nice one,Gurjot.Keep it up.

Investment success has multiple paths and so let the concentration/diversification debate continue, while you make returns and keep peace with yourself

Wanted to ask one question: given that there are around 80-90 companies that u have put together in portfolio, how do you track them? I am sure, it would be impossible to read and track all of them closely, given that you are full time into a demanding job.

1 Like

Coverage Universe

Thanks @abhijain. I have a coverage of 200+ companies overall which I’ve shortlisted based on different parameters such as past business performance, management quality, industry / sector, size of the company, growth potential and track them at a high level at least in terms of price movements.

This was obviously not done in 1 day. I did the majority of this exercise last year in May/June when I couldn’t believe the valuations of some of the businesses - very good track records of performance of 8-10 years with strong dividend payouts were quoting of 4-5 P/E. I initially shortlisted 80-100 businesses across market caps (40-50 were so easy - typical coffee can names - paints, FMCG, pharma, top private financials, insurers, retailers, IT, platform, etc.) in a few weeks, a lot of which I had already invested or was about to invest in. And over the last year or so have kept on adding more and more businesses in that overall universe as I got to know them. I also have a screening sheet which quickly helps me decide in minutes whether it’s worthwhile to track that business or not. If yes, I try to come up with a reasonable valuation multiple, which will come up on my screen if the price comes in that range, at which I will dig into that business a lot more deeply before investing. The flaw with this technique is that - I need to redo this exercise for all the businesses I’ve not invested in. As it’s been more than a year and their earnings of FY21 now need to be considered in my reasonable valuation multiple.

Portfolio Tracking

With regards to my portfolio - I’ve held a maximum of 78 stocks and currently 73 stocks. For the high quality coffee can type businesses such as HDFC Bank, Kotak, Britannia, Divis, ITC, HDFC Life, ICICI Lombard, etc. - I really don’t invest or spend much time tracking them except the CMP at which I may want to keep SIPing or adding more onto them. And I’d say a good 20-25 businesses in my portfolio would fall in this category of little to no tracking.

For the remaining 50 - you can say it’s top down based on the allocation / current weight / coverage by brokers (SME listed, micro cap prioritized) where I’d make sure that for 30-40 I’d go through the quarterly results, presentations, management interviews, broker reports and concalls at least year ending ones. Also moneycontrol Pro is a fantastic value for money service in my view which shares quarterly results analysis for all the major large cap and mid cap companies along with some small cap ones as well. And what I’ve also started doing is capturing all of these managements future growth guidance in my portfolio sheet - so I can easily validate whether the business performance is somewhere in the vicinity of guidance or completely off-track. And no management guides quarter on quarter - each management guides for either 1 or 3 or 5 years vision. So if you document those details every year, I think you should be doing fine unless some extreme environment / company event changes the outlook for the company. And I’m able to spend most of the time on weekends to do these activities.

Few pointers to track your portfolio businesses:

a) Add them on screener watchlist

b) If subscribed to BSEalerts, add them to watchlist (also provide insider trading details every day)

c) Setup Google alerts for all the companies you want to track

d) Follow them on Twitter / Youtube - all concalls/management interviews get put there

Let me say - this is definitely not an easy task to do and can consume entire weekends (ex: just this weekend I listened to 5-6 concalls -RACL Geartech, Rajshree Polypack, Apollo Pipes, Fiem Industries, Macpower, RKEC Projects, etc.) if you start analyzing each business in any depth. However, if you want to get that edge and outperform the market, I believe this level of work is required and I’m happy to put in that time. Hope this helps.

14 Likes

Hi Gurjot

This is an exceptional stretch of run. Congrats.

Two queries since I take a similar approach (with respect to the quoted text above).

- Do you keep a broad view in terms of what is a good price for heavy allocation vs just SIPing. Or simply only SIP these

- There will certainly be a juncture where you will feel they don’t deserve passive monitoring but rather active monitoring. If yes then what is the tenet you use for that judgement call.

My two cents on diversification vs concentration: It is a waste of time and everyone must chose what they feel comfortable in.

Good luck!

Rgds

Deepak

3 Likes

Thanks for the kind words!

Firstly, just want to say it is great to see the last few comments on portfolio approach (concentration vs diversification) recognizing that both approaches work and no one method is absolutely perfect / always recommended.

- I probably should have rephrased what I said earlier - I’m actually not a SIP person. I basically mean averaging up on the positions in small quantities without following any SIP approach purely based on recent growth and current valuations. Some of the high quality banks like Kotak/HDFC at any 3-5% dips from current levels, seem good to me to average up based on my return expectation. For heavy allocation - it has to be seen in the context of your target return expectation, recent few years growth rate, current valuations compared with historic in tandem with the earnings growth rates. If all these parameters are ticked, then I can think of much higher allocations. For most of these blue chips, I think that time was only last year during Mar-May 2020 - but then again it has to be seen in light of target returns for any individual, for someone happy with 11-12% for 8-10 years, even loading up at current levels may be a good idea.

Sorry, I forgot to add here - 200 day SMA/EMA is also a key indicator I use when averaging up on these large caps apart from obviously the fundamentals. And I also look at the last few years charts to see how frequently these 200 day averages get violated, which sort of tells me whether I should be prepared for much deeper plunges in normal market environment or these levels should remain sacrosanct.

- Honestly I haven’t thought about this aspect for now and would not be able to provide valuable input here. My total investing experience is 7-8 years and I think some structural growth stories like private banks, insurance, select FMCG / Pharma / Retail is still intact for the foreseeable future. I don’t want some impatience of 12-18 months underperformance come in the way of long term compounding which we can benefit from in these businesses. I would not let lack of growth in revenue / PAT for a year or so make me take any judgment call except if the future holds massive disruption for their business models. And that I think is very business specific on what could be a big disruptor for these businesses - ex: ICICI Lombard - they have more than 50% business from motor insurance, I think about this some times - what will be the impact of EVs and driverless cars/two wheelers? Will motor insurance get wiped out with mass EV / driverless adoption? However, I think that time is at least 10 years away still, also in India it doesn’t seem feasible how we can ever manage traffic and chaos on the roads (apart from maybe 2-3 planned cities) plus don’t think auto insurance has been done away with in any country as yet, so some of these factors keep me at ease that such trends are still a fair way away.

3 Likes

Well, although not invested in ICICI Lombard but an ardent fan of Insurance as a business, if run rightly, and waiting patiently for opportunity to invest in HDFC Ergo or even Star Health…I do not think EV would wipe out Motor insurance…not even driverless cars…infact they could make insurance more costly & important. Motor insurance is a legal mandatory requirement in many countries, including India. As EV and driverless cars will be technologically superior with costly parts, insurance is even more important. Wear and Tear of engines maybe less but that would balance the cost structure…under no condition I see need of motor insurance going away.

On the contrary, Motor insurance can be a very good proxy of playing EV shift as well…as no matter which ever car manufacturer wins in EV race or battery producer…a 50% market share company in motor insurance would be selling its product to majority of consumers making the shift either voluntarily or by need of regulations that may eventually come up!

Recently, I have learnt never to write off any business, so I would want to correct my approach of waiting for HDFC group or other pure play general insurance company to list and would start tracking & evaluating ICICI group for general insurance as well…Thanks!

3 Likes

Thinking back on Motor insurance from known example, I see it a bit complicated…for example a Ford company selling car, the dealership gives option on Ford insurance and Bajaj Allianz (not ICICI in this case). One is free to use any other from second year onwards though but at time of purchase one usually end up buying the one which dealership offers to avoid hassles…Now on buying bajaj allianz, we get email etc from something called “Tata motors insurance broking company”…now Tata motors was never in picture but god knows how this broking company came in middle…

So, I see three players here - The car manufacturer dealer, the broker company in middle, the final insurance player which has a tie up with dealer/broker company…from second year onwards many people tend to continue with same arrangement as the costs go down usually and they dont bother much…if they bother, the quotes are reduced appropriately by same players…

In US, the switch and buying insurance for motor is highly digital and direct…is it same in India as well? If you switch to a new player after 5 years, do they come and inspect the vehicle first?

The above arrangement in India can be a moat and entry barrier as deep relationship/investments in that difficult ecosystem would ensure maintaining market share…but how is the final profitability because of this indirect route? Any idea on how ICICI lombard is faring on profitability in motor insurance as it is already a long time in this area…also going digitial and direct would although reduce the cost but improve competetion and switching options for consumers so would make pricing more and more competetive and predatory…so important to know current profitability…Thanks

1 Like

I have switched every year for last 3 years, when i am in the country and none of the time they came for reinspection. I have switched from chola( taken from dealer) to icici to royal sundram. I just put the details online and you will get the quote from different providers and i just choose the one who gives me the cheapest quote. I don’t see a major moat here. Earlier, the dealerships used to trick people to take only through them, i see that’s changing now as most of the quote aggregator sites, give you a quote in a min and the entire process can be done in a hour.

The bigger advantage i see, sometimes people tend to stick to big guns as the claim process is more streamlined and quick compared to smaller players,as they don’t want to switch. This will work in favor of icici.

4 Likes

True aggregator site would work as enabler of digital

Among bigger guns also, there would be many players - current as well as potential. interesting how ICICI still managing 50% market share and also leading since long. Is it doing it because of its dealership relationship/push or product innovation (not much scope here) or cheapest/relatively matching quotes policy (most likely) which would affect profitability/margins…

Unlike Life Insurance/Health Insurance, which offer multiple product innovation option and not just the cheapest policy wins…in case of Motor - I see the cheapest winning…this may not be good for business over long term…but having said that GEICO became what it is by selling motor insurance only, if I am not wrong! So need to understand this further…

1 Like

There are couple of reasons for geico’s sucess.

They positioned them as a cheap policy provider. Their first year policy quotes used to be ridiculously cheap when compared with others, thereby attracting sticky customers. Second year onwards it used to really closer to other providers so people tend to retain them.

Their marketing strategy with innovative advertisments made them stay releavant to the masses.

Their mobile app used to be miles ahead in terms of claim reimbursment /settlement process. Not sure if others were doing it as well,as i had only geico. You can raise claim, upload pics of accident, claims adjudged, get body shop details, request road side assitance etc. I guess icici can follow similar approach if they aren’t already.

2 Likes

Monthly Portfolio Note - July 2021

It’s that time of the month again to revisit how the portfolio is faring. So the crazy outperformance (8-9% every month) over the past couple of months had to end sometime and this month’s seen a steady 3-3.5% PF gain (well outperforming the Nifty still which was flat as a pancake at 0%). This month has seen my Core and Satellite holdings going in somewhat opposite directions. While many of the small and micro caps like Vmart, RACL Geartech, Goldiam International, Worth Peripheral rallied 30-70% in a month, large caps like HDFC group, Kotak Mahindra, Britannia have been sulking. And I think it’s a great time to add onto some of these behemoths in their respective industries - strong cash generating machines with stellar track records and growth ahead of them.

Portfolio Updates

Additions

Rajshree Polypack - This SME company was on my radar since May 2020 and I somehow overlooked it at that time due to price anchoring and invested in a few others. And I can happily say I haven’t lost a penny in opportunity cost as almost every SME company has become 3x since that time including the ones I invested. Now, thanks to @Tar for bringing it in the spotlight on VP forum at a very opportune moment when the company has finished a significant round of capex. I really like the consistency in revenues since this is a proxy FMCG play, read as essential business, in my view and the very small size of company gives it huge scope to grow in the future, almost debt free and good operating cash flows. At current valuations - looks quite tempting to dip some more into this.

Alembic Pharma - This has been in the news for all the wrong reasons post Q1 results. Anyway, sharing my investment thesis on this - it has withdrawn FY22 EPS guidance of Rs.50 due to intense competition seeing a lot of softness, delays in FDA inspections, however long term guidance and view of US market remains intact - expect to do $400 million annually in US by FY24, one or two quarters here or there can be off. For this year guidance - seen lot of pricing erosion, not heard back from FDA when they’re going to do the inspection and higher competition on few molecules, so overall not comfortable continuing with the guidance. US business - doing a lot of cost cutting rationalizing expenses, picking up some volumes some new businesses - so effect of all of this should be seen in Q3 and some part in Q2FY22 as well. My FY24 estimates based on gross fixed assets addition (2.5x from FY16-21) topline 8000 cr, EBITDA margins 22% (taken conservatively much lower than historic margins) and PAT around 1200 cr which should be sustainable and growing. At 25x multiple it’s a 30,000 cr market cap company. I realize that the business model for Alembic may not have the same kind of entry barriers which some of the CDMO players have, however those kind of businesses trade at 40x+ multiples given the superior quality of earnings. It seems like a heads I win, tails I don’t lose much opportunity at current levels - however I think I’ve realized, you can’t allocate too much to such opportunities as the opportunity cost could be very high. So will closely watch whether management is walking the talk or not in the next few quarters (cost reduction initiatives showing up in P/L, FDA inspections of new injectable facilities, etc.) - else will trim my holdings.

Apollo Pipes - Another one which was on my radar in May 2020, but went with APL Apollo that time. Now, thanks to @Worldlywiseinvestors for highlighting this company in the top 10 best moated small caps and brought to my attention again. Sharing my notes on this from Q4FY21 results concall - Management guidance for doubling of capacity utilization from 47-48k metric ton per annum (MTPA) to 1 lakh MTPA by FY23 (current capacity of 118,000 MTPA end of FY21) and revenue close to 1000 cr with increasing focus on building products segment which has higher EBITDA margins of 15-20% compared with agri products 8-10% margin. Stock can easily double within 2 years currently trading 30x trailing earnings. Very strong growth in last 5 years - 20%+ revenue and 25%+ PAT CAGR. Investor presentation guided for 25%+ volume growth for next 3 years. Promoters increased stake by more than 15% in last 3 years. Samit Vartak Sage One invested in Nov 2020 and Apr 2021 at levels of Rs.600 and Rs.1000. Plastic pipe solid growth sector with big players like Astral, Supreme Industries, etc.

Reliance - As promised earlier, bought again now that it’s almost at 200 day EMA and see very good times ahead for telecom given Vodafone Idea will most likely get crushed and will be a duopoly. Plus, Reliance Retail is super aggressive in all it’s initiatives whether be it JioMart, Ajio Luxe competing with Tata Cliq Luxury and obviously the standard retail outlets. And now the green energy businesses could be a joker in the pack.

Topping up on holdings - Kotak Mahindra Bank - doubled up position, Britannia - 50% more allocation and reasonable increase in HDFC Bank, HDFC Life - few others minor increases. See great run ahead for high quality financials if Covid remains under control.

Exits

CAMS - I hate to let this one go as it’s a platform business with many potential growth areas. However, when it’s almost doubled my money in a few months and now at 80x multiple with a 8-9% topline CAGR, I feel a lot more comfortable allocating this back into large caps like Kotak, Britannia, HDFC Life, etc.

LG Balakrishnan and Samkrg Pistons - Both small auto ancilliary companies without much investor interaction (presentation, concall, etc.) so it really makes it hard for me to track them and get an idea about the future business performance apart from the annual reports. With the large threat of EVs hanging around, really didn’t feel comfortable with the business model as they’ve already given me 140% and 70% returns effectively in the past 1 year. When I googled and came to know about one of their peers - real threat from EVs as Shriram Pistons Rings have been diversifying their lines of business in 2018. So that was the straw which broke the camel’s back.

Profit booking - Acrysil (8x) - capital taken out, Worth Peripheral (3x) - capital taken out, RACL Geartech (8x from initial buy) - high % of initial capital taken out, Goldiam (4x from initial buy) - high % of initial capital taken out, Divis (2.25x) - high % of initial capital taken out and some very minor profit bookings in Titan, Lal Path Labs, Indiamart, Vmart.

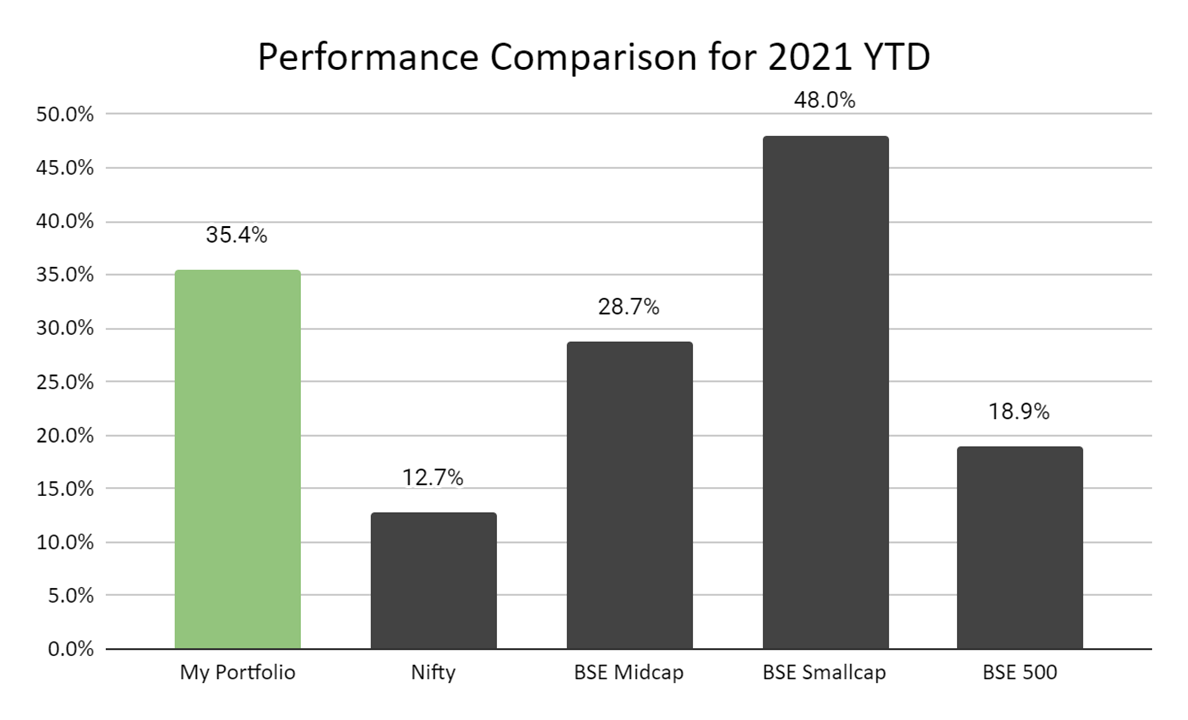

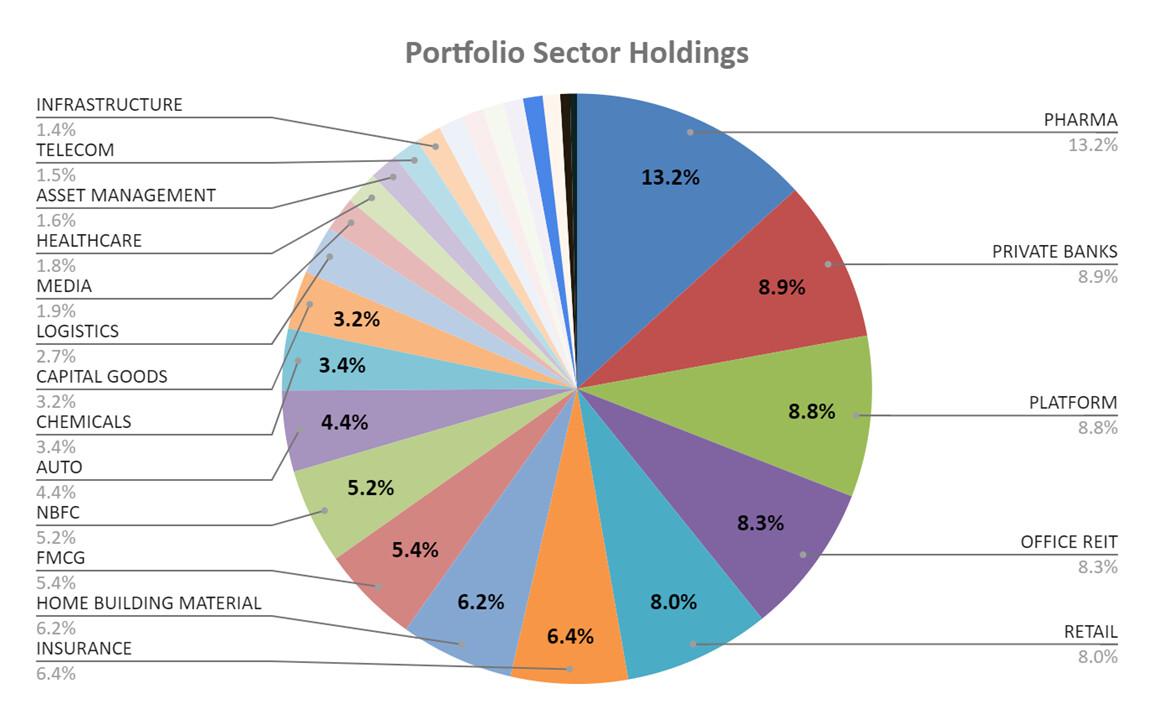

Portfolio Sector-wise Holdings

14 Likes

Monthly Portfolio Note - August 2021

August brought something which a lot of market veterans had been expecting and predicting. Somebody finally slammed the brakes on the heady small and micro cap run. A month with no returns on the small cap index and a reasonable correction (>15-20%) mid-month for a number of it’s constituents. We’ll only find out in hindsight if this was a good opportunity to unload a lot of unnecessary baggage in our portfolios. I definitely took this as a stern warning from the market to lighten up on positions of lower conviction and have acted on the same, along with preparing a ready list of companies I’d like to sell in the near future to reallocate to higher conviction bets. So I’m currently sitting on ~8% cash, which is the highest level of cash position since last year. Overall - my portfolio mostly mirrored the small cap performance with minor gains of 1.5% mainly in the last few days of the recovery as Nifty crossed yet another milestone.

My portfolio strategy going forward will be to consolidate the top 10-15 high conviction ideas and top them up as and when markets present opportunities. I realized making 4-5x on 50-60 businesses will be no easy feat and if I only achieve that on a few businesses with small allocations, it won’t take me to my financial goals anytime soon. But I’m still fighting internally on the best way to construct the portfolio without letting go of high quality average growth (10-16%) compounders like HDFC group businesses, ICICI group businesses, Britannia, ITC, Reliance, etc. So these are like 20-25 businesses in the portfolio which I just don’t want to give up on (only maybe in severe bear market where mid/small caps are at 4-5x multiples something like May 2020). But one thing is clear in my mind, whenever I spot the next 4-5 bagger opportunity over 2-3 years - I will look to allocate at least 4-5% of capital.

Portfolio Exits

Embassy and Mindspace REIT - Seeing the 20-30% fall in some good high growth mid-small caps in the middle of the month made me really itchy to allocate more capital towards high growth businesses than a steady 14-15% potential return compounding (incl. distributions) in REITs. I had to think again whether I actually want to own a REIT because of good stable returns or just for the sake of diversification and real estate ownership. And the answer was definitely not because of good stable returns as the office REIT business environment has been impacted with vacancies of all the REITs going up significantly over the past year and a half resulting in no-growth in distributions or much capital appreciation. With interest rate hikes looming around the corner (4-6-8 months), distribution yields of 6.5% (albeit tax-free) doesn’t sound that enticing with rising vacancies and no growth. Also, I didn’t have a lot of margin of safety in my buy price to be confident of making good returns. At yields around 8%, may look to add these back again. I’ve held on to the Brookfield REIT for now because I have a good MoS in that as I bought at attractive 9-10% pre-tax yield at 225.

Poly Medicure - This was a proper shakeout exit when the small mid caps were bleeding and I wanted to re-allocate to similar / better growth stories at much more attractive valuations. Although, this is a very good business still with phenomenal management execution over the past decade, I might just regret exiting this business if I don’t re-enter sometime in the future. Overall, can’t complain much though with nearly 4x returns in a year and half.

Portfolio Entry

Chola Investment Finance - I exited this business earlier this year in Feb at 550 levels, but recently came across this being part of the Marcellus Kings of Capital portfolio. I re-looked at the business in some more detail and this has been another phenomenal story of top notch management quality and execution. I got in at 475 levels in the recent small cap correction and it just shot up the very next day onwards not giving me too many chances to allocate much on this.

Investment Rationale - Excellent corporate governance track record, flagship company of Murugappa group. Vehicle finance business mainly commercial vehicles - 99% loan book secured, historical 24% book value CAGR last 9 years, excellent 17-18% ROE. 1-2 bad years like 2017 with NNPAs shooting up to 3.2% else every other year below or equal to 2.2% even post Covid wave 1. Covid wave 2 (Q1 net NPA shot up to 4.38%) - very high but transitory impact on asset quality as per management. In Q1 FY 22, due to second wave and localized lockdowns, there had been roll-forwards to higher buckets and hence a higher Net Credit Losses NCL, and considering the reasons specified, the quarters are not comparable. This position in Q1 FY 22 is temporary, and we expect the loan losses to get to normal levels in subsequent quarters, as it happened in Q3 and Q4 of FY 21 where the customers started paying up once the lockdown was lifted, and normalcy returned

Vaibhav Global - I only have a small position here because this never broke or even got close to 200 DEMA where I like to buy strong businesses trading at relatively elevated multiples. Anyway sharing the investment rationale - Asset light business with excellent operating leverage and 16-18% growth guidance for the near future, Covid and adverse market conditions only increased business tailwinds. From 2017-21, both revenues and EBITDA margins have doubled ~ 4x profit jump! Agile product portfolio and supply chain, concall - “for example, right now the handbags are selling like crazy. We can’t have them enough in our inventory and last year nobody wanted handbags. There is an example. We would quickly get that handbag even by air, usually will come by sea. We get them by air offer to the customer and address their needs. Last year it was essentials, so we scrambled all over the world to get that essential to our customers.” Focused management - don’t take in any new product in our entire business which would give us less than 50% gross margin

Glenmark Life Sciences - Another small position on this due to the 1162 crore transaction doubts I had and the recent correction in pharma made me jittery to allocate big, and soon enough it went well below the IPO issue price as well. However, in terms of valuations - based on the kind of complex APIs and high margin products it deals in, the valuations seem quite favorable from a risk reward perspective if management can execute well in the future as well.

Investment Rationale - API business in Chronic diseases, diabetes central nervous system CNS, pain management, and also has a fast growing CDMO business. In APIs, generic and complex APIs. Complex APIs are the high value and high margin APIs. CDMO is currently only 10% of overall business. It’s customers include 16 of the 20 world’s largest generic pharma companies globally. Excellent clean systems and process compliance with impeccable US FDA, European and other regulatory inspection track record in last 6 years, not received a single warning letter or import alert. Since 2015, GLS facilities have been subject to 38 inspections and audits by regulators including the USFDA, PMDA, COFEPRIS, Health Canada, MFDS (Korea), EDQM, other European regulatory agencies and CDSCO conducted on a periodic basis. Margins guidance - Plan to introduce 8-10 new products every year which should have good margins, pharma business is run in that fashion where older molecules suffer price erosion but need to keep adding new molecules to maintain the margins which we plan to do. Current capacity will more than double, so current capacity is 720 kilo litres and will be adding another 1000 KL, so total 1720 KL with brownfield and greenfield capex of roughly 775 crores. 155 crores to be used for brownfield capex at Dahej to add 200 kilo litres of capacity + 30 crores oncology block in addition to current capacity of 140 kilo litres, so total 340 KL.

Increased Allocation - TCI Express, Valiant Organics, Neuland, Symphony, Tips, IGL, Mas Financial.

Watchlist - I really like some of the recent IPOs such as Sona Comstar, Clean Science & Technology and Tatva Chintan. They all have great growth stories lying ahead of them, waiting for better market opportunities and valuations to take exposure to them.

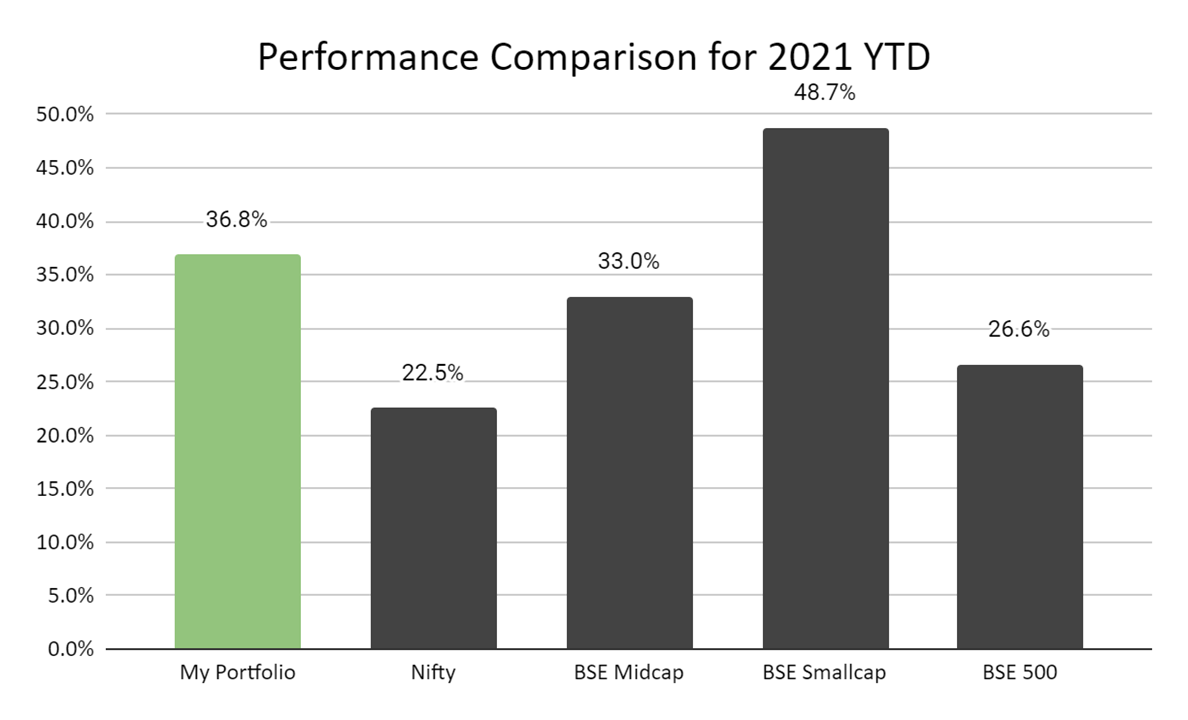

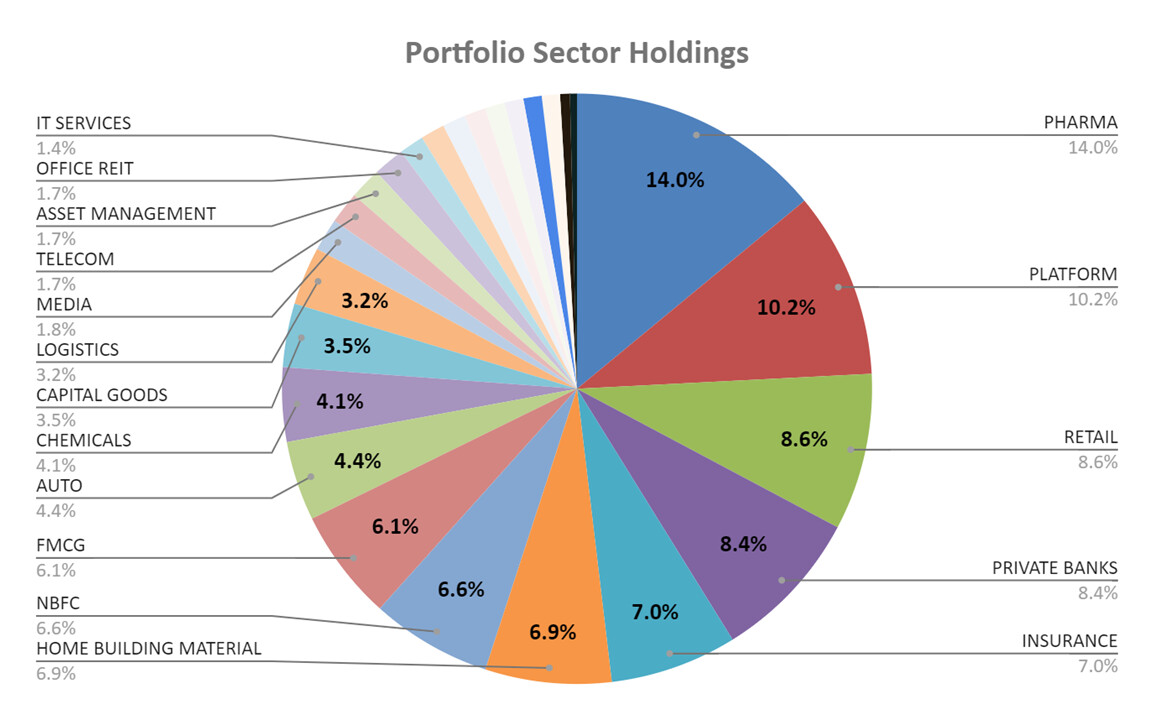

Portfolio Sector-wise Holdings

22 Likes

Hello Gurjot,

Can you share your latest portfolio holdings?

Hi - I’ll be sharing my portfolio at the end of the month. Will be a good time to review the performance at the end of Q2 and H1 of FY22. The jittery broader markets are making me shuffle some positions and enter few new ones, so will be in a better position to share in 10 days time.

1 Like

Monthly Portfolio Note - September 2021

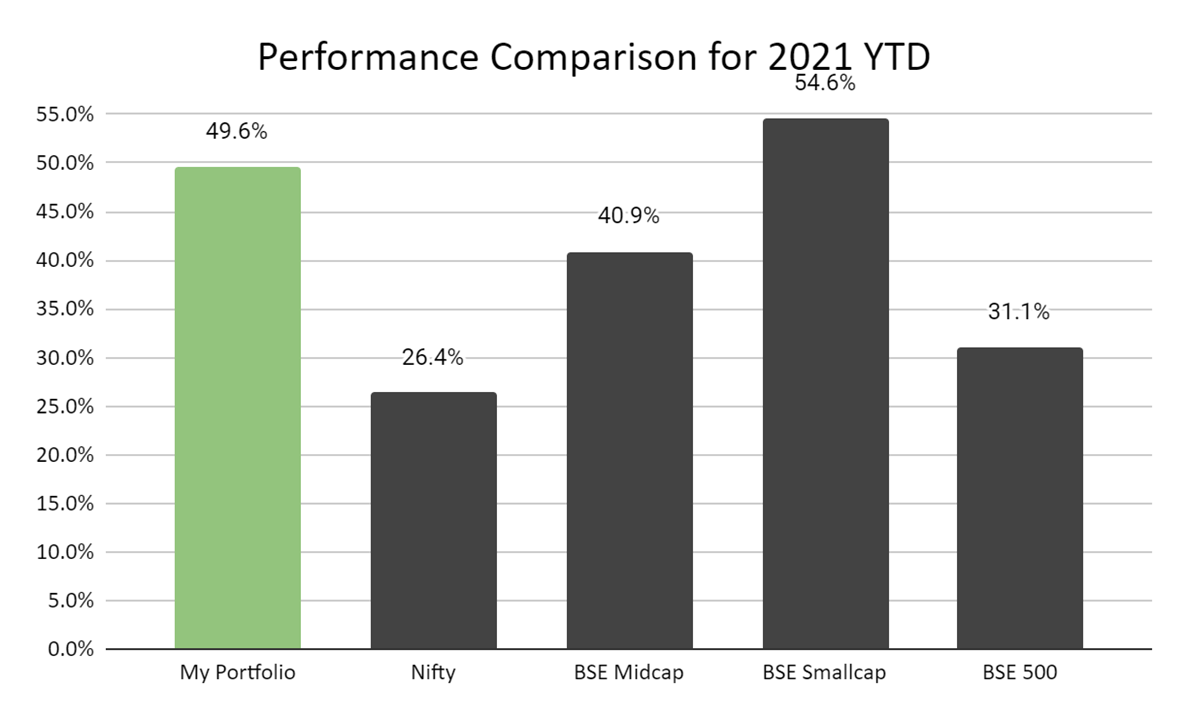

Are we back on the hedonic treadmill already? After a sedate previous month, September has again seen the mid and small caps flying off the charts with decent participation from Nifty as well. Luckily I had some of the high fliers in my portfolio as well (IRCTC, IEX, Delta Corp, Beta Drugs, etc.) which helped outperform all the major indices last month. Overall, it’s been a fantastic year (assuming same for most retail participants) but the real proof of the pudding may come during any 10-15%+ corrections on the major indices. How much of these gains do we retain that time will demonstrate the true quality of the portfolio

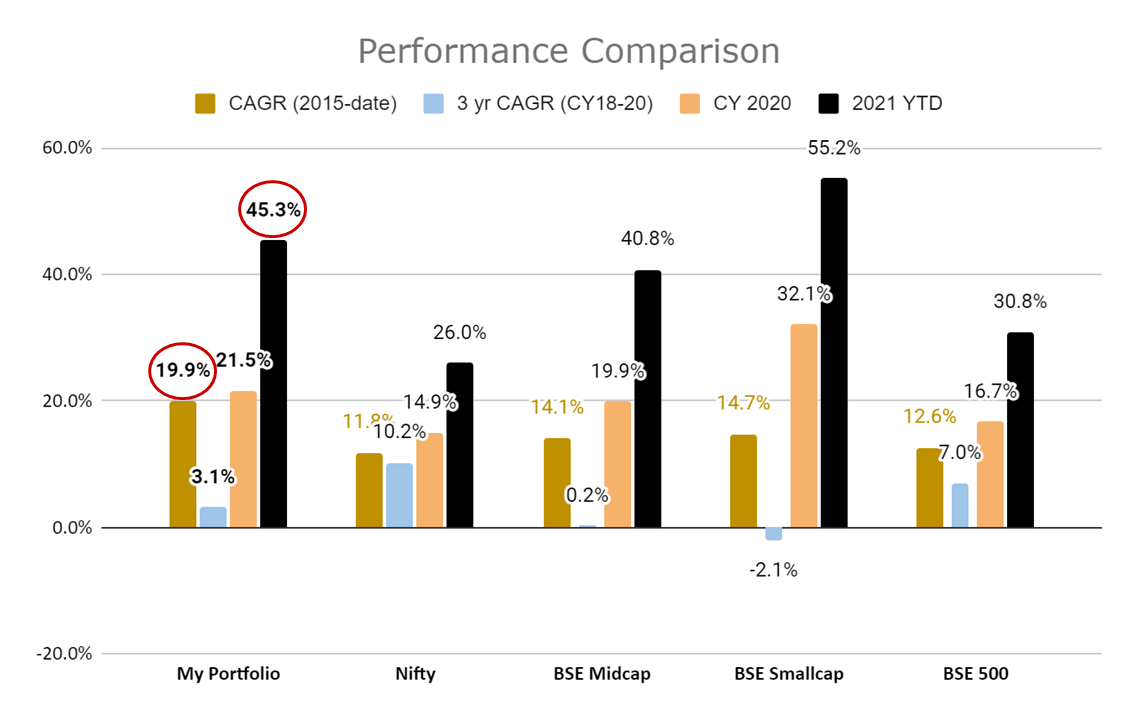

On a personal note, I’m extremely glad with my last ~7 year CAGR which is almost 20% as of date and comfortably exceeds the major indices. Most of this is due to the performance over the last couple of years but I feel pretty confident of maintaining this XIRR for a long time to come. The last 7 years have seen lots of market volatility at different points in time (Brexit, demonetization, GST implementation, NBFC crisis, 2 US and 1 India election, small/mid cap bear market, Covid crash, etc.), my personal disastrous investments in Yes Bank, Lasa, Secur Credentials, many more, etc. and having a 20% CAGR in the face of all that volatility makes me quite content and optimistic about the future.

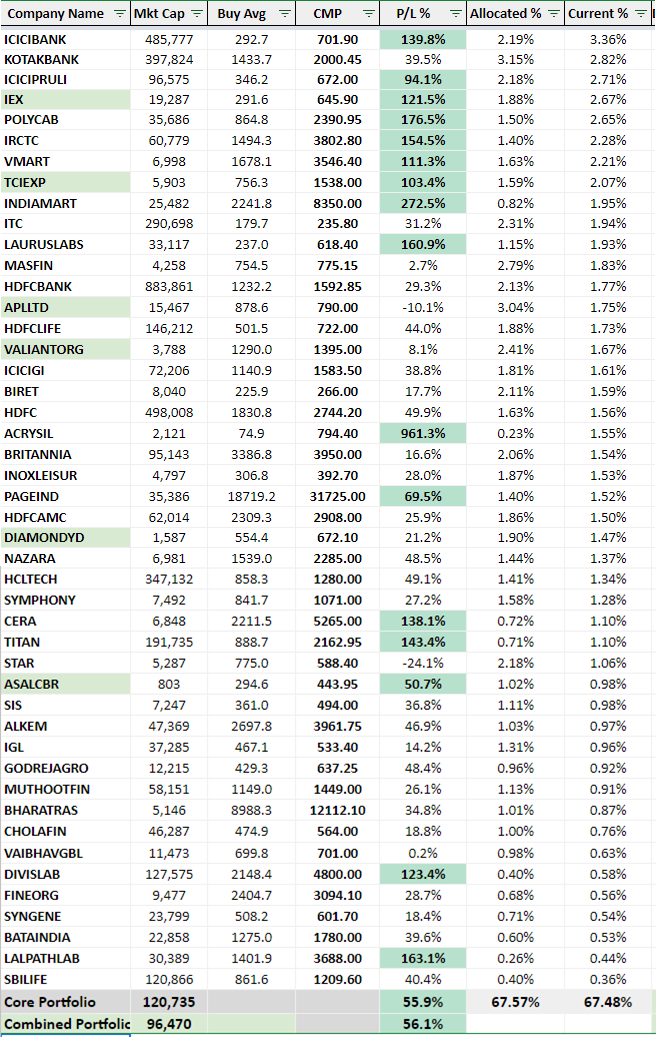

Core Portfolio

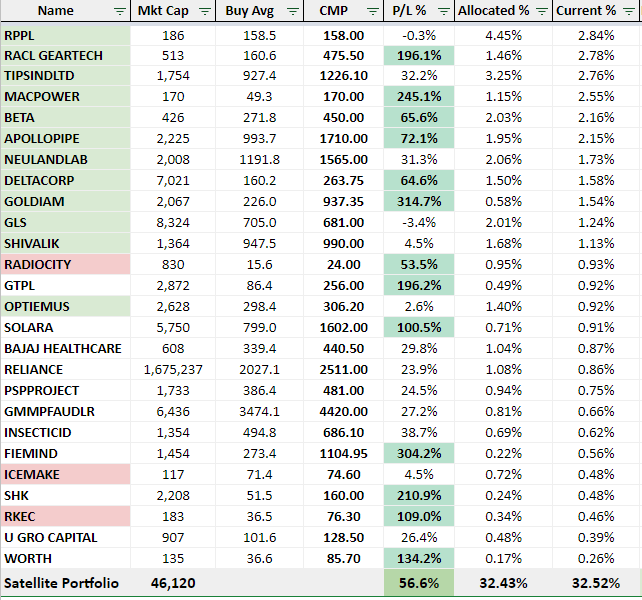

Satellite Portfolio

The ones in green is where I have higher conviction and the ones in red are next exit candidates for me.

Satellite Portfolio Entry

Shivalik Rasayan - The company is into manufacturing of agrochemicals, specialty chemicals and APIs. In 2015 it forayed into pharmaceuticals by acquiring Medicamen Biotech Limited which is engaged in manufacturing pharmaceutical formulations. AR 2021 - SRL is a manufacturer of Organo Phosphorus (OP) based insecticides and chemicals, with its organophosphate products including, Dimethoate Technical and Malathion Technical. Dimethoate Technical is an important element in formulations used to control a variety of insects, pests, and mites, while the Malathion Technical is a non-systemic, spectrum OP-based contact insecticide, particularly favourable in agricultural production of multiple feeding crops. The Company’s API plant is now operational and SRL has received WHO-GMP approvals for its Dahej-II Plant. Plant validation of 7 API completed, the products are under stability. Planning to file 2 DMF by December 2021. Capacities - a) Agro and Specialty chemicals - Current capacity 1450 MT, doing capex of 3500 MT Per annum First Phase One-Block. Initially set up one block with a total project cost of Rs. 125 Crores to be completed in 15-18 months. Further strategic expansion to set up a green field Agro & Speciality Chemical Plant at Dahej-III, GIDC Gujarat. Received Environmental Clearance(EC) from Ministry of Environment and Forest Department to produce 12,000 MT per annum AgroChemical Technical and 8,000 MT per annum Intermediates and Speciality Chemicals (final capacity will be almost 15x of current capacity). SRL has industrial plot of 50,000 square meters for establishment of manufacturing of KSM, Intermediate, Agro- Chemicals and Specialty Chemicals at Dahej III, Gujarat. Already sanctioned capex for agrochemicals and specialty chemicals. Supply of Intermediate/ Advanced Intermediates for captive consumption and thirdparty sales in India and abroad. The Company has established new pharma API manufacturing facility at PCPIR* zone in Dahej (Gujarat) which is designed to be a dedicated, stateof-the-art facility for manufacturing General APIs & Oncology APIs and committed to supply high quality APIs to regulatory markets.SRL Dahej site has received Manufacturing Licenses for Cytoxic & General API from Gujarat State FDCA in year- March 2020 and 05 Oncology and 02 General API products have been validated on site till date. Also, SRL has received WHO- GMP Certificate in year 2021 for 02 Oncology and 01 General API products. During the year the Company has purchased 2,77,000 equity shares of its Associate Company i.e. Medicamen Biotech Limited from open market, thereby increasing its stake to 41.79%. Company changing product line - new API plant in Dahej began production in March 2020 investment thesis

My take - The company has been doing significant capex over the past few years and recently announced even bigger capex. There is a real execution risk that management may not be able to fully utilize the capacities within a reasonable timeframe which will drag margins for a long time. However, just the opportunity size and the scale at which the company plans to operate is startling and at just over thousand crores market cap, I think there is a huge opportunity and decent risk reward payoff from 5-10 year timeframe. Key monitorable will be scaling up of revenues for recently completed capacity expansion.

Optiemus Infracom - This one will be very hard to justify in terms of business performance as there is nothing really to speak about. It is just a calculated guesstimate of what can happen in the future based on the recent event flow around the company and management/leadership changes. The electronics manufacturing potential is just way too big that even if some part of that potential gets realized I should be handsomely rewarded. Optiemus Electronics, 100% subsidiary of Optiemus Infracom, has been awarded PLI for 2 sectors (mobile phones and IT hardware). They signed an MoU on a strategic partnership with Wistron Infocomm Manufacturing (India) to manufacture mobile devices, IT hardware and Automotive- EV products. They’ve announced an investment of 1350 crores with revenues of 38000 cr in 5 years (I think a lot of people are reading this incorrectly on the internet. I assume this is a sum of next 5 years revenue and the revenue in 2026 could be 8-12k crores). A Gururaj appointment as MD (ex VP in Reliance Infocomm and MD of Wistron India) in June 2021. The promoter holding is excellent in this at ~75% and I don’t see a single share being sold in the last 8-10 years at least. The management has mentioned in a couple of recent interviews they are in advanced discussions with a very big potential customer. At 2,500 crore market cap - it can be great play on the contract manufacturing theme and long term growth of mobile phones / electronic devices / wearables.

Increased Allocation - Rajshree Polypack (amongst my highest allocation now), Vaibhav Global and Glenmark Life Sciences.

Portfolio Exits

Indusind Bank - I had exited this one in August only at a 20% loss, forgot to mention in my previous monthly post. As I’ve mentioned earlier, when it comes to leveraged financials I only want to sleep with the best managements in India with flawless books and asset quality. In banks, I only own 3 now - ICICI, Kotak and HDFC along with few NBFCs.

Eicher Motors - A 2x for me since May 2020 (nothing special as Nifty has given similar returns). Nothing much against the business, best in class profitability and return ratios, except that this is a somewhat cyclical industry and I don’t have as much confidence in it’s growth trajectory as some other smaller businesses in other sectors. I also don’t know how EVs will impact this industry so would like to partner with businesses with better visibility.

Edelweiss - Finally booked loss (35%) on a pretty decent allocation wrt my portfolio. Wealth destroyer for me over the past couple of years, another one of my crazy mistakes in the NBFC crash of 2018-19. I also finally realized something which I was told within my first few months of joining VP. “money has no color”. Even though I find current valuations of Edelweiss quite depressed compared to the growth opportunity in the current economic revival, if I have any other alternatives available with similar conviction of 2x returns in 2-3 years, then I should move my capital there rather than hoping the turnaround will materialize here. Moved proceeds from this to Rajshree Polypack. Just remembered, a similar strategy already paid off in spades for me when I sold Indiabulls Housing in Feb at 50% loss, deployed proceeds to Chemcrux, booked 70% gains on that and moved all to Britannia in May with another 20% MTM agains, so already recovered my entire capital in 6-7 months.

DB Corp - Even though I made 50% here along with a 7% dividend of Rs 5 at buy price of 70 and total returns of 55% in a little over a year, it really pales in comparison to what other growth companies have achieved. Deep value investing is really not my cup of tea especially in a sector in permanent decline till the time technology disrupts news distribution, viewing and reading just like music streaming took about 8-10 years to really catch on. There is very limited future for growth of physical newspapers over the next couple of decades and there will be massive disruption through news related tv / mobile apps. But that time is still far away and also the business of news publishing isn’t as strong as music streaming. You need to generate brand new content every single day to captivate your audience but music is something we can hear again and again and again and again.

This month has also been special for me in one more way and it has taken me a full 8 years to get there.

This is the first time one of my investments became 10x from the original buy price, had come very close with Avanti Feeds in 2017 (went 9x presplit from 300 to 2700 only to retrace sharply and never ever gotten close to those levels again).

Barely 10 days after the first 10x (Goldiam), Acrysil became the 2nd one. Unfortunately both were relatively low allocation, so markets still teaching me lessons along with the rewards ![]()

23 Likes

Hello @gurjota , I am planning to invest in stocks which are corrected in recent fall. Igl had fallen almost 10% from its high. Is it a right time to accumulate this stock considering COVID impact on sales , EV sector rise and increase in natural gas prices?

I see IGL in your portfolio. could you please share your thoughts on this company and overall gas industry for long term.

Thanks in advance!

1 Like

Hey @gurjota congratulations on your first 10x. I have been following your portfolio for quite some time and I have to say many of my premade notions have been proven wrong by your portfolio.

I have a question about size of your portfolio. At what point do you think that number of companies in your portfolio needs to be reduced? Or does the number of company does not bother you at all?

Also, subsidiary question to that is, how do you decide to allocate capital to particular company?

Also, unwanted suggestion from my part regarding deep value investing, I think you should check out deep value pockets in cyclicals or commodities. As from personal experience, Kanchi Karpooram a very basic camphor business with capacity expansion and price hike in camphor price turned out to be multibagger for me.

Hi @Harsh2021,

I’ve actually tripled my allocation in IGL in October as I’m very optimistic about the next few years growth drivers for the company and overall demand outlook. The management has expressed supreme confidence in delivering 15-20% CAGR volume growth in the next few years driven by the new GA expansion of PNG/CNG, high conversion of petrol/diesel vehicles to CNG in NCT area with skyrocketing fuel prices, expect PNG conversions to continue as it is cheaper than the non-subsidized LPG cylinders, regular additions of more CNG stations, resumption of schools, offices, etc. You should see the recent ET Now interview of management shared below where they’ve talked about these growth drivers.

In terms of EV impact, that time is still few years away till EV technologies improve and get economies of scale to match costs of current petrol / diesel vehicles Just the fact that auto makers like Maruti are targeting 25% of sales from CNG vehicles in the next few years gives enough confidence that CNG as a fuel is not going away anytime soon. And they expect to launch an EV only by 2024 or so. Also Delhi government has placed an order for 1000 CNG buses earlier this year.

Also, I found this research report which has compared the TCO of EV cars vs CNG cars. For now, TCO of CNG cars makes more sense as EV vehicles are still quite expensive. However, there will be a tipping point some years down the line where there’ll be mass EV adoption by car buyers. When that point will come, I really don’t know as of now.

Over the long term, the main anti thesis in my view is the potential PE derating by markets if they believe natural gas, being a fossil fuel, is not environment friendly and still a cause of climate change. If we look at some ICE engine related auto ancillary businesses, how markets have treated them at sub 7-8 PE, they’ve definitely come to the conclusion that these businesses are in permanent decline and going to be dead in a few years. I’m not sure if the threat for IGL is so grave as of now.

But the business pivot will definitely be required few years down the line. Just look at Reliance and the whole acquisition spree around green energy. The IGL management has started taking cognizance of the EV threat and is setting up 2 wheeler battery swap points at it’s stations. But these are baby steps for now.

I envisage a healthy ecosystem of CNG and EV led Indian economy by 2030, which should largely be EV by 2040. How would IGL as a company have changed by then, what proportion of business would have be coming from just PNG, it seems to early to comment as of now. So, whilst this is a very good business in the foreseeable future, it would need to be watched with hawk-eyes.

5 Likes

Hi @Chaitanya_Tanti,

Thanks for the appreciation ![]()

I believe investing as an art or skill can mostly be practiced from the comfort of your home with some amount of real-world scuttlebutt. So if we can comfortably track a high number of businesses sitting at home, I feel it’s fine for now. Also whilst I hold 70 companies, do I need to track 70 businesses?

No! A lot of these 70 companies have identical businesses (Banking - HDFC, Kotak, ICICI; Life Insurance - HDFC Life, ICICI Pru Life, SBI Life, etc.) - so I’m actually tracking 35-40 businesses overall.

I do agree that going through annual reports, concalls, investor presentations, management interviews, etc. of so many businesses is quite time consuming. And I’ve mentioned earlier how I’ve tried to optimize the process - I don’t think it’s perfect and it still requires a lot of time though. It’s an evolving process and I may change it drastically in the future.

I’m not sure exactly what you mean here, but I’ll assume you’re referring to the % of capital allocation. If I’m extremely bullish on a company, I’ll max allocate 4-5% capital. I’ve not had a great track record with my highest allocations - they’ve almost always lost money except ICICI Bank which was also losing money since 2016-17 days but finally turned around last 2 years superbly.

I generally start with a 1-1.5% of capital allocation through my primary source of income, salary every month. Given the massive run-up in valuations since Mar’20, I find it hard to average up 3-5x from my buy prices in a lot of the names. Hence, I need to find a lot of new companies which might still be available at reasonable valuations and end up buying so many companies. However, in well established multi-decadal businesses and themes (consistent compounders) I find it easier to average up and keep increasing allocation.

On the deep value investing, I’m generally averse to cyclicals or commodity plays such as steel, ferrous, coal, power, etc as those businesses need to be tracked and monitored on a day to day basis. Congratulations on your multi-bagger, however I find it easier to identify longer term compounding themes which should also be multi-baggers few years down the line.

1 Like

Monthly Portfolio Note - October 2021

I have never experienced a month like this in my 8 years of investing experience! It was literally a “chalk and cheese” month of two halves, like north and south pole! The first two weeks Mr. Market made me feel smarter than Albert Einstein, you just needed to wake up and smile like a cheshire cat with 1-2% of daily gains at the portfolio level. With each passing day, mid/small caps started making sharper and sharper vertical moves upwards.

And then it finally happened! 19th Oct - IRCTC’s market cap touched 1 lakh crore and that for me was the peak euphoria moment for the broader market. At that moment, it might have dawned on a lot of market participants that it’s time to take money off some of these overheated names. Add to that the margin compression for even the consistent compounder businesses, and I think we’re seeing the after effects of all that till date with a decent broader indices correction which could extend into November as well.

My portfolio continued to outperform this month largely led by IRCTC (where I luckily pulled the chain) and leveraged financials as Nifty Bank gave ~5% monthly return vs all major indices which were flat. The recent correction made me do a lot of changes in the portfolio and also allowed me to redeploy IRCTC gains, all covered below.

Core Portfolio Update

Exits

IRCTC (3.5x) - What a roller coaster ride this has been, quite unexpected from a train journey ![]() If I skip the entire convenience fees fiasco for a moment, I first hand witnessed the great rebound in demand for IRCTC’s services as I travelled on one of the Shatabdi trains, they were running full all across the country and huge demand for revenge travel. But I don’t know what market forces were driving the stock price to crazy valuations even if you built in great growth in the next few years. My internal FY24-25 market cap target for the business was 1 lakh crore at 50x multiples and I started selling when it reached 80,000 cr in 2nd week of Oct. On 19th Oct, it reached my next 3-4 year target of 1 lakh crore and I sold significant chunk of my position that day. On the same day, I had even alerted on a Whatsapp group that platform companies in India including IEX seem to be in a bubble.

If I skip the entire convenience fees fiasco for a moment, I first hand witnessed the great rebound in demand for IRCTC’s services as I travelled on one of the Shatabdi trains, they were running full all across the country and huge demand for revenge travel. But I don’t know what market forces were driving the stock price to crazy valuations even if you built in great growth in the next few years. My internal FY24-25 market cap target for the business was 1 lakh crore at 50x multiples and I started selling when it reached 80,000 cr in 2nd week of Oct. On 19th Oct, it reached my next 3-4 year target of 1 lakh crore and I sold significant chunk of my position that day. On the same day, I had even alerted on a Whatsapp group that platform companies in India including IEX seem to be in a bubble.

Let me not even get started on the convenience fee issue, the big risk of government as promoter has and always will be the biggest risk in this business. It just came to life few days back! Anyway, now I just have 15% of original holding mainly because of the split shares which I couldn’t sell during the week and plan to offload soon.

Page Industries (2x), Divis Labs (2.5x) and Brookfield India REIT (25%) - Nothing wrong in any of these businesses except I find much more lucrative opportunities elsewhere given the current valuations/yield.

Allocation Changes

More than doubled allocation in IGL (covered 2 posts earlier), Bharat Rasayan and Vaibhav Global. Added more in HDFC Life, ICICI Lombard, Valiant Organics, Syngene, MAS Financial, Laurus.

Trimmed 30% position in ICICI Bank, had another superlative quarter (solid 3.3x in 5 years) and some in Alembic.

Re-entered Poly Medicure - There is a massive size of opportunity and TAM for medical devices. Global companies like Medtronic and Baxter have $10-20+ billion valuations. Government is also providing impetus with setting up of 4 medical device parks. The business is no longer cheap but management execution is top-notch, typical coffee can style consistent compounder and size of runway is so big that longer term investors of 5-10-20 years can still make a very good IRR.

New Addition

Deepak Nitrite - This has been a dream business for many investors in the past 5-7 years with astounding growth handsomely rewarded by the markets as well. The recent correction gives a decent opportunity to buy into this non-stop growth story with another big capex (1200+ crores) announcement by the management. There are some who compare this with peers like Navin Fluorine which have double the multiples, but even without expansion in PE - we can expect decent CAGR if the management continues to execute and maintain the growth track record. The risk I see is the dreamy vision laid out of “Make for India” and “Make for the world” not being fulfilled. I’m not sure if there are many companies in this industry globally who’d be successful in being market leaders across range of products.

Satellite Portfolio Update

New Addition

Prevest Denpro - Huge size of opportunity India and globally - just India market size is 15,000 cr for dental materials (all currently imported materials - huge import substitution opportunity) as per AVP Group pharmaceuticals Sathyanarayanan. Also, company’s 5 products are already US FDA approved in May 2021 and applied for approval of another 15 products. Also cleared MDSAP audit for exporting to Canada, Australia, Japan, Brazil, etc. and now awaiting the formal certificate. In my view, US FDA approval for a nano size 30 cr dental materials company is a huge tribute to the management and credibility of company’s products, manufacturing process, compliance. Management is targeting 500 cr of topline in the next 10 years and I think it can comfortably beat that with the exports into large regulated markets such as US.

RKEC Projects (2.5x) and GTPL Hathaway (3.5x) - Markets don’t generally reward infrastructure companies with high multiples and I find more lucrative opportunities elsewhere. GTPL - I think cable TV business is another disrupted business with the huge demand for OTT, streaming content services. The other broadband business is good, but I’m not sure it can cover and grow the overall revenues / PAT of the company at a healthy CAGR.

Doubled allocation in Solara and increased allocations in Apollo Pipe, Macpower, Glenmark Life, Shivalik Rasayan.

PS: Just a caveat, given the large number of businesses in portfolio, I might have missed few minor changes and could happen in the future as well.

12 Likes

Hi Gurjot,

I thoroughly enjoyed reading your portfolio thread. You are doing great in terms of pf performance - CAGR of ~20 from inception. Congratulations.

Back in 2017 in the above post, your CAGR is 27.8 which is always a great number. I would like to know your thoughts about how to maintain a similar CAGR. Just wanted to understand the different pathways to sustain CAGR and to reduce the errors. I am aware there are many unknowns in equity investing.

The reason why I am asking this question is , I am right now in a similar position. I started serious equity investing around Feb-18 and with the current bull market, I am sitting on a good CAGR(~25). However, all good bull markets come to a close. I did better as MF investor CAGR(~28).

4 Likes