About the Company

GGL is India’s largest City Gas Distribution company, with 25 CGD licenses spread across 41 districts in 6 states and 1 Union territory across the states of Gujarat, Maharashtra, Rajasthan, Haryana, Punjab and Madhya Pradesh and Union Territory of Dadra & Nagar Haveli.

Holding Disclosure:

Together with GSPL, the parent company, total 10% of my portfolio since past 2 months. Have been adding since PE has been falling even as performance remains good/improving. As seen from screener.in, PE is at historical lows, while performance and outlook is the best ever.

Preamble:

Discovered this after having invested in Gas space about 3 years ago when first starting my investment journey. First picks were Petronet LNG, GAIL, Mahanagar and Indraprastha Gas. Exited most of them after some disappointment by the modest gains within a year. 2017-18 were turbulent times to judge value!

Mostly the bet was pre-mature and in case of Petronet LNG I could foresee that it would be a laggard in the terminals business. Was shocked by Indraprastha gas re-rating and hence re-entered.

Objective is to create a thread for collecting/sharing ideas/opinions/information. The ValuePickr way!

Disclaimer:

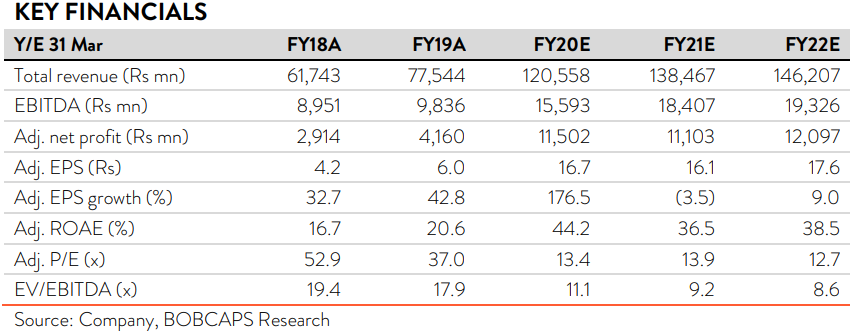

Most of this article is credited to this report of BOB capital markets published a week ago:

The analysts write:

At our recent meeting, GUJGA’s management assured robust outlook on volumes driven by (a) implementation of anti-pollution measures by the state government (new CNG state buses), and (b) relatively low LNG prices.

Volumes continue to trend above 9 mmscmd, as Morbi units sustain >6 mmscmd offtake, and carry additional 1-2 mmscmd potential. We raise GUJGA’s TP to Rs280 (from Rs270), as we roll forward valuation to Mar’21.

At 12.7x FY22 EPS, GUJGA remains most attractively value among its peers.

Buoyant volume outlook:

Ceramic units in Morbi (Gujarat) continue to offtake >6 mmscmd volumes, and carry potential for another 1-2 mmscmd as new units get connected. Concerns on Morbi customers shifting to GAIL for sourcing gas seems to have alleviated, as GUJGA’s pricing remains most attractive, along with its commitment to add incremental pipeline capacity to connect more units. CNG volume growth could improve as Gujarat state transportation (GSRTC) has approved induction of 1000 CNG buses (250 in Q4 FY20). Over the long-term, management expects most of the GSRTC’s ~7000 fleet of buses to convert to CNG.

Volume potential from new areas to fructify from FY21/22:

GUJGA is aggressively pursuing expansion into newer areas, maintaining capex guidance of Rs6-7bn annually. Initial strategy is to tap potential from existing network from Rajasthan until rural Thane region near Mumbai. Simultaneously, this would help tapping volumes from new areas such as Dahej, Punjab (GUJGA has license for about 6 areas) and Rajasthan, that offer 4-5 mmscmd potential.

Undemanding valuations:

At 12.7x FY22E EPS, GUJGA’s valuations remain relatively attractive to CGD peers (~16x for IGL/MAHGL). This gap may get bridged gradually, given stability in volumes and margins.

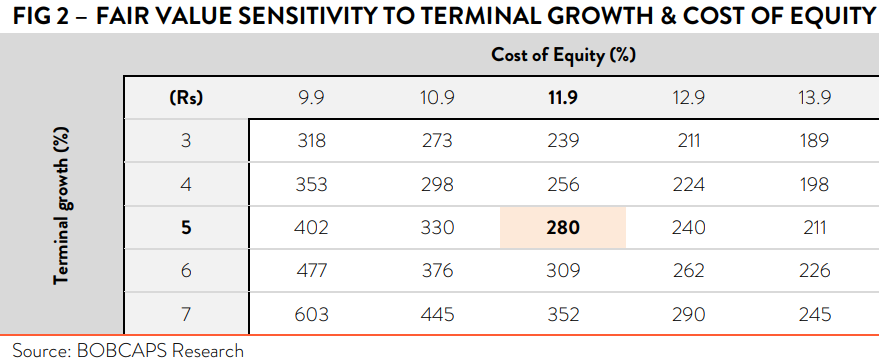

Valuation methodology

GUJGA’s unique positioning in the CGD space makes it one of the best bets on gas volume growth potential, based on a) access to more than 80% of CGD potential in Gujarat, and b) strategic expansion into new areas (such as Dahej in Gujarat, Rajasthan, western Maharashtra and Punjab) that are contiguous to its parent GUJS’ pipeline networks.

At 12.7x FY22E EPS, GUJGA’s valuations remain one of the lowest among CGD peers (13x-17x for MAHGL/IGL). This gap may get bridged gradually, as volumes and margins sustain as elevated levels. We raise GUJGA’s TP to Rs280 (from Rs270), as we roll forward DCF valuation to Mar’21.

Key assumptions for our DCF-based fair value are as under:

Cost of equity of 11.9% (from 11.4% earlier) and terminal growth of 5%

Long-term average EBITDA margins at Rs5/scm

Key risks

Lower-than-expected margins over FY21-FY22 could change our valuation outlook for GUJGA

Below-expected volume growth.

Change in the PNGRB regulations, or an unfavorable court ruling (against NGT ruling for ceramic units), could alter volume growth outlook.

Note:

GSPL owns 55% of Gujarat Gas. Gujarat govt owns 5% and only 25% is free-float for public.

Apparently there is an old “special situations” thread about an open-offer in 2012 when GSPL wanted to fully acquire this

My investment thesis:

As mentioned above it did seem that the Gas space would see increased activity, since few years ago, amid pollution and cost concerns where Gas has advantage and the Govt making lots of noises and big long term deals for Gas. Most of the CGD (City Gas Distribution) players have been giving good numbers, though only IGL has been loved by the markets.

Among all CGD plays, I chose to pick only Gujarat Gas (+ GSPL, in 70:30 allocation ratio). After browsing through CGD companies on ValuePickr, there was realization that they were bidding aggressively and winning CGD rights over others. So they were trying to grow but no certain profitable growth. “Gujarat” brand name helped since they were backed by the state-entity GSPL. Apparently GujGas is the retail and CGD arm while GSPL is the infrastructure arm. LNG terminals are mostly on west-coast and lots in the Gujarat area.

Along with robust numbers it appeared that PE was exceptionally de-rated which gave considerable up-side and low-risk. GSPL apparently has been a bit of a bad-boy and has not completed the pipeline to Punjab, now with a delay of 1-2 years, but they are now targeting completion within a year, apparently GAIL has been given orders to link their gas-generating fields and pipeline to this trunk pipeline of GSPL. I bet it also helps that Gujaratis are in the right places, right now.

Rating upgrade from CRISIL covers several points of interest: (2 weeks old)

Detailed Rationale

CRISIL has upgraded its rating on the long-term bank facilities of Gujarat Gas Limited (GGL) to ’ CRISIL AA+/Stable ’ from ‘CRISIL AA/Positive’.

The upgrade reflects CRISIL’s expectations of an improvement in GGL’s credit profile over the medium term. Sustainable improvement in cash accruals is expected to improve GGL’s financial risk profile notwithstanding the sizeable capital expenditure (capex) programme.

GGL has reported a healthy growth in operating profit led by higher gas sales volumes and benign cost of re-gasified liquefied natural gas (R-LNG), in the first half of fiscal 2020. The volume growth was mainly driven by higher gas sales in the Morbi industrial area. In March 2019, the National Green Tribunal (NGT)'s order of banning the use of coal gasifiers in Morbi (Gujarat) region led to migration of industrial customers, mainly ceramic tile manufacturers, to piped natural gas from coal. Commercialisation of new geographical areas (GAs) will further support the volume growth.

GGL has annual capex plan of Rs 700-800 crore, to be largely funded through internal accruals. GGL has received the authorisation to set up city gas distribution (CGD) network in 7 new GAs won under the Round 9 and Round 10 bid conducted by the Petroleum and Natural Gas Regulatory Board (PNGRB). Further, it plans to expand the network within existing GAs as well. The project risk on account of sizeable capex and newer geographies is partially mitigated by GGL’s long standing experience in CGD business.

The rating continues to reflect the company’s sizeable scale of operations as the largest CGD entity in India, its healthy financial risk profile and stable profitability levels. These strengths are partially offset by its exposure to volatility in R-LNG and domestic natural gas prices and exposure to regulatory risks.

Analytical Approach

CRISIL has combined the business and financial risk profiles of GGL and its subsidiaries/associates to arrive at the ratings.

Please refer Annexure - List of entities consolidated, for details of the entities considered and their analytical treatment for consolidation.

Key Rating Drivers & Detailed Description Strengths

*** Largest CGD player in India with diversified customer profile**

GGL’s strong and established market position in the CGD industry in India is indicated by its industry-leading presence in 23 districts spread across Gujarat, Dadra and Nagar Haveli, and Maharashtra. Further, the Company has also won bids during the 9th and 10th CGD bidding round to set up CGD networks in 7 new GAs in the states of Gujarat, Rajasthan, Haryana, Punjab and Madhya Pradesh. New GAs should help attain geographical diversification while expanding the scale of operations. The company’s user base comprised around 14 lakh domestic households, 3626 industrial units, 12,397 commercial establishments and 347 CNG stations, as on September 30, 2019, thus providing strong revenue diversity.

*** Sustained improvement in operating performance, driven by rise in gas volumes sold and stable realisations**

GGL is the largest CGD player in India, with strong and established market share. The company has been able to sustain improvement in its operating performance, despite volatility in RLNG and domestic gas prices. The domestic gas prices rose 19% during fiscal 2019, while the spot RLNG increased by 10%. Despite this hike, the company was able to pass on the increased cost to its customers, and maintain a healthy gross profit per standard cubic metre (scm).

Operating performance during first half of fiscal 2020 further improved, contributed by rise in the gas volumes sold and improved margin levels. Gas volumes sold grew by 43% to 9.3 mmscmd (from 6.5 mmscmd in fiscal 2019). Significant growth in volumes was mainly contributed by sales recognised in the Morbi industrial area, wherein the NGT has banned the usage of coal gasifiers. CRISIL expects such volumes to sustain going forward. Operating margins improved to 17% during first half of fiscal 2020 (from average 13% earned in the past) mainly due to decline in the spot LNG prices. The sourcing mix had tilted towards the cheaper spot LNG to meet the incremental demand of industrial customers. CRISIL however expects the margins to normalise to 12% - 14% going forward, with revival expected in the spot LNG prices.

*** Healthy financial risk profile**

GGL’s financial risk profile is driven by healthy cash accruals, comfortable debt protection metrics, and adequate liquidity. Cash accruals increased to Rs 640 crore during fiscal 2019 from Rs 515 crore in fiscal 2018. The company also reported healthy cash accruals of Rs 627 crore during first half of fiscal 2020. Gearing improved to 0.86 times as on September 30, 2019 as compared to 1.18 times as on March 31, 2019 and 1.49 times as on March 31, 2018. The annual cash accruals generated is expected to be sufficient to fund the capex plans of the company over the medium term, and accordingly the Debt/EBITDA position is not expected to exceed 2.5 times.

Weakness

*** Exposure to regulatory risks**

Regulation of natural gas, including CGD, is still in the initial stage in India and hence there is considerable uncertainty regarding the regulatory norms for natural gas allocation and distribution. Though the uncertainty in regulation is expected to subside as the industry attains maturity, any unexpected change in regulations regarding allocation of natural gas and pricing of end-product can adversely impact CGD players like GGL.

*** Exposure to competition from alternate sources**

Post the end of the marketing exclusivity period for the allotted GAs, the company remains exposed to competition that could set in from the other CGD players. ~70% of GGL’s volume mix accrues from the industrial/commercial segment, which is generally price sensitive to the pricing of alternate fuels. However, GGL has demonstrated a healthy track record of supplying gas in the allotted GAs, wherein it has been able to maintain its customer base and margin levels, despite competition setting in from alternate fuels.

Liquidity Strong

Liquidity is strong with cash and bank balance of Rs 478 crore as on September 30, 2019 as compared to Rs 289 crore as on March 31, 2019. Net cash accrual, healthy at Rs 640 crore during fiscal 2019, has further improved to Rs 627 crore during first half of fiscal 2020. Annual cash accruals generated is expected to be sufficient to service the debt repayments due of Rs 164 crore in fiscal 2021. Expected annual capex of Rs 700-800 crore is expected to be mainly met through internal accruals. Liquidity is further supported by largely unutilised working capital bank lines.

Outlook: Stable

CRISIL believes GGL will continue to depict a steady growth in operating performance, backed by healthy volume growth and stable realisation levels.

Rating Sensitivity factors Upward Factor

*Improvement in the financial risk profile, with a net debt/EBITDA below 1 time

*Reduction in project risk with early commercialization of newly won GAs.

Downward Factor

*Material impact on operating performance on account of significant delays in project execution

*Large debt-funded capex or acquisitions, leading to net debt/EBITDA position exceeding 2.5 times.

About the Company

GGL is India’s largest City Gas Distribution company, with 25 CGD licenses spread across 41 districts in 6 states and 1 Union territory across the states of Gujarat, Maharashtra, Rajasthan, Haryana, Punjab and Madhya Pradesh and Union Territory of Dadra & Nagar Haveli.

The draft policy suggests setting up of a committee, under the chairmanship of the chief secretary, which will help formulate policies and streamline the processes for various permissions to develop the CGD infrastructure.

It will cause setting up of a suitable single-window clearance mechanism for the same in the state for the promotion development of CGD infrastructure and ease of doing business.

With a view to promote clean and green fuel, the draft policy is looking to make CNG/LNG as the preferred fuel in public transportation. “State transport corporations will accord priority to CNG/LNG buses, while purchasing new buses and retrofitting in present alternate fuel fleet (which is viable), in order to actively promote the usage of CNG/LNG in the public transport," the document says.

In order to provide user-friendly clean and green fuel CNG and PNG to the general public at affordable and reasonable rates, VAT rates may be reviewed and rationalized with a ceiling of 5%, the document said.

Further, to promote the safe usage of CNG/LNG in the transport sector, state policy thrust may be given by rationalizing road tax for factory-fitted CNG/LNG vehicles and making them at par with electric vehicles

1st stage from E Godavari to Urea plant at Ramagundam operational, start of 2MMSCMD offtake by March.

NO further construction planned since deemed unviable, at present.

Mahesana-Bhatinda-Srinagar target is by end of FY21.

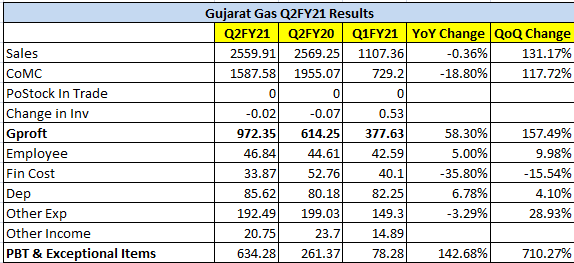

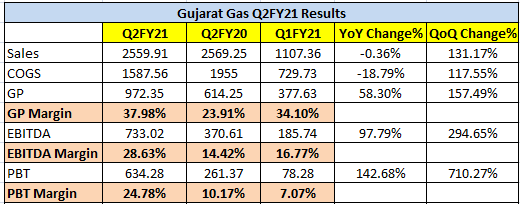

Q3 results seems are perfectly in line with trend/expectations.

YoY PBT up 30%, PAT up 40%.

QoQ PBT is up 1%, PAT is down 62%. Tax rate difference essentially here.

Parent GSPL also does decent in Q3.

YoY PAT up 32%, PBT up 22%.

QoQ PAT down 55% PBT down 8%. Tax rate difference essentially here.

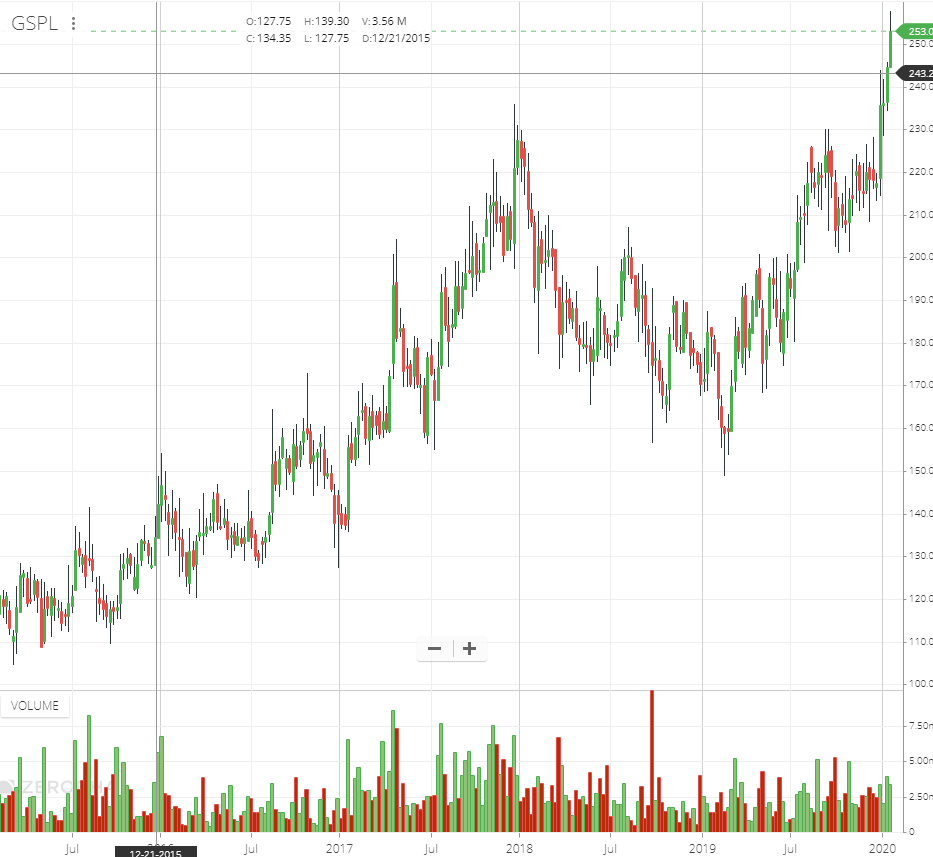

Stock is down to its 50 day MA.

My conviction in GujGas was somewhat due to the price action, while personal preference is for GSPL which is entirely open access already. I have them now in 55:45 ratio, preferring GSPL.

Open-access was tried earlier by PNGRB but failed. Do not see why it might succeed if tried again.

Anyway most analysts have factored in 10% downside already for the risk as per this article.

I see this as possible but at least 4-5 years away, when GAs are saturated.

Though the largest CDG player, their realization density per km of pipeline doesnot look attractive as they mostly operate in non Metros. even the new GA’s they won also seem similar areas

Stock has already runup from Nov’19 due to talwind in GAS commodity due to low input prices and favorable Govt regulation to increase Gas share from 6% to 20% in Indian energy mix by 2025

Not being in GST ambit is a disincentive for Industrial/Commercial players when compared with Fossil fuels

Customer concentration risk - 1) Morbi Ceramic industry 2) Gujarat Industrial area

State concentration (Guj) and related political exposure risk possibly in long run if BJP is out of favour for policy intervention wrt to Guj Industrial area

CNG expansion plans with heavy capex. EV phase will be a risk for CNG plans in long run

I myself exited this, primarily to consolidate total number of holdings below 10 mark. GSPL earnings look better than Gujarat Gas, but CGD is more attractive to markets.

True, that has always been the case, industry and power focus will have growth, next few quarters.

Yes, run up to full value, almost. Fuel is low and will remain low.

Some change is expected here.

Yes, currently quite concentrated but IGL, MGL are diverse?

Heavy capex biz definitely, that is one downside but EV will not be big till few years more.

Disc: exited both Gujarat Gas and GSPL after big run up and also in order to consolidate portfolio. GSPL is a sleepy stock even booming results only nudge it a bit.

Seems the industrial volumes have been increasing quite well after the govt banned coal gasifiers in Morbi industrial area. I was trying to understand if this will be a mere volume growth or will permanently improve the company’s quality and its financial ratios like margins / ROCEs. Have been looking at MGL’s conference calls and noted some points.

Sourcing cost of gas is expensive for Industrial and Commercial purposes:

Benefits like 110% allocation of domestically produced gas to CGD sector is limited to only CNG and Domestic PNG customers. To supply gas to Industrial and Commercial customers, the CGD companies have to import gas and pay higher cost.

Domestically produced gas typically costs $3-4 per MMBTU while Imported gas costs $6-7 per MMBTU. So the average sourcing cost of GGL is and will remain higher compared to its peers. Their new GAs are apparently more retail-focused compared to industrial focused, but it will take couple of years for their share to dominate in total topline.

Alternate Fuel Availability:

As per MGL management, their pricing for Industrial customers always depends on liquid fuel alternatives and their price tracks the prices of those fuels and they have no pricing power. Alternate fuels suggested by MGL management include LSHS, LPG, LDO, FO. Also some googling suggests that Propane is another alternative available to them.

Based on news articles with respect to Morbi, the Govt has banned coal gasifiers but not sure if it includes above mentioned fuels.

Gas Exchange:

India has lots of prices for Natural Gas (APM / PMT for examples) and this is apparently causing a lot of inefficiencies in the Gas markets. So the govt is planning to come up with a gas exchange where the price realization is market-driven and everyone can get gas at the same price. As India’s gas domestic production and imports are in the ratio of 1:1, the realized price could be about $5 per MMBTU. This will increase the sourcing cost for CNG focussed players like IGL / MGL and decrease for Industrial focussed players like GGL.

However, MGL management has simply shrugged it off saying this is against the vision of allocating 110% gas to CGD companies. They also said that a similar exchange was setup for Power and it had no real impact (Experts on Power industry can help comment please).

New Regulations:

There was a question or two about new PNGRB regulations coming up related to pricing. Those are still being formulated and have no idea when they will be out. I think this is more of a follow-up of the PNGRB losing its case with IGL in Hon’ble Supreme Court of India. So they might be looking to come up with more reasonable restrictions on pricing power of CGD companies. In the old case, they were ruthless on their restrictions and hence lost the case. Regulations may be more focussed on CNG / Domestic PNG as they are the ones who are enjoying higher pricing power.

With above factors, it will be interesting to see if the stock would be re-rated to higher levels by the market. GGL is trading at 17 PE while IGL is trading at 30 PE which has most of its revenues from CNG segment.

Just started analyzing Gujarat State Petronet as it looks attractive valuation-wise.

While studying Annual report of the same, had a basic question :- The report mentions Consolidated revenue break-up as : -

Revenue from gas transportation

Sale of products

Can someone explain what is this sale of products here ? If its revenue from Natural gas, then what is the difference between Gas transportation revenue and this other product

Gas transportation revenue is revenue generated by letting others use their gas infrastructure to transport and transmit gas. Sale of products is sales generated by selling gas products B2B and B2C.

GSPL is a parent company of GGL. GSPL is involved in multiple businesses providing gas Transmission network by pipelines, fleet of trucks etc. GGL is basically selling gas B2B and B2C while supporting the infrastructure required for their business operation (Gas stations, pipelines to housholds).

The basic difference between GSPL and IGL, MGL is that GSPL’s revenue tilt more towards B2B and IGL, MGL is more pure B2C play. So IGL, MGL are given higher multiple than GSPL by the market.

That’s not all. The main difference is Gujarat Gas, IGL, etc. sell gas and bear the gas price risk. GSPL is a pure transporter and does not bear gas price risk.

Thanks all for your inputs. Based on what you guys mentioned and the valuations - GSPL then seems to be a value pick right now.

The only difference I see between them and others is that they’ve taken on a reasonable level of debt from GSFC to fund their expansion plans. This seems to be a smart move but can backfire due to execution risk.

Was researching the company, just want to highlight that while on paper it may look like Gujarat Gas bears natural gas price risk, they have been able to pass on the increase price quite easily to their customers in such scenarios. On the contrary whenever spot price falls, GG is not so quick to reduce prices. That’s one of the reasons why PAT increased this quarter as LNG prices were low but GG didn’t pass on the savings to their customers.