Can you share the report?

2 Likes

Thanx. write up on the same video:

85 lac SCM : total capacity of Morbi

66 lac SCM : consumption right now

20 lac SCM : From Propan

45 lac SCM : From Gujarat Gas

earlier they were using 100% from gujarat gas. Now 25% is coming from Propane.

Currently, gujarat gas is charging Rs. 64 / SCM whereas propane gas is costing Rs.57 / scm. This gap will only increase. So, propane share will increase to 45% in next 3 months.

Big hurdle for Gujarat gas.

Disc: Invested

6 Likes

Started researching about this stock on the recommendation of @santoshj on the mgl thread.

The great cagr is what got me curious to look into this company but deep diving in,I have found there is certain risk one of them being competition from adani gas which is providing same product but cheaper also reading in there annual report they operate in the same region as gujarat gas ,so going forward the company might not get the monopilistic valutions it once did and personally i find that a private player will always take market share from the government operated company due to it being more cost efficient and better managed.

Although cost of natural gas prices has fallen last month but is expected to remain volatile let’s see how it will fair against the competition from methane and adani.

personally i believe Cng is the future specially in cities like delhi and mumbai ,where most people don’t have designated parking spaces to charge there car given the high real estate prices.Moreover a used or new car can be converted into cng easily making the cost of purchase low compared to the cheapest electric car.

Disc :No investments bullish on the sector ,will wait and watch how the next few quarters play out in.

3 Likes

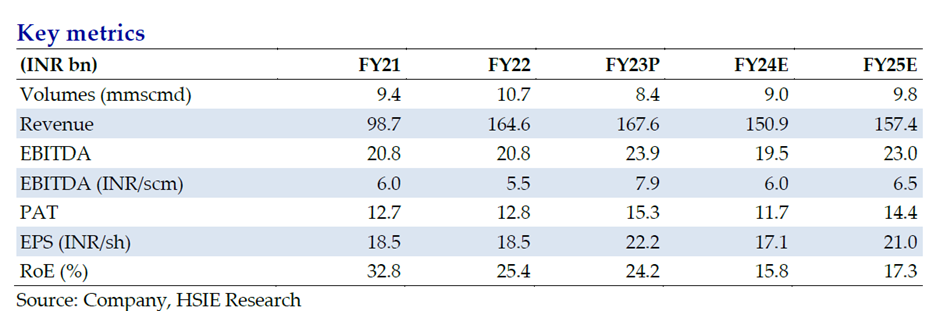

- Volume growth of only 8% is expected over FY24-25. GUJGA’s long-term volume growth prospects remain robust, with the addition of new industrial units, and expansion of existing units.

- Increased pricing competition expected from alternate fuels.

- Q4 saw a higher than expected gas cost due to which margins were affected.

- Low visibility on the spot LNG prices in the medium term.

- Volume recovery in industrial PNG segment. Growth in CNG, domestic PNG to support overall volume growth.

- Better pricing power and regulatory tailwinds over the long term.

- In the near term, price trend/global LNG costs trend will be key monitorable.

- Brokerages recommend buy/add with a target of Rs. 500-600.

- Brokerages recommend an EPS between Rs. 22-24.

1 Like

hi @santoshj do you feel the gap in pricing of LNG and LPG having sustained for such a long period of time; will encourage even more Morbi players to move to LPG/Propane.

Also in the latest development, Aramco y’day cut the Propane prices to lowest since Nov 2020

1 Like

Govt wants to promote both sources of energy, hence making Propane gas price equivalent to Natural Gas. Next they should bring Natural Gas under GST.

2 Likes

| - | Selling price saw a pressure. 84% can be attributed to reduction in selling price and 16% on account of reduction in sales. |

|---|---|

| - | During the quarter, the company reduced industrial selling price to compete with lower alternate fuel mainly propane in the Morbi area which has impacted the profit. |

| - | The company successfully completed a pilot project on hydrogen blending with NTPC. It is planning to increase the hydrogen bending further. |

| - | CNG and domestic PNG now contributes ~35% of the total sales volume (v/s 31% in Q1 FY23) supported by growth in CNG volume. |

| - | With the softening of spot prices and availability of cheaper domestic sources of gas, the company adjusted its selling prices to retain and regain customers at Morbi and other industrial customers. |

| - | The board approved investment of ₹100 crore in GLL). The company is at Mundra in Gujarat having a capacity of 5 It currently sources ~4-4.5 mmscmd of imported R-LNG. After this investment, Gujarat Gas holds of It provides better synergy and integration in the gas value chain. |

| - | Going forward, the company continues to balance between volumes and margin. |

| - | The company plans to incur capital expenditure of ~₹1,000-₹1,200 crore every year for the next 3 years. This would be mainly in new geographical areas, existing geographical areas and CNG infrastructure. The capital expenditure would be funded through internal accruals. |

| - | The CNG sales volumes are expected to grow supported by addition of CNG stations and higher competitiveness to alternate fuels. |

| - | The company would add ~60-70 new CNG stations in FY24. Most of the addition would be in the Ahmedabad rural areas. |

| - | The reduction in APM price coupled with the lower VAT is expected to give strong growth momentum to conversions both in domestic and CNG sector. |

| - | The company anticipates maintaining its EBITDA/scm at ~₹4.5-₹5.5/scm, going ahead. |

| - | It is planning to expand in newly acquired areas in Thane rural areas, Ahmedabad rural areas and some areas in Rajasthan for industrial volumes. |

2 Likes

Two points I need clarity on -

- Use of Propane in Morbi is impacting profit (this can happen in other industrial belts)

- They are increasing CNG stations, however with increase in adoption of EV, how effective / profitable these stations would be.

Disc : Tracking not invested.

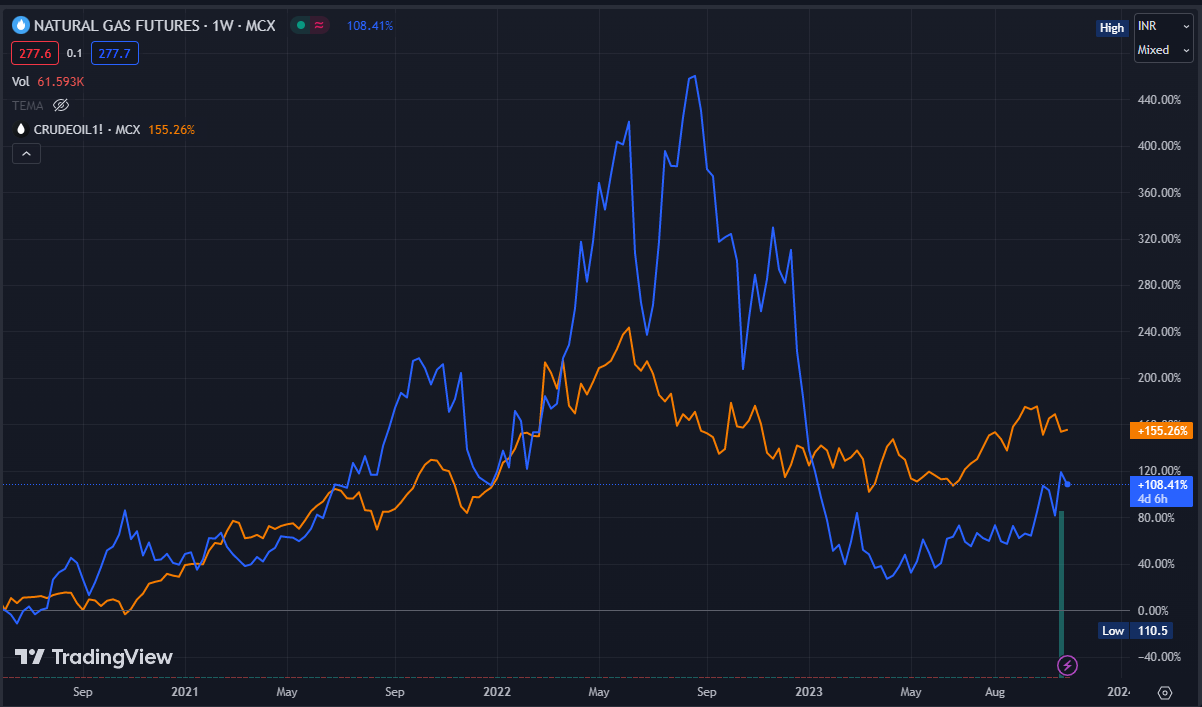

Here is a comparison between Natural Gas and Crude Oil.

In May 2022 Natural Gas prices are greater than crude oil prices that’s the main reason industries are using propane instead of natural gas. But right now natural gas prices are falling. and natural gas is cheaper than propane. A fall in natural gas prices increases the extra margin in Gujarat gas.

2 Likes

-

Industries back of spot prices

-

looking at a few industrial customers in Punjab

-

looking at industrial areas in MP

On point 2, what if Gujarat govt comes up with similar policy as Delhi on EV by 2030. IGL fell 10% because of that.

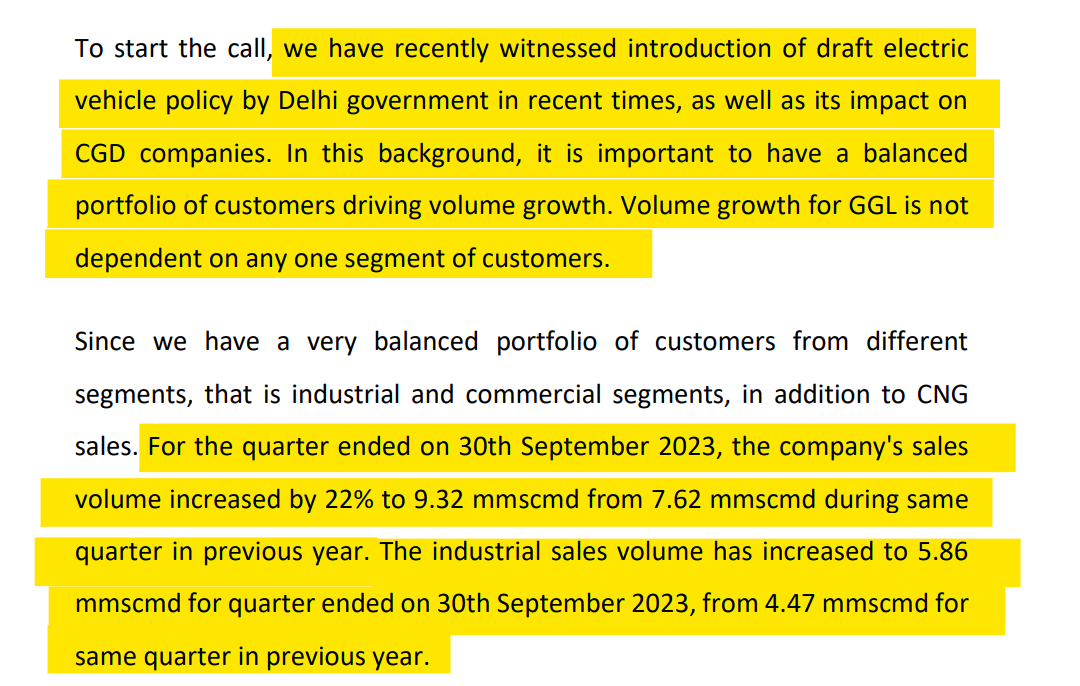

Recent con call GGL’s chief financial officer said that the volume of GGL is not dependent on any one segment. Since GGL has a very balanced portfolio of customers from different segments, that is industrial and commercial segments, in addition to CNG sales.

So maybe it not might affect GGL as compared to IGL

1 Like

Gujarat Gas Limited Q3 FY ’24 Earnings Conference Call February 15, 2024

-

We have achieved highest highest-ever CNG volume of 2.78 MMSCMD in Q3, which is 14% higher than Q3 of the previous financial year.

-

We have introduced smart meters for domestic customers at GIFT City, Gandhinagar.

-

We have set up new CNG stations to promote the use of environment-friendly fuel. We have also achieved the injection of biogas into the GGL system. We have kick-started the operation of taking the supply of biogas into the GGL system at Sanchore, Jalore, and Sirohi.

CNG business:

With better availability of supplies, new CNG model launches, strengthening of CNG infrastructure, and reduction in CNG prices, the CNG penetration is expected to grow from the present 11% in 2023 to 18% in 2027.

CNG will be the second most preferred fuel in the year 2027.

FDODO (Full Dealer-Operated and Dealer-Owned scheme):

This will cover the entire market of the Gujarat gas. If I talk about Gujarat, we have received a major or massive response to this scheme. More than 700 online applications were submitted by enthusiastic potential partners. GGL is planning to operationalize 200 plus CNG stations under this scheme over 2 years.

We are expecting 15% to 20% growth in the present CNG volume on a year-on-year basis. This scheme, FDODO, is dedicated to the entrepreneurial spirit of the country and we are creating a startup opportunity in the energy sector for even small entrepreneurs. FDODO scheme, where it is allows dealers to invest in and operate compressed natural gas stations, this innovative approach empowers local entrepreneurs and fosters economic growth while simultaneously expanding GGL’s city gas distribution network.

We have signed a MoU with HPCL, which will help us in the FDODO scheme implementation with the OMC. We are going for NFR, that is Non-Fuel Revenue, through selling lubricants at our CNG stations also.

-

We may explore liquid business opportunities with OMCs also. We are starting with the HPCL. Sooner we will sign with other OMCs also. This will allow us to have mother stations in remote areas also. And this will, of course, give us a pan-India reach for developing our transportation business.

-

We are also working on developing hydrogen and CBG transportation capability for the company. For that, we have signed a MoU with FEV, which is the Field Evolution Group of Germany. This group is a globally leading engineering provider in the automotive industry and an internationally recognized leader in innovation across different sectors and industries. But this will help us have leverage in developing hydrogen and CBG-based automotive fuel businesses.

-

GGL is working towards achieving operational excellence and customer delight through digital transformation. For that, we have signed an MoU with a Polish company called AIUT Technologies, will help us develop such strength in digital transformation across the business.

3 Likes

Usually, it is not a good sign if the regulator makes noises about your margins and profits. Views of fellow boarders?

2 Likes

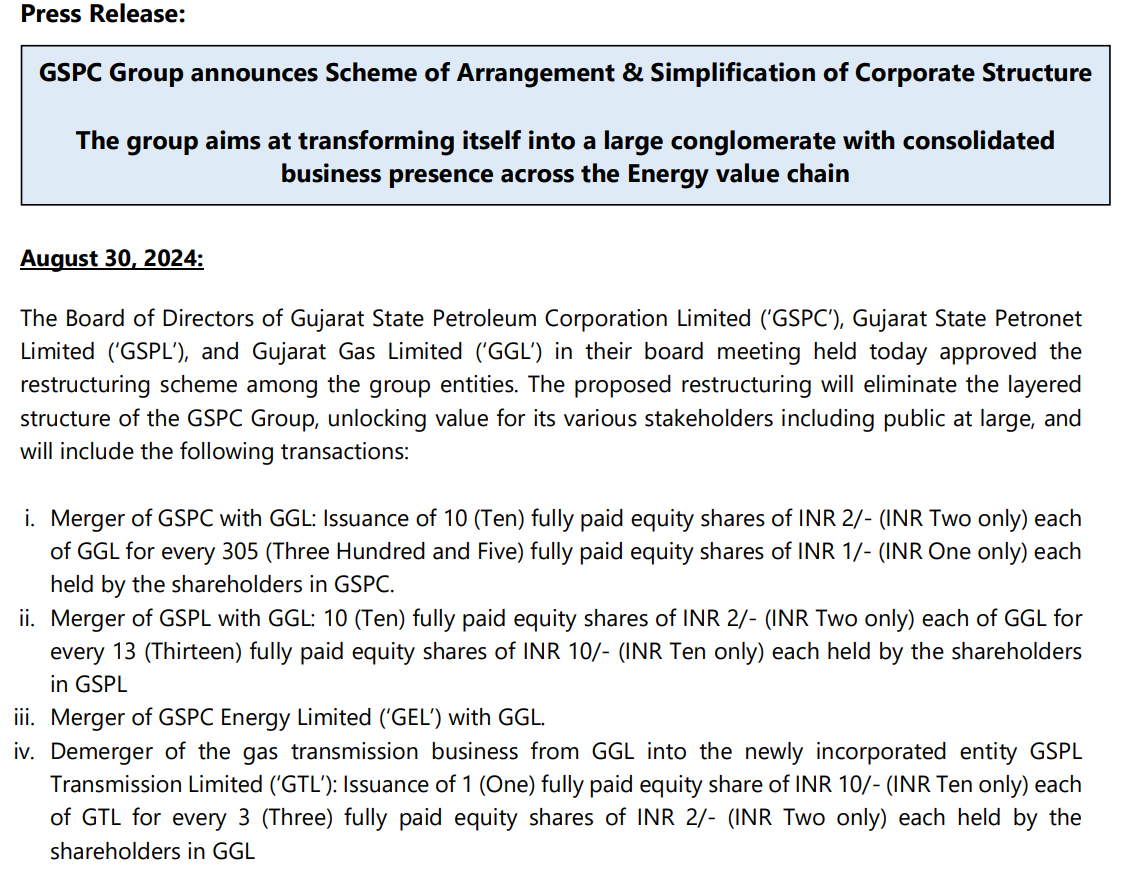

Merger of GSPL with Gujrat Gas Ltd.(GGL)

Shareholders will be allotted 10 shares of GGL for every 13 shares held of GSPL. GSPL owns about 54% stake in GGL. Gujarat State Petroleum Corporation Limited(GSPC) which owns 37% in GSPL will also be merged in GGL.

Transmission business of GSPL will be finally demerged into GSPL Transmission Limited (GTL) which will be subsequently listed on the stock exchange. Shareholders will be given 1 share of GTL for every 3 held in GGL.

Press Release

Scheme of Arrangement

Investor Presentation

Stock of GSPL has already run up 30% in last week, now it is almost priced ideally for the 10 to 13 swap ratio. Assuming GGL at 600 per share, GSPL should be priced at 461 per share, current price of GSPL is 443 per share.

There is a investor call at 3.00 pm on 31st August to discuss this restructuring.

7 Likes

Can anyone tell me the positive and negative impacts of yesterday’s news on the Gujarat gas

Very small impact. I used to hold is earlier but now sold so not tracking much. But ~60% of GGL’s revenue come for morbi where they can’t use APM gas. For that they buy gas from open market. So this announcement of lower APM allocation won’t hurt them much. Also, allocation from APM has been gradually decreasing since last 1 yr. Only this time the fall is drastic (~20%).

However please note morbi is partially shifting to propane gas which is cheaper. This is the reason why GGL share has not performed since last 3 yrs as Morbi shifted ~25% gas requirement to propane. This is also the reason they can’t increase gas price. So there is no supplier’s moat in GGL currently. Which is also the reason GGL shares won’t perform much, unless they increase volume sale in other GAs, which has its own challenge.

4 Likes

The new proposed regulations may fundamentally impact CGD companies if they are implemented. Views invited.

1 Like

Gujarat Gas Limited Q2 FY25 Summary

Key Pointers from the Call

- GGL is the largest city gas distribution company in India, operating in 27 geographical areas across six states and one union territory.

- The company has filed a scheme of arrangement with stock exchanges to eliminate the layered structure of the GSPC group, promote business synergies, and unlock value for stakeholders.

- GGL has been able to grow CNG volumes by 12% year-over-year.

- They have added nine new CNG stations during the quarter, bringing the total to 820 stations.

- The company is planning to increase the blending level of its hydrogen blending pilot project after receiving necessary regulatory approvals.

- GGL is evaluating options to increase CNG prices in the near future to offset the increased cost of gas procurement due to a reduction in APM gas allocations.

- They are seeing positive growth in the domestic segment, with a customer base of over 2.19 million domestic customers.

- GGL is targeting new markets in Ahmedabad rural, Silvassa, and the Daman, Diu and Silvassa markets.

- The company is looking to enter the LNG trucking business and is in the process of surveying routes connected to major ports in Gujarat and expressways coming up in and around Gujarat.

- GGL’s EBITDA margins are expected to be in the range of 5 to 6 rupees going forward.

- The company maintains a focus on expanding geographical coverage, and expanding its gas network to lead to increased volumes and profitability.

Key Financials

| Metric | Q2 FY25 |

|---|---|

| Revenue from Operations (Crores) | 3,949 |

| Profit After Tax (Crores) | 415 |

| EBITDA (Crores) | 553 |

| EBITDA/SCMD (Rupees) | 6.86 |

| Capex (Crores) | 130 for the Qtr |

| Morbi Volume (MMCMD) | 2.86 |

| Non-Morbi Volume (MMCMD) | 2.05 |

| Total Volume (MMCMD) | 8.75 |

Gas Sourcing Details:

- APM Gas: 31%

- Long-term Contracts: 35%

- Spot LNG: 34%

Average price of spot LNG: ₹37.4 per SCM

Future Outlook

- GGL expects the number of customers in the domestic and commercial segments to increase over time as new areas mature.

- The company is hopeful that volumes will recover in Q3 FY25.

- Management believes that expanding geographical coverage and expansion of the gas network will lead to increased volumes and profitability.

- GGL is in discussions for a new LNG contract to replace the volumes from the BG contract that will expire in mid-2025.

- The company is evaluating options for deploying operating cash flow, including diversifying into renewables and hydrogen.

- GGL aims to grow its presence in the industrial segment, targeting the Ahmedabad rural, Silvassa, and the Daman, Diu and Silvassa markets, and expects volumes in these areas to grow substantially in the next few years.

- The rollout of the FDO scheme is expected to ramp up in the coming quarters, with 125 franchisees already having accepted LOIs.

- When replacing expiring contracts, GGL will prioritize oil-linked contracts but will also include some Henry Hub exposure.

- Overall volume growth guidance for FY25 remains at 5-7%.

Challenges

- Reduction in APM Gas Allocation: GGL has seen a significant reduction in APM gas allocation, which is being replaced by higher-priced new well gas and spot LNG. This will impact margins in the coming quarters.

- Competition from Propane: GGL faces competition from propane in the industrial segment, especially in the Morbi region. The company is working to convert propane users to natural gas, but price fluctuations in propane can make this challenging.

- Maintaining Volume Growth: While GGL has a positive outlook for volume growth, achieving its target of 5-7% growth will depend on factors such as the pace of infrastructure development, competition from alternative fuels, and economic conditions.

- Passing on Increased Gas Costs: The recent reduction in APM gas allocation and the increase in spot LNG prices will require GGL to pass on these costs to customers. The company will need to carefully balance price increases with maintaining its competitiveness against alternative fuels.

- Exposure to GSPC: The proposed merger with GSPC creates indirect exposure to GSPC’s performance until the merger is finalized. While GSPC is not a listed entity, its performance will be closely watched by investors and analysts.

1 Like