Same thing happened last year as well

No answers from management on what happened during bad times…

They nicely come and project in good time

Though a bad quarter here and there is ok but communication gets missing

Primarily the reason i got out of this

“Changes in Inventories” is indicative of what you might be looking for. Two products, limited customers, batch deliveries (lumpy business). Volatility is bound to be there. Q-o-q is a terrible way to judge their business.

Real scale in Intermediates comes only when there is product diversification. There’s a limit to where you can scale intermediates individually. Intermediates at an individual level aren’t fast churn because these are critical in manufacturing the API and are therefore stocked for a decent period of time. Because they don’t overload the inventories (value wise) for an API manufacturer (fractional cost). So, criticality + low value warrants stocking.

Gross margins also aren’t all that different. And Ebitda also has to take a hit when you have operated fully but haven’t sold the batches. Your overheads would eat up the margins.

Seems that there is a decisive shift (after deliberation, diligence for 10+ years) in treatment approach towards fight against Tuberculosis/LatentTB. All the key global policy/decision makers are pushing for the new regime of treatment– preference of using Rifapentine (12/30 doses) as against current preferred treatment based on Rifampicin (90/120 Doses) formulation.

Worth exploring what are the implications of same on GTPL (manufactures Rifampicin API and its intermediate Rifa-S/O.)

Some facts to understand why the change in approach in the first place.

As adopted in 2015, ending the TB epidemic by 2030 is among the health targets of the United Nations Sustainable Development Goals (SDGs).

Milestones for 2020 was a 35% reduction in the number of TB deaths and a 20% reduction in the TB incidence rate.

However, between 2015 and 2020 the cumulative reduction was 11% only as against the end TB Strategy milestone of 20%.

Two way constrain/challenge leading to sub-optimal performance on End-TB initiative:

US$ 13 billion are needed annually for TB prevention, diagnosis, treatment and care to achieve global targets agreed on at the UN high level-TB meeting. However, so far, global spend has been in the range of US$6B annual

In fact, there was a decline in global spending on essential TB services from US$ 6.0 billion in 2019 to US$ 5.4 billion in 2021.

For research and development, according to the Treatment Action Group, only US$ 0.9 billion were available in 2020 of the US$2 billion required per year to accelerate the development of new tools. At least an extra US$ 1.1 billion per year is needed to accelerate the development of new tools.

According to latest national TB patient cost survey data, globally, ~50% households reported treatment costs to be > 20% of their household income.

Current regimen requires 90 days/120 days continued daily medication. In low per capita region and under developed countries, this longer regimen leads to discontinuation.

Considering the sheer scale, magnitude and context of Tuberclouses spread, fight has always been a calibrated global effort across different funding partners, implementation agencies, NGOs of global reach. Even in this case, global humanitarian agencies, implementation and monitoring agencies and eco-system members are working in tandem towards adoption and accelerated shift towards new medicine:

US Centers for Disease Control and Prevention: Recommend 3HP (rifapentine) for treatment of LTBI in adults, persons with LTBI aged 2–17 years and persons with HIV infection. Link

WHO: WHO encourages manufacturers to develop quality assured formulations of the game-changing drug rifapentine (Link).

Big sponsors and funding partners striking volume guaranteed pricing deals with key drug manufacturers to address the affordability barrier:

The Global Fund UNITAID and Sanofic (innovator) deal for 70% price reduction for volume committed agreement for Preftine (innovator drug). (Link)

In August 2021, MedAccess, in partnership with CHAI and Unitaid executed a volume guarantee agreement with Macleods.

Further In July 2022, they s negotiated a new agreement with Lupin to secure affordable prices for 1HP and 3HP. (link)

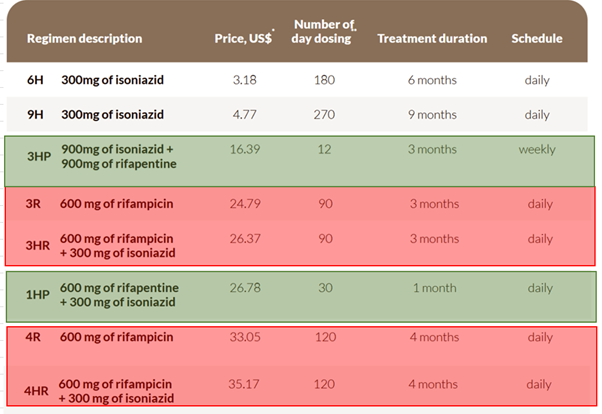

Prevailing treatment options:

P.S – On the above image, prices for 3HP and 1HP has come down significantly (in the range of $12-13) post Sanofi/Macleaod/Cipla deal with funding agencies.

Potential Impact to Gujarat Themis:

1: GTBL currently has approval for Rifampicin (API) and Rifa-S/ Rifa-O (intermediate). They are not manufacturing Rifapentine. Any decisive changes in treatment approach may impact Rifampicin volume offtake quickly.

2. Logically thinking, even GTBL can add capacity to manufacture Rifapentine since backward production value-chain is mostly identical. However there are few aspects to be thought through:

Due approvals and Environment clearance may take its own bit of time. They already have sizable capex of ~200 Crs. underway for other formulation/R&D/AI.

The API intake volume is going to drop substantially with the new medication norms – Rifampicin (600 mg * 90 days) to Rifapentine (900 mg*12 days) even if they start manufaturing Rifapentine.

Part of the volume contraction may be offset by higher mg (900 mg) requirement and lower yield (~65% yield for Rifa-S to Rifapentine as against 85% yield for Rifa-S to Rifampicin). However, even with that net volume demand loss potential could be >80% for Rifa-S intermediate.

In general, both the big players Lupin (20 MT/year) and Mcleods has capacity of Rifapentine and have mostly been ahead of curve to the regulatory changes. Will be interesting to see how GTBL respond to evolving situation.

Thanks Tarun for your insights. Couple of quick questions:

Is the Rifampicin market functioning as a cyclical commodity? In the sense, has there been a dramatic rise in the price of these API intermediaries in open market…any chances of mean reversion when chinese suppliers come back etc.?

Is fermentation the only way to produce these APIs or is custom synthesis chemically an option as well?

Any reason for clients to prefer GTBL? ( Cost, FDA approval etc.) over the longer period ?

To best of my understanding, there is no easy/direct tracking of Rifampicin domestic price trend. Even have not noticed this being tracked and reported by some of the sell side institutional desks who generally cover bulk chemical trend. However, purely by trade data section of Screener, import price has been in a narrow range for most part of the duration except some one-off spike for a short duration of time (mostly external factors) which gets normalized within months.

[ i have desisted from providing direct screener.com trade data screenshot respecting the paywall requirement. You can look up for this info directly using following HS codes, if have access to Premium features of Screener]

API Name

CAS No

HS Code

RIFAMPICIN

13292-46-1

29419011

Vancomycin HCl

1404-90-6

3004209090 / 30042096

Daptomycin

103060-53-3

29419090

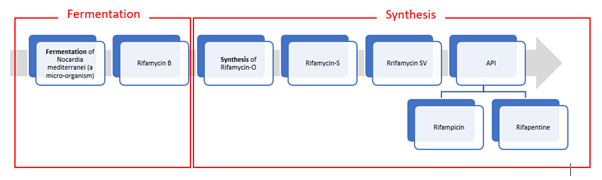

Reading through bit of back ground info about the company and product, my understanding is that Rifampicin is a fermentation only process. To best of my understanding, below is a multi-step fermentation chain from -n to Intermediate.

My personal honest assessment is that more than cost advantage or tech edge, it’s more a function of they persisting and surviving in a challenging industry while enduring brutal competition. Two pointers to this:

Listening through multiple management commentary from the industry, fermentation is a hard to master stream. Even the folks who has been successful at lab scale production finds it challenging to get the required output meeting specifications at commercial scale of production.

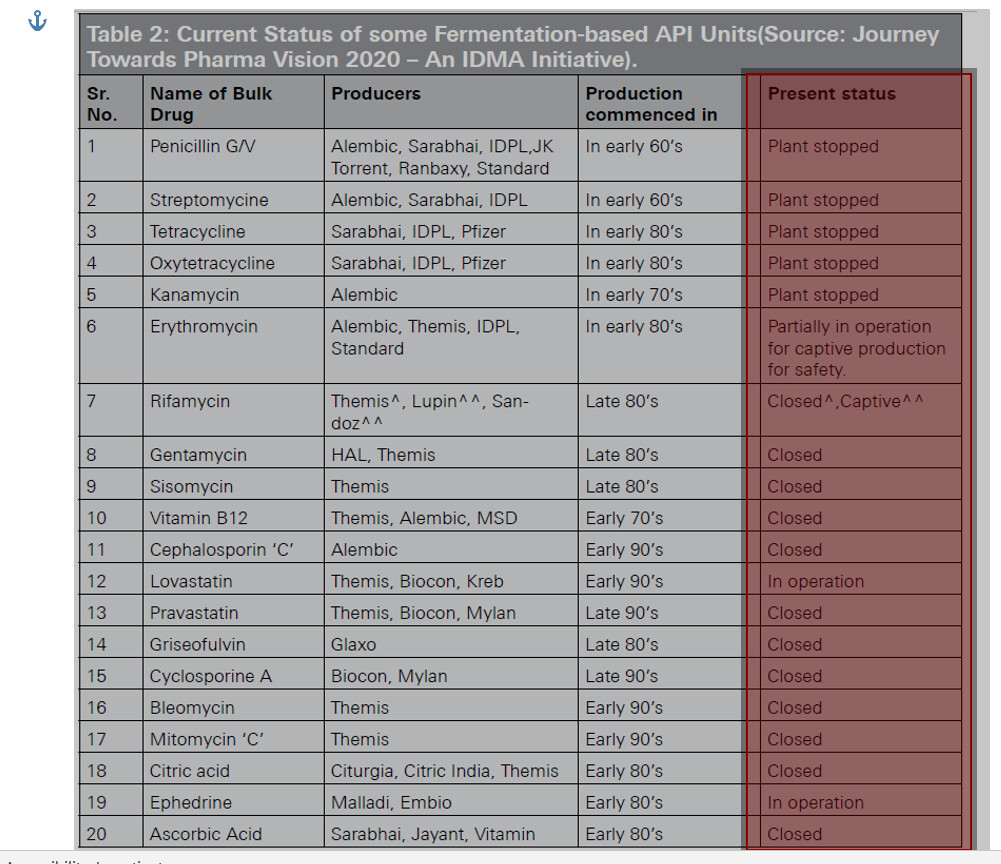

Will not be exaggeration to say, entire fermentation industry in India was brought to knees by Chinese dumping riding on low power/labour cost and favourable policy actions by state. Check the below image to see how the fermentation industry was just annihilated:

Silver lining is that Government/s has recognized the importance of independent industry eco-system and strategic importance of self-reliance. Here is a good read from Gov. thinktank on how honestly they have reflected on policy/action shortcomings and trying to course correct ( Pharmaceuticals.gov.in.pdf (944.8 KB) )

Thank you so much @T11 for taking the time out to respond. I have put GTBL on hold primarily because of the Chinese dumping point you mentioned…I am not able to make an independent opinion on whether this is done or likely to happen again.

Just my thoughts on this business.

I was holding from 500 levels to 800. But sold at 750.

My reasons were - Too concentrated product portfolio. Only 2 products and that is also in TB where there can be bigger regulation/price control.

Management is good but has to wait to see how they can actually put the new plant and diversify in other products. And that is nearly 2 years away as per the management.

And valuations are not cheap for sure. Though PE is less. Check price to sales. It’s 8 and Divi’s is at 10.

For just 2 product portfolios, a P/S of 8 is just too costly.

@ankit_tripathi - Cannt think of any direct implication for Gujarat Themis. One, they are not into the value chain of Bedaquiline. Two, Bedaquiline is second line/fall back treatment once Refapentine or Isoniazid efficacy stops.

Though should be positive for GTL customers like Lupin, Unichem or Mecleods who will get access to adjacent market (second line treatment) - at least in domestic market.

Pretty average results, no growth YoY. Token dividend declared.

Last time management said they are running at 95% capacity. Hence any growth will come only after new capex comes online. Will take 2 quarters, post that there will be customer qualifications.

Is 12 months a fair estimate before we can see any real growth?

For Q4’23: EBITDA margin is 52.98%, which is up by 751 bps. Better realization and lower R&D investment of about INR3 crores helped improve the profit margins.

For Full year FY’23: 29.71% year-on-year rise over the previous fiscal year. Growth was mainly driven by rise in volume coupled with better realizations. EBITDA margin is 49.82%.

Overall Business Outlook:

Rifa-S offtake remained on the lower side during the quarter since this is largely a tender-driven segment. Several tenders continues to be delayed and that reflects in lower sales volume year-on year.

Tenders are now opening up gradually, which is why there is a slight growth quarter-on-quarter. Otherwise, based on the inherent demand in the system, have continued the production of Rifa-S to build inventory to be ready once the tenders open up entirely.

Capex:

Capex plan of INR200 crores, spanning over two-plus years is progressing as per plan. We have capitalized about INR16 crores while another INR20 crores is in CWIP and about INR10 crores of capital advances for the equipment have been given. Another INR30 crores or INR40 crores expected to be expensed by September 2023.

Breakdown of capex cost:

R&D lab cost: ~9 Crs.

R&D pilot suite (1&2)- ~33 Crs.

Fermentation block 1 - ~80 Crs. (3 additional blocks may come subsequently however not part of current 200 Crs capex plan). Expected to be up and running by the end of next calendar year.

The new warehouse, R&D and API block is expected to be ready by September ’23. these new facilities will be compliant with global regulatory norms since we shall be targeting export markets in addition to the domestic market.

The last leg of our capex will be the new fermentation facility, which are expected to be ready by the end of the next calendar year.

Asset-turn/Top line projection from capex: Hard to give numbers at least at this particular stage - may be practical post few few quarters. We are more looking at in terms of how quickly we can get the ROI, rather than asset turnover.

Challenges in commercial scale-up of identified new products - it is possible that scale-up from pilot to fermentation is tricky, we’ve dealt with multiple products in the past, our team has dealt with multiple products in the past and we are confident enough to invest in the whole project.

Impact due to TB medication regimen change/market disruption (from Rifampicin to Rifapentine):

WHO recommendation for moving from rifampicin to rifapentine is a very recent development, It happened sometime during the course of last year. WHO will also go cautiously because they need to figure out, on the larger population side, how rifapentine is actually effective.

We consider a scenario where rifapentine is going to be the mainstay instead of rifampicin tomorrow, it really affects us very positively. First of all, Rifa-S that we currently supply to manufacture rifampicin is the same intermediate that is required to manufacture rifapentine. The second part, amount of rifapentine which needs to be given as per the new WHO treatment is quite significant. Also, ratio of conversion of Rifa-S to rifapentine is lower than that of rifampicin, which means we need more Rifa-S, to make that amount of rifapentine, vis-a-vis, rifampicin.

And, of course, not to lose sight of the fact that we are coming out with a API block, so we also have very much plans to manufacture rifapentine. Realistically speaking, we can expect rifapentine business to start in the next financial year or the API business to start in the next financial year or end of this financial year

There’s a market locally for Rifapentine, because as in line with WHO, even the Indian government is moving from rifampicin to rifapentine. We believe that there is going to be a reasonably good requirement for rifapentine in years to come.

May not have much changes to customer mix even if market shifts from rifampicin to rifapentine. There will be things that we will do, but only in consultation and cooperation with customers.

Overall think this was very good call to clarify apprehensions on medication regimen changes and impact thereof on GTBL. Broadly, with reasonable certainty, its established now that Rifapentine is going to be the preferred treatment approach- both globally and domestically. Another re-assuring part is that management finally divulged the intent of venturing into manufacturing Rifapentine once new API block is ready. In that sense, not much of existential threat (which otherwise could be significant situation for 2 product, 2 client company) rather could significantly increase intermediate Rifa-S demand (as per management guidance)

Thanks @T11 - As always super interesting. Just wanted to quickly check on a couple of things:

What happens if the GTBL’s customers do not win the tender? How is GTBL sure they will ultimately be beneficiaries of the tender?

Any idea on what is the market share of GTBL in Lupin/Optrix for the articular intermediaries?

Does LUpin & Optrix buy both the intermediaries or Rifa -s is with Lupin & Rifa-O is with Optrix?

By any chance would you also know from whom does Lupin/Optrix competitors procure the intermediaries for the same APIs? Is that costlier/similar price as as what is being provided by GTBL

Sorry for the delayed response. Some inputs based on my understanding:

Rest all things being equal, global tenders are reach (overall and geo specific number of product approvals), scale (volume, backward integration) and depth (width of product portfolio) game.

Lupin has been largest supplier of anti-TB drugs for years. Globally Lupin has second largest product approvals (20+) from WHO while rest of the players have low single digit product approvals (except Macleod Pharma, who has 32 approvals and is emerging really well). Due to backward integration into API and intermediates (in some cases) and scale of operations, they have been able to offer competitive pricing. Another aspect, i think could be agility to adopt to newer medication developments (case in point could be MDR TB, pre-adult TB medication, Rifapentine adoption) etc. where Lupin has been able to garner a significant place for itself by being in sync.

Keeping above points in mind, hard to fathom a situation where Lupin does not get a share in Tuberculosis tenders pie - unless, they lose focus or get caught in compliance issues.

Not sure on GTBLs exact valet share in Lupin and Optrix demand, however, my understanding is that only Olons (Sandoz entity) and GTBL has domestic capacity of Rifa-S and Rifa-O.

To best of my understanding, Lupin is customer for Rifa-S and Optrix for Rifa-O. (just my understanding).

Other India based competitors for Tuberculosis business are Micro labs, Cadila, Sandoz and Maclods. As I mentioned above, as of now, Olon (Sandoz) is the only other domestic fermenter of Rifa-S. Macoleds has recently got PLI approval for Rifa-S, however, that may cater in parts to captive uses. GTBL has indicated that they have started catering to 2 other domestic manufacturers, though in small quantity. Rest of the demand, if any, I presume is met from China supply. On price competitiveness, I am not too sure, however, looking at margins of GTBL, least likely that there is too much of Chinese competition at the moment (however, one never knows enough about China).