I sold Birlasoft today, and this had more to do with portfolio management than reasons linked with Birlasoft.

- After deploying cash, allocations dropped, and I’m more confident in other ideas providing better risk/reward rather than averaging up at this price. Gurjota’s diversification style has made so much sense to me in this context:

- I had a long conversation with my family, and since Infosys and TCS make up a large part of the family portfolio, I don’t feel like I’m missing out by selling Birlasoft/IT right now. Perhaps if attrition gets out of hand, or there’s a revision in forward multiples, I’ll get back in with much higher allocations.

Where I find comfort in high allocation to Ugro:

A lot of things have happened together for me to make this decision:

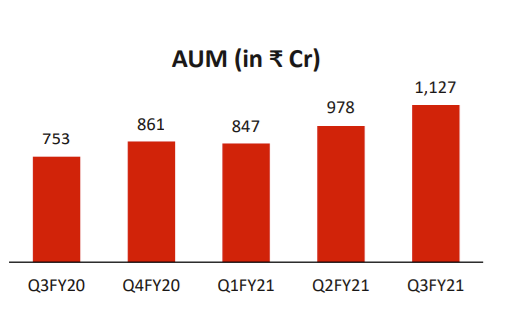

- Ambitious management guidance is backed by the numbers. They have set a target of 20,000 Cr. of AUM by 2025. Here’s what the picture looked like when I first invested:

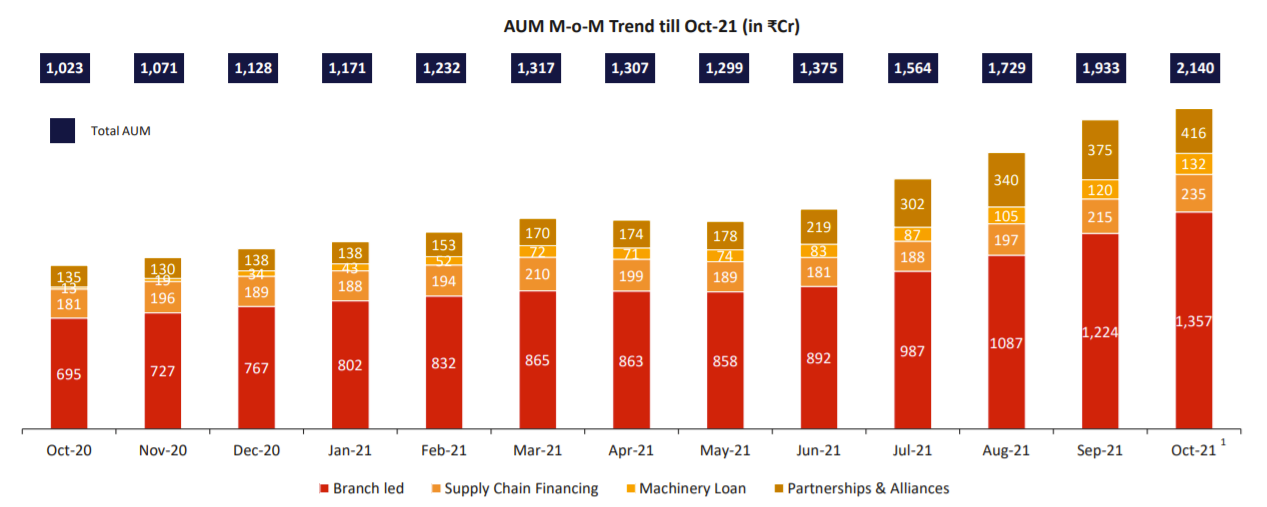

During the next wave of covid, management almost halted new disbursals completely and acted very prudently in Q1. Fast forward past a few earnings calls and crucial business updates to today, and here’s what the picture looks like:

At the present run rate, monthly disbursals are 320 Cr., and management is expecting monthly disbursals to reach 600 Cr. by March 2022, meaning Q1FY23’s quarterly disbursal will be today’s AUM. They’re currently far outpacing the run rate needed for their targets.

- The Q2 earnings conference has given me confidence that they have the infrastructure in place to scale, and that there’s plenty of liquidity on the liability side to meet their goals. The industry view is also attractive, with a lot of large banks also talking about the same credit gap that Ugro’s management is targeting. Recent onboarding of SBI as a part of their co-lending model further affirms that the management is walking the talk.

- I have a lot of valuation comfort right now, with my buy average being close to 130, well below the book value based on FY21 numbers. Despite the recent run up, the company is still overwhelmingly cheap on forward numbers, and I’m happy to add on more whenever I deploy cash. Furthermore, as SEBI has now mandated monthly business updates, the data available to track how the thesis is playing out gives me comfort, rather than having to wait for updates every three months.

There’s a lot more to be said about the company, but most of the questions people have prima facie, such as promoter holding, what NIMs will look like, why they’re confident of asset quality being good, etc. have been answered masterfully in the Q2 earnings call, and I would ask interested readers to watch the presentation.

Cheers ![]()