Annual Report Summary - Gujarat Gas

https://drive.google.com/file/d/1YQF0np7q0iDwGcGqp3m-AIAM_rLEZ9Cq/view?usp=sharing

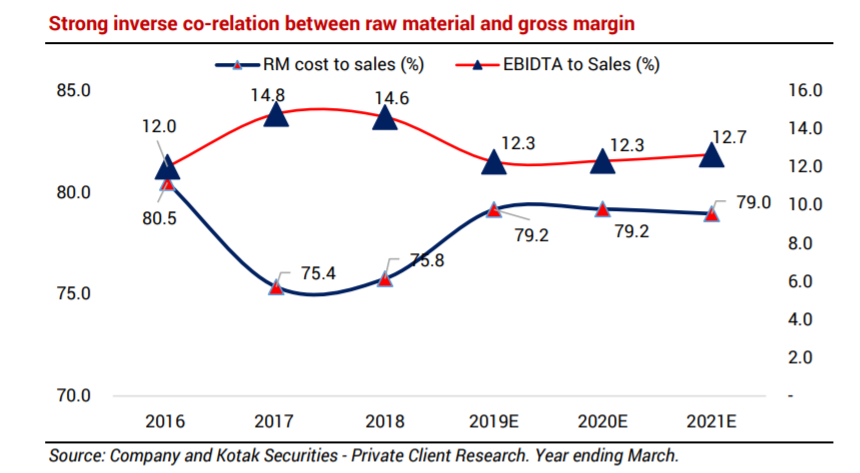

Improvement in Operating Margins to 18.85% in 2021 from 13% in the fiscal 2019 and 16.44% in 2020. This is mainly because of decline in the spot LNG prices. Also, the sourcing mix has tilted towards the cheaper spot LNG to meet the incremental demand of industrial customers.

Doesn’t it make sense to buy GSPL (parent company) instead of Guj Gas. GSPL mcap is lower than value of Guj Gas holding. So effectively GSPL stand alone business is free.

At current prices, 54% holding of GSPL is valued at 24,000 cr whereas GSPL mcap is only 17,600 cr.

I too want to know why GSPL is also not trending higher or valued higher as they own GujGas. I have invested in both and started focussing on GSPL as they have Gujgas and other dist gas n/w. At least to my untrained eyes, GSPL holdings should reflect Gujgas dividend income at least, no?

Target of 730

Q2FY22 Results Out - Link:

Summary:

Q2FY22 EPS: INR 3.62 (Down 47.5 % YoY)

Reason: Increased Gas Cost. On YoY basis, ‘cost of materials consumed’ up by ~88% whereas revenue up by ~44%

Added 26 new CNG stations

B/S, C/F statement’s KPI:

Cash + Bank Balances: ~424Cr.

Borrowing (LT+ST): ~ 521 Cr.

Repaid Borrowings: ~ 376 Cr.

Invested in Capex: ~673 Cr.

Hi Surender - Thanks for the right up. Insightful. Just curious if you were able to get more details on the below in your research -

- Raw material sourcing & pricing - If you notice, both GSPL and GGL Sep 21 quarter sales were high but OPM showed substantial reduction because of raw material. Further, in your table, you would notice, GGL has the lowest OPM vis a vis competitors though it has highest volume. Reading both together, is this because GGL is at a disadvantage on raw material sourcing & pricing front? Note that both IGL & MGL did not report a substantial drop in OPM for Sep 21 qrtr.

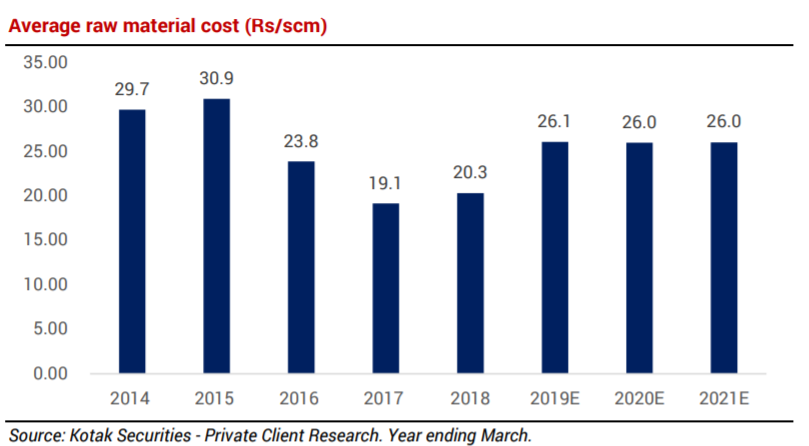

Historically, this seems to fluctuate over the years - see screenshot below from Kotak report. Reading analyst report, everyone is bullish on volumes (can see that panning as it expands in new geographies and move to clean energy with the exception of CNG stations below) but if raw material cost eats that away, earnings would not rise as witnessed in Sep 21 qrtr. ARs (no concalls) have no info about how this risk is hedged. While studying GSPL, it mentions that it works on open access (credit rating report also talks about it) and thereby insulated from change in natural gas prices - 20% of its supplies are to GGL.

- Read that company is setting up 60 CNG stations. With move to EV, is this a good LT strategy? What would be the capex? How could this be leveraged post move to EV? Though GGL’s biggest volume comes from industry and commercial clients currently, would this change the mix and thereby convert to a threat in EV era which is expected to span out in 3-5 years?

Interested to get thoughts. Thanks!

Here is my opinion:

GGL’s majority of sales (~80%) are to the industrial/commercial customers who are more prone to prices of alternate fuels instead of EV theme. For the industrial/commercial customers, raw material (R-LNG) is imported and its prices are determined by the international market. Hence, every business is at equal footing. Net result for GGL (as I anticipate the volume mix to remain as is): Higher volumes, minor impact from the EV theme but lower margins. Once a customer is onboarded, business has pricing power. Any immediate loss can be regained but with a lag. On the other hand, IGL & MGL are B2C businesses and I think that they are more prone to EV adoption.

Capex - Expected annual capital expenditure of Rs 1000 crore for the next 3 Yrs, mainly to be met through internal accruals.

Number of CNG stations are upfront committed while bidding for any geographical area and must be honored to avoid penalties from the regulator. I assume that they would find ways to become nodes (charging network, battery swapping network) in the vast network of EV while servicing the regular vehicles for ~ 20 Yrs.

Disc: Invested.

Surender,

Thanks for the swift response.

Based on the annual report of the company, GGL is shifting its focus from industrial to domestic/CNG stations. Below is one of the extract for reference (this is also mentioned in other places in the AR) -

Your Company has continued its focused efforts for developing and growing PNG (Domestic) and CNG business. Your Company added more than 1,02,000 residential customers and erected / commissioned 150 ne w CNG stations during the year (including the GAs of Amritsar and Bhatinda). Your company is aggressively planning for penetration in PNG (domestic), PNG (commercial) and CNG (transport) sector which is comparatively less volatile.

Going back to the question on raw material, here’s chart from AR -

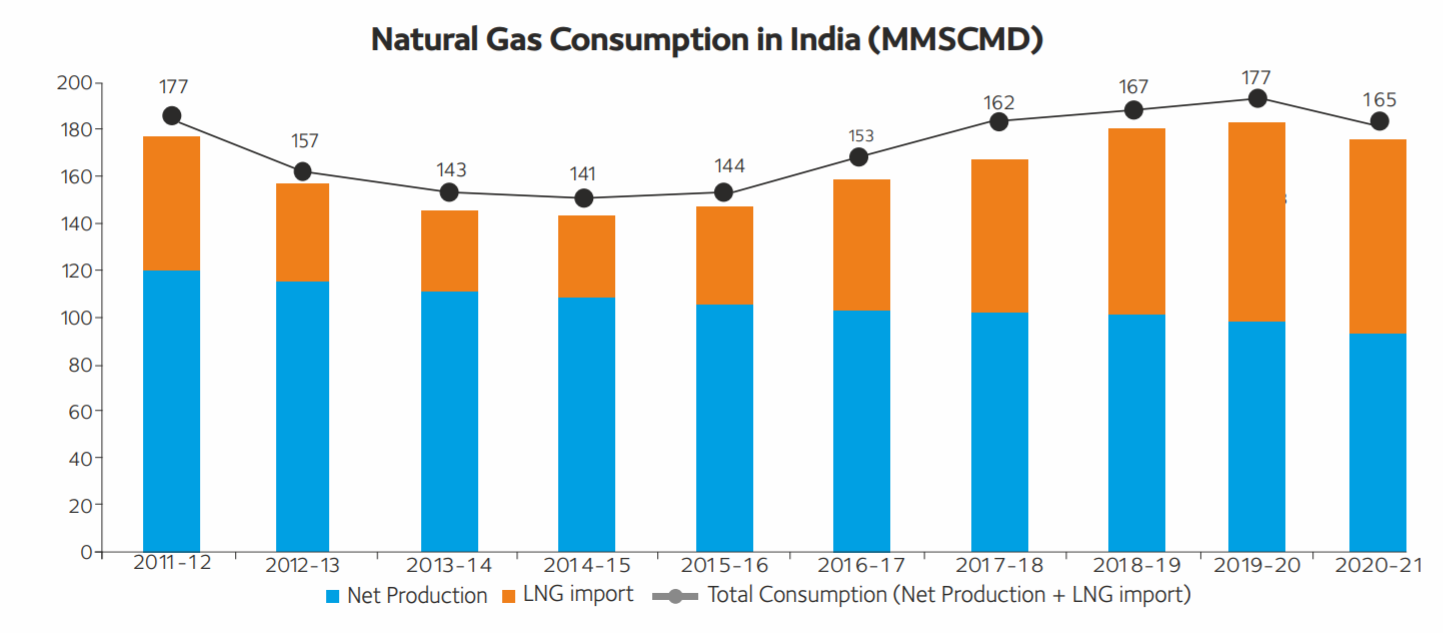

As you would notice, demand in 2019 was same as 2011. However, in 2019 this was met almost 50% by LNG import which was 25% in 2011. While there is no mgmt commentary/concall, I am guessing this (constant domestic gas supply and increase in LNG imports coupled with crude oil increase post C19) has lead to fall in margins in Sep 21 qrtr. It did not impact earlier as crude prices were low on account of COVID-19. AR also acknowledges it.

Hence, was wondering how do GSPL and GGL hedge this risk apart from price increase? Would IEX or increase in domestic gas production help?

What is the competitive advantage that IGL or MGL have as their OPM margins have not seem a substantial fall in Sep 21 qrtr vis a vis GSPL/GGL. Even if GGL has pricing power, if price increase happens, natural gas would lose its competitiveness to alternative fuels (trying to get more data on the gap - until what time can co. increase prices. it has already cumulatively increased by 70%) and within the Morbi area, there is not much room for volume growth. It would come from new avenues like CNG/domestic or new geography.

Curious to get thoughts…

Thanks for probing further. Here are my views :

Sustainable margins are around 15~16% and last year was an outlier due to cheap R-LNG prices in the spot market. I am more focused on the earning power and sustainability of the same. For the next 3 years, business has plans to fund capex of 1000 Cr. each year while servicing existing debt. After that it should become a free cash flow machine.

On growth front, I am more hopeful on the below scenario in addition to the ones mentioned by you:

Industrial / commercial PNG demand outlook-The National Green Tribunal (NGT) identified ~100 industrial clusters with critical pollution levels that could add to the overall gas consumption basket once the gas infrastructure has been commissioned in the next few years. This appears promising for the sector, considering the stringent norms prescribed by the government in implementing the ban on polluting fuels. For instance, CGD demand significantly increased in Gujarat following the NGT order to ban coal gasifiers in 2019. As a result, gas consumption in the Morbi region increased to 5.1-5.2 MMSCMD in 2019-20 from 2.9-3 MMSCMD in 2017-18. << From ATGL FY 21 AR>>

What may help to hike prices?

- Considering NGT’s objective, customers do not have an option to switch back. Also, quality of products manufactured using gas is better (read somewhere and do not have the source).

- Inflation impacts all types of fuel.

- Convenience to the customer.

- A societal cause with governments focus.

To fulfil demand, 3 sources are available for buying gas:

- Term contracts

- Spot basis purchase

- Domestic gas fields – These are controlled by Government policies. From AR of ATGL - In February 2014, the government announced a domestic gas allotment to meet the entire demand from the CNG and PNG segments. CGDs get the highest priority in domestic gas allocation. Following court orders, the central government facilitated the supply of 100% domestic gas for all gas consumption for CNG/domestic piped gas, which was later increased to 110% allocation - the highest allocation priority over competing fuels. I think that this is the main source of supply for IGL and MGL and hence lower material costs, resulting in better OPM.

On hedging, I do not think GGL does anything. Per FY21 AR on Commodity Price Risk, risk arising on account of fluctuations in price of natural gas is mitigated by ability to pass on the fluctuations in prices to customers over period of time. The company monitors movements in the prices closely on regular basis.

Considering the nature of this business- customer deposits an advance amount, pays the bill at regular interval, agrees to price hike as per market forces and the business owns NIL inventory, I find the above policy reasonable. I checked for one other competitor(ATGL) and even they follow the same policy.

Note: Nothing more to add from my end. Trust you will keep up your enthusiasm and revert with your findings.

Picking up this thread again. Last few months, personal things diverted attention.

Here’s my study so far (source is ARs, google research, users). Would like to be challenged on the thought process and get more insights.

Undoubtedly, CGD business is recurring stable revenue. Biggest risk is spot LNG prices (50% is imported) which was witnessed in Dec 21 qrtr wherein we saw GGL’s OPM fall to 5% vis a vis IGL at 21%. Both have a drop but GGL had sharper one for last 2 qrtrs. In June, it was 24%, Sep fell to 12% and Dec to 5% vs IGL OPM in June was 30%, Sep at 29% and Dec at 21%. This is attributed to raw material cost. Reason being that GGL predominant sales ~ 80% are to industries vs IGL predominant sales ~ 69% is to CNG. Govt has mandated supply of gas at subsidized prices for transport (CNG) and domestic (PNG). Thus, IGL gets raw material at subsidized cost vs GGL and that explains diff. in raw material cost impacting OPM.

Positive side of this is GGL is less prone to EV risk vs IGL or MGL where 70% of revenues comes from CNG business. Speaking to Ford folks, understand that EV adoption in India is much faster than West. COVID has slowed down pace. Having said that, this would still take 5 years (Anyone residing in NCR/Mumbai area, can you please validate adoption of EV in these areas vis a vis CNG).

Another thing to note while reading annual reports of GGL and IGL is -

IGL future outlook -

In Delhi, NCT region industries have moved to gas. Govt in neighboring states like Rajasthan, Punjab, etc is also encouraging similar move. Volumes can grow

inorganic growth thru stake or M&A in other CGDs

50 new EVs charging stations. 2 are completed

New models like HCNG – e.g long route buses from Delhi to Dehradun on CNG. This will spur volume growth as buses move to CNG

Backward integration, move to digital – 35% - better customer experience

Move to hydrogen and bio gas

GGL future outlook -

Focus on CNG (transport) and PNG (domestic)

How much such measure help in the margins needs to be seen

Read a report saying that morbi ceramics have shifted to propane and lpg and will keep doing so.

So is this a temporary setback or a longterm one for Gujarat gas since most of the revenue is from industrial sector for the company