Disclosure: Invested and Biased. No transaction in last 30 days. Not an IA or RA. Please do not use this as an investment advice due to the below reasons: * I might be wrong in my understanding of the business** You may not know if I changed my mind*** Resources around you will help to build the conviction, which is the most important thing for direct equity investing. ****Return expectations from this position suit my risk profile, which is unique for each individual.

Warning!!!: Long post.

Request!!!:Trust you will critically read and comment to disprove my hypothesis.

Sources: ARs and quarterly results of Gujarat Gas Ltd. ARs of other players in Gas business- Gujarat State Petronet Ltd, Adani Total Gas Ltd, Mahanagar Gas Ltd, Petronet LNG Ltd.

Objective: To judge whether GGL is an ideal business- Recurring revenue, Generates high FCF, ROIC > 20%, Low Capex, Ability to scale and High Margin or High Asset Turns or not with a long runway?

How does the business operate?

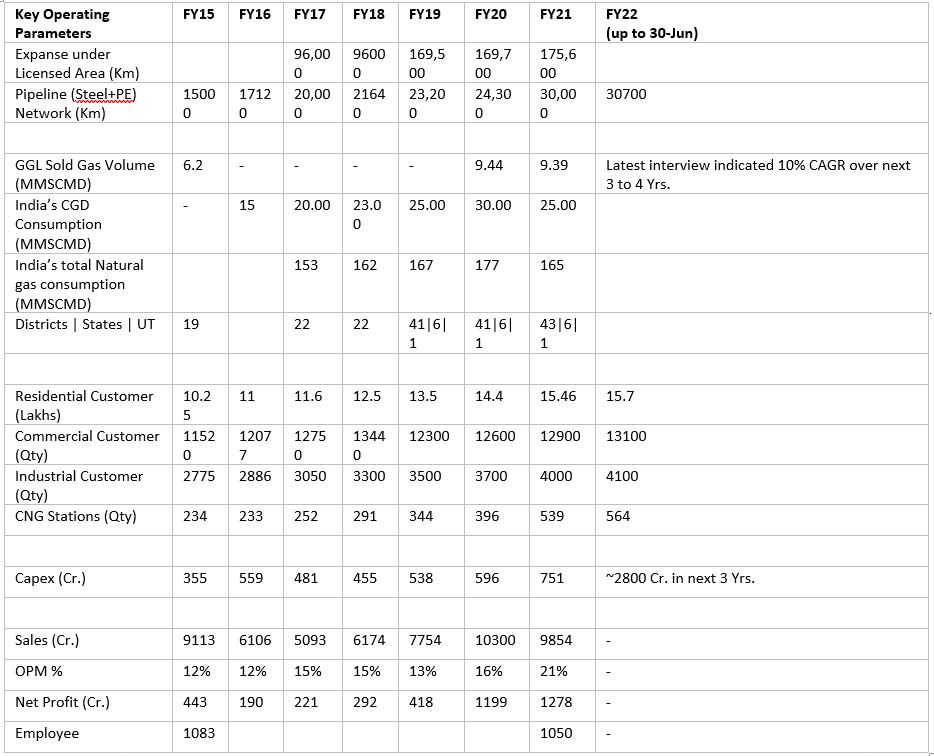

The Company is engaged in Natural Gas Business in India. Natural gas business involves distribution of gas from sources of supply to centres of demand and to the end customers. In the energy value chain, the business operates downstream as a retail demand aggregator and supplier for natural gas. As of 30-Jun-2021, it serves its customers – households (15.7 lakh), its own CNG stations (564), commercial places (13100) and industries (4100) using owned distribution network pipeline of 30,000 Kms and a transmission pipeline of 73 Kms (HAPi pipeline).

How does the business make money?

Revenue comes from monthly/bimonthly billing to the customer for the metered gas consumption. For the sales at gas stations, cash is deposited in the company’s account on the next working day by the operator. Major expenses include gas purchase charges, gas transmission charges, employee salaries, other expenses, interest costs, depreciation charges & taxes.

Business Evolution :

- 1991 - Commenced natural gas supply operations as GGCL (Gujarat Gas Company Limited) in Ankleshwar, Gujarat. Promoter – Mafatlal Industries Ltd.

- 1992 - Commissioned 1st CNG station

- 1997 - British Gas (BG) acquired a majority stake (~65%) through BG Asia Pacific Holding Pte Ltd.

- 2012 - BG, while rationalizing it’s worldwide operations, sold the company to GSPC ( Energy conglomerate, owned by the Gujarat Government, that has presence in upstream, midstream and downstream segments of the energy value chain) at a valuation of ~3800 Cr.

- 2015 - Amalgamation of GSPC Gas Company Limited, Gujarat Gas Company Limited. Post amalgamation, company was named as Gujarat Gas Limited and emerged as India’s largest City Gas Distribution Company.

- 2016 - Won the Geographical Areas of Thane including the District of Palghar and the Geographical Area of Union Territory of Dadra and Nagar Haveli.

- 2017 - Won 6 new geographical areas in the State of Gujarat. Total 18 CGD licenses spread across 22 districts

- 2018 - GGL grew its natural gas supply by over 17% in the industrial segment replacing carbon emitting fuels like coal, Furnace Oil, etc. GSPL bought an additional 28.40% stake in Gujarat Gas Ltd., thereby raising its holding to about 54.17% and making Gujarat Gas Ltd. a Subsidiary Company.

- 2019 - Won 7 new Geographical Areas in the 9th and 10th CGD Bid Round to expand its network in the state of Rajasthan, Punjab, Haryana and Madhya Pradesh, making the Company a pan India company. Total 25 CGD licenses spread across 41 districts

- 2020 - Steep volume growth in industrial customers of around 63% compared to previous year. The volume increase was mainly on account of ban on usage of Coal Gasifiers in the Morbi industrial cluster (which is considered as Ceramic Hub of India) resulting in switchover to natural gas. CGD Business of Amritsar and Bhatinda GAs from GSPL are transferred to the Company

// Gujarat government via various entities holds ~75%. GSPL (Gujarat State Petronet Limited) Ltd holds majority of the stake (~54%).

Customer Base:

- Households, CNG stations, commercial (such as hotels) and industrial entities in the city’s vicinity

- Diversified

- Provided with an essential, cheaper, uninterrupted and environmental friendly source of energy (natural gas as PNG, CNG, or r-LNG )

Sustainable competitive advantage and it’ source:

- The business has 27 CGD licenses that cover 43 districts spread across 6 states and 1 Union territory from industry regulator - Petroleum and Natural Gas Regulatory Board (PNGRB). These licenses have gas marketing exclusivity of 5 (old ones) or 8 (latest ones) years and network exclusivity of 25 years. Post end of marketing exclusivity, CGD entity will have to provide access to its network capacity to third parties desirous of gas marketing in its Geographic Area. The above provides 1st movers advantage and results in a low probability of gas-on-gas alternative in the area of operation. Any new competition in the Geographic Area will have to pay an additional transportation tariff for using the company’s distribution network, increasing gas price for the competitor.

- 30 Yrs. of experience in operating CGD (city gas distribution) in Gujarat and now expanding to other parts of India.

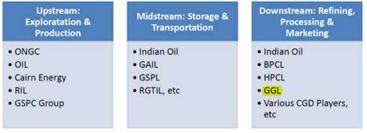

- Support from parent entities that operate in upstream (Exploration and Production- GSPC ensures gas availability) and Midstream (Transmission Pipeline – GSPL ensures transmission pipeline and storage capacity) ensures a robust supply chain. Value chain for petroleum and natural gas and key players is as below:

Ability to raise prices without losing customers:

Natural gas is cost effective compared to alternative fuel and CGD customers have capacity to absorb the price hike. Few additional factors that works in favour of natural gas are -

- Reduced maintenance cost: CNG does not contain lead, so spark plug life is extended because there is no fouling. CNG does not dilute or contaminate crankcase oil, so intervals between oil changes and tune-ups are extended. Pipes and mufflers last longer because CNG does not react with metals, which reduces maintenance costs while extending overall engine life.

- Performance advantages: CNG is superior to petroleum based products because natural gas has a high octane rating compared to alternative fuels. CNG vehicles experience less knocking and no vapor locking, since natural gas is already in a gaseous state. CNG vehicles enjoy superior starting even under severe cold or hot weather conditions

CGD Industry’s evolution:

The Petroleum and Natural Gas Regulatory Board (PNGRB) constituted in 2007, regulates midstream and downstream activities in the petroleum and natural gas sector. It protects the interests of consumers and entities engaged in the specified activities and ensures uninterrupted and adequate supply of petroleum, petroleum products and natural gas in all parts of the country to promote competitive markets.

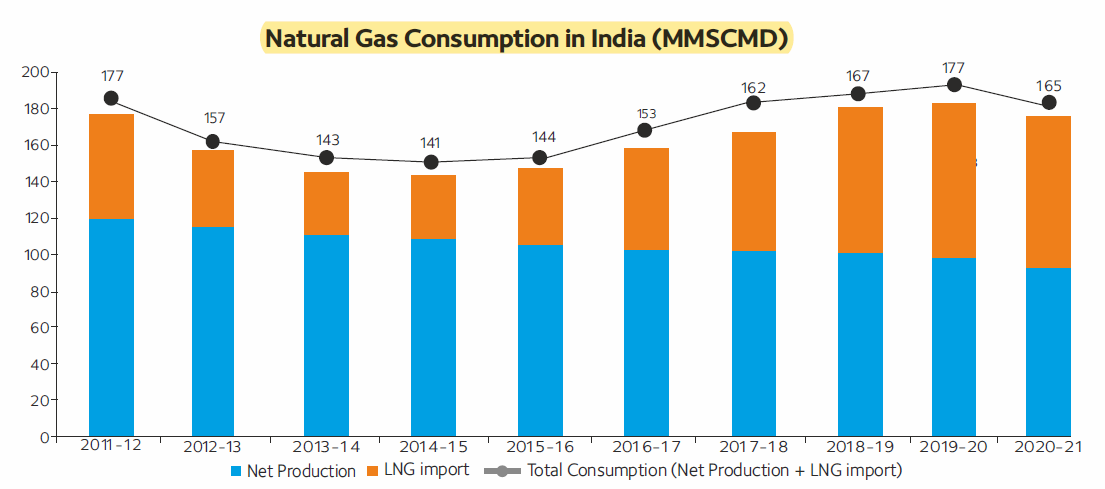

India plans to increase the share of natural gas from current 6.3% (while the world average is 24% currently) to 15% in India’s Energy basket by year 2030. This would require a fourfold increase in gas consumption to over 600 MMSCMD by year 2030 from present consumption of around 155 MMSCMD. With a goal of increasing the share of natural gas to 15% by 2030, the Government of India (GoI) has put strong emphasis on (i) development of additional pipeline network as a part of integrated National Gas Grid (ii) expansion of City Gas Distribution (CGD) network coverage (iii) development of new /expansion of LNG terminals across the Country.

India is investing significantly in expanding its infrastructure for natural gas, which had previously been almost exclusively configured for coal and oil. Indian energy use is dominated by coal, which accounts for 58% of India’s total energy consumption. This is followed by oil at 28%. India’s natural gas demand is forecasted to grow at about 6% annually over the next five years, due to increases in domestic production and falling LNG import prices, growth in pipeline infrastructure and proliferation of City Gas Networks.

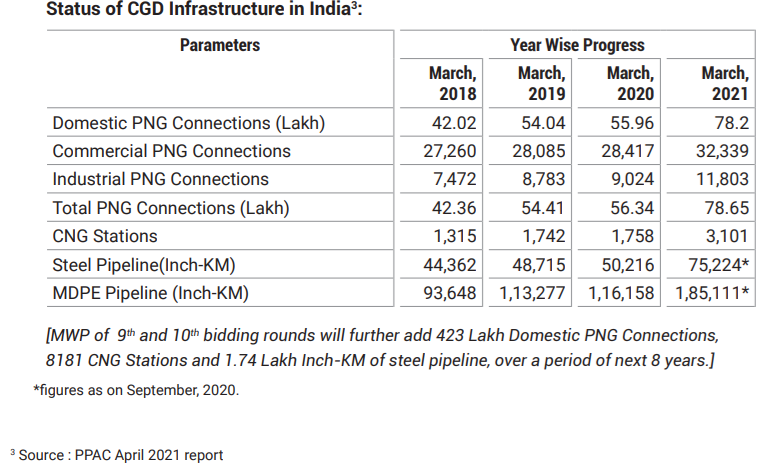

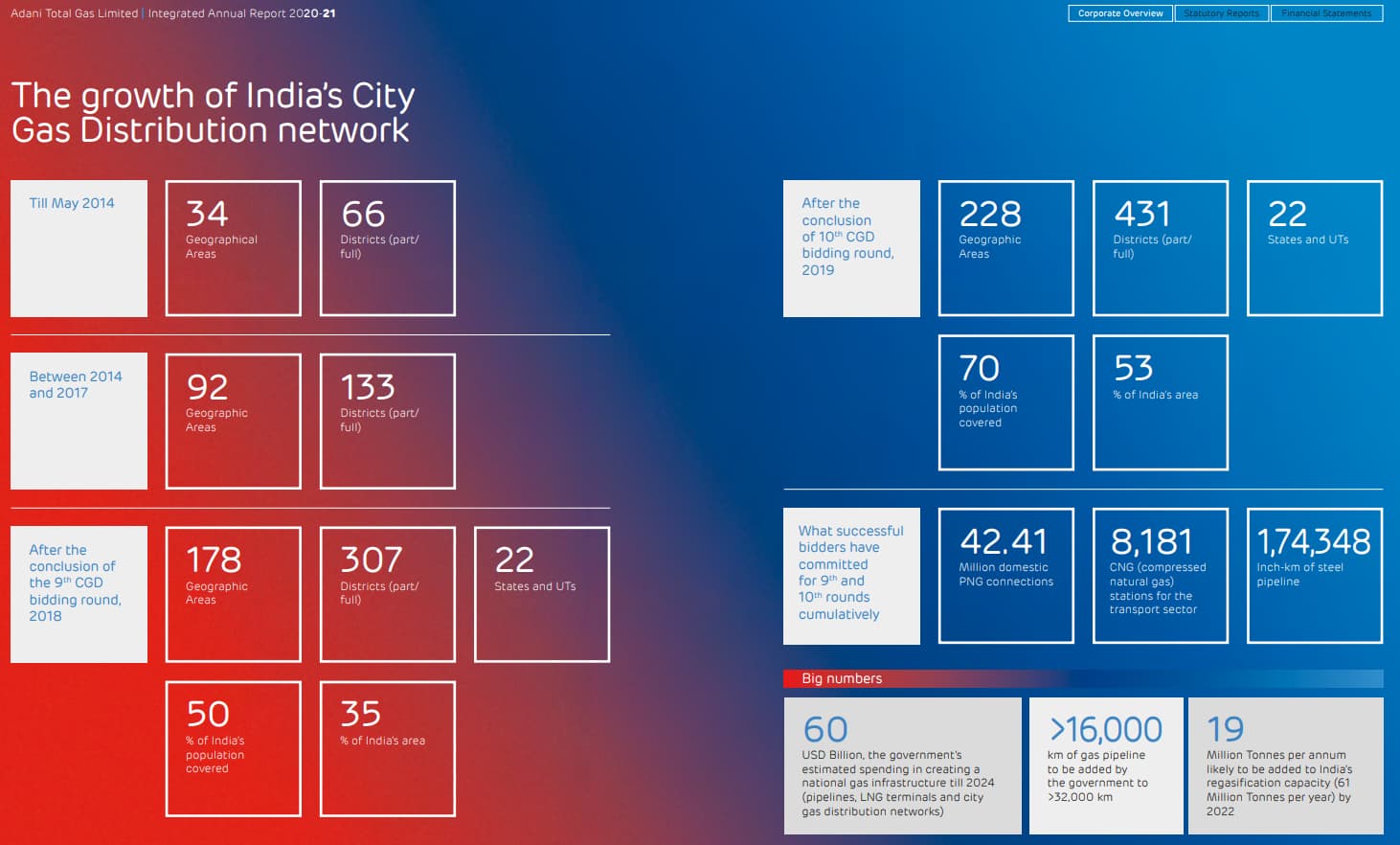

In 2014, only 66 districts were covered by the CGD network. With the completion of 9th & 10th rounds in 2018, the potential coverage of the CGD network would expand to about 70% of the population spread over 400+ districts in 27 States/Union Territories (UTs) and more than 53% of the country’s area. Currently the CGD network caters to about 76 lacs domestic household connections , 2,837 CNG stations, 32,282 commercial establishments and 11,172 Industrial units. The CGD sector consumes about 30 MMSCMD gas (~19% of the total Indian gas consumption). As per the commitment made by various entities in the 9th & 10th Rounds, around 3.5 crores PNG (domestic) connections and 8000 CNG stations are expected to be installed by 2026-27 across the country. To service the above demand points, gas requirement is estimated to rise to 60 MMSCMD under CGD. According to media reports, PNGRB may cover the entire country at one go in the upcoming 11th round of bidding.

The GOI is planning to set up around 5,000 compressed biogas (CBG) plants by FY2023. This will require an investment of INR 175,000 crore. The GOI is planning to invest US$2.86 billion in upstream oil and gas production to double natural gas production to 60 BCM and drill more than 120 exploration wells by FY2022.

PNGRB authorized Indian Gas Exchange on December 02, 2020. Indian Gas Exchange Ltd to promote and sustain an efficient and robust Gas market and to foster gas trading in the country. Also, PNGRB has simplified the country’s gas pipeline tariff structure to make the natural gas more affordable for distant users.

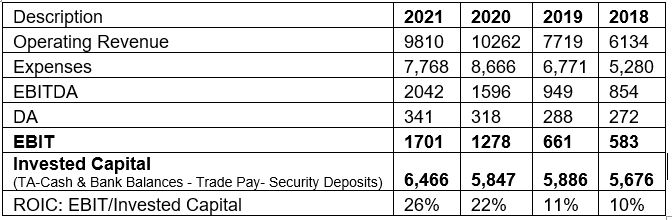

Operating Metrics:

Key Risks:

| Description |

Impact |

| Softening of crude oil prices |

Industrial customers may switch to alternate fuel; Materialized in FY16 & FY17 |

| Slowdown in industrial sector |

80% of companies gas supply is to this sector; Materialized in FY17 |

| Lax safety standards |

Loss of life, reputation & business |

| Non-availability of natural gas and higher prices of LNG |

Reduced gas demand |

| Multiple local approvals for Gas pipeline connectivity |

Delays the laying out of the network |

| Regulatory Regime |

Regulatory Board (PNGRB) frames various regulations on ongoing basis |

| Disparity in the tax structure compared to alternate fuels as PNG and CNG are still out of GST ambit |

Delay in signing up industrial customers as they are unable to take input tax credits, thus lowering their gas feedstock cost |

| Competition following the Expiry of Marketing Exclusivity (5 Yrs. for Old GA and 8 Yrs. for Gas awarded in 9th & 10th round) |

Entry of new competitors |

| Promotion of “Only EV” Policy in India |

Threat to economics of the CNG business |

| Invoking of performance bank guarantees by the regulator (PNGRB) |

Per say AR of 2017, company’s borrowings may exceed limit of 7000 Cr. MGL missed the plan and regulator permitted to submit an alternative plan to catch up instead of penalizing. |

| DTL of ~800 Cr. in FY21 B/S |

Additional Income Tax on future income |

Inflation Impact: Positive . Business shall benefit from inflation due to following factors -

- Pipeline delivery protects against inflation in transportation costs

- Low need of capex in future

- Low fixed costs

Return on invested capital: 25% +. Improving trend in the last 4 years.

Revenues: Recurring but cyclical as 80% of revenue comes from gas supply to industrial entities. Impact was evident in the revenues of FY-16 and FY17. This feature mitigates the risk from -

- EV only theme or evolving alternate fuels for mobility sector.

- Future regulation to limit ROE of the business - May impact only the CNG and PNG segment (mass utility), and not the industrial segment.

Considering India’s push for growing the manufacturing sector and environmental commitments, businesses in the industrial segment shall consume more quantity of gas in future.

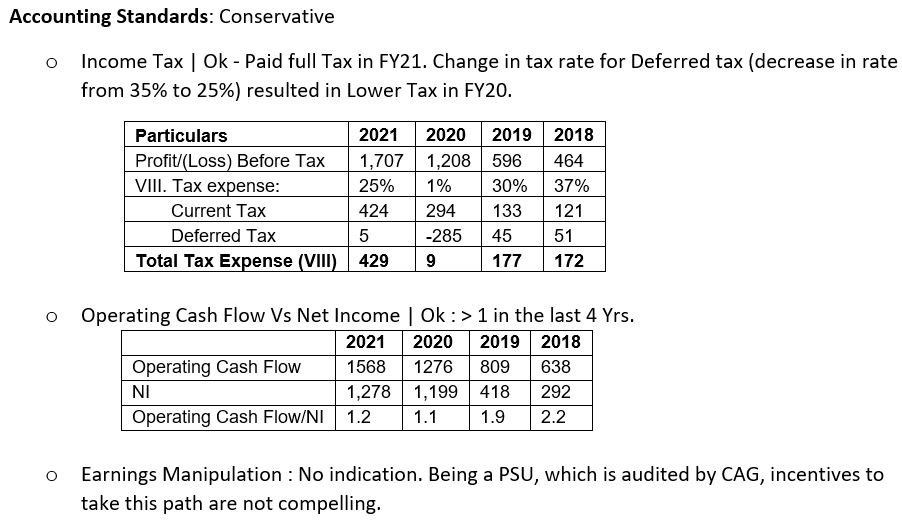

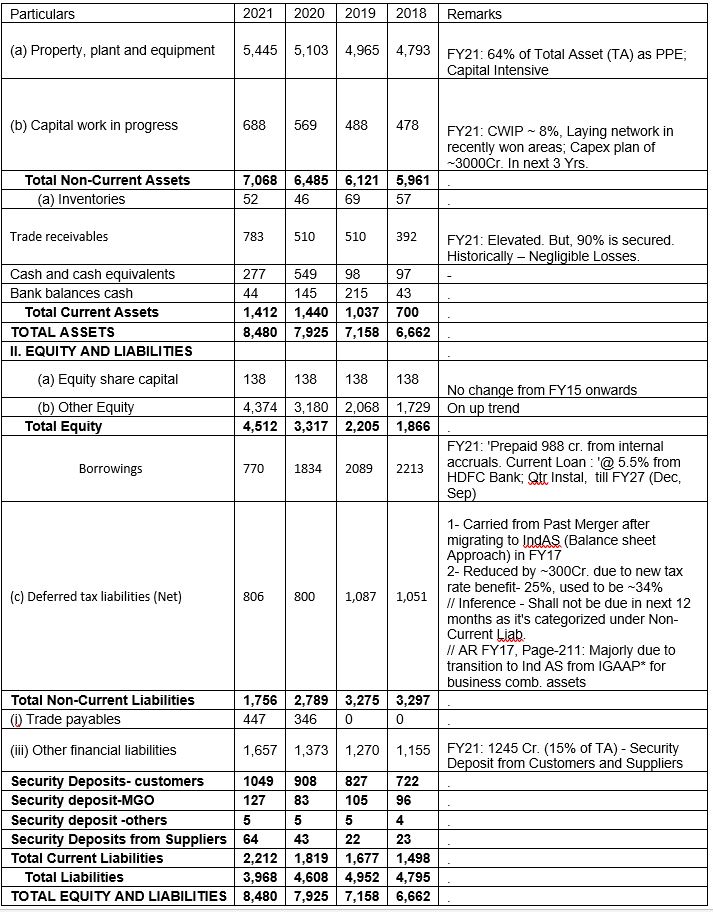

Balance sheet: Strong. I assume that the Deferred Tax Liability may lead to taxes beyond 25% in future. In FY-21, Current liabilities are 26% whereas Current Assets are 17%. On first look, the same is a concern but mitigated by the fact that 15% of the current liabilities out of total 26% are security deposits from the customers and will not be due anytime soon as well as at once. Interest rate on borrowings have reduced to 5.5% from 11% in the last 6 yrs. Also, business has a Bank Facilities of 2000Cr. (CARE ratings - September 14, 2021). Considering overall financing of the business in FY21, L-T assets are at 83% but L-T liabilities are only 73%, indicating that some of the LT assets are financed using current liabilities. Since the business generates cash flow on fortnight or monthly basis, the same does not seem to be a concern for this business.

Operating Leverage Impact: Low. At the B/S level, PPE consists of ~80%+ of the Total Assets. However, variable expenses in the Income statement make up 85% of the total expenses. The same shall result stable cash flows & earnings.

Working Capital (WC) impact on Cash Flow: Insignificant. Sales increase of almost 3700 Cr. in the last 4 year resulted in WC increase of only 66 Cr.

Future Capex Need: Per say latest rating from CARE Ratings, business plans to invest ~3000Cr. over the next 3 yrs. using internal accruals.

Quality of Management:

Last AGM was conducted in 30 minutes (per say document filed in the exchange). MD is an IAS officer deputed by the Gujarat government. Only source of communication are the Annual Report, plain Vanilla Quarterly results and short interview with business channels. No conference calls. No investor presentations.

Management’s motivation to grow:

As mentioned earlier, GSPL bought an additional 28.40% stake in Gujarat Gas Ltd. in 2018, thereby raising its holding to about 54.17% and making Gujarat Gas Ltd. a Subsidiary Company. Rationale - Direct synergy of gas transmission and gas distribution businesses as Gas Distribution Network provides last mile connectivity to the end users of the gas.

Future Growth prospects:

- Over the last few years, the company has expanded beyond Gujarat by participating in the bidding process tendered by PNGRB and winning the new geographical areas, which are contiguous to the existing areas of operation around parent’s gas transmission pipeline.

- As covered under heading ‘CGD Industry’s evolution’ , tailwinds due to governments focus provide the thrust for higher growth that may last for next 3 to 5 years.

- Performance clauses by PNGRB while awarding areas to the CGD companies.

Items to watch out for:

- Including Natural gas under GST: If gas is included under GST, the company would benefit from increased volume off-take, as industrial consumers would be able to take input tax credits, thus lowering their gas feedstock cost. Gujarat Gas will be able to take the tax credit on operating expenses and capex as well.

- Future regulatory actions on industry’s around cities to stop using conventional fuel: National Green Tribunal (NGT) identified ~100 industrial clusters with critical pollution levels that could add to the overall gas consumption basket once the gas infrastructure has been commissioned in the next few years. This appears promising for the sector, considering the stringent norms prescribed by the government in implementing the ban on polluting fuels. For instance, CGD demand significantly increased in Gujarat following the NGT order to ban coal gasifiers in 2019. As a result, gas consumption in the Morbi region increased to 5.1-5.2 MMSCMD in 2019-20 from 2.9-3 MMSCMD in 2017-18.

- Impact on CGD businesses from evolving regulatory actions

Valuation: Foresight…Exercise for us all!!! : Perfect hindsight in the below snapshot showing the nearest competitor: