SOLVAY, CHEMOURS , ARKEMA, AGC and ORBIA Q2CY23 UPDATES

SOLVAY

Management on PFAS

I’m really pleased we reached a settlement with the New Jersey Department of Environmental Protection on PFAS. This marks an important milestone in derisking our operations and follows the successful innovation of non-fluorosurfactants polymers in New Jersey, which was the first step in our journey to become fluorosurfactants free.

Management on Specialty Polymers (PVDF, PFA)

Sales up 7% in the second quarter to EUR 1.1 billion. Once again, 9% high prices were the real driving force behind this growth, more than offsetting a pretty small reduction in volumes for the segment of around 2%. Specialty Polymers delivered sales increase of 4.7%, driven by higher prices, whereas volumes were down 4%. The continued positive pricing momentum in Specialty Polymers demonstrates both the investments in our capability that we’ve been making, for example, to the value pricing, and more importantly, it demonstrates the fact that our customers appreciate the differentiated technologies that help to make them sustainable at a lower total cost of ownership, and we’re sharing that value creation – value pricing. Specialty Polymers volumes were up in electronics specifically in semiconductors and in industrial applications, but this was offset by continued destocking in EV batteries and that impacted PVDF volumes.

Now I invite you to take note of the fact that our PVDF business is diversified as we serve many markets, including EV batteries, of course, but as well as oil and gas, electronics, construction, health care. The fact is that not a single market dominates in terms of sales. Also, PVDF volumes other than EV batteries, of course, have shown resilience in the first half. When you consider the total PVDF view as we look at it, I can also confirm to you that we maintain the contribution margin percentage in batteries whilst we have grown our contribution margin percentage in the non-battery markets.

Management on Guidance

First, let me start by confirming our full year guidance. As a reminder, following our strong start to the year, you may remember, we raised our EBITDA guidance last quarter to be in the range of plus 2%, which would reflect the recovery in volumes to minus 5%, which would reflect volumes remaining stable. We had, in fact, a strong end to June, yet July sales were soft and demand remains volatile. So our order books for the remainder of quarter 3 indicate that demand will not recover in the quarter. If volume recovery doesn’t materialize, then the second half will likely be consistent with the current full year official consensus. The same focus and discipline that sustained our performance in the first half will persist in the second half. Staying close to our customers, ensuring we drive the right pricing for our offerings and maintaining cost and cash discipline internally. We may not be able to control demand, but you have seen what our teams can achieve even in challenging markets. These are the factors that give us confidence to reconfirm our full year guidance.

Analyst on Guidance

The first question was more a confirmation because I was a bit confused, on your point about the trajectory of volumes, you said June improved or was stronger at the end and then July weekend and then you said you are expecting or you’re not expecting a recovery in Q3. When you say you’re not expecting a recovery in Q3, are you implying that volumes in Q3 will be similar to Q2? Or are you actually saying because July probably was weaker, you are actually expecting Q3 to be weaker in terms of volumes versus Q2? And I think my core of the question is, today, we see a big step down in in consensus in Q3 versus Q4 – sorry, Q3 versus Q2. And I guess that just keeps this concern alive, right? which is we are seeing a step-by-step normalization at Solvay in terms of pricing. So I’m just curious how you’re thinking about that step down from Q2 into Q3 based on consensus, which clearly seems quite steep

Management on Guidance

What I was trying to say, I guess, is that demand is volatile. June was a very strong month, right? I mean, you remember, I even guided you guys on quarter 2 sequentially versus quarter 1. And I told you at that time, and I’m looking at my team [ as ] minus 5, minus 10, right, somewhere in my road shows, and we ended up minus 6. So – and the quarter, the June month really finished very well, but then July is probably one of the lowest months we’ve seen in terms of sales since 2021. And the order book so far remains very soft, right? And that’s what our peers, most of our customers, they have been telling you, right? So frankly, I’m extremely comfortable with the guidance we have given you earlier and we confirmed today. I don’t have a crystal ball. If the volume starts to recover, right, I mean, we still have a scenario where we can reach the higher end of our range. But if the volumes remain stable, , I’m talking stable versus as they were in quarter 1 and quarter 2 because we had the same decline year-on-year in the volume. I think it was minus 12% and minus 13%, right? So then we will be at the lower end of minus 5%. So that’s was the guidance implies a reduction in the second half versus the first half. And again, demand is still volatile. And I look at it with prudence and cautions but also with great confidence, right?

Management on Destocking

To give you an idea about destocking, 2 main areas Wim, EV batteries in China was impacted. Obviously, there was a big destocking in China, which impacts the specialty polymer sales. But frankly, you’ve seen this as well, material did really well, including specialty polymer. sales of polymers and other auto applications were stable, and we grew volumes actually in areas like industrial markets and electronics, for example.

Analyst on specialty polymer pricing

in Specialty Polymers, only a clarification. Is it right that sequentially, prices in Specialty Polymers were still up?

Management on specialty polymer pricing

On specialty polymer pricing. We had strong – the strong pricing was maintained. And sequentially, quarter 2 prices are slightly above quarter 1. So they have been practicing their value pricing. And where they couldn’t like in some EV batteries, right, the contribution margin well maintained. So really glad that specialty polymer strong pricing was maintained.

CHEMOURS

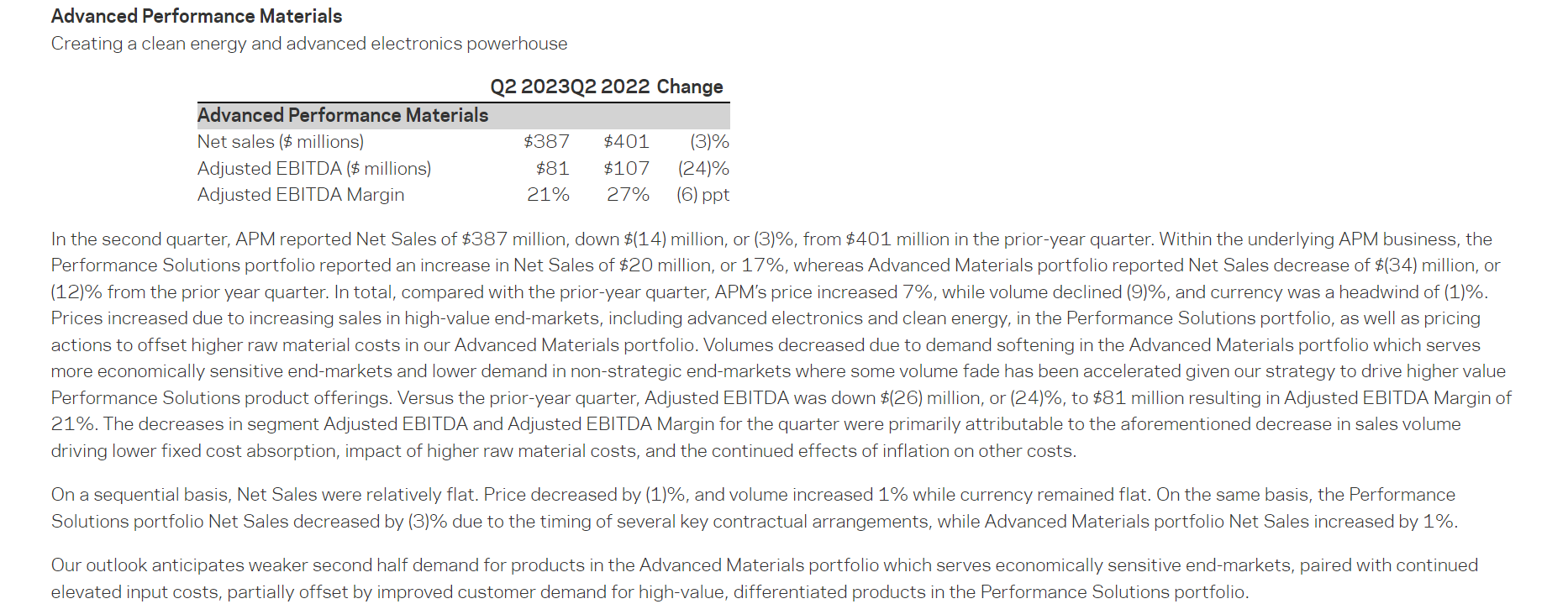

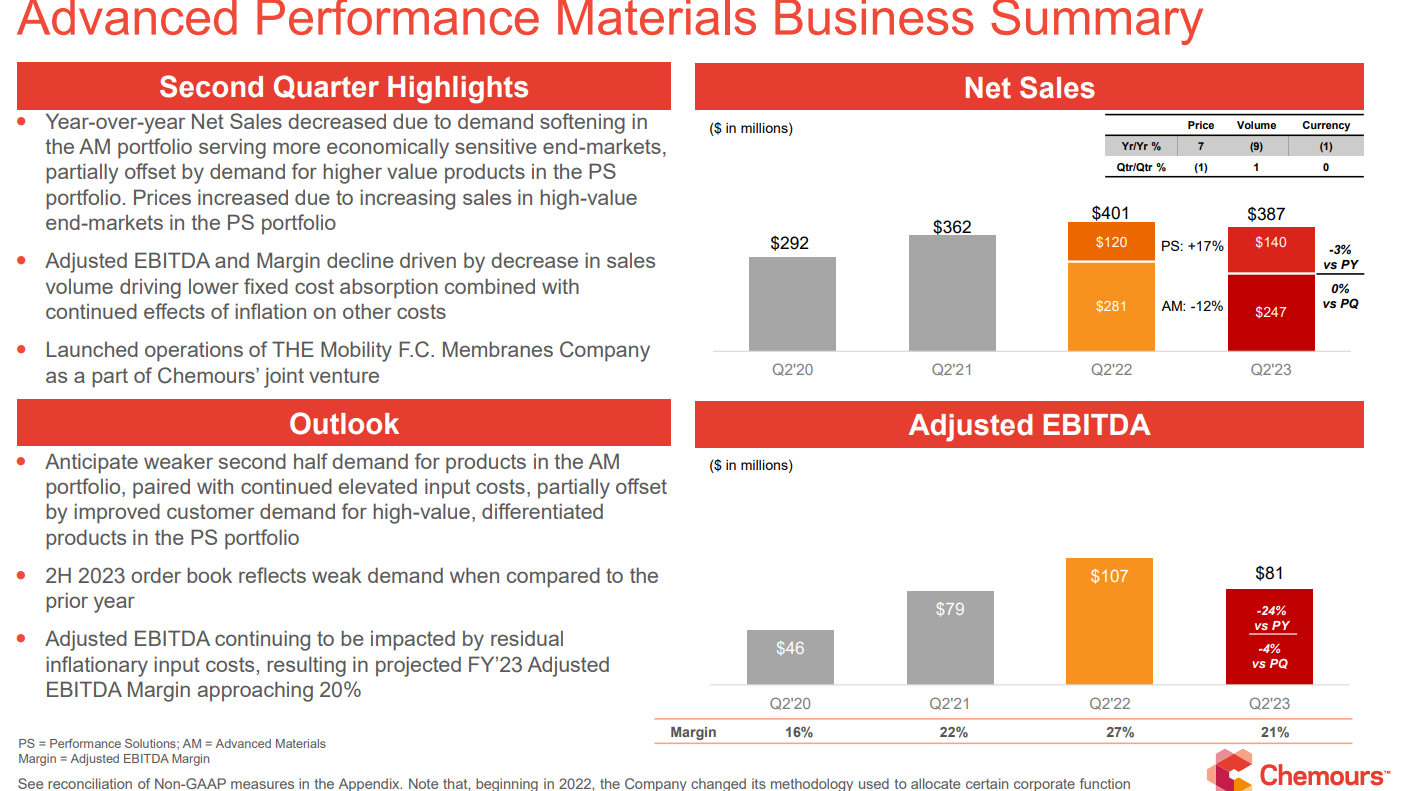

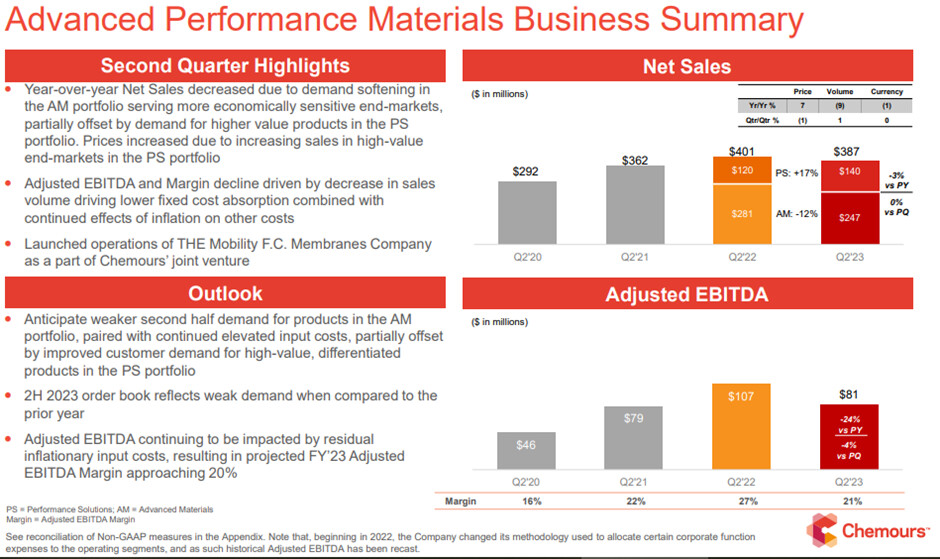

Analyst on Fluoropolymers

First question on APM. Could you maybe drill down into what areas you’re seeing the demand weakness in the second half? And then separately, could you just update us on how you’re seeing demand specifically developed for Nafion and your semicon PFA currently?

Management on Fluoropolymers

Remember, we’ve always described 2023 as a transition year for APM. What do we mean by that? We’re really ramping up our ability to our capacity in our Performance Solutions space to serve both clean energy and advanced electronics markets. And so in terms of where we’re seeing weakness, it’s in our Advanced Materials business, think of that as either broad industrial or in some specific segments like land cables, which are tied to construction, we’re seeing some weakness there as well. So I’d say, generally speaking, the weakness we’re seeing is in our Advanced Materials business.

On our Performance Solutions business, we remain sold out. And so what we’re witnessing is our growth rate here this year is really capped by how much capacity we can liberate. So as we look at the second half, we expect Advanced Materials to be weaker from a volume perspective. And obviously, there’s only so much you can do in the second half to relieve capacity. And that’s just the timing it takes to implement capital projects or, in some cases, to get permits to expand at some facilities.

So the team is really hard at work in doing everything possible to maximize throughput in our Performance Solutions area, but there’s just practical limits in what we can achieve in the second half, while we’re seeing a weakening of the Advanced Materials, which today is the larger portion of the total revenue of that business.

No, the only other thing I’d add is that, obviously, if you look at APM, like as a business, regionally, our exposure to Asia Pacific is high, right? It’s 35%, 40% of the overall business. And so as we think about that and the kind of the lack of a strong recovery in China and whatever kind of spread that has to the rest of Asia that’s certainly impacting the business.

The only other thing I’d remind folks on the call is that Q3 of 2022 is going to be a tough comp, right, for Q3 of 2023. So as we look ahead, we do expect a drop off there on a year-over-year basis in addition to something that’s going to happen sequentially in terms of both top line and bottom line.

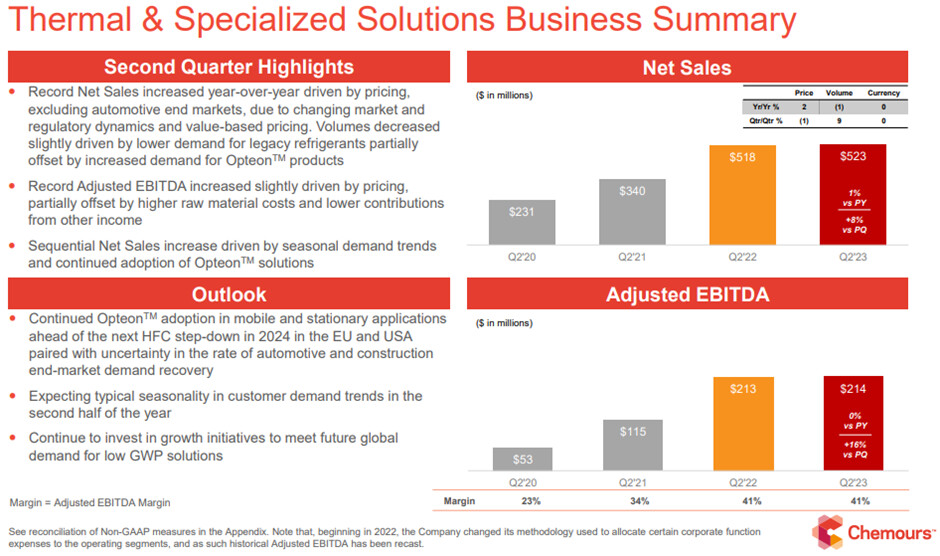

Analyst on Refrigerants

And then if we could turn to refrigerants, can you just update us on your latest thinking with the step-down, particularly in North America with HFO? What do you think that does to pull forward volumes the rest of this year? And then can we still grow those volumes into next year with the step-down? And what are we seeing on supporting HFC pricing as we’re moving into that step-down for HFC?

Management on Refrigerants

But generally speaking, as we look at the second half, we think – we believe that the step-down is beneficial to our second half. Clearly, remember that this business has a seasonally weaker especially going into Q4. So bear that in mind as well. And obviously, we’ve had a very robust first half on OEM bill rates. The question is, does that continue in the second half? And with weaker construction, that’s also a moderating impact.

So listen, I think it’s beneficial to TSS with a step-down in terms of folks wanting to make sure they’ve utilized their quota. Clearly, with end demand being more modest in a somewhat weaker economy in the second half, that could have an offsetting impact. But net-net, we factored that into our guide.

I’ll just build on that comment and just remind folks on the call that the AIM step-down coming is 30%, and the F-Gas step-down coming in Europe is 20%. So that’s obviously a 2024 dynamic that we’re going to face into. And I know that Joe and his entire team are ready to serve the market to make sure that our OEM equipment customers get all of the products that they need to build out their fleet and to deliver that next generation of HFO hardware and to make sure that our distribution partners on the refill side are well taken care of through that coming transition.

Just to be sure, as we think about the guidance for the full – the revised guidance for the full year, we haven’t really baked in a material amount of pull forward, right? So we’re not envisioning a scenario sitting here today where you get a material amount of pull forward in either the third or the fourth quarter. Obviously, the things that are going to drive that, right, through the summer and into the fall are going to be how hot is it? How much of an inventory depletion do we see down the channel? And of course, what is the strength of the overall economy? That give folks the confidence to say, hey, I’m going to pull ahead some volume into '24. So listen, I mean, with this business continues to perform very well and obviously, with the coming '24 step-down, as you all know, we’ll be ready to serve the refrigerant markets that need the product.

Obviously, the step-down in quota drives further adoption of HFO technology. We’re hard at work at our Corpus Christi site to drive the 40% expansion there, which we expect to have completed by the end of next year.

Analyst on Refrigerants

On the TSS business. So kind of a look at like the cooling degree data and that type of thing, would actually say 2Q despite all the press about the hottest day in the world and all that kind of stuff, it was actually kind of a light start to the air conditioning season. But it looks like the 3Q has really ramped up aggressively. Do you feel that pull? Like is it something that – I hesitate to say it’s spot because that almost implies it’s a commodity, but like do you feel that pull when it gets hotter? And I guess, how should we think about how that plays out if the current trends continue throughout the rest of this year?

Management on Refrigerants

Yes. So , as you alluded to, we had a relatively cool first part of the summer, which delayed the start of the season. And obviously, with the more recent warm weather, we will see higher utilization rates or higher consumption of refrigerants as folks need to service their equipment to deal with the current weather patterns we’re seeing, especially here in the U.S. and Europe. And so our view has always been that any pull ahead related to the step-down would come later in the year, dependent on how much quota folks had used throughout the year.

A lot of the refrigerant products – what’s really great about our TSS business is that a significant portion of it is a replacement or a service business. And so there’s not a lot of transparency in terms of where distributors are in terms of consumption of inventory. And so we – yes, it creates demand when you have hot days like we’re seeing recently. But there’s also quite a bit of inventory in the system held by distributors. And there’s typically not a lot of line of sight as to where that inventory level is and whether folks will need to consume more to use up their quota.

So as we reflected on the second half, we believe there will be some pull ahead as it relates to the step-down. Folks will want to make sure they’ve used their quota. But a lot depends on utilization through the end of the year, especially through the cooling season this summer, and we’ll just kind of have to watch it as we go.

Analyst on Refrigerants

Okay. Perfect. And I also wanted to ask a little bit about illegal refrigerant imports. There have been some articles and some mentions by the American HFC Coalition about a high amount of R-401B refrigerant coming to the U.S. from China. And I don’t believe it was an issue for your second quarter results, but is it something that you’re concerned about in the second half of the year?

Management on Refrigerants

Yes. As we think about illegal imports, we learned a lot of lessons out of Europe, right? So as we were launching HFO technology in Europe on the stationary side, specifically, we learned a lot of lessons from the illegal imports that came across from Eastern Europe and Southern Europe and changed the quota dynamic in that market. So we took a lot of those learnings around inventory management, border control checks and working with authorities and layered that into our approach to the U.S. market and worked a lot with EPA and a number – Homeland Security and a number of other agencies in order to make sure that as AIM was getting stood up. We had some of the right enforcement mechanisms in place, and we created some awareness right around the issue. So obviously, we need to remain vigilant on illegal imports. It’s not something we’re ever going to take our eyes off of.

To your question specifically about 410B, we wouldn’t necessarily view that as an illegal import issue, but more of a composition of product issue and the importation of that being used to kind of to skirt other regulations around the import of 410A. So our teams are all over this. Joe and his entire team, they work hand-in-hand with federal, state and local authorities here in the U.S. to ensure that there isn’t a problem going forward. So we’ll keep an eye on it. But for now, we remain confident that the law can be well enforced here in the U.S.

Analyst on PFAS

First question is just around the PFAS potential settlement. We’ve all seen a number of state AGs have kind of stood up against the 3M settlement. Would you expect something similar for your settlement where there would be people that prominent that would try to either alter it or kill it? And if not, can yours go forward do you think with the judge if the 3M’s doesn’t?

Management on PFAS

No, listen, we saw the news of the AG opposition to 3M settlement. Obviously, when you’re dealing with something this complex and this far-reaching, I think we would certainly expect folks to have an opinion, right, on how they think the – what they think the outcome should be. Sitting here today, we can’t predict whether or not similar objections would be raised against our settlement or not. But I think that what we do have confidence in is that the settlement that we entered into based on what the plaintiffs have asked is a very good settlement. And I think that, that opinion has been reinforced by the court, right, that they believe that this is a good settlement. So we’re going to continue to do what’s asked of us by the court, certainly, and work through the process first through preliminary approval and then ultimately, right through final approval at the end.

ARKEMA

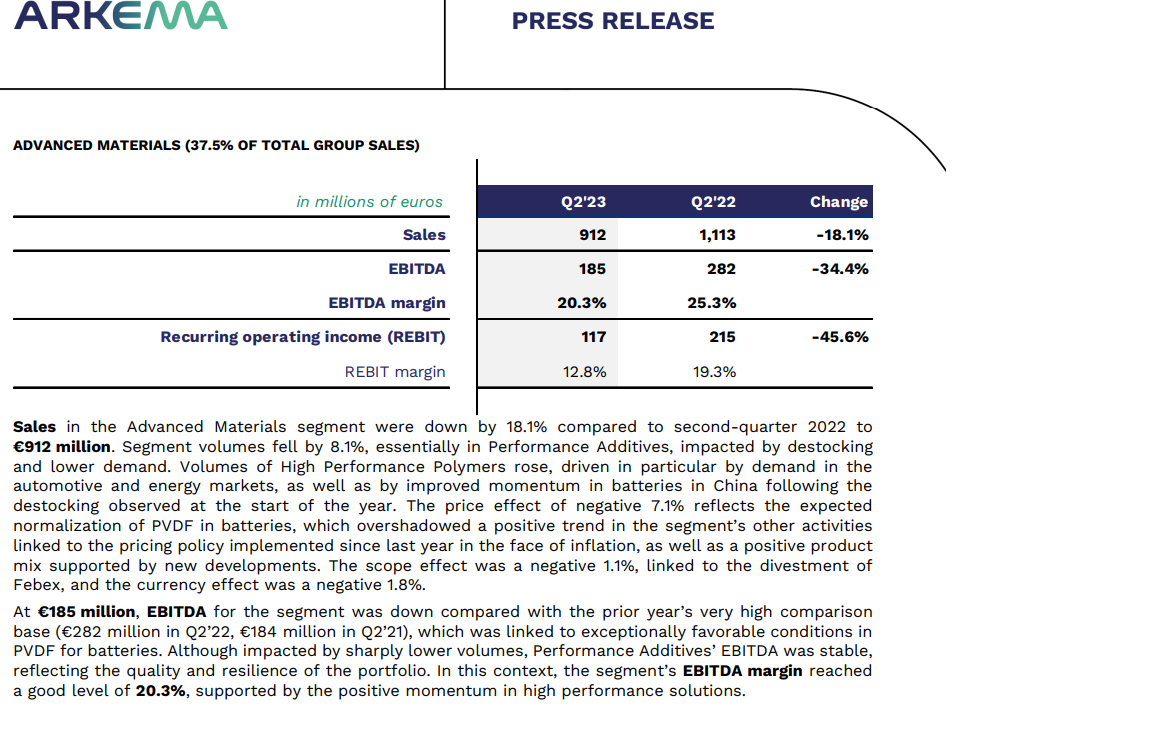

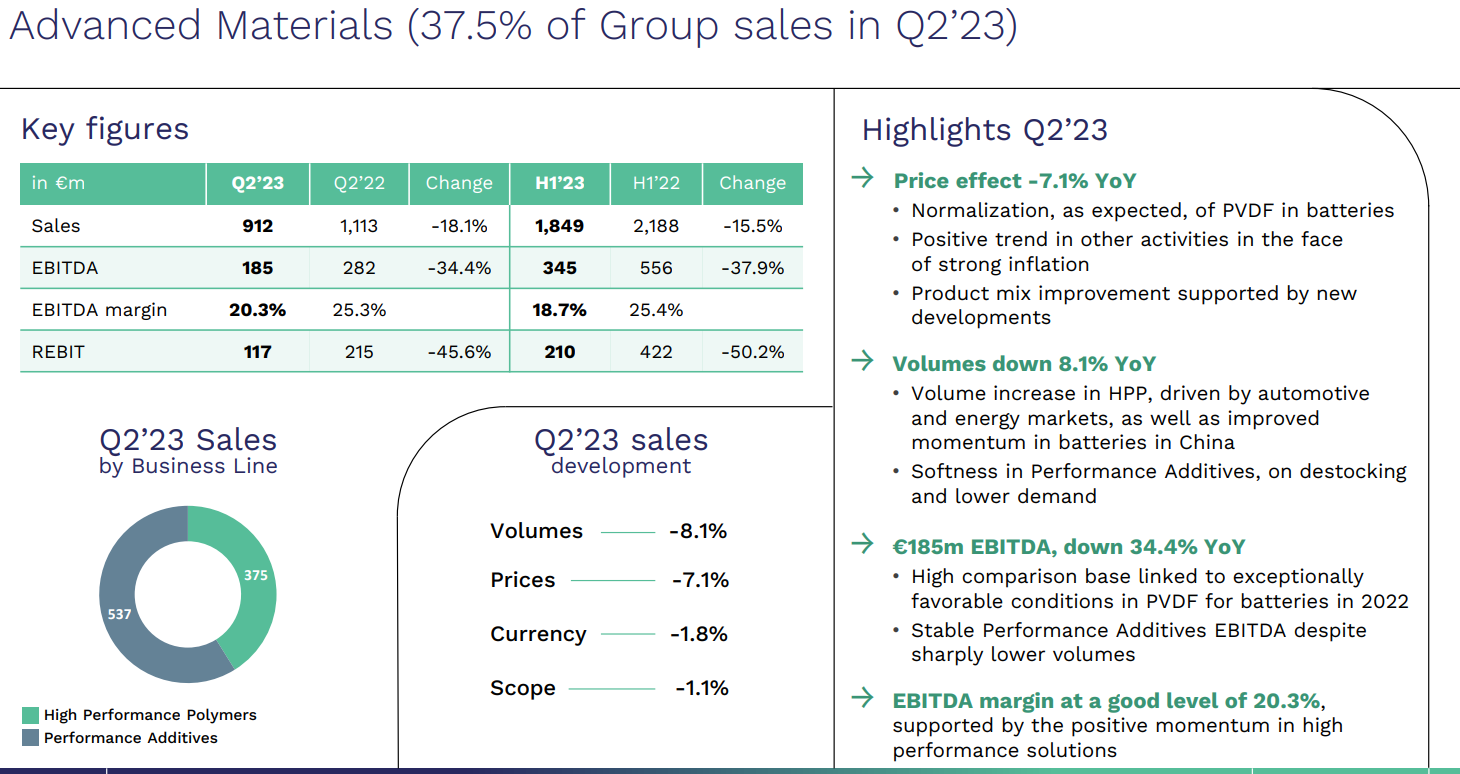

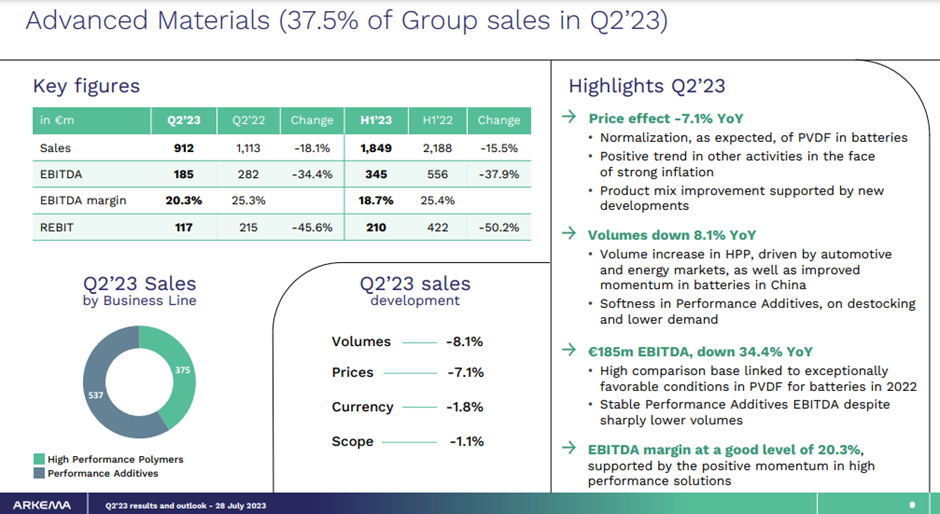

Management on Advanced Material

This performance was achieved in difficult macroeconomic conditions marked by low visibility and weak demand, including continued destocking. This quarter was nearly all over the place with nevertheless a few exceptions like automotive, energy and batteries. In particular, destocking of the battery in China continued in the early part of the quarter, but seems to have come to an end and volumes finally turn positive on the quarter. All in all, while group volumes were lower year-on-year, our pricing remains firm for the most part in the context of general inflation, even if raw material declined. Excluding the expected normalization of PVDF and upstream acrylics I’ve mentioned before, we already had the opportunity to comment in the past quarters.

In Advanced Materials, we had the reversal of the PVDF overrunning, but we benefited from high value-added new business developments as well as resilience in high performance polymers in the U.S. and to a certain extent also in Europe.

Analyst on Refrigerants

but just first question on the topic on fluorogases. I know we’ve not talked about it for a while, but just looking at some of the anecdotal data, et cetera, it seems that prices are very high this year or going up strongly this year on the back of the planned reduction in quotas both in the U.S. and Europe, I think it’s in 2024. I mean in the past, we’ve seen this dynamic where the prices go up into the cuts – into quotas and then they fall post the initial buying wave. Is this something similar we should be expecting this cycle? Or is there a different pattern you think, because of maybe changes in the market structure, et cetera? And is this something a material driver to Arkema’s earnings in intermediates this year? That would be the first question. And the second question was just around – you mentioned certain seasonality, and that seasonality – typically, even for second quarter, you tend to see a softer – sorry, third quarter – softer third quarter versus Q2 just because of seasonality. Is that something you expect? Or because of the project contribution and fixed cost savings we should be not expecting that seasonal decline in Q3 versus Q2?

Management on Refrigerants

So on the first one, the answer is rather easy. In the old time, our profitability was really shared between Asia, Europe and the U.S. U.S. has already been very stable. Europe was, I would say, rather stable with a low performance, but with no quota implemented, except with 1 year where we have disturbance because the regulation was not applied, but it’s not the case anymore because it took some time for the European Commission really to make sure that this regulation was implemented, but now it’s done. And Asia was a big contributor. Today, different. So I would say the – most of the large – very large majority of the contribution is between U.S. first, then Europe. In Europe now, the quota scheme is respected. And we don’t have the disturbance we had in the past, and in the U.S., it’s stable like it was. Now when you say that we seem to have a sort of elevation of prices and profitability for [ all ] this year versus last year, it’s not the case now. So we have a rather stability in fluorogas, while – maybe a little bit better than the last year, while we decrease in intermediates on the Chinese companies as we mentioned. So our feeling, and it’s a strong feeling, we believe that fluorogas in the coming years will be rather stable. And the mechanisms are different now than they were in the past. And the Asian part, which was really a relative one is quite small now. So we have a far more stable positioning. With regard to seasonality, I will not comment really quarter-by-quarter. But what I say on the semester, and I say – I think I said that last time, is that the second semester normally is a little bit softer in seasonality than the first one. If you make the math and if you look at – several years have passed for Arkema. This year, it’s a bit different because we have still momentum – Even if it’s already a little bit below in new project contribution. This contribution will be there. These are good elements. And I would say even if today we have no visibility, even if we have not – if we remain quite cautious, maybe end of the year a little bit incremental, less of destocking, it can make a difference also. So if you take these 4 elements, it’s not a pure rationale. There are still uncertainties. But all in all, it makes, I would say, a seasonality not exactly the one we had in the past. Okay?

Analyst on PVDF

Firstly, on PVDF., could you give us some indication of what sort of volume growth do you see in the second half versus first half, and then into '24 based on sort of your customer feedback? It seems like volumes have stabilized. So – and then Chinese prices have, on a reference level, also stabilized. So do you expect price stability in your portfolio as well for H2 and into 2024? That’s my first question.

Management on PVDF

On the first one, we already have good volume growth between Q1 and Q2, significant. So it depends if you compare us to H1 or H2 to the trend of Q2. I would say, in terms of volume we plan to have the H2 more in the order of magnitude of the Q2, which is more comparable. While, as I mentioned, the Q1 in volume was more difficult. So then in '24 versus '23, just because we had the weakness at the start of the year, will continue to grow. And as you know, we have invested also both in France and in China for, let’s say – to make the story short, midyear. One is a bit before midyear. The other part is more a bit after midyear. So which means all in all we’ll get more capacity overall in '24 than in '23. So because of that, because the market – we have a lot of – the business, as you know, in battery – but not only in battery normally, '24 should be above in volume compared to '23 and even compared to the second part of '23.In terms of pricing, we see for the Chinese pricing it’s clear that we were the big leader in the first part of the year, even we continue to see decrease in Q2. I agree with you, normally, we should be more or less stable. But again, wait and see, but everything is factored in our guidance anyway

AGC

Management on Performance Chemicals FKM, PFA, PTFE, ETFE, PEM

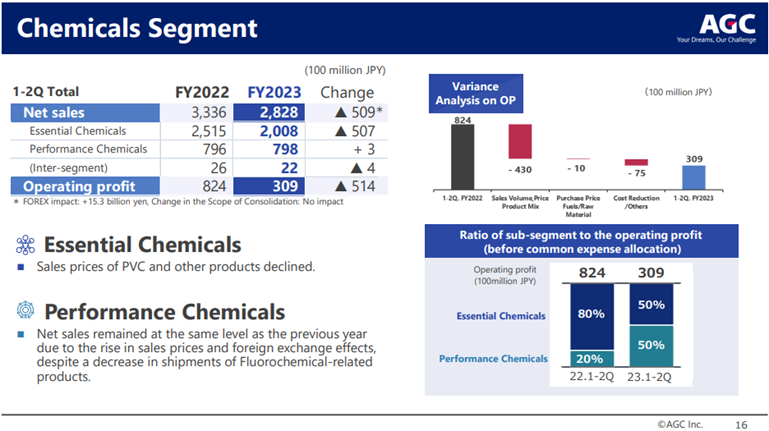

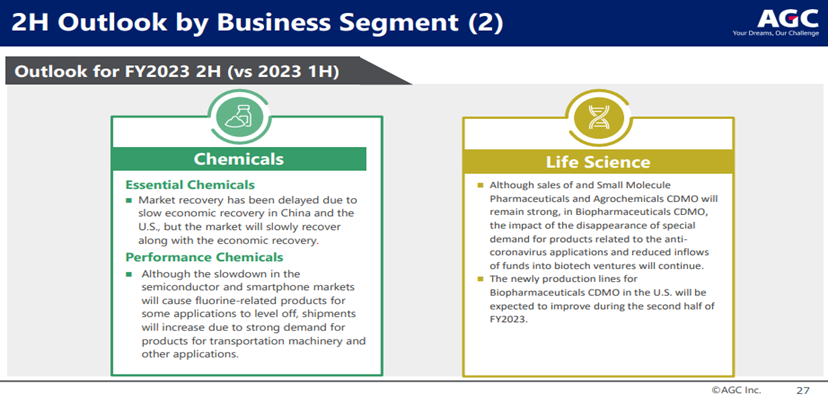

Next is Chemicals. In essential chemicals, the market is expected to recover gradually as the economy recovers. However, not a dramatic recovery. In Performance Chemicals, the semiconductor and smartphone markets are slowing down. And the demand for fluorochemical-related products is expected to reach a standstill. However, the product demand for transportation equipment sector is expected to increase.

As for Performance Chemicals, we have been affected by the semiconductor and smartphone markets up to this year, but starting next year for Essential Chemicals. The gradual recovery in China and U.S. markets are expected, and with that, we expect the gradual recovery. As for Performance Chemicals, in addition to the market recovery, the capacity expansion is to contribute to the improved profit.

Analyst on PFAS

Would like to move on to the next question about PFAS regulation. What will be the impact on AGC business? So within PFAS, especially carbon PFOS and PFOA has come under a lot of scrutiny. So the carbon of 6 or over 9, so it has actually been expanded to these sort of fluorochemicals as well. So perhaps with lower the carbon number may come under the scrutiny of the regulation. So within AGC’s groups, what will be impacted going forward? What are the potentials of – so Miyaji san, please?

Management on PFAS

So in terms of PFAS, PFAS. So we have projected the slide already. As many of you are aware. So PFAS, P-F-A-S that is, this is really a name for the entire group for the polyfluoro chemical substance. So about 15,000 different substances come under this group – or 12,000 rather. And what has been under a major scrutiny right now. And of course, there’s been a lot of report domestically. So PFAS for the inflammatory agent. And so this is under the regulation for PFAS. And of course, we have seen some litigation in the U.S. as well.So for this particular usage, P-F-O-S, PFOS, we have no track record whatsoever in terms of production and sales. And therefore, our exposure is none as far as PFOS is concerned. Now for PFOA, again, this is another regulated substance. So it is a water repellent agent, as one of the representative example. So we have seen some different generations. So historically, regulations become more stringent application of this – we have actually withdrawn completely from this. So that’s where we stand right now. So we do not perceive any major risk related to this PFAS regulation.What we are focusing is on the right-hand side, more on the resin focused products. So they are not absorbed into human bodies, extremely safe in terms of its nature. So in pharmaceuticals and agrochemicals, they are completely regulated by the regulation. The safety has been confirmed. So our focus is more on the right, and that’s where we are growing.So PFAS was in this grand scheme of regulation. We may have been categorized as part of the operator was in it. However, in terms of our business focus, we are very much focused on more of a safe and highly regulated material. So we do not perceive a large risk, as far as our business is concerned.

Analyst on PFAS

Next question, again, is related to PFAS. Overseas, the litigation on the products are being made are reported is AGC not affected?

Management on PFAS

Well, again, using this slide, the biggest issue today is PFOS products. Many litigations, lawsuits, especially the fire extinguishing [ firms ]. The litigations in the U.S. tend to try to cover a wide area, because we use chlorine – there are so many companies that are being sued, and we – sometimes our name is included on the list. But actually, we have yet to receive any of the lawsuit notification. So it’s not a risk right now. And of course, we are consulting with the lawyers for appropriate response, and that will continue. Of course, in Japan, no litigation

Analyst on Margins in Chemicals

Thank you. Next question. In Chemicals, second half operating profit plan, JPY 9.2 billion increase is projected over the first half. Could you divide them between essential chemicals and performance chemicals?

Management on Margins in Chemicals

Yes, this relates to what was explained earlier. In essential chemicals, at least given the current situation, we are not expecting a big recovery. And that is the basis of our projection. So that projected increase is largely in the area of Performance Chemicals. Performance Chemicals by nature are more focused on the second half, including increase in shipments, and the increase in sales and profit are always expected in the second half. So right now, with the recovery in the automotive, we expect a growth in Performance Chemicals.

ORBIA

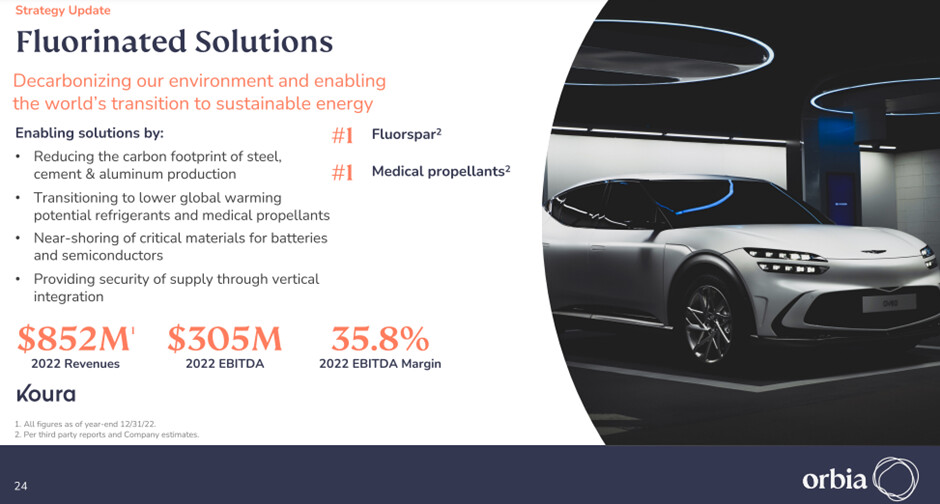

Management on Fluorinated Solutions

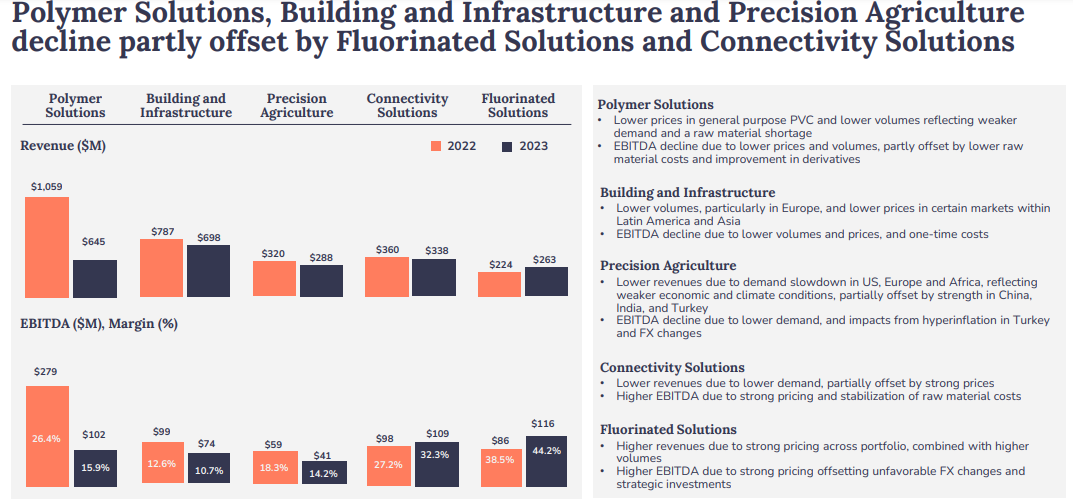

Fluorinated Solutions had another strong quarter with second quarter revenues of $263 million, up 18% year-over-year. These results were primarily driven by favorable pricing across the product portfolio, as well as higher volumes. Second quarter EBITDA was $116 million, an increase of $30 million year-over-year, with an EBITDA margin of 44.2%, an increase of approximately 560 basis points. This was largely due to the strong pricing that more than offset unfavorable foreign exchange impacts and spending on growth investments.

And finally, in Fluorinated Solutions, demand and pricing are expected to be generally stable in line with normal seasonal patterns for the rest of the year. We continue to see increasing interest in our next-generation refrigerant gases and momentum in the conversion to medical propellants with lower global warming potential. Our projects to manufacture lithium-ion battery materials in the United States are on track.

On Koura’s performance and its margins. And the Fluorinated Solutions business, as many of you know, is very well positioned in the fluorine chain with the unique access to fluorine that we have with our mine in Mexico. And as I’ve talked about this many times in previous earnings calls, as the decade continues, demand for fluorine, particularly in new applications, will continue to grow and supply will remain constrained. So, our long-term view is, the fluorine chain is favorably positioned to benefit over the long term, both in existing applications and in new applications.

Now, in existing applications, particularly the refrigerant gas business, where much of our participation is in regulated markets, where there are F-gas quotas, and these quotas decline over time, and as volumes decline, prices go up. And I talked about this at the Investor Update call, where eventually you would expect the pricing of current generation refrigerants with the quota to converge with the declining prices of the next-generation refrigerants. So, that is what has contributed to strength in Koura’s earnings across the board, in all of the segments we participate in.

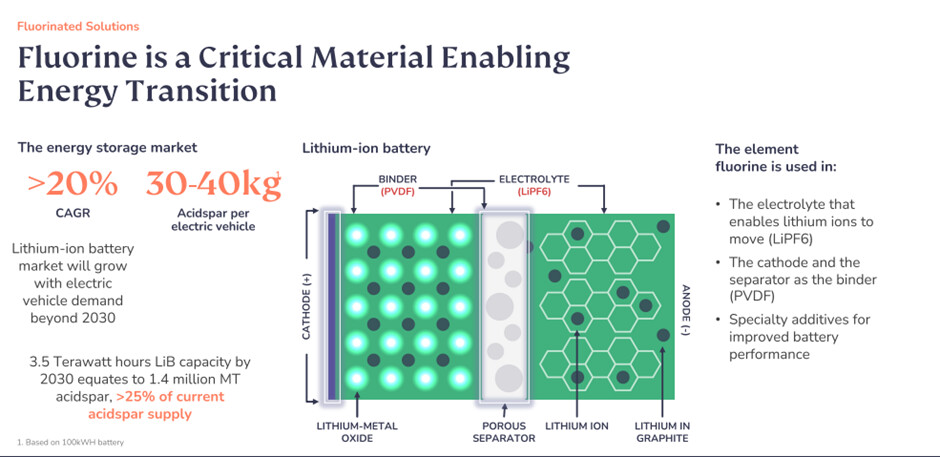

Now of course, the cooling season is getting over. And so, as I had indicated – as we had indicated in the press release, going forward, it will be normal seasonal patterns in Q3 and Q4. And over the next couple of years, we will continue to see the transition from the current generation refrigerants to the next-generation refrigerants. And then, eventually in 2026, when our new assets for battery materials are in place, that’s when you will see some contribution from the energy materials business to Koura.

Analyst on PVDF

I actually have a follow-up on your strategic CapEx and some of the projects that you just mentioned. So, the first one has to do with PVDF. It seems to be that there’s a lot of things happening in the EV space, on-shoring trends, Inflation Reduction Act, so things are unfolding, well, rather quickly. And you mentioned that this project is on track. So, I was hoping to hear, if you can just elaborate a little bit more as to where is this project at this stage? How is it evolving? Whether you could be perhaps thinking of a different timeline, given the quick turnaround in the space and the very big opportunity for the EV space, and how PVDF is important for that?

Management on PVDF and LiPF6

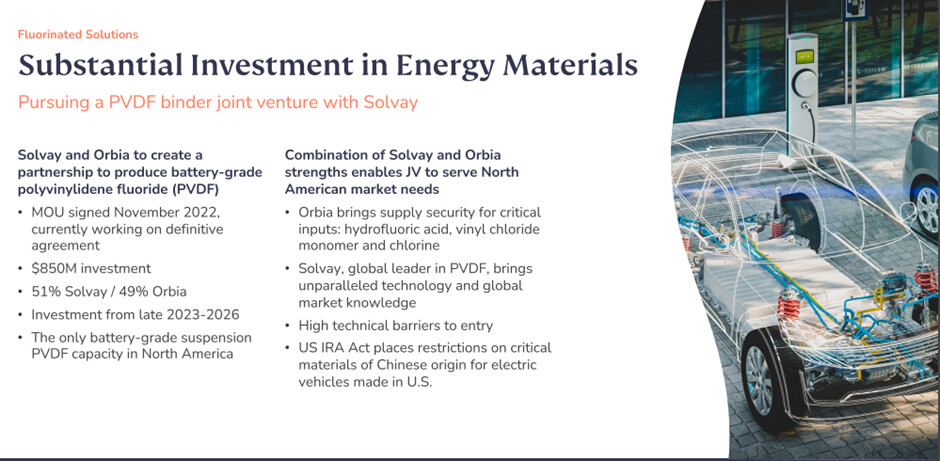

Look, first and foremost, you don’t make long-term commitments based on short-term high frequency information or short-term considerations. It may affect – it may fine-tune timing of your projects or some tweaks to your projects, but you don’t typically make long-term commitments based on short-term information. Now, speaking of energy materials, and here, we have a very significant effort in both PVDF and LiPF6. And let me remind everyone, PVDF, we are doing this as a joint venture with the Belgian company, Solvay, and this has been structured as a 51/49 JV.

Solvay is the world leader in PVDF for batteries. This will be the first plant in the United States catering to the EV industry. And Solvay is the beneficiary of the DOE grant for this project as well, and it will partially benefit the JV. We had signed a MOU with Solvay back in November, and now we’re in the final stages of finalizing the definitive agreement, but the engineering is going on in parallel. This project is expected to come online sometime in 2026, potentially in the second half of '26. Timing varies depending on how soon you can build these plants, but that’s when it’s beginning – it’s expected to start contributing.

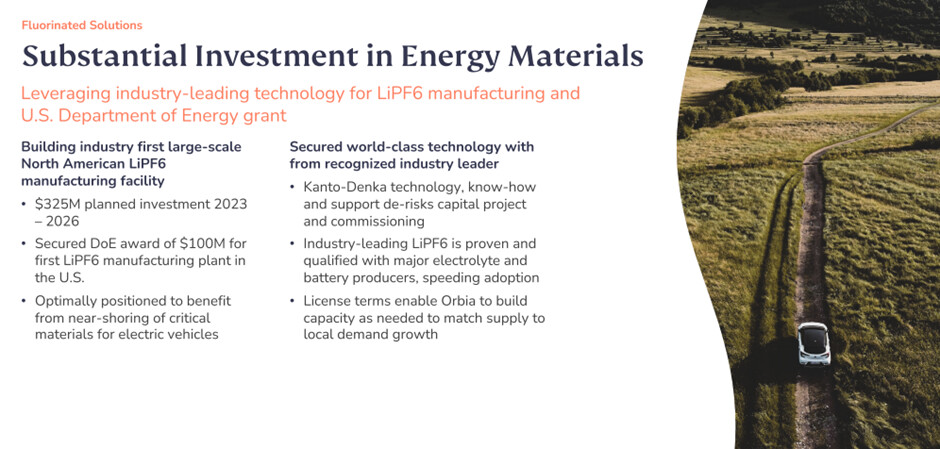

The second project, which is equally important, and this is 100% owned by Orbia, is in LiPF6, which is another key battery additive, which is used in the electrolyte. And for this, we have secured a license from the Japanese leader, Kanto Denka. That’s done. That’s finalized. And the technology exchange is going on, even as we speak. The engineering work has begun. And the timeline for this project is also sometime in the middle to the end of 2026. And for this project, we have received a $100 million grant from the Department of Energy.

Now, both of these are incredibly high-value projects. And as I’ve indicated earlier, in terms of the returns, the returns are in the range of 2x to 3x EBITDA multiple on these projects. And you can imagine, you can do the math on the amount of battery capacity that is needed over the course of the decade, and that we might have to exponentially grow this capacity over the following years. So, this is going to be – these 2 projects are going to be very important to Orbia’s growth going forward.