Intro:

https://www.screener.in/company/506879/

- Market Cap: 290.21 Cr.

- Current Price: 199.75

- 52 weeks High / Low 205.00 / 31.40

- Book Value: 29.05

- Stock P/E: 12.26

Gujarat Themis Biosyn Limited (GTBL), located at Vapi, Gujarat, was incorporated in 1981 as a joint sector company with GIIC Ltd. and Chemosyn Ltd. (possibly NCL, Pune helped) commencing production in August, 1985 by producing Erythromycin and Erythromycin salts and formulations. The company was subsequently taken over in June 1991 by the Yuhan Group (one of the biggest South Korean pharma cos) and Pharmaceutical Business Group (India) Ltd. (PBG); a unique consortium of five competing drug companies - Themis Medicare Ltd (TML), Kopran Ltd., Anant & Co., Cadila Health Care Ltd. (Zydus) and Lyka Labs Ltd. It is being actively managed by Themis Medicare Ltd. (JV Company of Gedeon Richter Ltd, Hungary) since 2007. The company manufactures active pharmaceutical ingredients on job work basis for Lupin Ltd.

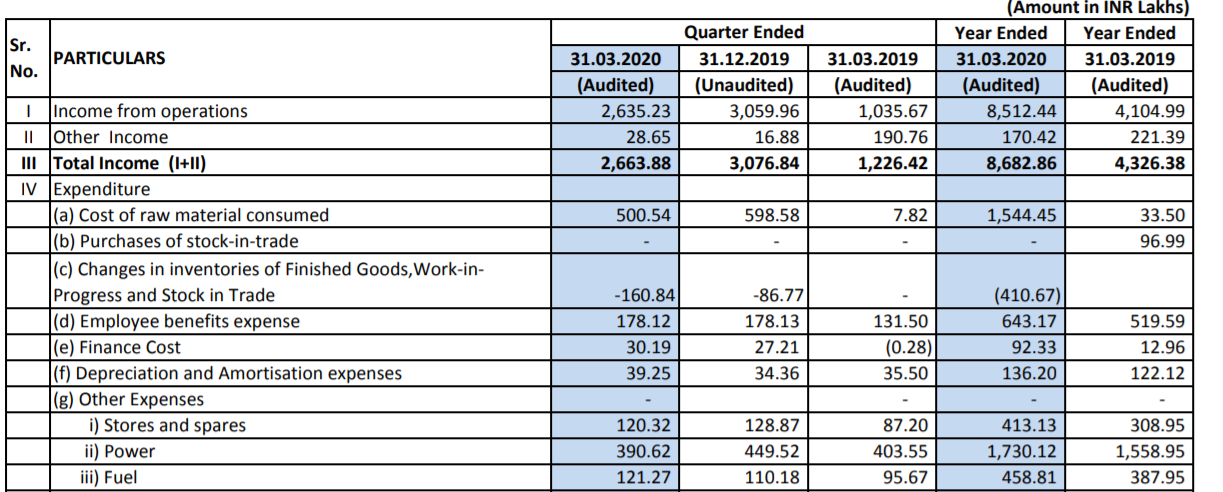

The latest results show that the company has re-classified its business from contract manufacturing to bulk drug seller.

Collectively 3 promotor groups (Themis, Yuhan and PBG) own 75% distributed equally, the rest is public. Somehow they are the only manufacturers of Rifampicin in India. Overall seem to have large fermentation facilities to make such drugs. Now they have added anti-cholesterol Lovastatin to this.

Discovery:

I got this investment idea from @kdjolly who had posted once on valuepickr an analysis of the company. The product is used in TB multi-drug combination therapy so market is big and growing, till some new science changes the treatment.

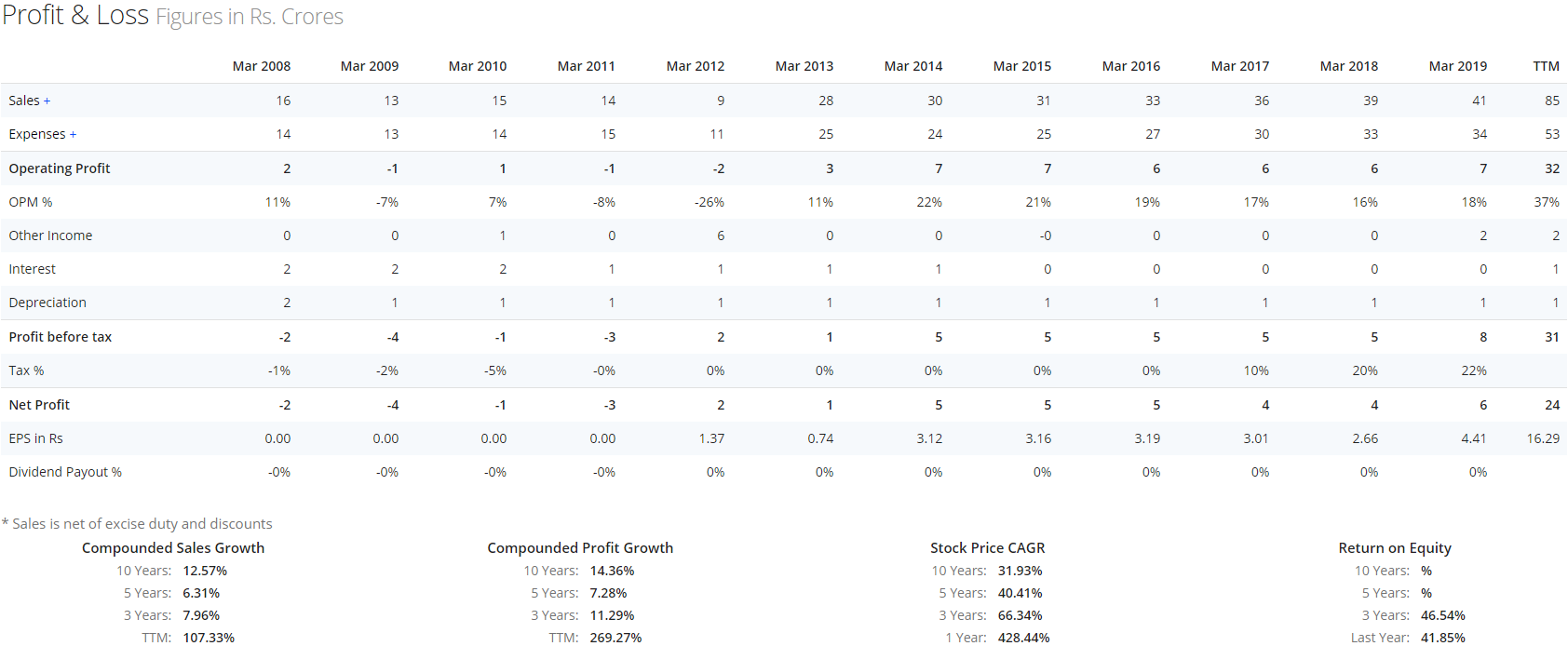

The technology is from Korean company which has also invested in it, 25% stake. The idea is that they may replace China (whose imports may have caused the problems for this co) as source of more anti-biotics and have started looking beyond Lupin, another investor and collaborator/buyer. CAGR is quite uneven, company had early turnaround from BIFR in FY2016 technically but only acknowledged in FY2018 AR. Now it appears that it is able to deploy a strong growth strategy. How much momentum can be sustained is difficult to say, I cannot find much details on this, hence, took a small position in overall PF.

More details: :

AR 2019 has very less interesting disclosures.

Gujarat Themis, went into BIFR in 2008 under the impact of consistent losses and debt. Under the scheme of re-habilitation a lot of operating and functional changes were brought in the company. The Face Value of each share of the Company was reduced from Rs.10 to Rs. 5 and the reduction in the value of equity shares was utilized to write-off a part of accumulated losses of the Company . Themis Medicare Ltd. was inducted as co-promoter of the Company and issued 2928702 shares of FV rs 5 at 10rs each. The induction of Themis as a co-promoter brought in the much needed sting and zeal in the operations of the company. The new promoters also brought in the sole long term customer in Lupin . Lupin’s deal with GTBL changed the fortunes of the company. The contours of this deal were very lucrative for GTBL. GTBL entered into a contract with lupin to supply Rifa (with the technology know-how brought in with another co-promoter – Yuhan Corporation). Lupin gave GTBL interest-free loan for capex that was required to finish the contract. This loan from Lupin was a returnable non-interest bearing loan and was repayable against 50% of the “Conversion Charges” for each invoice raised. So, this deal was beneficial to GTBL in more than one ways. Needless, to say this contract brought in very good topline and bottomline for the company.

To the credit of GTBL, with each passing quarter the company has been improving its operating efficiency and it now has one of the best operating parameters in the industry. With announcement of the supply agreement with Lupin that started from 1st April 2015 – Mar 2018 the company got solid visibility to its earnings. This had a very positive impact on the fiscal position of the company. Since the company came out of BIFR, the company will expand to newer products. Additionally, the company is also exploring the possibility of “offshoring” some of the manufacturing of its another promoter, Yuhan Corporation. Given the already established operational efficiency of the company any increase in revenue would significantly add to the bottomline too and the company is expected to clock significant revenue and profit growth in the years to come.

From AR FY2018

which may explain more freedom in operating decisions and general uptick in revenues since then.

Products as per cos website:

http://www.gtbl.in/products/

Concerns:

- Themis seem to dominate the overall management and that could be a concern given that they themselves have a chequered track-record.

- Investor friendliness may also be an issue due to promoter domination but that may improve(?) as company scales operations. Currently they do not have even latest reports on the company website.

- AR 2019 mentions full capacity use, but does not disclose any investments in growth, so current spurt in revenues and huge jump in margins is a mystery.

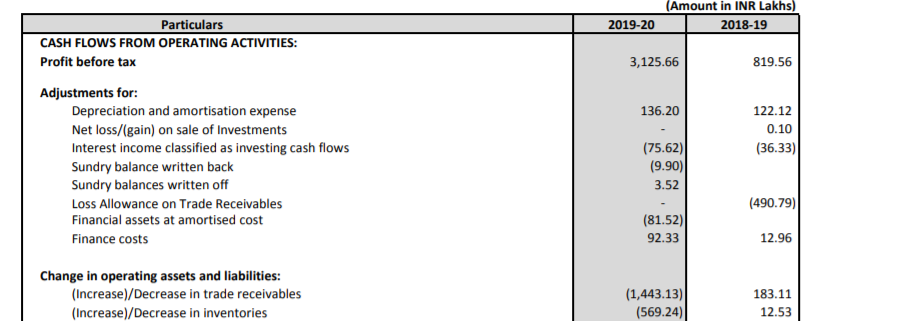

Financials:

Zero debt with high ROCE of 45% and first dividend announced in latest quarter.

https://www.screener.in/company/506879/

Sources: (from 2015)

Disc: 3% of PF, freshly acquired this week