Arihant Note on Hariom Pipes

Key Highlights

-Debt to be Zero by FY27E

-Q4 would be the best quarter

-Entering new states (Gujarat, Maharashtra & Rajasthan)

-Guidance of FY26 is intact (2500 Crores)

-WC will improve going forward

No Recommendation

Biased & Invested

4 Likes

|

NO OF EQUITY SHARES |

2.89 |

|

|

|

|

|

|

FY24 |

FY25 |

FY26 |

| REVENUE |

1290 |

1754 |

2404 |

| EBITDA |

154.8 |

211 |

288 |

| PAT |

90.3 |

123 |

168 |

| EPS |

31 |

42 |

58 |

| CURRENT P/E MULTIPLE |

29 |

|

|

| CURRENT SHARE PRICE |

565 |

|

|

| FORWARD MULTIPLE |

|

13 |

10 |

This is a very basic estimate of the company’s forward earnings that I have created. I have taken the following assumptions in the table:

- I am assuming the fact that they will double their topline from FY23 in FY24, as the had mentioned.

- I am assuming the Ebitda margins to be their average ebitda margins of 12% and their pat margins of 7%.

- I have assumed that to have a top line of 2400 Crs by FY26, they will have to grow by anywhere between 35-38% in next two years (keeping in mind all the factors like capex and market size and growth and their capacity utilisation).

Fundamental things that I understand will play a role in their growth story are as follows:

Backward integration: Since they are backward integrated, they have stability in their raw material prices, which promises a stable margin if not better.

Sectoral growth: Consumption is in their favour, overall market is growing and is very unlikely to go down in the medium term.

Operating leverage: Operating leverage is going to play out for them in the next quarters.

What I can not understand is the antethesis in the comnpany’s core operations and corporate governance and the things that can go wrong for them. I want to understand that more deeply. If anybody who’s tracking thgis closely can throw some light on this.

It will really help new investors to get a deeper understanding.

2 Likes

Preciously and Very Neat estimates… Even I agree with all your assumptions + Triggers…

Trading at very reasonable valuation of below 10 in FY26 Estimates

For antithesis:

- Concentration in Revenue (Top 10 customer contributes over 50% of sales)

- Cash Flow + Debt Saga (Weak CF need to be fund with Debt or Equity… If CF hasn’t improve then whole growth + OP lvg would be messed)

- China Dumping of Low quality & price Pipes, (Although Hariom has advantage but this can harm margin profile)

- Almost all players in ERW industry is doing Capex, this can again hamper profitability if Supply > Demand

- Some Related Party transactions (But I feel it’s okay as every company has such things)

2 Likes

Anti dumping duty on China is on till 2028

If I am not wrong then Anti-dumping duty is on Stainless Pipes & not on ERW Pipes

I read the concalls, management commentary, investor presentations, got pretty excited. Just remembered today that I forgot to check one of the main things i.e. Operating cashflows. Operating cashflows of the firm are negative! Can anyone give their views why is it the case and is it normal or can be a red flag?

Disc.- tracking position. No recommend to buy/sell

I have a question, did anyone notice in Mar’23 results the cash conversation cycle and trade receivables increased heavily. Any idea why ?

With increasing loan and negative CFO does not look good unless their capex plays as per expectations

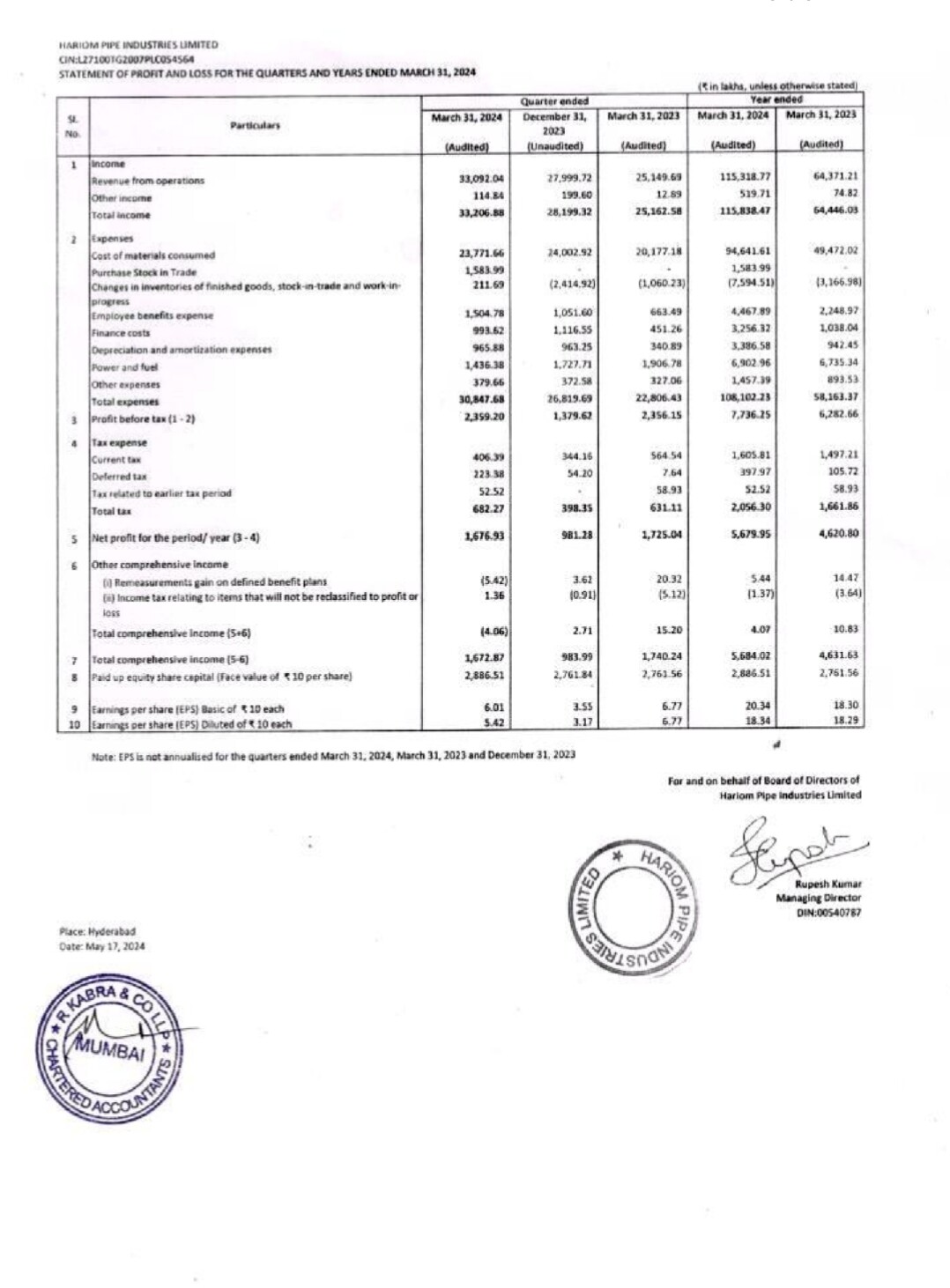

Results Q4 look good.

In a quarter when all its peers struggled to post 10% growth.

They have posted excellent topline growth.

Dep. And intrest is hurting but that will play out gradually.

1 Like

Hariom Pipes Results

Impressive Set

Sales up 18% QoQ n 32% YoY

EBITDA up 29% QoQ n 34% QoQ

EBITDA Margin at 12.7% vs 11.64% QoQ n 12.47% YoY

PAT up 70% QoQ n -3% YoY

OCF +4.95 vs -100cr YoY

OCF +ve after 5 Qtrs

Div of 0.6₹

Expectations Beaten

2 Likes

Even I Beleive Results are Good

Some Positive things:

- Margins are back to 12.5% odd levels from 11.7%

- OCF turns positive; small +ve of 4 cr but still can boost sentiments (Big +ve)

- Debt, Int. & Dep are somewhat stabilize in this Q (all thanks to OCF started improving)

- WC has started to improve QoQ

- Management is walking the talk now

Only Negative:

- Dividend… they should have wait for a quarter or two… as from dividend money they can reduce debt clearly

2 Likes

The company kept its guidance of achieving Rs.2500cr. revenue by FY26. The fixed assets/Capacity has been expanded and kept in place… But still 0.8 debt to equity ratio. Now it remains to be seen whether company will be able to optimise and reach revenue targets or not.

Proposed dividend outflow is minuscule : 2.89 Cr equity shares x 0.60/- = 1.73 Cr approximately which anyway wouldn’t have any material impact on debt /interest reduction.

I think its more of a signal to investors that they are confident of OCF gearing up in coming quarters.

2 Likes

Absolutely Agree…

Just I feel they should have waited to further stabilize the operation as OCF turns positive after many Quarters as every penny saved will move to bottom-line

Not a Negative thing… I take my word just what I feel

1 Like

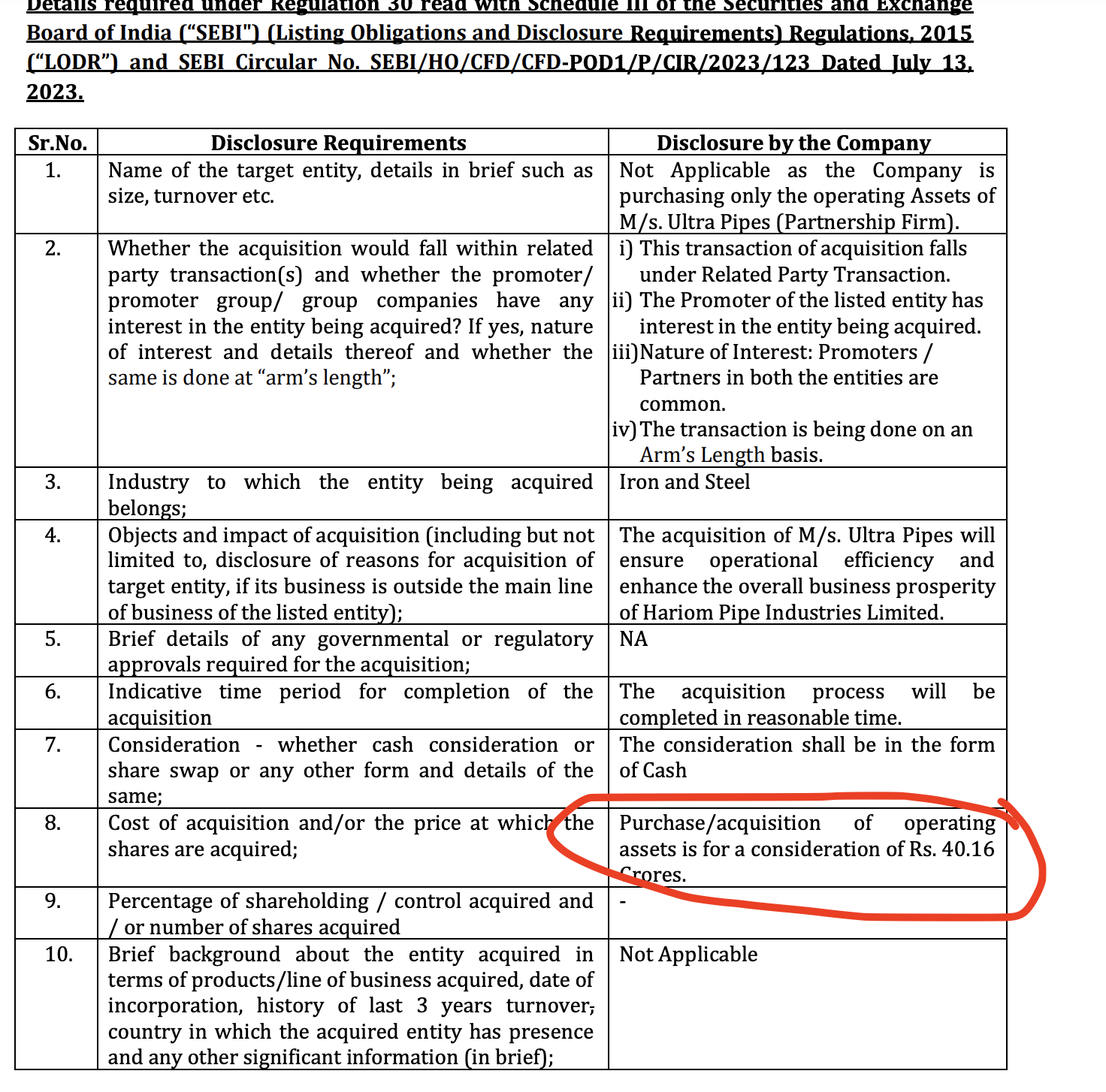

Announced acquisition of Ultra pipes operating assets for 40 cr :https://www.bseindia.com/xml-data/corpfiling/AttachLive/1199b8fa-1749-4d5a-9884-eab8290d8bf9.pdf

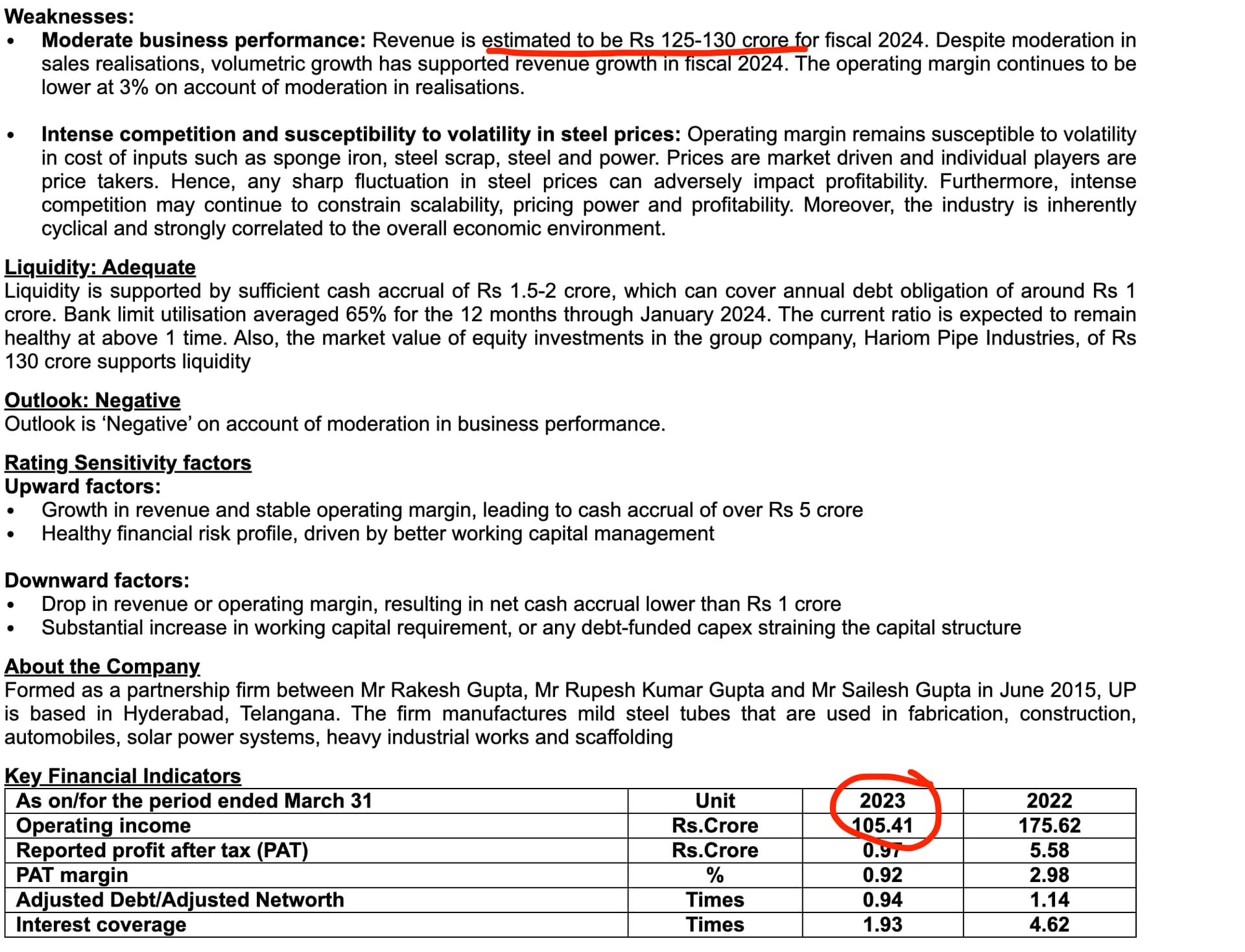

Snapshot of credit rating report of ultra pipes below : Rating Rationale

2 Likes

what will be the net impact ?? And how are they going to pay 40cr ?? Already 372 cr of borrowing they have

Now that’s an intresting development ultra pipe’s acquisition will come under "Related Party Transaction ", not sure what’s the point of it for an already debt loaded company.

There has been changed in promoter holding in March quarter.

Reduction of almost 3%.

Anyone familiar whether it was an open market sale?

In January, warrants issued by the company got converted to actual shares. This leads to the dilution of shareholding

1 Like

what advantage could you please help

1 Like