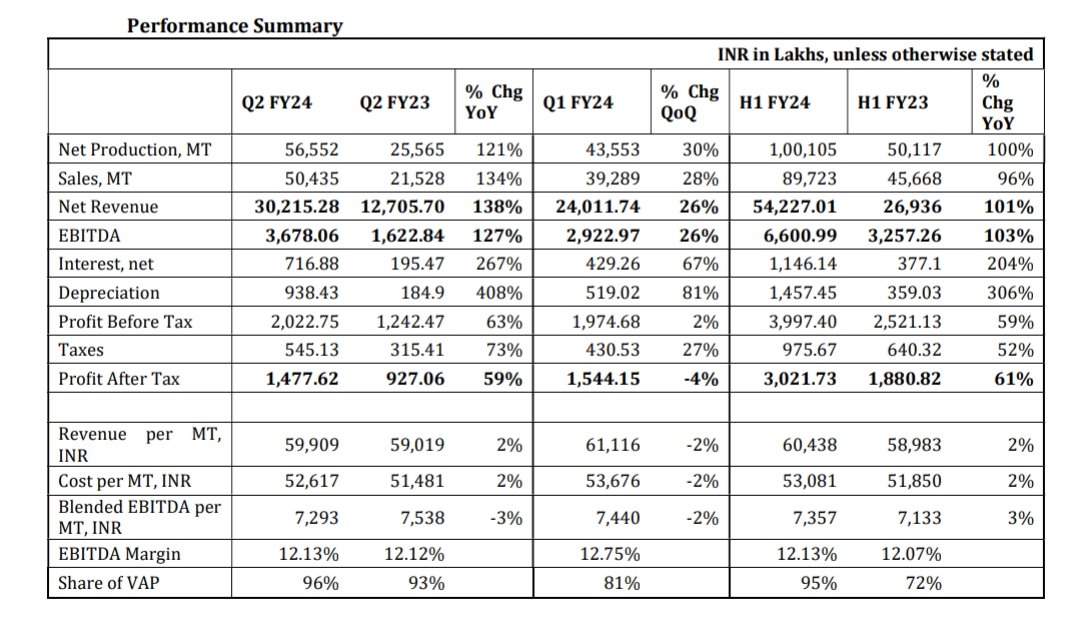

My Estimates (can be totally wrong):

- FY24 Revenue can be around 1000-1200 crores

- EBITDA Margin can be in the range of 12-13%

- PAT is expected to be around 58-68 Crores

- Trading at a forward PE of around 26

Strictly, No Recommendation

Disclosure: Invested & can be Biased

Note: Can’t able to Put proper Analysis with Images cauz of New Member restriction. If anyone want to read full analysis, one can check my twitter profile: https://twitter.com/BansalSwapan

I hadnt done Financial Analysis as one can check screener for it!!