Its out - https://www.bseindia.com/xml-data/corpfiling/AttachLive/b399af4e-bdd0-4e03-bd20-2ccfa9c561be.pdf

Bad results it seems

So the sales are hit in the result.

Yupp… bad results as what price action was telling…

Sales miss led operating deleverage & PAT down significantly

Waiting for their press release if happens to know the exact reason

Yeah the price action deteriorated from middle of December. So the insiders knew this was coming.

3 Likes

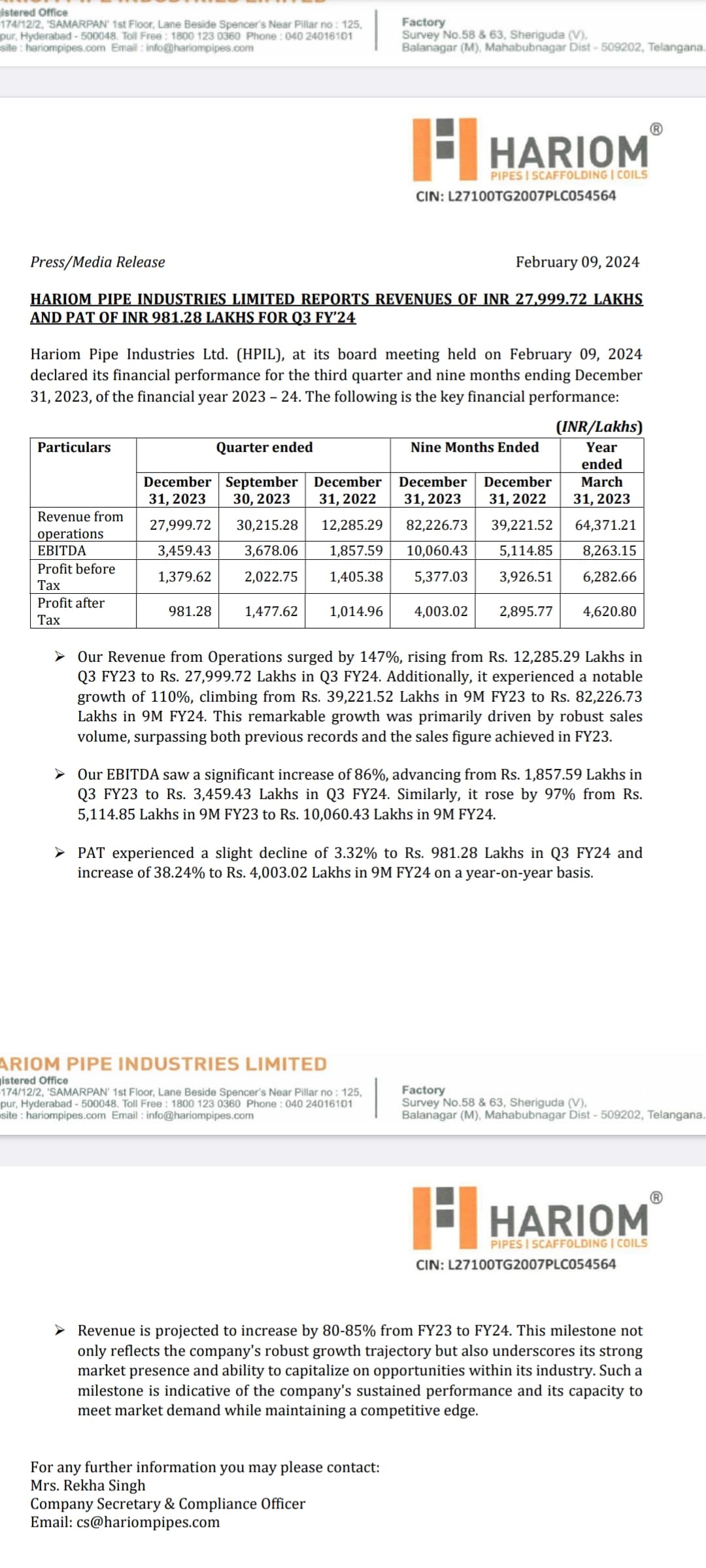

Hariom Pipe Results update:

-Revenue growth of 146% n QoQ fall

-EBITDA growth of 86% n QoQ fall

-PAT fallen QoQ n YoY led by dep & int exp

-Lack of disclosure in press release, what I believe industry weak demand + South flood had led the impact on operations

-Management released a simple press release compared to the last one which was detailed…

-Poor results were already backed in price as suggested by fall of 20% from ATH

-Behind the words guidance is given of 80-85% growth in FY24 over FY23

Q4E Sales: 360-375 cr

Q4E PAT: 15-17 cr

-Warrants money allotted can take care of Q4 WC requirements

-CF needs to be improved to have some impact on PAT & Free cash flows… if not happens then growth guidance (2500 cr revenue Target in FY26) will turn out to be a hindsight

-My honest review

No Reco

Disc: Invested

1 Like

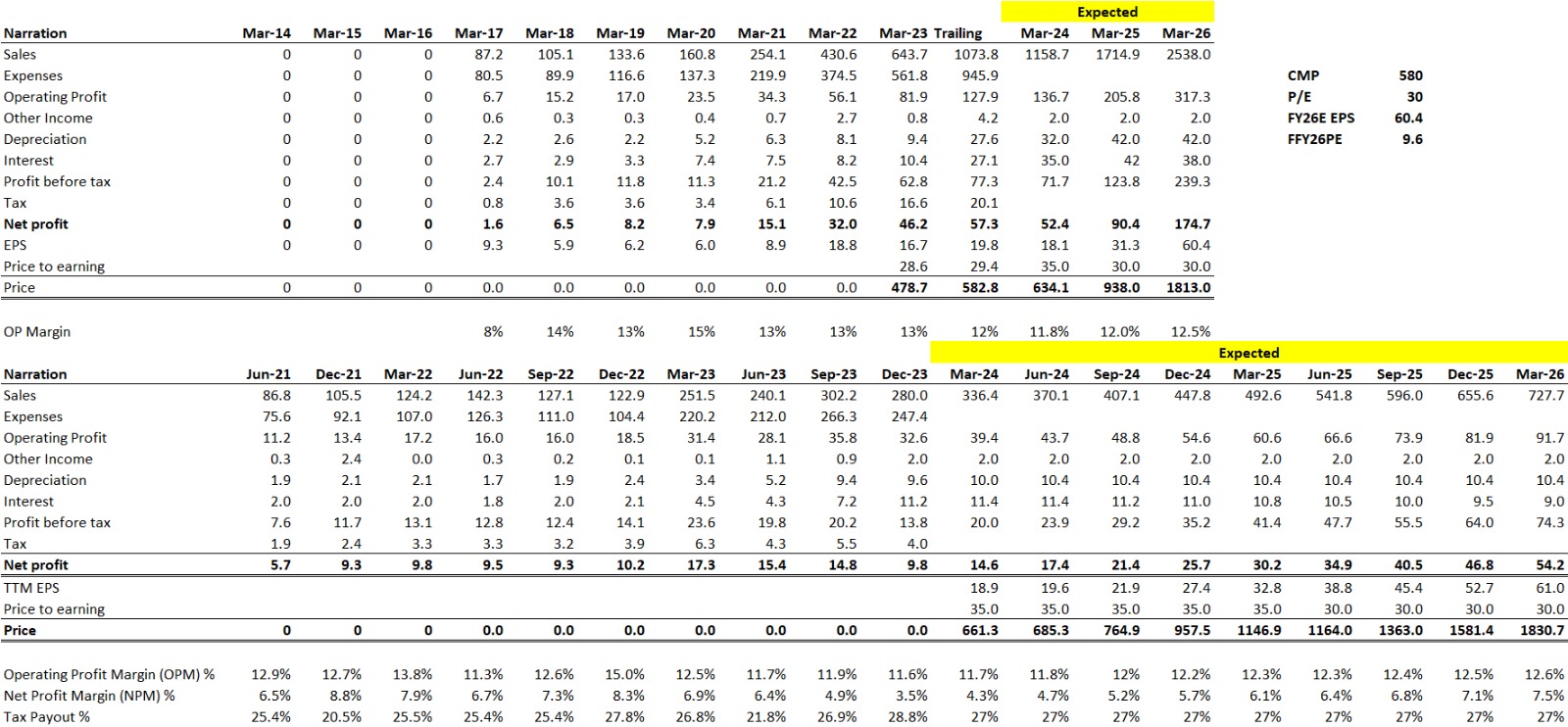

Hariom Pipes

-Made a simple financial model as per guidance given by management

-I believe the next 2-3 Q more pain ahead on the Int & Dep side… after that Operating Lvg & Economies of scale will start to kick in… if CF improves

No Reco… posted just for educational purposes

7 Likes

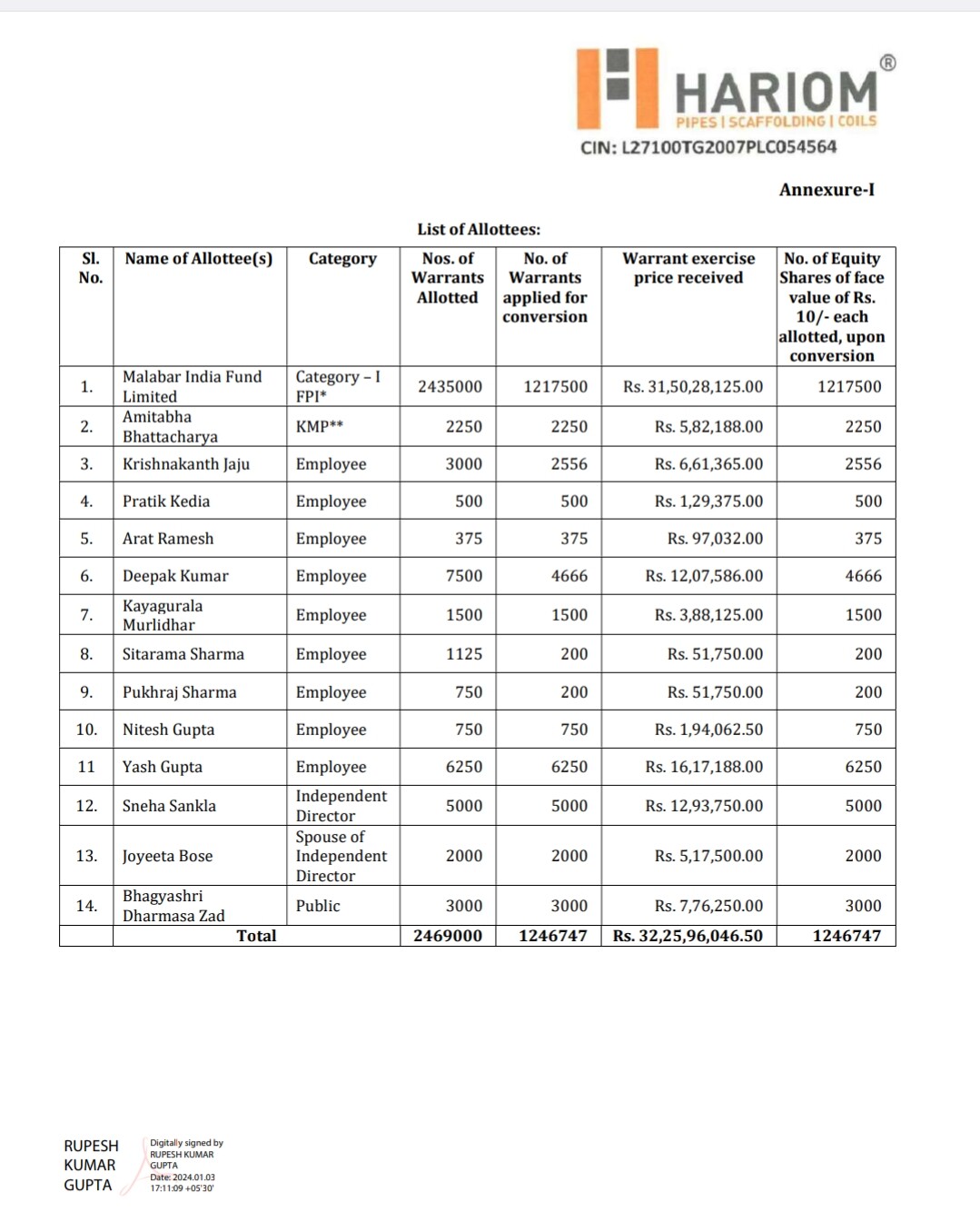

Malabar has increased stake in Jan.

But promoter has reduced the stake.

Are we expecting a few soft qtrs going forward.

Why would the promoter offload stake ?

If only these number would come to play.

We can expect that, but nothing is certain.

Bro

- Promoters hadn’t sold a single share till now (No. Of share still holds same)

- Conversion of Warrants leading to No. of share O/S increase & this shares are allotted to Malabar & other investors, which led the Malabar stake rising as a % that much and promoter % wise falling

List of Allottees

Nothing is certain…

My Assumption only comes true, if:

- Cash flow improves

- Operation stabilize

- Above 2 leading to WC normalise & Debt reduce

- Operating Lvg + Premium products come into play (which lead to margin expansion)

Sales growth I fell is not at all a concern as they are giving enough growth

If CF Improves & Margin expand… I will be more than happy & satisfied

Disc: Invested & had done transaction in last 30 days

Thanks Swapan,

Yes growth story seems intact, one of the reasons i started building positions gradually.

As long as guided topline is achieved in accordance ro the forecasted growth. Int& dep on elevated levels wont hurt for next few qtrs, coz market will discount that in accordance to forward looking no’s.

Discl: started building in recently & accumulating on bad days.

2 Likes

Why does the company doesnot do concalls? Did anyone get a chance to meet the management and ask them?

I have tried mailing them but then no respond.

Disclaimer: Invested!

1 Like

Even I don’t know particularly why

But I feel they had done institution meet last year, they were not good in English speaking

I feel maybe that’s the reason… only an assumption

The managment have interviewed in fluent english in the recent past.

Guiding revenue of 2600 by FY-26, thats around 2.5 times of FY24.

Thats a big target, lets hope & see if they deliver on that, i would be happy if they come close to it.

If the projection stands true we xan aim for around 30-45% topline growth in FY25.

I have doubts value added products aline can make 40% odd percentage of total revenue mix in such a short span of time.

1 Like

- Fy24 is expected to be between 1160-1190 Cr as per the last quarter press release (80-85% growth over FY 23)

- The above translates to nearly 340-370 Cr sales in Q4-> this will be the highest ever quarterly sales, and if the EBITDA margins sustain, 40-45 Cr ebitda

- FY26 target of 2500 Cr will be nearly 2x of FY24 ( in the arihant capital interaction - available on youtube, they have mentioned the internal target of 2500 Cr in calendar year 25 itself, so FY 26 might be slightly higher if they sustain.)

- In case they achieve these numbers , stock price should reflect this trajectory over next 8-10 quarters

Disc- Invested and biased , holding from 590 odd levels.

4 Likes

i have started tracking this script, i am wondering why was the reason for resent fall if apl apollo can have PE of 50 why does this fellow at 22 times,

i really dont know how is management is it reliable and does they keep promises of 2500 cr sales

I had mailed to the company and they replied me as follows.

Dear Sir,

First of all congratulations to the team of Hariom Pipe Industries Limited on a great set of numbers in Q3 of FY 2024. Company is on the way to achieve its goal of ₹ 2,500 crore revenue guidance by FY 2026 without compromising on probability. Company did a great job in every parameter. However, I wanted to know the following things because I want to understand the company in a deeper way as I’m an investor in this company.

- Company do exceptionally well, then why company not hold earnings conference calls?

- Why is the company is not cooperating with rating agency i.e., CARE RATINGS?

- Is there any planning to raise equity funds in the foreseeable future?

It is requested to reply to the abovementioned. Quick reply will be greatly appreciated.

Dear Mr. Sumit,

Thank you for your congratulations and keen interest in the performance of Hariom Pipe Industries Limited. We truly appreciate your support and dedication to understanding our company in depth.

Allow me to address your queries:

-

Regarding earnings conference calls, while it’s true that we haven’t held such calls in the past, we are actively working on initiating them in the near future. We understand the importance of transparent communication with our valued investors, and conducting earnings conference calls will be an integral part of our efforts to enhance shareholder engagement.

-

Concerning our cooperation with rating agencies, we want to clarify that Hariom Pipe Industries Limited has been engaged in an External Credit Rating process with CRISIL LTD for the past 4 to 5 years, resulting in an A- Rating. The agreement with CARE RATINGS had lapsed, but they retain the authority to continue the process. We are currently in discussions with CARE RATINGS to formally conclude the agreement and withdraw the rating process from their purview, adhering to all legal procedures.

-

As for raising equity funds, there are no immediate plans to pursue this avenue. We believe in prudent financial management and are committed to exploring various financing options to support our growth ambitions without compromising on the interests of our shareholders.

It’s important to note that Hariom Pipe Industries Limited remains dedicated to keeping our shareholders informed about all significant developments related to the company. We consistently update pertinent events through the stock exchange, ensuring transparency and accountability.

Furthermore, we are actively working on organizing conference calls with our shareholders, providing a platform for direct interaction and sharing insights into our performance and future prospects.

Your continued support and interest in Hariom Pipe Industries Limited are invaluable to us, and we look forward to your ongoing partnership as we navigate the path to sustained growth and success.

Thank you once again for your inquiries, and please feel free to reach out if you have any further questions or require additional information.

Thanks & Regards

7 Likes

Yesterday only there was conference here is the summary of it

-

Difference between hariom and other players is that Hariom has it’s own raw material and that’s why the margins are higher and they don’t use coal- it’s eco-friendly

-

Some of the products can’t be made by their competitors and they have a monopoly in certain value added products

-

Saved nearly 26 crores in power cost in the last

9 months due to 2 MW renewable power capacity

They will help with dealer financing in order to bring receivables down significantly -

Will start dividend policy from next year

-

Guidance for this year is intact

-

Right now, 50% capacity utilisation - there was a small delay in the latest plant - can go to 80% next year

-

Not competing with JTL and Apollo because they are into customised products, so it’s a different customer and different application - mostly into infra, fan, auto - Working with Asia’s biggest fan manufacturer

-

Q4 will be the highest topline ever - crossed

1100 crores by February already -

Scaffolding EBITDA per tonne is 12,000 but the volume is low as this is a customised product. Rs, 8,000 Rs for galvanised pipes and 7,400 for MS pipes - average is lower due to coils and the average holding period is 15 days

13 Likes