They are Backward integrated

If u see their product manufacturing chain

They Source Iron Ore and makes sponge iron & from that billets & then Pipes and so on

This is the reason behind their stable & High margin compared to Peers + They focus only on VAP Products (90%+ sales of VAP), while competitors & china focus on High Volume/Commodity products

Backward Integration can save Hariom in bad times like if for any reason Sponge Iron/Steel/Billets rises they would not be impacted much as they manufacture such products (Even they can sell that products, if they gets opportunity as management is growth oriented)

In short:

-Backward Integration (Save margin & can fight competition in bad times)

-Focus on VAP Products only

Above 2 lead to stable margin

Hope you get it

5 Likes

Does the business need to do additonal capex to fuel the 2500 revenue goal?

If not it could work on debt reduction and lead to growing positive cash flows

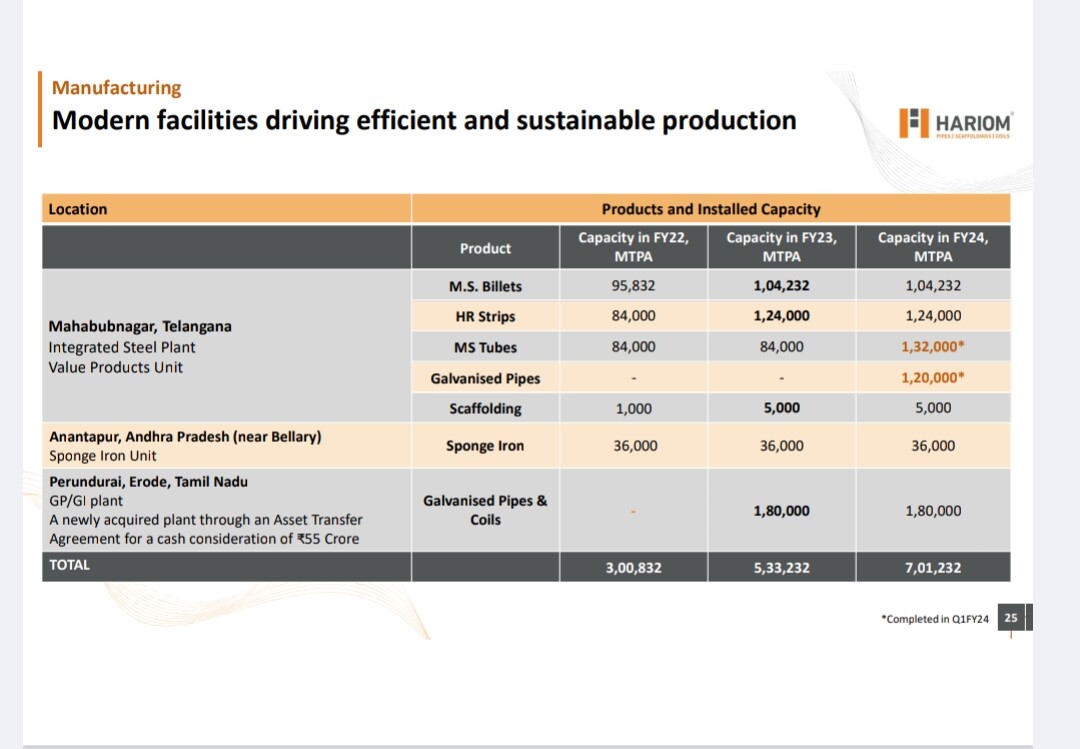

No Capex required for Revenue target of 2500 Cr in FY26

They are currently running at 30-35% capacity only

Total Capacity is 7,00,000 MTPA

Current Capacity can easily generate potential revenue of 3000-4000 Cr

Huge operating leverage with Debt reduction leading to PAT margin expansion (if CF Improves) can easily happen

4 Likes

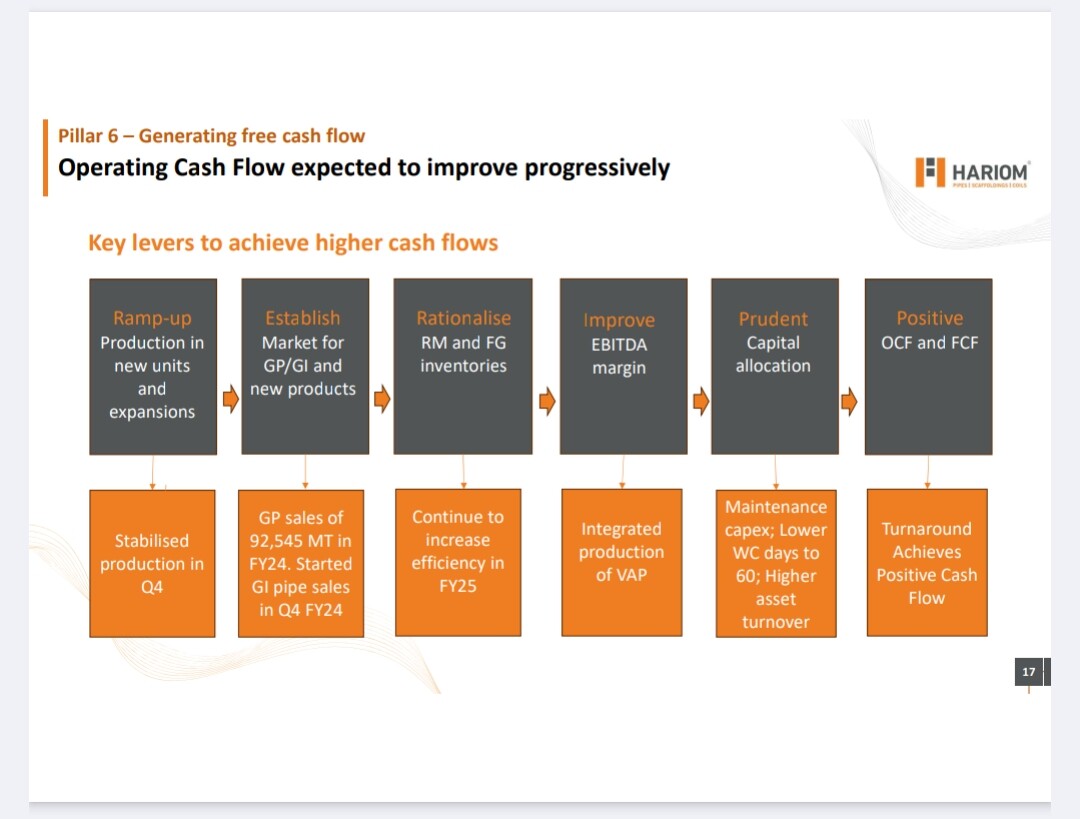

Problem is not capex. Problem is working capital. How do you solve for that?

Here, they have guided… How they will

Also, CF turns positive after long time in last Q + Inventory, Receivables turnover ratio also improved

Hope for the best from Q1

3 Likes

Hariom Pipe Management Interview

Some Important things:

-Past growth will sustain

-Will focus on improving operating efficiency & VAP

-ROCE will inch upward to 21%

4 Likes

is venus pipes a competitor in any way

Venus is not a competitor

Both are totally different:

Hariom is in ERW Pipe segment & Venus is in Stainless Steel Pipe segment

The latest investor PPT from Jun 26th gives a comprehensive overview of current operations and expansion plans. Request all to go through the same, so that basic queries can be avoided on the forum.

https://www.bseindia.com/xml-data/corpfiling/AttachHis/402e10ea-cc88-4564-b0e9-78d3b085dfaa.pdf

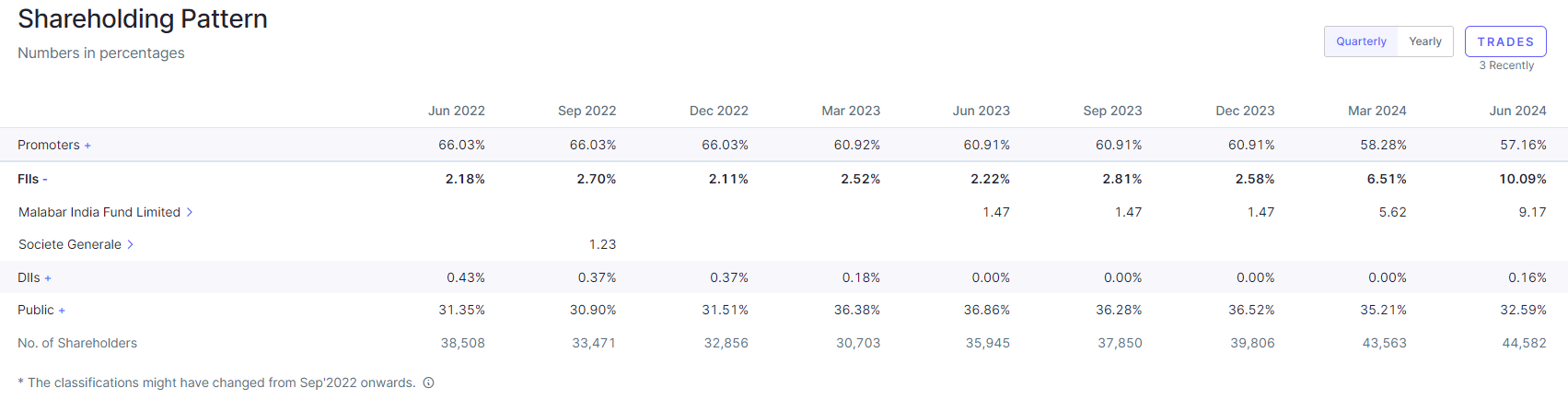

Malabar India (of Sumeet Nagar) has been acquiring a significant position over the past few quarters

5 Likes

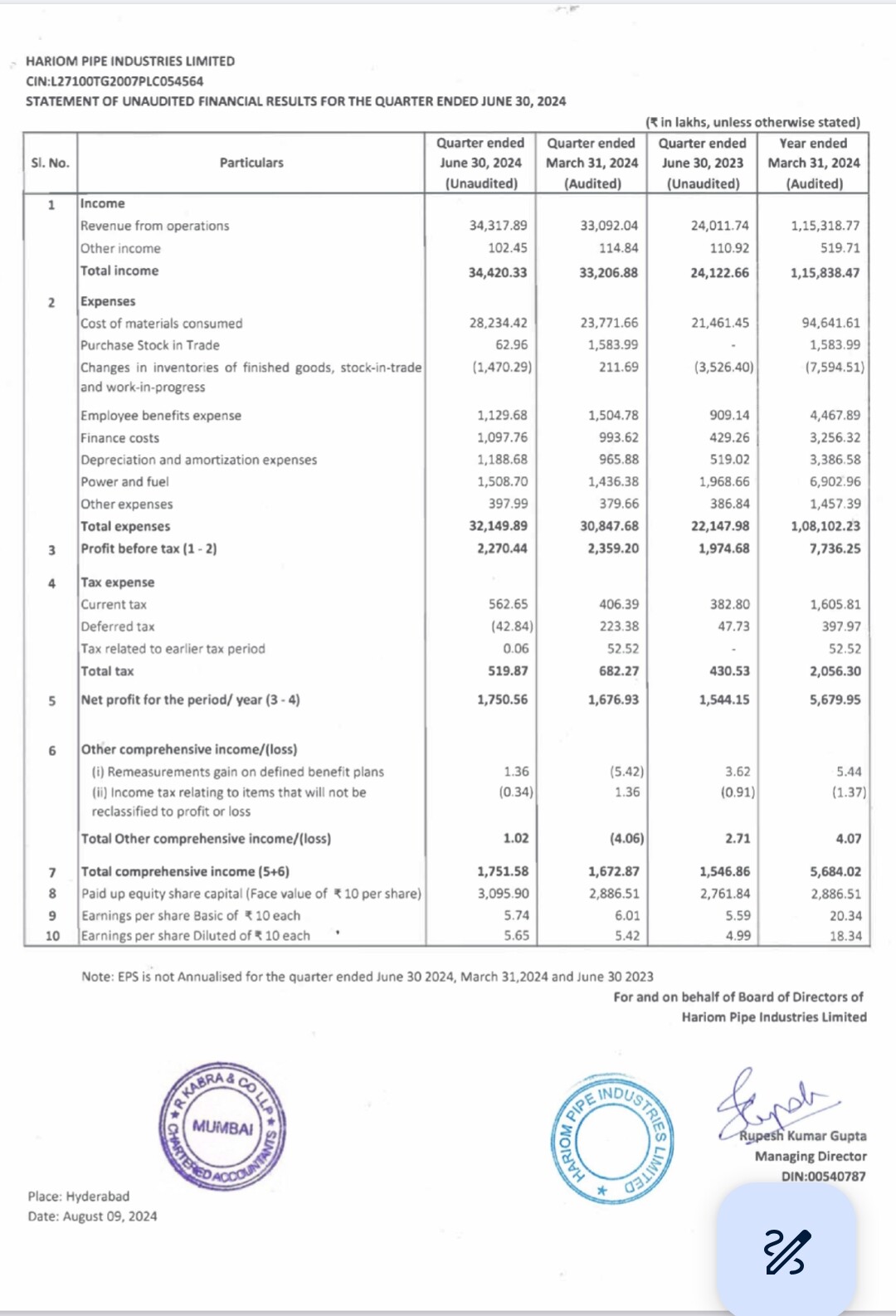

Excellent results from Hariom

Total Income of ₹344.20 Crore, up 43% YoY

• EBITDA of ₹45.57 Crore, up 56% YoY

• PAT of ₹17.51 Crore, up 14% YoY

I dont know why market took it negative i see upside once people understand the results correctly i think this will be last quarter for major interest burden

2 Likes

I find it decent to good. PBT is actually lower QoQ. But this does not change the long term thesis. I am confident about it.

1 Like

The result should be compared yoy. Qoq comparison is not right in this one

Hariom Pipe Results

Very Good Results beyond my expectations

Revenue up 43% YoY n Flat QoQ

EBITDA up 59% YoY n 6% QoQ

EBITDA margin at 13% vs 12% YoY n 12.6% QoQ

PAT up 13% YoY n 4% QoQ

Finance cost up

Operating Leverage now comes in Play (QoQ momentum started)

Overall very good set… Q1 is weak for sector and then too it has beaten Q4…

Might be Revenue expectations were high from market but Hariom has clearly beaten on Margin side

Now onwards Q1 < Q2 < Q3 < Q4

Based on guidance FY25 Revenue would be 1650-1750 Cr

Q1: 343 Cr

Left: 1300-1350 Cr

If Revenue would be around 375 Cr than it would be real beat… but still track this number whether they would able to achieve this or not

Debt free target till FY27

No Reco

10 Likes

From next 1-2 quarter onwards eps should blast off as revenue goes up

1 Like

New Investor Presentation released today is worth a look

Very Detailed one

Link: https://www.bseindia.com/stockinfo/AnnPdfOpen.aspx?Pname=83f2e395-b656-4467-a544-7816d617362a.pdf

Almost all the triggers are covered in this 2 slides + management is very much focused on such incentives

Better time ahead

Enjoy the Ride

3 Likes

Thanks Swapan,

You have been consistent with updates & your conviction on this script.

Due to recent run up valuation seems slightly streched from FY-25 stand point.

But I do believe company is poised for future.

I expect EPS in the bracket of 25-30 for FY-25, with that metrics it seems slightly expensive.

But I also think intrest cost is gonna peak at around 40 and FY26 onwards we will see reduction in intrest cost that along with revenue growth will add fuel to EPS and we may land at somewhere around 50-60 EPS numbers in FY27 if not in FY26

So with a slightly longer time horizon stock still looks attractive.

Disc: INVESTED

2 Likes

Thanks Jhon,

Absolutely correct with your thoughts

From FY25 perspective it looks little expensive around 30-35x PE, but just one yr forward P/E will be back in the range of 15-22x

Market might start discount FY26 earnings if Q2 would show good growth

If holding from lower level then be invested… it would suprise many with its execution skills

Disclosure: Invested & Fully Biased

1 Like

is management given any margin expansion guidance as business is at very low margins right now.

1 Like

My Outlook on Interview & Fundraise:

- 700 Cr is huge amount almost 30% of Market Cap, 55% of TTM Sales (Management told no fund raise required & sudden fund raise news)

- Dilution will be huge, not at all good for Investors (EPS won’t rise in FY25 as well)

- No reason given how will fund utilise

- This Q will be soft with EBITDA falling (can see consolidation or price falling near future)

Some Good parts:

- Growth outlook is intact

- Guidance is intact for FY26 + Margin will increase as suggested 8000 EBITDA per ton guidance

- Capital might be utilise in lowering debt & WC as suggested Capex is completed & utilisation is below 40% (so growth might accelerate + PAT would increase as interest rate would fall)

Let’s see what’s management says in Q2 Results outlook

+Don’t forget to track Q2 CFO number with QIP, I feel CFO is still -ve for H2… let’s see what’s number says!! If it would be -ve then might build as big Antithesis in Growth Journey

No Reco (Invested; will see what to do in Q2 when numbers come)

5 Likes