I reckon numbers are very soft in this qtr.

Guidance is intact.

But what’s the fundraise for, they were easily able to service the debt and CFO is hesitant in answering the reasons for fundraise.

I reckon if this qtr is soft for hariom , it may be horrible for other players.

But next few quarters don’t look good from existing shareholders perspective , due to dilution.

I noticed one thing from the video. The CFO in spite of not answering the reason for fund raising directly, he kept implying that the present and future CAPEX to come can be easily managed with present funds and accruals. I feel this fund raising could be for a new big project rather than addl fund requirements or wc

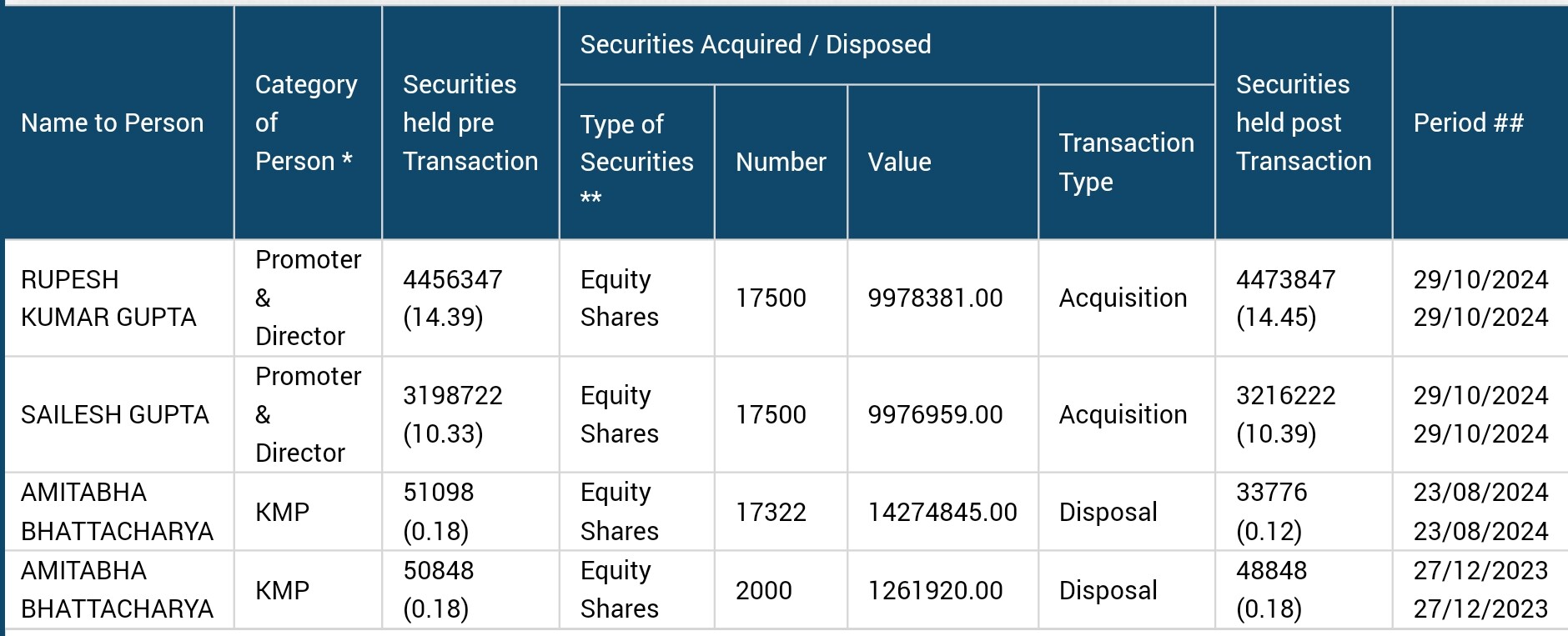

Curious to know on why these individual are not exercising their warrant. Considering current share price which is double of exercise and 25% of exercise price is already paid. Why would someone do this?

Only explanation in my mind is the investor doesn’t have the funds to invest or they simply forgot. Malabar recently converted their warrants into equity shares in Q1 of this FY.

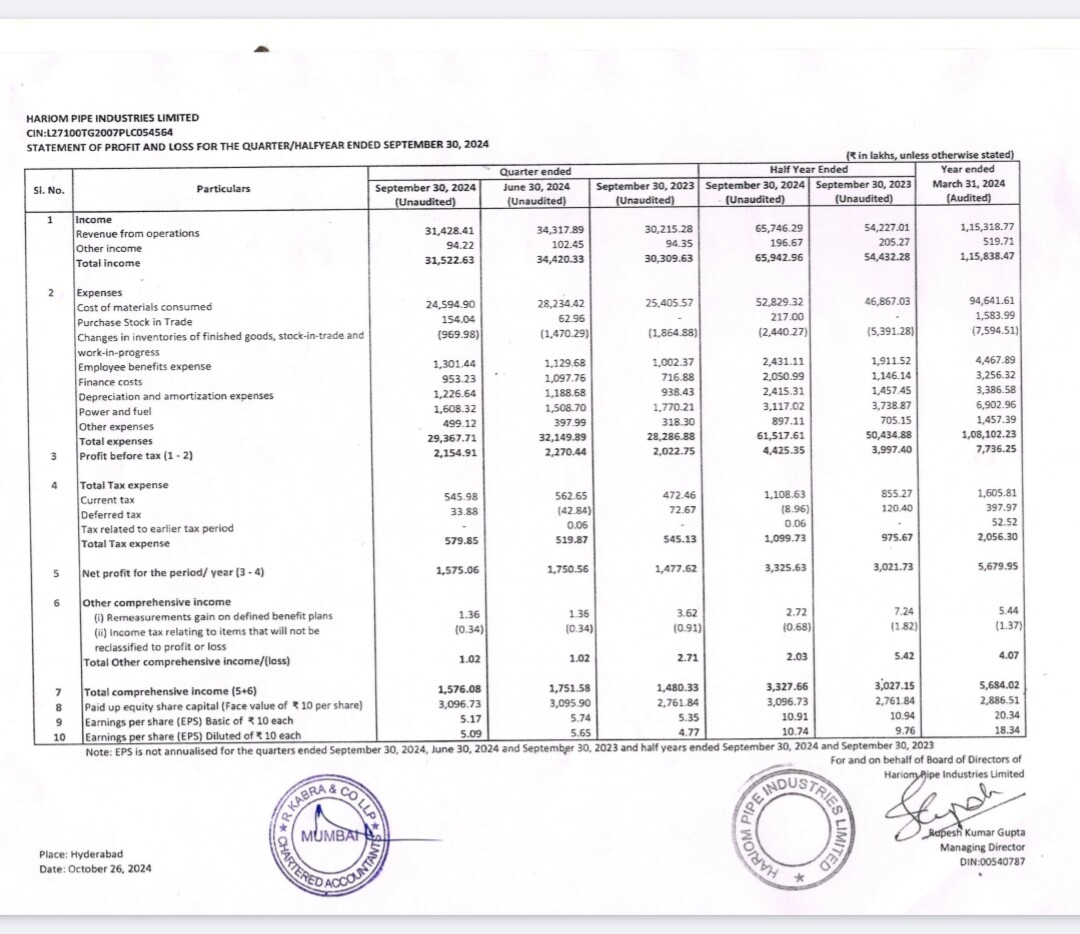

The Q2FY25 result is extremely weak. The company promised sales CAGR of 50% over FY24-26 until Q4FY24 (mentioned in the result PPT). Interestingly, in their Q1FY25 PPT, they didnt mention any guidance. Now with a result disaster in Q2FY25, it shows what the management is upto.

While the results aren’t the best, the recent crash should prevent further downside. Hopefully H2 is better. It is still marginally better YoY. Nice to see that they have scheduled a con call so hope the right questions are asked. Overall I see this as flat results. The fund raise may add to existing pressure on price upwards though.

The result in the current quarter for all pipes companies will be subdued given the fall in steel prices, late budget and rainy season.

the steel prices have corrected by 30% to 40% from the highs leading to fall in realization of pipe making companies.

Hariom which is an integrated player makes pipe out of HR coil which has better realizations as compared to Patra Pipes so, the difference between Patra pipe & HR coil prices have now Shrinked down and now the difference is of 20% to 25% which is a good thing as the market gets more mature increased traction will be seen by HR coil Pipe manufactures as compared to Patra pipe Manufacturers due to better quality and strength.

This fall in price will lead to increased stocking leading to many pipe companies like Hi-tech pipes, JTL Industries and more posting record volume but the realizations will be more or less flattish.

this, is a short to mid term i expect that by Q3 or Q4 of this year we’ll also see reversal in steel prices and value growth along with volume growth for pipe companies.

Point to highlight:

In 2020, APL Apollo the sector leader stopped selling products on credit and to this decision all players followed except hariom pipes today it is the only player in the industry that provides credit to it’s customers to me this was interesting also it is verified by debtor and creditor cycle.

The Six Monthly Balance sheet attached in result of current quarter shows increase in debtors as well as the payables have grown from 19 crores to 108 crores so what can be the possible reason behind it. (one need to think of it.)

Revenue grew +6% as realisation declined -5% YoY due to reduction in end prices

Monsoon in South India were exceptionally disruptive this season and hence the demand was weak in the past few months - slower construction, infra build out

EBITDA grew +18% YoY

Better metric to track company is EBITDA growth and EBITDA/ton since realisations/revenue can fluctuate based on steel price; however Hariom can capture adequate EBITDA/tonn regardless of commodity price volatility

WC down to 58 days in H1FY25

OCF for H2 was +50 crores and 35 crores of debt was paid down

Capital Raise

Enabling resolution of QIP; Focus will be on specialized steel products + Geography expansion

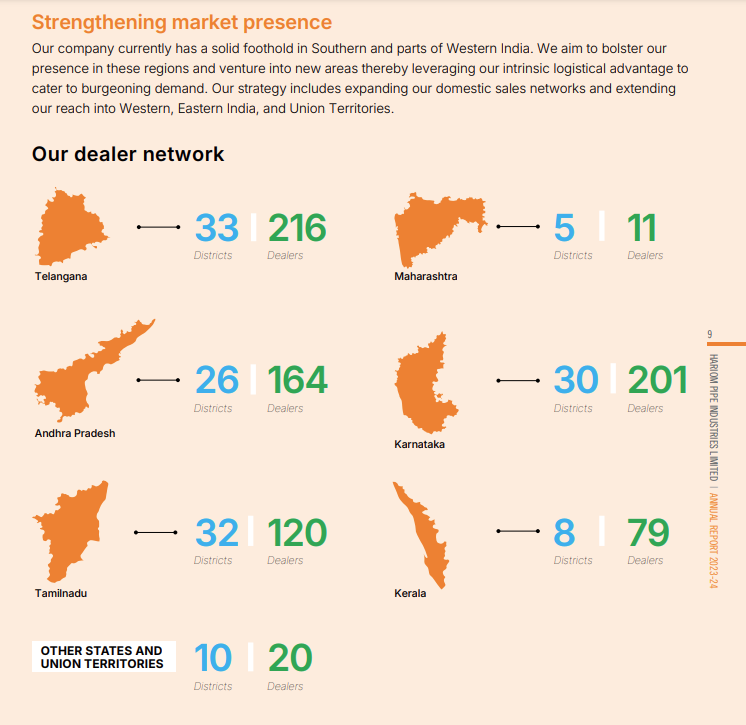

Distribution

Have direct connect with 800 dealers in south india; don’t work with distributors

Work with fabricators but not directly, instead connect with local dealers

Guidance

Co has ~270kt sales target for FY25

In H1, 114kt volume done, so ~156kt remaining for H2

FY25 revenue target = 1,600 cr

FY26 revenue target = 2,500 cr reaffirmed; this hasn’t been changed despite weaker than expected Q2

Only bought 35k shares, but still shows commitment of Promoters on Biz even after weak Q2

Concall was also seems Bullish with Guidance Intact, QIP is just an enabling resolution, CFO issues solving, Operations stabilizing, focusing on Geographical Expansion & Deleveraging + Promoters Trust on future growth

It is said that insiders can sell stake for many reasons, but there is only one reason for buying.

H1FY25 revenue is 657 crores. During Q2FY25 earnings call, mgmt shared guidance to get to 1,600 crore revenue in FY25.

This implies guidance of 943 crores revenue in H2FY25.

Company has done 611 crores in H2FY24 and hence promoter buying from open market could mean that they have good confidence in achieving this 50%+ revenue growth in H2?

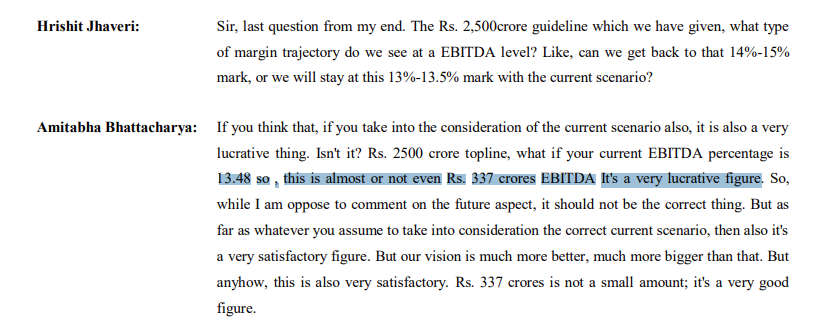

So maybe 13.5% is a conservative guidance on margins for FY26?

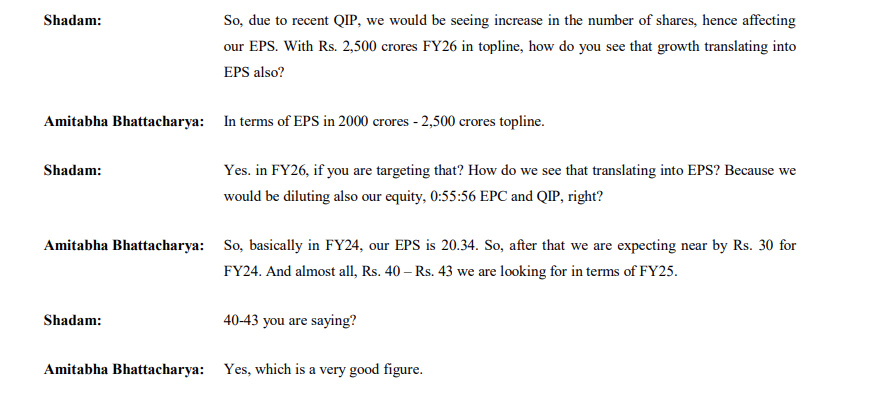

EPS guidance assuming dilution of due to potential ~700 crore fund raise.

EPS expected for FY25 = ~30

EPS expected for FY26 = ~40-43 | This assumes dilution of a certain % at a certain stock price.

We need to do some math on back calculating the implied dilution % in-built in this EPS of 40-43

a) No dilution scenario:

337 crore of FY26 EBITDA mentioned by CFO above

50 crores of depreciation

40 crores of interest cost

= expected PBT of 247 crores.

Assume a 27% tax rate

and this gives us 180 crores of PAT.

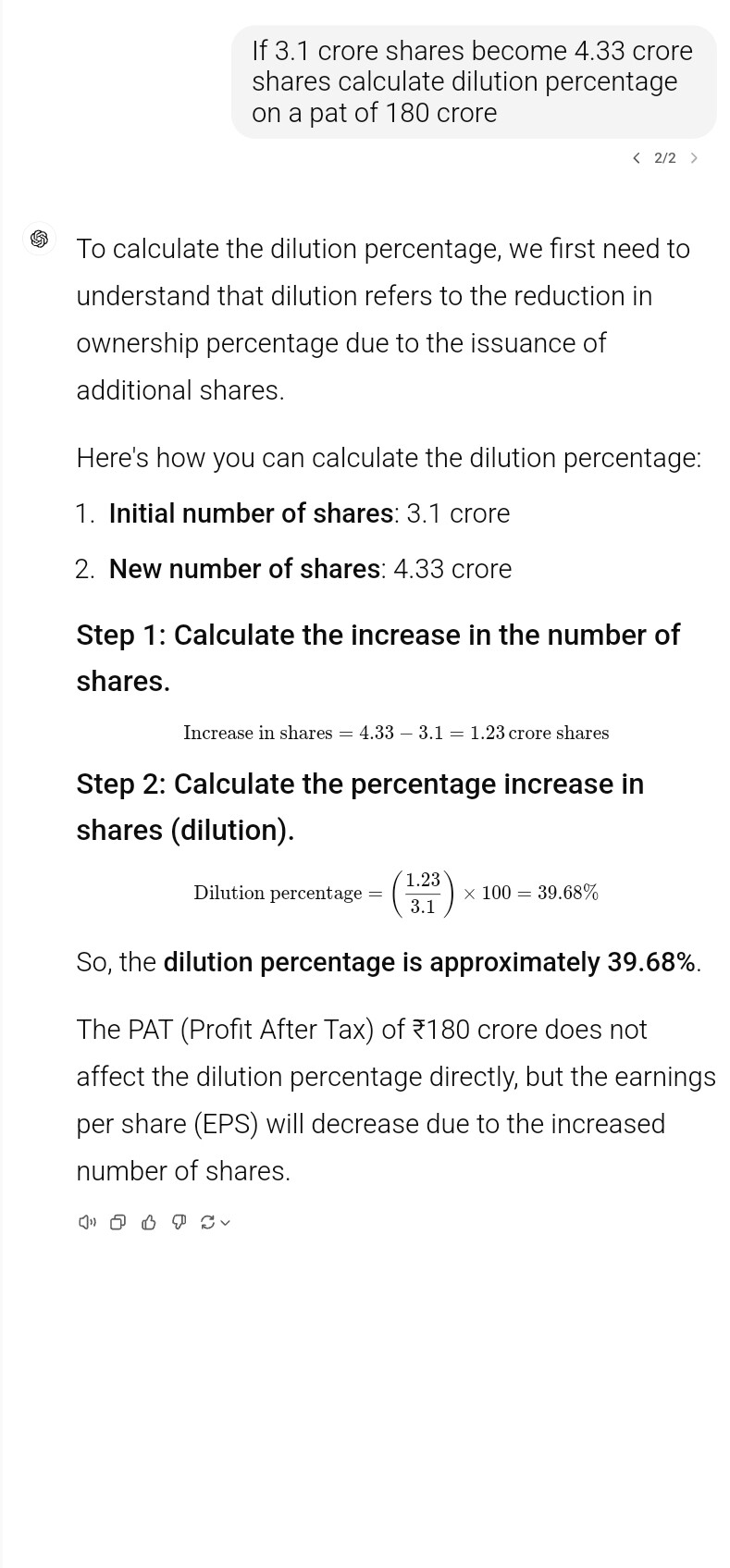

3.1 crores total shares outstanding gives an approximate FY26 EPS of ~58

b) Dilution Scenario

If we apply an EPS of 41.5 (mid-point of dilution scenario), on 180 crores of PAT, this assumes total shares outstanding of 4.33 crores which means ~40% dilution on share count basis

Current Market Cap is ~1800 crores and 40% dilution means a fund raise of 1800*0.4 = 720 crores. So, basically the 40-43 EPS for dilution scenario assumes (1) QIP happens at CMP and (2) the entire 700 cr is raised and (3) No interest cost savings by debt paydown from QIP money (4) No incremental revenue or profits from incremental fund raise.

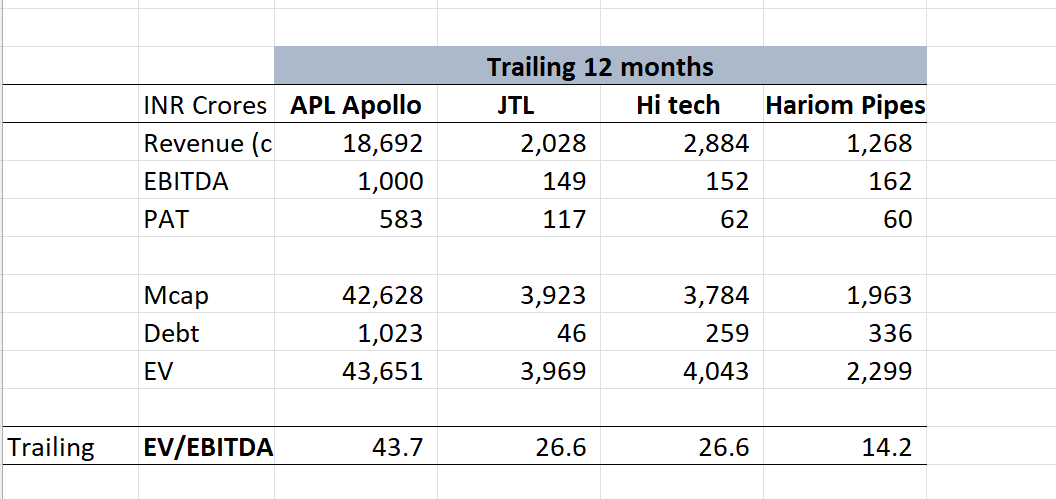

Now that all pipe companies have reported Q2 numbers, here is compilation of valuation comparison based on EV/EBITDA.

Note: This is based on trailing reported numbers and doesn’t take into account future growth.

@SwapanBansal , thanks for your detailed analysis earlier. You have been quite passionate and very much consistent in providing the business level update for this scrip. Also thank everyone else for adding the details.

I have a few points that i want to mention here.

@SwapanBansal : your analysis mention earlier as the below exhibit. Does this mean that the industry installed capacity is more than market size? I am sorry if this sound stupid question but do we have any view of estimate market size in India? ALso i see that other players are also doing capex to increase capacity what is the scenario here? I think it is important to understand this in order to be able to completely understand the 2x growth they are planning to achieve, though i do not deny their growth story.

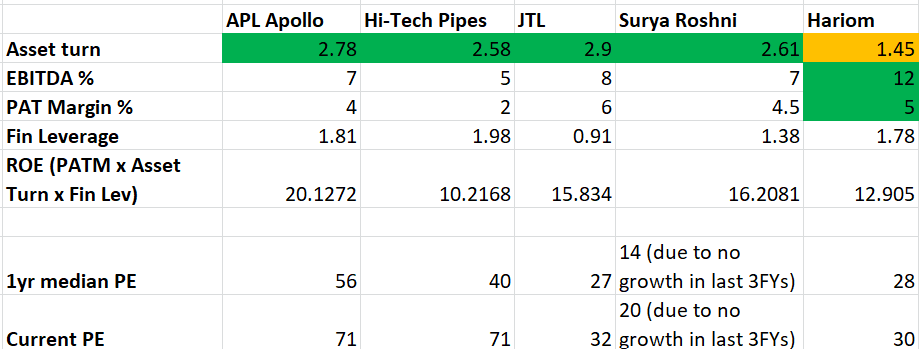

I have observed that the ROE for Hariom is just matching the other players (if not below), and main reason i can see is the asset turns for Hariom is significantly lower. All other competitors operate at >2.5x of asset turns while Hariom is <1.5. WHat is the reason for this? I can understand that this may be partially because they produce VAP as opposed to the commodity. But this may not be the sole reason behind the significantly lower asset turn. If they can achieve the same asset turns as the peers, this can be a very big game changer given that they are already working to improve PAT margin by reduction of debt. Currently they are just able to match the ROE in fact it is lower than peers) as the peers because of a little higher PAT. This is also one reason they have lower PE than peers i believe.

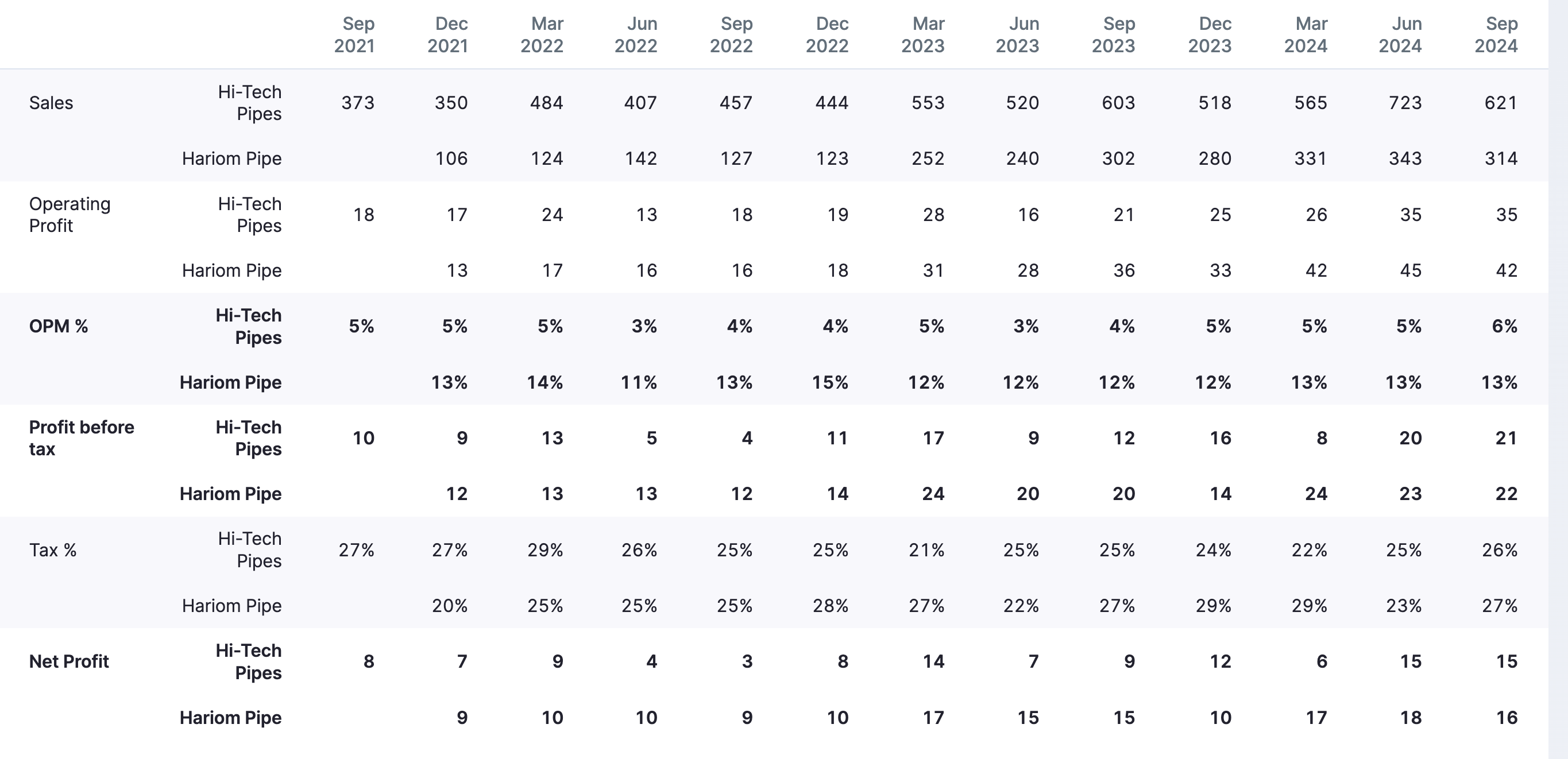

Any idea why Hi Tech pipes has a higher valuation multiple v/s Hariom despite Hariom having slightly levels of absolute PAT/EBITDA ? DII+FII ownership in Hitech is ~30% vs 10% for Hariom.