FY22 AGM Notes:

• Very Few Global Players in this industry

• Number of Customers increased to 6 – 3 major clients, 3 minor clients

• 1st Phase of Capex to be completed in Mid-2023; 70% in Plant & Infra, and 30% in R&D

• Total capex of 1st Phase – 80 crores (internal accruals)

• ICD – Safely invested (predominantly in Debt Funds)

• Running at 70-85% capacity right now

• Expect the Demand to be strong

• Concord Biotech is the only peer that will enter the listed space (DRHP filed). Anyways not too many players in public and private.

• FY22 – 20% volume growth

• No capex done for expansion yet. The ones done last year was purely for upgradation and R&D was partly for expansion

• No new customers have a take or pay or any other kind of arrangement. But they are planning to have it in future

• Rifa S – contributes 60-65% of Sales

Thanks a lot for the notes, I have been looking for them.

Which industry mgmt refers to ? RifaS, RifaO ? or fermentation chemistry based industry ?

Just trying to see, if I got the status of first phase of Capex right. So this 80 cr. is to be spent by Mid 2023, out of which 70% to be spent on infra & plant and 30% on R&D. Once this is complete will it enhance capacity ? by how much ?

Any info on what kind of asset turns they expect out of this expansion in plant.

Any news on what kind of capex is planned for second phase ?

Any news on the kind of new products they are planning ?

If they meant, fermentation chemistry based competitor, then Natural Capsules will become one once they complete capex by this year end.

Disc: invested.

In recent couple of years, there has been few noteworthy developments with this otherwise slippery company.

- Significant improvement in top line and margins – EBIDTA margin turbo charged from 18% to 50% between FY’19 – FY’22. Likewise, top line expanded by ~3x between the same period.

- Announcement of sizable capex of ~200 Crs. over next 2-3 years (for context, current Net block is 20 odd crores.)

- Cessation of long-standing relationship with Yuhan Korea. More than change in ownership construct, it has higher implications from technology atmnirbhartha’ and capability maturity.

- At the same time, change of business model with largest/longest customer (Lupin) – from contracted job work/conversion operations to market-based operations. While previous model was much stable and risk-free in nature, margins awarded were commiserate. Again, remarkable that this customer has been saviour of short for longest possible time in companies’ history with some benevolent loans under most liberal conditions

- Healthy liquidity for past two years for a company who was walking on clutches of BIFR/customer advances and hypothecated assets just couple of years back. Free cash and cash equivalents stood at Rs.39.40 crore for FY’21. adequate liquidity position reflected in free cash and bank balance of Rs. 32.70 crore for FY’2022.

Capex:

Upcoming Capex:

-

Overall ~200 Crs capex over 2 to 3 years. Looking at a portfolio of six products. Replacement of imports plus new products which have just come out.

-

Average capacity Utilization has been ~60 – 70%. As per recent concall, not increasing capacity for our current products, but we definitely see a lot of opportunity in terms of introducing new products which we are working on in the facility.

-

Current capacity.

-

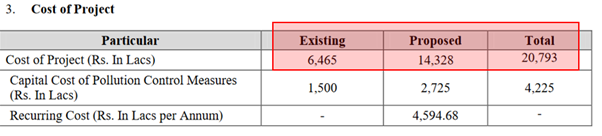

Recent Environment clearance proposal (SIA/GJ/IND2/176366/2020) cost of capex 143 Crs. (total 207 Crs.)

-

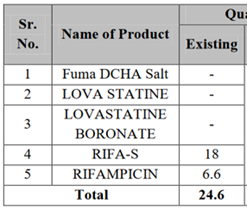

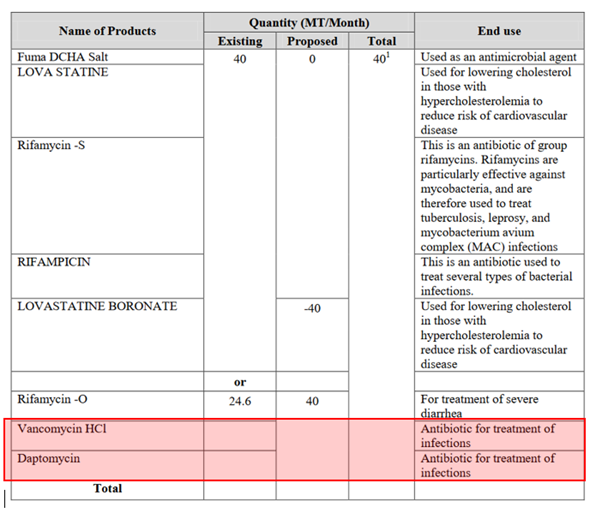

In summary, Vancomycin HCI and Daptomycin are the two new intermediates that they are adding while dropping/transferring out existing intermediate “LOVASTATINE BORONATE” (possibly to other entity Themis Medicare).

-

My understanding is that this reference of 200 Crs. capex and 6 products is a cumulative numbers between last Capex (SIA/GJ/IND2/20578/2017) and current proposed capex (SIA/GJ/IND2/176366/2020).

-

Current update on Capex: GTBL has undertaken capex wherein it is setting up warehouse and research and development department at its existing plant located at Vapi, district- Valsad. Total estimated cost of the project is Rs. 32 crore and entire project cost is to be funded through internal accruals. The land for the same is already in place and company has incurred Rs. 18 crore towards execution of the project through internal accruals till mid of 2022. Project was started in June 2021 and is expected to be completed in December 2022.

GTBL Product Profile:

Rifamycin S →

-

Started manufacture of Rifamycin S an intermediate for Rifampicin 2011. Rifamyicin S production capacity of 10,000 KG/month currently running at full installed capacity.

-

Rifamycin is used for treatment of several types of bacterial infections. India is the largest single market in the world of this therapeutic class where about 50% of global consumption of Rifampicin takes place.

-

India’s total import value is 273 Crs. (303 MT). 98% of import coming from China.

-

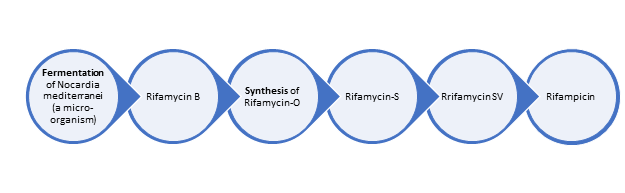

Process Complexity/Edge: Manufacturing process of rifampicin consists of two stages, viz :

i) Fermentation;

ii) Synthesis

-

In general, industrial fermentation technology is very difficult to master. Rifamycin fermentation is even more difficult and complex since the behaviour of the micro-organism could not be fully understood nor have all the conditions been identified which would give an optimum yield.

-

The synthesis stages, though not simple, are not as difficult as the fermentation stage.

-

fermentation yield is the most critical stage which determines the overall process efficiency. One of the most important parameters for determining the quality of the product is the bulk-density of the (uncompacted) product. Higher the bulk density higher is the bio-availability of the drug. Higher bulk density is obtained by proper crystallization

Rifamycin O → Started sale of Rifamycin O from September 2019- Capacity of Rifamycin-O is 6,000 Kgs/Month. Rifaximin is used for treatment of diarrhoea, irritable bowel syndrome, and hepatic encephalopathy. Owing to complex fermentation capabilities with high capex involved, there is high entry barrier.

Vancomycin-> (HS Code 30042096) - Vancomycin is in a class of medications called glycopeptide antibiotics. It works by killing bacteria in the intestines. It is used to treat colitis (inflammation of the intestine caused by certain bacteria) that may occur after antibiotic treatment. The approved product has an estimated market size of US$ 94 million for the twelve months ending January 2016 according to IMS.

100% import (contradictory since Concord has capacity of ~10 MTPA)

Daptomycin-> - Daptomycin injection is used to treat certain blood infections or serious skin infections caused by bacteria in adults and children 1 year of age and older. According to IQVIA (IMS Health), Cubicin® for Injection (daptomycin for injection) had U.S. sales of approximately $606 Million for the 12-month period ending June 2019

Customer Profile:

GTBS is largely a two customers Lupin and Optrix (Optimus Group company) accounting for majority of revenue (ranging between 80%- 90%) two products company:

- FY 2020: Revenue arising from sale of products to two customers amounted to INR 33 Crs. and 34 Crs. respectively.

- FY 2021: Revenue arising from sale of products to two customers amounted to INR 61 Crs. and 26 Crs. respectively.

- FY 2022: Revenue arising from sale of products to two customers amounted to INR 42 Crs. and 62 Crs. respectively.

Lupin

-

Is a global leader in the anti-TB segment; it is the world’s largest manufacturer of Ethambutol and Rifampicin (through the complex fermentation process). Its Rifampicin plant is one of only three plants in the world approved by the USFDA

-

Lupin **may have 120-tonnes per annum (tpa) rifampicin capacity **. Lupin’s large installed capacities ensure that we they among the global leaders in the supply of key APIs for anti-retrovirals, anti-malarials and first-line TB treatment drugs – Rifampicin and Ethambutol.

-

Lupin has strengthened its market leadership by signing a non-exclusive agreement with TB alliance for Highly Drug resistant TB. TB Alliance has granted Lupin, a non-exclusive license to manufacture the anti-TB drug pretomanid as part of the three-drug “BPaL” regimen. Lupin intends to commercialize the anti-tuberculosis (TB) medicine in approximately 140 countries and territories, including many of the highest TB burden countries around the world.

Optrix (Optimus Group):

- ‘take or pay’ agreement with Optrix Laboratories renewed annually.

- In 2018 Unichem had acquired 20% of shares for ~48 Crs. in Optrix Laboratories Pvt. In a recent development in May’22, PAG consortium has acquired controlling stake in Optimus Group. The PAG-led consortium will invest a total of around Rs 2,000 crorefor a 74% stake each in group entities Optimus Drugs Pvt. Ltd, Optimus Pharma and Optimus Lifesciences

Global Manufacturing Know-how:

-

There are four main regular manufacturers (fermenters) of rifampicin in the world, viz : Lepetit (Italy), Ciba-Geigy (Switzerland), C.K.D., (S. Korea), Youhan (S. Korea).

-

Besides the above, Proter (Italy) is also a regular manufacturer of Rifampicin intermediates

Key Domestic Competitors:

Based on limited reading, Indian Fermentation industry has faced significant challenge from China and most of them died a slow death (or went into BIFR etc.)

Olon Active Pharmaceutical (hived off entity of Novartis/Sandoz):

-

Indian operations were set up in 1997 as a joint venture under the name Ciba CKD Biochem Ltd. to produce Rifampicin. This operation was merged with Novartis in 2001 and changed to the Sandoz API - Business Unit in 2005. In 2018, the Novartis divested Mahad facility to Olon S.p.A Italy.

-

Olons Capacity:

Rifampicin – 160 MTPA

Rifa – S – 53 MTPA

Rifa - O pure- 60 MTPA

Rifaximin – 80 MTPA

MacLeods:

- They are global #5 player in TB treatment with highest number of WHO pre-qualified anti-TB product registrations with 32 registrations, as at December 31, 2021.

- MacLeods is in the process of setting up 200 MTPA Rifampicin capacity in the upcoming facility in Jammu (cost outlay of Investment of Rs 200 Crs.) Interestingly, they have approval under PLI.

- The PLI Schemes entitle eligible manufacturers to receive 20% financial incentives for first 4 years, 15% for year 5 and 5% during year 6, on meeting certain sales and investment targets based on the product-category.

Concord Biotech

- Vancomycin - has applied for 10 MTPA capacity

- Daptomycin - has applied for 2 MTPA capacity

Open questions:

1.Personally to me, most perplex part of this jigzshaw puzzle has been the fundamental question…..why was the company into this job/conversion work based model in the first place if market based sale was/is so remunerative? Was that just for the paltry loans of 5 – 7 Crs. that company was getting from its customers from time to time?

Look at the loan from Lupin:

- 2012: Secured loan 3.75 Crs. Returnable non-interest bearing loan and is repayable against 5 0% of the “Conversion Charges” for each invoice raised by till such time the loan is recovered in full.

- 2013: Secured loan reduced to 1.61 Crs

- 2014 -2016: No outstanding loan

- 2017: Unsecure,non-interest bearing Loan of 1.90 Crs.

- 2018: Unsecure Loan, non-interest bearing of 0.20 Crs.

- 2019: Loan amount went up again. Unsecured loan 5.98 Crs.

- 2020 onwards: Loan paid-up. No outstanding

Loan history with Optimus:

- 2020: Secured loan 8.15 Crs.

- 2021: Starting outstanding 3.02 Crs., paid withing year, zero outstanding

- 2022: No Loan

(a). Were promoters in individual capacity not able to infuse this low-ticket amount? What about other shareholder Pharmaceutical Business Group (India) Ltd which has backing of Themis Medicare Ltd., Kopran Ltd., Anant & Co., Cadila Health Care Ltd. (Zydus) and Lyka Labs Ltd? Even all of them collectively were not able to pool this amount as loan?

(b). Or, in the past, margin had not been so worthy under market-based model for the risk involved to tilt the decision in favour?

- As per one of the recent concall, GTBL is adding two more customers. Who are those prospective customers and for which therapeutical areas ? For Rifa-S and Rifa -O has little headroom only since operating at ~70% capacity and are not expanding capacity there. Scanning market landscape for Vancomycine and Daptomycine can give some clue.

- Sustainability of high margins? Mcleoads adding significant capacity (200 MT) just for Rifampic and have competition killing edge due to 20% incentive for 6 years under PLI. This huge capacity will find its way in domestic market only to avail PLI benefit.

- Working capital is expected to get elongated since historically 50% of Lupin sales was getting adjusted against unsecure loan. In market pricing-based model of operations, that privilege is gone.

Tarun

Disc: No investment

Hi Tarun,

You have nicely summarised about the company. Regarding your question about having to do job work in the first place, the company was declared as a sick unit for the second time when in 2013 the new promoters brought in lupin as their client to do job work, without the need for WC and get out of the mess.

And regarding Mcleods adding significant capacity, it has been communicated that they are just setting the capacity that they used to earlier import from China. So for now the known capex through PLI is for captive consumption

Tarun - can you please clarify the source of the information on the Customers and the amount of sales made to each one of them.

For recent years, they are capturing this info under Segment reporting section of the AR. (Hidden inside ‘notes to accounts’ section):

Hope that helps,

Tarun

Hi @salonihemnani011 - Appreciate your perspective. I understand Lupin was de-facto saviour to tide over the BIFR situation. Me questioning the continuation of conversion/job work based business model was more around post BIFR phase. Company became net worth positive in 215-16 and was out of BIFR (SICA act was repealed in 2016).

Also, based on my reading the terms of loan from Lupin, first loan (3.75 Crs loan between 2012 -2014) was helping them from working capital (at least debtor days) since the 50% of the loan was getting adjusted against ‘conversion charges’ invoice. However, the second loan in 2017-18 for ~2 Crs. did not had the clause of loan being re-couped against conversion work. In that sense, my guess that it was not much WC accretive.

May be, it has to be looked at in context of the unstable history that the company (unfortunately) had, China choaking entire fermentation industry and the sheer market dominance that customer had.

Nevertheless, a positive sign if management is making some bold and decisive moves while being conservative and resilient for a very long period.

Thanks,

Tarun

Yes it is a positive announcement as rifapentine requires higher amount of rifamycin s than rifampicin. The yield is therefore higher.

So from backward integration, Lupin is referring to Gujarat Themis capacity only ? or is it something else ?

Good results… https://www.bseindia.com/xml-data/corpfiling/AttachLive/fde407d0-ffd1-46a1-be2d-b6b51b82ea72.pdf

Theres a concall tomorrow at 10:30 am

Update : Concall has been postponed to 16th nov

Some rough notes from Q2’23 call. Missed the first few minutes of mgmt update

capacity utilization : 95%

Capex : 200 cr. in 2 to 3 years, period starting from last year when it was announced. (to be funded mostly by internal accrual).

API block (capex : 40 cr.) : To be ready by end of next year (end of Q2’FY24). Market in RoW, US, domestic market too. So once plant is ready, some business can start, while regulatory approval work is getting done for regulated markets.

Fermentation Block (Capex : 160 cr, 3 plants, in phased manner over next 2 to 3 years, no capex done so far, project is under planning. Plan to start work by next month): By end of next to next year.

Asset Turn : Not thinking in terms of asset turns, but payback period 3 to 4 years.

New Product (under development) : product details not in public domain. Looking for products with lesser competition. May have dozen products in development, but very careful in what we want to make commercial.

Existing Product : No guidance on margins as pricing is not under their control. Don’t want to speculate on pricing.

New customers : 2 to 3 added but volume is low

Tuberculosis : Tender driven business so if tenders don’t open then business volume can get impacted. But overall worldwide the number of patients remain stable.

Competitor: has filed DRHP seeking double the valuation. (which one ?)

I couldn’t attend the concall. If capacity utilization has already reached 95 % , any comments from management on where the growth will be coming from in next 1 year as all the capexes will take good time to fruictify .

Fermentation block has not started yet . Does it mean that they are dependent upon the success of new products development & their commercialization potential ?

Competitor : I think they mentioned in previous calls “Concord Biotech” as likely competitor.

The reference is for Macleods (DHRP link). worth reading from page 145 if someone really wants to understand Tuberculosis (TB) market.

Thanks,

Tarun

Hi, sharing below the concall audio link held on 16-11-22

Hope it helps.

dr.vikas

HDFC securities recently came out with a coverage report on Gujarat Themis. This report has some additional clarity on the 200 Crs capex.

In terms of the capacities, the total fermentation capacity is about 450 cubic meters and the company plans to double this for which company has already received the EC clearance. With regards to raw materials, the company is not dependent upon China.

-

GTBL is implementing capital expenditure of about Rs 200cr. It would be for i) a new R&D Lab ii) increase fermentation capacity and iii) API block.

-

Fermentation business would have three blocks and would be commissioned in a phased manner. The capex would largely be through internal accruals. Payback period for new capex could be 3-4 years. Fermentation capacity could come on stream in H1FY25.

-

Company is setting up API unit with an outlay of ~Rs 40cr. It will cater to regulated markets, EM and RoW markets. In the new products, margins could be slightly on a lower side, however there won’t be significant impact on margins. It is likely to come on stream by the end of FY24.

-

R&D centre is expected to be completed by Q1FY24. It would be compliant with various regulatory authorities

Also, this snippet from the report has clarified some of the open questions that people raised during last concall in terms of possible stake increase by Patel Family/Themis Medicare entity:

Themis Medicare approved additional investment in Gujarat Themis Biosyn Limited (“GTBL”), an Associate Company by way of purchase of 91.4 lakh equity shares (6.47% of equity share capital of GTBL) from an existing shareholder of GTBL, viz. Pharmaceutical Business

Group (India) Limited (“PBG India") at Rs 745 per share. On completion of the said purchase, the company’s shareholding in GTBL would increase from 23.19% to 29.66%. This acquisition was however called off later.

Tarun

Disc: Tracking, no investment

Could you share the report