@gurjota hello gurjot, yours is an interesting portfolio…I wanted to know your views on bandhan bank against the backdrop of their recent results.

@ap1990 Thanks for the question.

I myself am invested in Bandhan Bank and given my learnings & changes in investment philosophy over the past couple of years, I would have never made this my highest allocation and consider that a mistake. Now, let me explain what I mean by this in more detail.

As a fundamental investor inspired by Buffett and Munger, I should think of every stock I purchase as taking part ownership of a business. So what is the business of Bandhan Bank?

It’s basically in the business of lending money and collecting that money with a wide interest spread/margin to pay off creditors, then deduct operational expenses, provision for NPAs and pocket the left over as profit for shareholders. And as you can realize, this is a business which will not make you much profit initially due to the opex, provisions, etc. as you need to really grow to a decent size and realize economies of scale before meaningful profits start rolling in.

Now if you understand this, you’d realize that banking is really not a very good business. Any kind of shocks to the economy (demonetization, GST, Covid, etc.) - banks and lending institutions get hit first! With so much economic and business uncertainty, this makes banking a (semi) cyclical business. Lending money is easy, but collecting that money in a timely fashion at an appropriate rate of interest is darn difficult.

But when we add leverage to the equation i.e. borrowing money and then lending it further which is what banks do as their balance sheets get levered 5-10x of equity, it becomes one of the most dangerous businesses to invest in.

Despite the above, you may say there are many successful banks like HDFC and Kotak in the market. However, the base rate is very low - you can pretty much count the list of successful long term banking wealth creators on your fingers. And that is why, well run institutions like HDFC and Kotak get rich premium multiples in the market. However, every bank (including HDFC / Kotak) faces the same risks and can go the way of a Yes Bank / PNB tomorrow!

Why? Just invert this quote - “I learned this very early, it is very hard to go bankrupt if you don’t have any debt" - Peter Lynch

Btw, there are different types of business models even within the lending universe which can help mitigate the general business risks and those with asset backed (gold, property, etc.) lending generally are amongst the safer business models within the lending space.

So even within the lending institutions, Bandhan Bank’s business model is amongst the most dangerous one with unsecured microfinance lending.

So that should be the first mental model in your head - is Bandhan Bank’s business a business that I want to take part ownership of?

If yes, the second mental model is how much are you willing to pay for that business? I’d leave that question up to you to answer as I don’t have the ability to predict the future profits of such an unpredictable business model and what might future NPAs look like (currently surging at 7% reported and 13% of total loan book incl. SMA1 and 2). However, if you can predict the future profits - my book value multiple for buying the business would not exceed 3-3.5 P/B no matter how bullish the outlook.

My 2-3 year view - There have been a slew of negative overhangs in the past few years (high priced acquisition and integration with Gruh Finance, CAA and NRC protests in Assam, Covid wave 1, wave 2 lockdowns, Bengal/Assam elections, etc.). I expect the company to enjoy some blue sky territory maybe 6-12 months from now just like the Indian economy and gain back market participant trust in the business model for a few years (at which point I plan to exit) before the next big economic shock repeats the cycle.

6 Likes

@gurjota thank you so much for the detailed answer. I have also made the same mistake. Bandhan having the highest allocation in my portfolio. I am also waiting for an oppprtunity to exit.

I don’t know what price you got in. But I cut down my position by 50% in December rally at a negligible loss.

You can also see in my January post, it’s no longer in my top 10 holdings.

My average is 419. I am expecting to cut my losses once the covid situation is better and the price rebounds a little.

Well, I think the market gave an opportunity for exit in Dec-Jan around your buy price. Curious why you didn’t exit then?

Now given the latest Q4 results, I do not foresee a dramatic rebound and the business seems to be getting derated in my view. Could be sometime before it goes back to 52 wk highs and many many years before it goes back to all time highs.

PS: I could be totally wrong as well

Monthly Portfolio Note - May 2021

There’s an old adage in equity markers “Sell in May and go away”. Thankfully, I wasn’t listening to whosoever recommended that as it would have deprived me of the largest monthly absolute gains in my investing journey till date (saying that at the risk of markets cutting me to pieces on Monday - the last day of May).

I had predicted in August last year that I expect the mid/small caps to come roaring back after a painful 2.5 years but I couldn’t have ever imagined the velocity at which this will happen.

The rally over the past few months has been extremely broad based and something also highlighted in Samit Vartak’s latest memo. Referring to the same - 99% of the smallest BSE 500 companies (i.e. 401 to 500) have delivered positive returns in the 13 months till April 2021 and pretty confident the trend only increased in May 2021.

Market have been very kind and rewarding personally as well, it’s been an absolutely phenomenal month of gains equivalent to a full year’s salary of mine just 5 years back of 2016. Also already equaled the full year 2020 returns in just 5 months.

So what do we do now? Where do we go from here?

I’d like to use a cricketing analogy of attack and defence. Think of this as a Test match where we are still on the 1st day of the match with about 80 overs bowled in the day. However, if we rewind to start of play (Feb 2020) it’s an astounding come back where the first hour of play was disastrous on a green seaming wicket (read Covid and March 20 market crash) and 4-5 wickets were lost for very few runs.

Then with all 11 fielders in catching positions and lots of open gaps, the batsmen (central banks, governments, corporates) decided to go on a Rishabh Pant style all-out counter attack (interest rates, stimulus, corporate cost rationalization). And that attack has paid off handsomely with a very strong comeback in the last 4-4.5 hours of play.

Now with 80 overs gone and batting going strong, it’s time to think about the next day and not the next 10 overs. The new ball (commodity inflation, valuation, slow Covid 2.0 unlock) can do a lot of damage and clean-bowl the whole team if not played cautiously.

To sum up, I think it’s time to be slightly cautious about the future (next 3-6 months), closely evaluate Q1/Q2 earnings before deploying fresh money or even take some off. Majority of the cats and dogs are also selling at the price of horses in this market.

Exits

Chemcrux and Jubilant Ingrevia - Both were fancied sector based undervaluation plays for me and never core portfolio bets. The pace of returns of both has been astounding and almost feels like successfully doing a shoot and scoot operation. Chemcrux has given me 70% in 3 months and Ingrevia doubled in less than 2 months. Both have combined to literally wipe of my entire losses in IBHFL in just 3 months combined. Thanks a lot to @Chins for highlighting the environmental risks with regards to Ingrevia’s plants.

With regards to Chemcrux, I tried to highlight in the Feb post when VPers were selling their holdings cheap, that nothing really has changed for the business. And I stand by that today as well and this could very well be 2-4-8x from here. However, I realized that the environmental concerns and ESG as an investing filter will always be like an albatross around my neck. These 2 cyclones are all an impact of global warming, carbon emissions and not taking care of our environment. If ever India decides to go the way of China, these will be the hardest hit companies. Why take that risk when there are so many other fish in the pond especially when you’ve already been handsomely rewarded. So, I quit.

Reliance - Only sold for raising cash assuming it won’t go anywhere like the last 8-9 months and will look to enter again soon. But then days like today make you regret. Let’s see if we ever see those levels again.

3MIndia - I realized that doing blind Coffee Can Investing may reward you, however I can never develop the conviction to hold it during tough times. And this business is something I find very hard to track and monitor without any investor presentations, conference call, etc. Exited with 50%+ gains again.

Kajaria - Fabulous coffee can investment again, I didn’t want to get out of this, however needed the cash to get into other opportunities mentioned below and this seemed the most fairly/slightly overvalued business from a 1-2 year perspective. 2.8x returns in a year - keep searching Saurabh Mukherjea style and keep getting rewarded.

New Addition

Tips Industries - This caught my eye from @ankush12495 's blog post and seems like a terrific digital play to me piggybacking on India’s growth potential of smartphones, internet, social media and last but not the least music streaming.

I know the management here is not top notch and also seemed to have an eye on valuations of similar companies in USA (billion dollar valuations) in last con call but at 20-25x trailing earnings and 25-30% growth over the past few years, I find it a great bet for the next 3-4 years. As music streaming apps consolidate, there could be pressure on the licensing fees paid out to these music labels but feel we’re a few years away from that yet.

Britannia - Now this is strange! I barely exited in Feb and have re-entered here. If I refer back to my attack and defence methodology, this is a form of defence for me with the current run to the moon. I’m using this as a hiding spot in the market from some of the other sold positions (Chemcrux, Ingrevia, etc.) proceeds. And very confident of getting a peaceful 12% CAGR (10-10.5% growth and 1.5% yield) at current valuations over the next 10 yearsa after the heady run-up of last few months.

Ugro Capital - Very well covered thread on VP already. Taking a small punt on this given the highly unlevered balance sheet from a NBFC perspective and expected strong bounce back of financials over the next 2-3 years.

Increased allocations to IEX, Goldiam, Neuland after 3 down circuits, MAS Financial, Mindspace REIT

13 Likes

Congratulations! Finally you are getting your mojo back. Being myself the king of diversified holding:) Liked your diversification pf angle. Great sharing and also liked the cricket analogy part and quick course corrections in Britannia. What’s your thought process behind allocating 2nd highest weight towards office reit? IMO tailwind sectors should get capital rotation atleast 20% for couple of years. What is your thought in this direction?

3 Likes

Thanks for the kind words.

In terms of REIT weight - this is a form of diversification for me as I don’t own any real estate and want to have min 10% real estate in my net worth. And REITs have little to no correlation with equity market performance. So this is a good stable way of creating a passive income stream at 6.5-7% post tax yield (as I’m in 30% tax bracket, it works out to a 10% pre-tax yield) with multiple growth optionality built in - annual rent escalation of 4-5% or 3 year rent escalations of 12-15%, MTM re-leasing spread as compared to current market rents and increasing rent by developing unutilized land owned by the REITs.

Thinking 10 years down the line - I don’t expect interest rates to be at 6-7%, best case scenario they would be at the current levels or further down. So with 4-5% bank FD rates - this seems like a great way to protect your capital with moderate growth.

I didn’t quite follow what you mean by “capital rotation at least 20% for couple of years”?

PS: The portfolio performance I share is including the REITs which have not done anything in the past 4-5 months and just a drag on the performance as of now. Also I do not include their hefty dividends or any other company dividends in my calculations. So I’d say I’m rather happy seeing 15-20% CAGR growth of net worth including REITs. Something I’ve emphasised before as well on the forum, people seem to obsessed with individual stock analysis or equity portfolio performance rather than focusing on net worth CAGR.

5 Likes

Congratulations on amazing feat! Either your portfolio size is significantly higher than your yearly salary or in this one month the returns have been phenomenal…in either case, it’s a great achievement!

2 Likes

How much percent of portfolio you have invested in Britannia? It seems from your post that this time you have not set a target for this stock but rather prefer holding for very long term…is that correct?

Also would be good to know what you did and thinking about your Abbott holdings…thanks

Actually I mean to say that in last couple of quarters we have seen a very good tailwind in pharma, Healthcare services, chemical, specialty chemicals with clear advantages for coming 2-3 years. So doesn’t it makes sense to rotate capital in these sectors to reap the benefits? Have you evaluated the favorable risks reward in medium term at pf level? Thanks for sharing your view on reit investment. I liked it planning to accommodate in my pf.

1 Like

Thanks! Yes portfolio is significantly larger and also the gains are equivalent to my income from 5 years back 2016, not as of today ![]()

Allocated about 1.8-2% of PF to it. Yes I want to hold this for the long term as its a fantastic growing foods business with so many successful brands entrenched in consumer minds. And the current valuations of 40-45x are absolutely acceptable for an essential FMCG business. If these businesses don’t deserve to command these multiples then nothing else does. So with limited risk of derating (other than any promoter / corp governance issue) all in all it’s a great opportunity to peacefully compound your capital at a reasonable rate.

If I can use a driving analogy this is a 4th gear type of investment after having driven in 6th gear for a long long time without an accident. As you know driving in 6th gear will not be sustainable for very long periods of time.

So now I want to protect and reasonably grow the gains from the recent heady run. If we go into blue sky territory again in a few months (very strong earnings, no change in interest rates, etc.) - may look to move back into 6th gear. My typical style of investment is between 4th and 5th (growing earnings between 15-20%).

I have very similar thoughts on Abbott, it’s growth is a lot better but then it’s multiples are also comparable with Britannia and an established FMCG foods business is a much better business according to me. So net net - at their current valuations both are 4th gear investments for me.

2 Likes

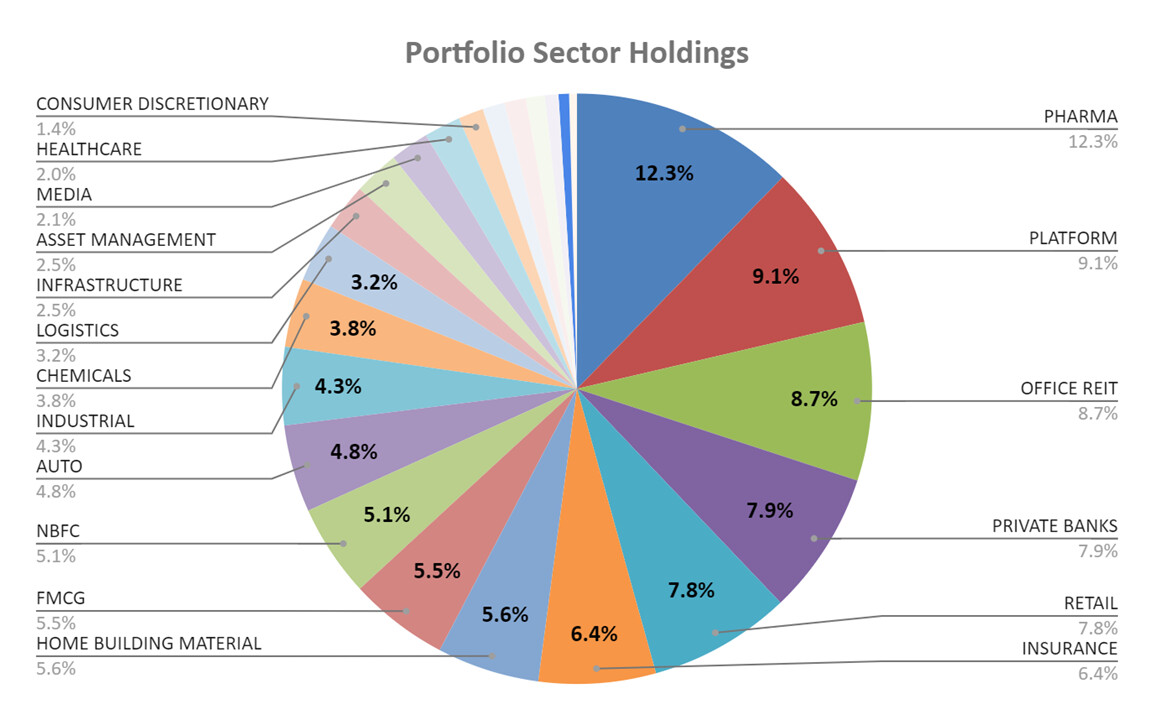

So I currently have 15% portfolio exposure to pharma, chemicals and healthcare. I know that pharma and chemicals have delivered excellent earnings and have strong tailwinds for the next few years as well. However, to take large concentrated bets - I need to have an edge in these sectors in terms of my business understanding or actually working in that sector. I have neither at the moment and this would result in me feeling very vulnerable if there were some big shocks to any of these sectors and not allow me to sleep peacefully at night. Hence, I diversify across multiple sectors and I genuinely believe you can make money in almost every sector as there are 150-200 excellent businesses / managements in India across different sectors.

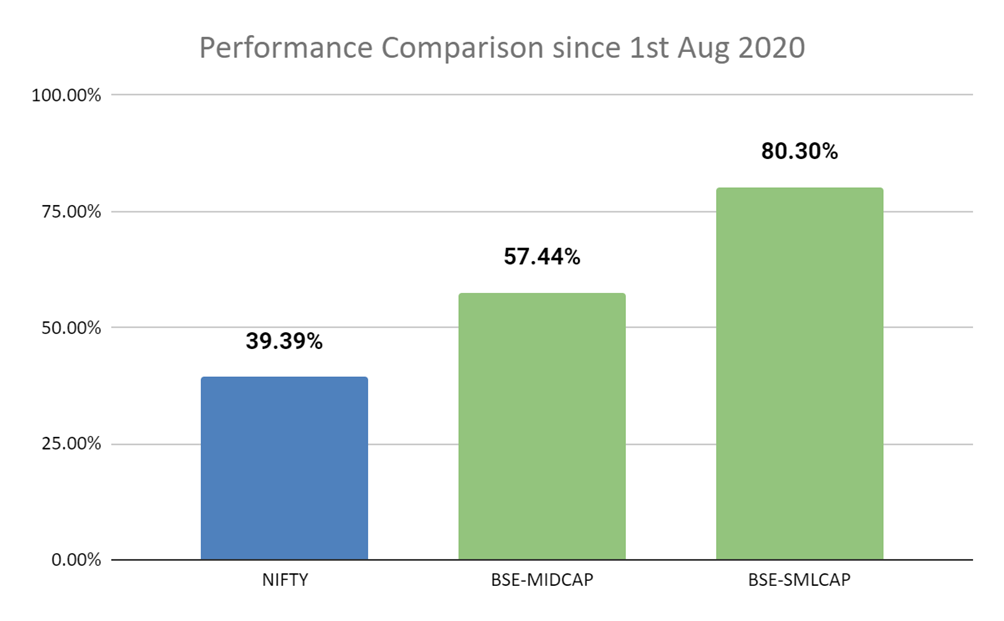

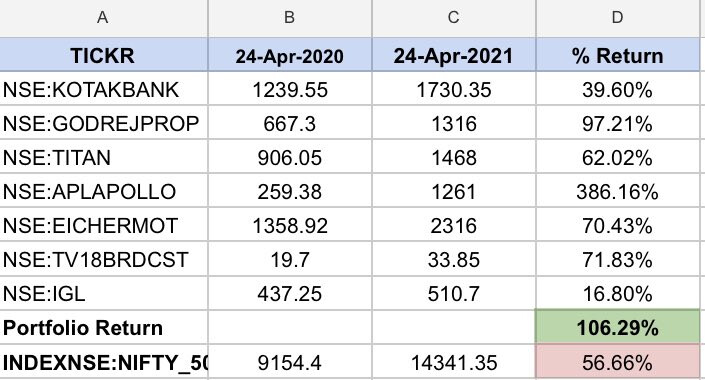

Here’s an example. A fintwit with more than 100k followers had recommended in April 2020 to stay away from 7 sectors which will suffer badly due to Corona. I questioned the wisdom by creating a model portfolio of some of the best market leaders from those very sectors. Here’s the result:

My objective is to build a diversified bullet-proof portfolio which lets me sleep peacefully by betting on the best Indian businesses across sectors. So basically, my portfolio should perform badly only if the future of India as a nation is in doubt or some global event / crash and not if 1-2 industries fall by the wayside.

Disc: Invested in 5 of the 7 - Kotak, Titan, APL Apollo, Eicher and IGL.

PS: There is 1 SME pharma company Beta Drugs on my radar which I sold last month and may buy back at a much higher premium. Management has guided for very strong growth for the next many years, you should go through the latest concall and transcript - full of distinguished VPers who could be behind the massive run up in the stock in last month.

10 Likes

Monthly Portfolio Note - June 2021

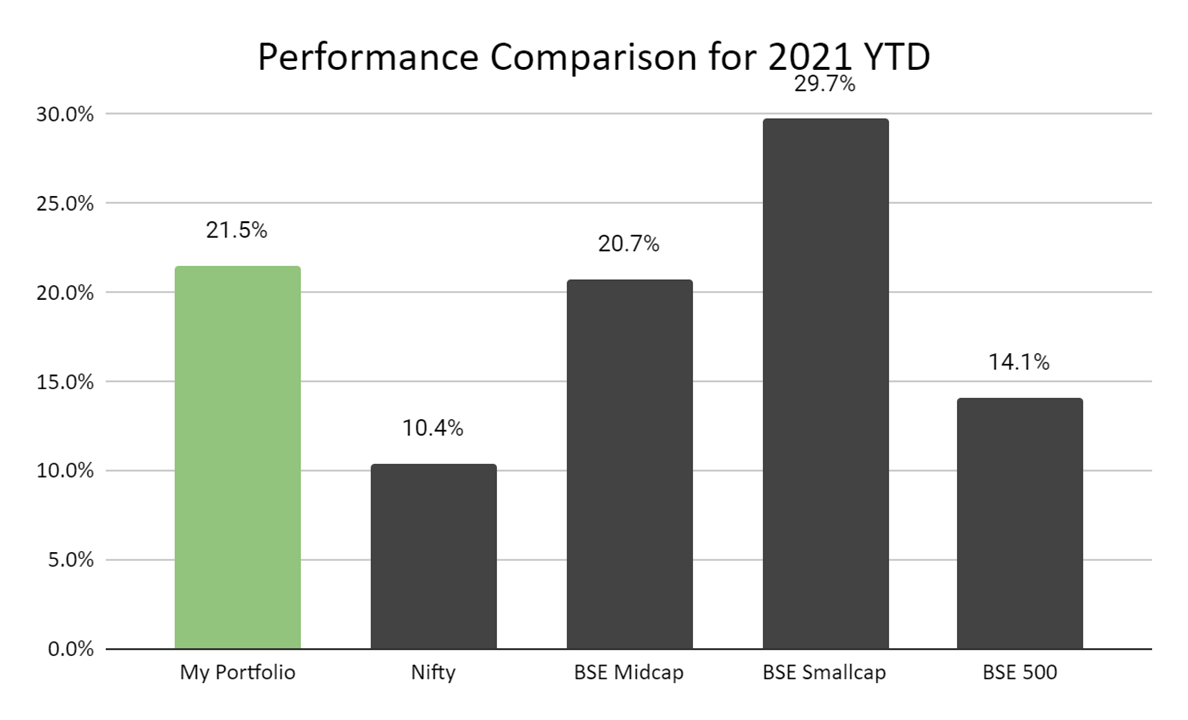

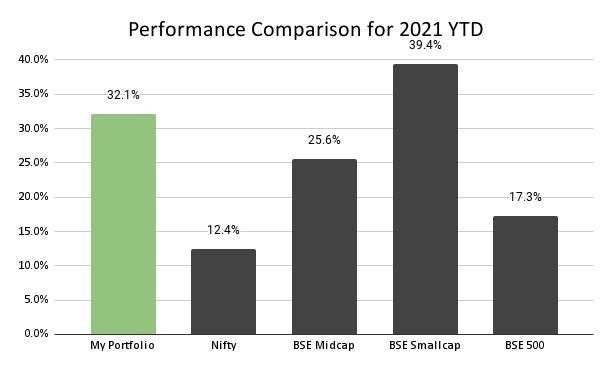

Gratitude! Rather bucketsful of gratitde! That’s the only way I can express my feelings on how rewarding the market has been in the last couple of months and it has been another month of stunning gains in the portfolio for me. The YTD performance chart explains this better (note that my PF performance includes more than 10% capital allocation to REITs which are quasi-equity instruments and excluding them the gains would likely be north of 40%). So exception has this year been, that my overall PF CAGR since inception (2015) has now crossed 17% which was at 10.8% at the end 2020. Overall, I’m starting to get nervous about the one way ride to the moon in the broader market, looking to get out of my positions / take some capital off wherever I don’t have good visibility on long term business performance.

Going forward, I will be posting my portfolio here on a quarterly basis or as per the request of any forum member if it is useful for anyone. This month’s strong gains have been led by many companies based on Q4 results / market discovery and few other triggers - Tips, Laurus Labs, Polycab, Acrysil (8x for me now), Macpower (NSE SME migrated), Bharat Rasayan, RACL Geartech and few others.

Core Portfolio - Strong established business models with good growth expectations

| Company Name | Mkt Cap | Buy Avg | CMP | P/L % | Current % |

|---|---|---|---|---|---|

| EMBASSY | 33,165 | 339.5 | 350.00 | 3.1% | 5.28% |

| ICICIBANK | 439,819 | 292.7 | 631.45 | 115.7% | 3.46% |

| ICICIPRULI | 88,099 | 346.2 | 613.25 | 77.1% | 2.83% |

| POLYCAB | 29,382 | 864.8 | 1970.00 | 127.8% | 2.50% |

| LAURUSLABS | 36,476 | 237.0 | 691.50 | 191.8% | 2.47% |

| INDIAMART | 21,266 | 2241.8 | 6999.00 | 212.2% | 2.06% |

| ACRYSIL | 1,666 | 74.9 | 623.00 | 732.3% | 2.03% |

| VMART | 5,555 | 1678.1 | 2817.95 | 67.9% | 2.03% |

| ITC | 249,500 | 179.7 | 202.70 | 12.8% | 1.91% |

| BIRET | 8,156 | 225.9 | 268.32 | 18.8% | 1.84% |

| ICICIGI | 71,291 | 1140.9 | 1565.10 | 37.2% | 1.82% |

| IEX | 11,221 | 291.6 | 375.90 | 28.9% | 1.78% |

| HDFCAMC | 62,164 | 2309.3 | 2916.00 | 26.3% | 1.72% |

| TCIEXP | 5,540 | 581.0 | 1435.45 | 147.1% | 1.67% |

| PAGEIND | 32,960 | 18719.2 | 29550.00 | 57.9% | 1.62% |

| HDFC | 446,976 | 1830.8 | 2477.70 | 35.3% | 1.61% |

| STAR | 6,810 | 775.0 | 759.00 | -2.1% | 1.56% |

| MINDSPACE | 16,763 | 288.9 | 283.00 | -2.0% | 1.55% |

| HDFCBANK | 823,352 | 1189.4 | 1497.00 | 25.9% | 1.54% |

| POLYMED | 9,801 | 220.4 | 1022.20 | 363.7% | 1.51% |

| KOTAKBANK | 338,875 | 1239.5 | 1704.90 | 37.5% | 1.46% |

| MASFIN | 4,676 | 748.0 | 856.55 | 14.5% | 1.44% |

| HDFCLIFE | 138,793 | 447.1 | 688.00 | 53.9% | 1.42% |

| IRCTC | 32,624 | 1494.3 | 2039.00 | 36.4% | 1.40% |

| INDUSINDBK | 78,707 | 1297.9 | 1015.00 | -21.8% | 1.39% |

| INOXLEISUR | 3,773 | 306.8 | 308.10 | 0.4% | 1.37% |

| ASALCBR | 876 | 294.6 | 486.90 | 65.3% | 1.24% |

| BHARATRAS | 6,079 | 8988.3 | 14750.00 | 64.1% | 1.21% |

| BRITANNIA | 87,883 | 3377.0 | 3652.90 | 8.2% | 1.20% |

| HCLTECH | 267,418 | 858.3 | 985.45 | 14.8% | 1.18% |

| TITAN | 154,284 | 888.7 | 1737.25 | 95.5% | 1.11% |

| DIAMONDYD | 1,577 | 510.3 | 670.00 | 31.3% | 1.10% |

| CERA | 5,843 | 2211.5 | 4490.80 | 103.1% | 1.08% |

| MUTHOOTFIN | 59,398 | 1149.0 | 1478.15 | 28.7% | 1.06% |

| GODREJAGRO | 12,172 | 429.3 | 630.40 | 46.9% | 1.04% |

| NAZARA | 4,599 | 1539.0 | 1511.05 | -1.8% | 1.04% |

| SIS | 6,354 | 361.0 | 430.40 | 19.2% | 0.97% |

| SYMPHONY | 7,193 | 816.4 | 1029.00 | 26.0% | 0.95% |

| DIVISLAB | 116,920 | 2148.4 | 4404.60 | 105.0% | 0.91% |

| ALKEM | 38,261 | 2697.8 | 3200.00 | 18.6% | 0.90% |

| VALIANTORG | 4,258 | 1299.4 | 1568.00 | 20.7% | 0.81% |

| CAMS | 13,613 | 1824.3 | 2794.95 | 53.2% | 0.77% |

| SYNGENE | 23,205 | 508.2 | 584.00 | 14.9% | 0.60% |

| IGL | 39,028 | 403.5 | 556.95 | 38.0% | 0.57% |

| EICHERMOT | 73,204 | 1359.1 | 2674.50 | 96.8% | 0.55% |

| BATAINDIA | 20,517 | 1275.0 | 1597.00 | 25.3% | 0.55% |

| LALPATHLAB | 26,994 | 1401.9 | 3276.95 | 133.8% | 0.49% |

| FINEORG | 8,903 | 2257.0 | 2886.00 | 27.9% | 0.40% |

| SBILIFE | 100,770 | 861.6 | 1007.15 | 16.9% | 0.35% |

| Core Portfolio | 96,384 | 44.7% | 71.36% | ||

| Combined Portfolio | 69,279 | 49.7% |

Satellite Portfolio - Relatively new or small scale companies / unestablished or cyclical business model / prone to disruption

| Name | Mkt Cap | Buy Avg | CMP | P/L % | Current % |

|---|---|---|---|---|---|

| TIPSINDLTD | 1,854 | 872.6 | 1438.80 | 64.9% | 2.80% |

| MACPOWER | 159 | 49.3 | 158.50 | 221.8% | 2.77% |

| RACL GEARTECH | 378 | 160.6 | 351.00 | 118.6% | 2.47% |

| NEULANDLAB | 2,751 | 1097.4 | 2170.00 | 97.7% | 2.10% |

| RKEC | 217 | 36.5 | 90.40 | 147.7% | 1.80% |

| BETA | 279 | 271.8 | 315.00 | 15.9% | 1.73% |

| GOLDIAM | 999 | 226.0 | 448.00 | 98.2% | 1.54% |

| DELTACORP | 4,732 | 160.2 | 177.30 | 10.6% | 1.22% |

| RADIOCITY | 897 | 15.6 | 25.95 | 66.0% | 1.16% |

| SOLARA | 6,054 | 799.0 | 1685.00 | 110.9% | 1.10% |

| DBCORP | 1,767 | 69.9 | 101.00 | 44.6% | 0.97% |

| EDELWEISS | 6,482 | 125.9 | 72.70 | -42.3% | 0.95% |

| BAJAJ HEALTHCARE | 1,126 | 678.8 | 815.65 | 20.2% | 0.92% |

| GMMPFAUDLR | 6,850 | 3474.1 | 4686.00 | 34.9% | 0.80% |

| INSECTICID | 1,458 | 494.8 | 739.00 | 49.3% | 0.76% |

| PSPPROJECT | 1,503 | 386.4 | 419.30 | 8.5% | 0.75% |

| GTPL | 2,036 | 86.4 | 181.00 | 109.4% | 0.74% |

| LGBBROSLTD | 1,409 | 213.7 | 449.00 | 110.1% | 0.69% |

| WORTH | 127 | 36.6 | 80.50 | 119.9% | 0.69% |

| SAMKRG PISTONS | 207 | 117.2 | 211.20 | 80.2% | 0.64% |

| SHK | 2,375 | 51.5 | 172.70 | 235.5% | 0.59% |

| ICEMAKE | 125 | 71.4 | 79.85 | 11.9% | 0.59% |

| FIEMIND | 979 | 273.4 | 746.05 | 172.9% | 0.43% |

| U GRO CAPITAL | 883 | 101.6 | 125.25 | 23.2% | 0.43% |

| Satellite Portfolio | 1,740 | 63.6% | 28.64% |

Portfolio Exits

APL Apollo - Sold my entire holdings today after earlier profit bookings, bought at last year’s lows of 235 post split price, unbelievable 6 bagger for me in just over 1 year. Fantastic execution by management over the past few years, excellent market share gain and handsomely rewarded by the markets. However, I don’t understand steel tubes business that well and fear it is a pseudo commodity play trading at FMCG / Pharma multiples with 3+ years of growth priced in which would not end well in case of commodity downcycle.

Bandhan Bank - Have already shared my thoughts on the business a couple of posts above and I do not want to touch this business ever again. Booked a loss of -13% overall, thankfully had already sold half in Dec/Jan rally

SIS - 22% position exited in the very very generous buyback by the management 30-40% above the CMP and overall ~50% profit from my purchase price.

New Positions

Strides Pharma - Brought to my attention by Neil Bahal’s PMS newsletters and then excellent work done by @Tar. Stelis Bio is the real dark horse in this one with a very big and bright future for biotech companies in the next couple of decades. I don’t have much else to add except my assumptions around the PAT / cash flows over the next few years which makes me believe it is reasonably cheap.

FY21 Pharma business EPS of 34.5 / share - 22x trailing multiple. $400m topline target given few quarters back, now I assume 3 FYs in FY24. FY24 Strides business 3000 cr and PAT 360 cr, Stelis PAT - 500-600 crore. Total 800-1000 cr PAT and 20-25k crore business, 3x from current market cap. Stelis Bio - Capacity of 500m doses. 200m x2 doses order for Sputnik from RDIF - validation batches shipped, expect commercial production from October. At $5 per dose - 400m = 15,000 cr revenue and 10% and PAT 1500 cr with STAR ownership of 33% = 500 cr

Bajaj Healthcare - Q4 earnings with Zee business Anil C Jain Joint MD - 5 year vision 1500 to 1800 crore with Dahej land capex also going to come on stream in next 2 years and current 90 crore acquisition. 15% EBITDA 225-250 crores - PAT around 150 crore by FY25-26. At 680 was trading 6x of expected PAT in few years https://www.youtube.com/watch?v=v87J6jWazh0

Beta Drugs - Love hate relationship continues, SME listed business very high risk and not for faint hearted. Reentered here at 272 level on a lower circuit pre-opening and closed upper circuit eod. SME volatility I tell you! You can read more about my thoughts here

Doubled up position in Nazara Tech after broker sell report - Very high growth business. India gaming industry grown at 28% CAGR in last 4 years and expected to grow at 30% CAGR till 2023. Debt free tech gaming businssess with improving EBITDA positive cashflows, since inception right up to December 2020, primary funding raised only to the tune of INR 126.30 million (in two tranches in 2005 and 2007) and INR 765.31 million in 2018. As a result, we have historically been EBITDA positive. CEO Manish Agarwal owns 1.42% skin in the game. Potential risk? Q4FY21 - May 31 Management doesn’t like to give any guidance on future (conservative or very uncertain business model?)

Considering topping up on Kotak Mahindra Bank, IGL, ITC, HDFC Life if they correct even slightly more from these levels. And add more to Beta Drugs. Looking to take out my invested capital from Acrysil - 8-9x in 11.5 months, unbelievable good, what a market! Just waiting for it to turn LTCG. Also in RKEC Projects, horrible results (vanity profits, very high increase in borrowing, trade receivables and pathetic operating cash flows)

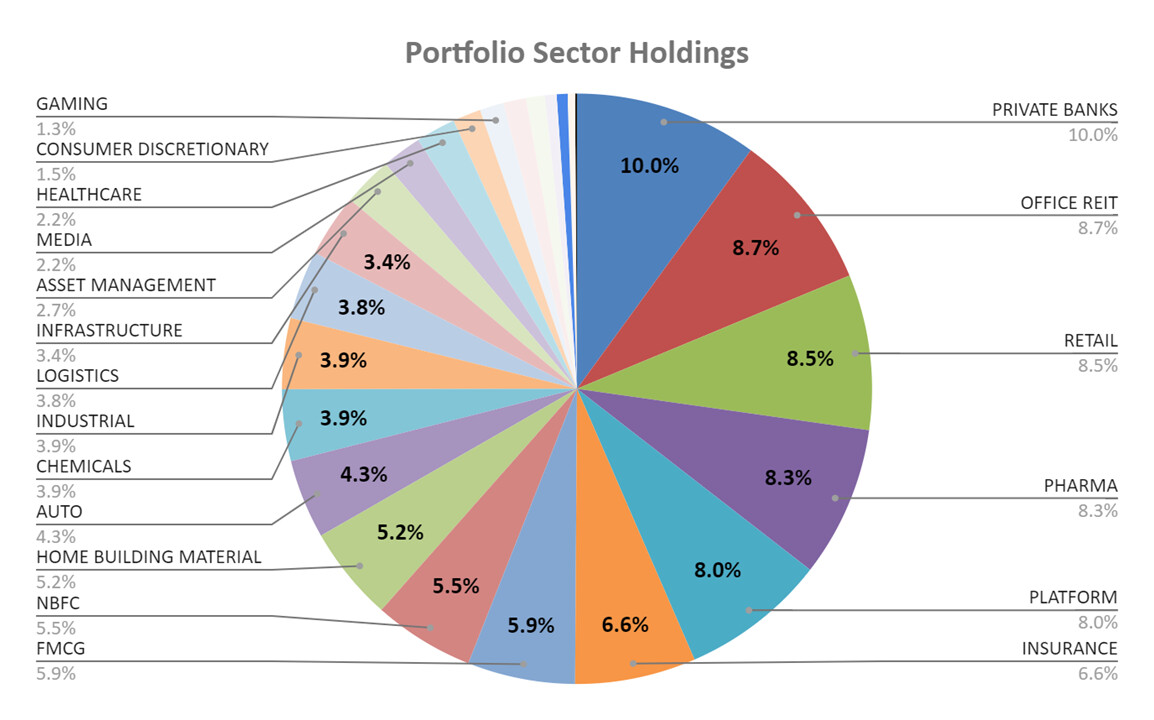

Sector Wise Holdings

PS: There was a reconciliation error of 1% in the calculation for month of May and my PF return up to May was 20.5% instead of 21.5%. So basically May month absolute gains were ~10% and June even better ~11.5%

Btw, why hasn’t anybody poked me on the concentration vs diversification piece yet!

13 Likes

wow, 73 companies and you seem to be on top of all of them, bravo! Probably why no one has mentioned about concentration vs diversification is because based on your posts you look very confident and know exactly what you are doing…and also the results are great as well…

One thing I noticed though is that in all 73 companies there isin’t any underlying theme or common thought process…I think you follow a very clear bottom up approach with triggers, value or growth per company at a time…not easy to do with limited capital!!

5 Likes

Wow, I could not have captured my investment philosophy or thought process in better words!

Thank you!

1 Like

As long as you know what you’re doing and are confident in your research and generating market beating return, why should anyone care if you’re diversified or concentrated.

Many paths to generate wealth, some go through the alleys of diversification and some through concentration.

Also, you’re not diversifying for the sake of diversification. You’re approach is researching companies bottoms up and dipping your fingers in many jars.

I school people on diversification when they do it for the sake of diversification without any understanding of what systematic vs unsystematic risks are.

You’re not one of them. Good job. Glad to know, Strides post helped you. Will post more details on the main company thread here.

6 Likes

Regarding the probable EBIDTA and PAT figure for Bajaj Healthcare for FY 25-26 as per you, the PAT will only grow by almost 2x. Isn’t 2x growth in 5 years a bit low for the CAPEX and the probable turnover which will increase 2.5X? How do you see the stock re-rating from hereon?

I genuinely believe this! And it’s also a massive bugbear of mine when I see so many VP folks discouraging others who have very diversified portfolios. Let me be the first to put my hand up and say - it’s much easier to maintain and monitor a relatively concentrated portfolio of 15-20 good businesses than 40-50+ stock portfolio let alone 70+. However, that doesn’t mean it’s the only way to generate wealth in markets. I find this lack of acceptance for other methods highly annoying and it can be quite damaging especially for those who’re just starting out in markets. They need to chart their own journey and go through the process of self-realization about their personality, risk appetite, temperament, etc. before finalizing any portfolio approach.

Btw, why I personally end up in so many businesses is that I have a certain % of cash coming in every month (salary) which I can deploy in markets owing to limited personal expenses. And I don’t like sitting on cash just waiting for my 15-20 businesses to come in my valuation range especially if I find there are good risk-reward opportunities elsewhere.

Hence, I don’t think about concentration or diversification - every single business I invest, I’m having certain profit / cash flow growth or rerating expectation at a minimum 15%+ CAGR for fresh capital. For redeploying capital where I’ve booked handsome profits, look at minimum 12%+ to relatively safely compound profit and still ensure overall CAGR of 15%+.

However, if I don’t have a monthly cash inflow I’d probably have a lot more concentrated portfolio for a variety of different reasons

a) I basically need to manage the same amount of capital, hence chances of number of companies increasing are low and as I would need to cash out / redeploy same capital

b) My risk taking ability would also go down as I won’t get any fresh capital at the end of the month and would not invest in a lot of nano cap SME businesses. Right now, I think of the salary as insurance, that the risky investment is worth x month(s) of salary even if it goes to zero

c) I would take more cash calls to be prepared for adverse events as I don’t have the monthly salary to take advantage of such events. Hence, would again result in being more concentrated and skip some lower conviction investments

If we take the upper end of revenue guidance from management at 1800 cr, PAT could be 180+cr and then we need to give it an appropriate multiple, so you could be right in terms of potential growth / re-rating if management executes well. However, the margin expansion seen in FY21 from 12% to 21% is unlikely to sustain in the next year and I’ve assumed a gradual improvement in operating performance over next few years to sustain 15% EBITDA levels. Also, I’m being conservative here in terms of my expectations going forward, 2x in 5 years is 15% CAGR, which is good enough for me - based on management execution the story can play out much better as well.

11 Likes