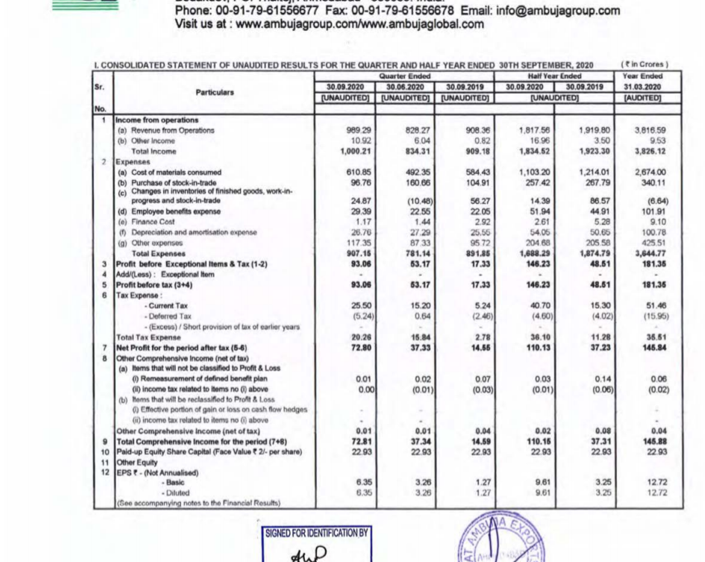

The Company recorded operational revenue of 3816.59 crores as compared to ` 4021.44 crores during the previous financial year.

The Company achieved EBIDTA margin of 7.63% in F.Y. 2019-2020 against 9.55% in F.Y. 2018-2019.

The Company achieved Earnings before Interest, Depreciation and Tax (EBIDTA) of 291.23 crores for the F.Y. 2019-2020 against that of 384.02 crores for the F.Y. 2018-2019. The EPS for the year reduced to 12.72 per share as compared to 17.28 of last year.

Debt to equity ratio improved from 0.17 to 0.11 and interest coverage ratio improved from 20.4 to 32 due to reduced debt and lower utilization of working capital limits.

Capex

During the year, the Company has invested about 60.43 crores in the ongoing projects. Out of this, the Company has spent 36.81 crores as routine capital expenditures in modifications of existing projects.

This investment was for its maize processing units at all locations and agro processing segments. Execution of various derivative products manufacturing facility at Chalisgaon is completed except for DAH and it has commenced commercial operations. The Company has so far spent 62.68 crores on this.

The execution work on the green field project of 750 TPD Maize processing facility at Malda in West Bengal has also commenced.

Client Mix

It competes in the domestic and global markets and caters to food, pharmaceutical and feed industries.

Export Sales for the F.Y. 2019-2020 was 569.02 crores as compared to 1206.46 crores for the F.Y. 2018-2019 mainly due to availability of more remunerative prices in the domestic market.

The export revenue has taken a dip since due to higher prices of corn and soyabean, the prices of finished products were not competitive in the overseas market.

Loan and Liabilities

The year started with moderate use of WC limits of about 190 crores in April 2019. It peaked to around 226 crores in May and ended with lower use of WC limits of around 146 crores in March 2020. The fall in use of WC limits was largely due to lower procurement of oil seeds and deployment of internal accruals.

During the F.Y. 2019-2020, the Company has not raised any funds through Commercial Paper (“CP”).

The Company has a rating of A+ with positive outlook for long term working capital facilities from CRISIL as per the applicable regulatory norms.

Miscellaneous

Disclosure on commodity price risks and commodity hedging activities. 16% of soybean seed exposure is hedged and 7% of soybean oil exposure is hedged through commodity derivatives.

Crop of soybean and maize was also affected negatively due to prolonged monsoon. Due to this availability of good quality material at particular market price was a serious concern during the year. The prices of maize reached a high of 24 per kg. This adversely affected the off take of finished products since beyond a point the market could not absorb the high prices. This in turn affected the grinding quantity and hence weakened the performance of the industry

Massachusetts Institute of Technology increased shareholding from 0.19% to 0.87%.

Covid-related:

Being a leading manufacturer of Maize Starch, Starch Derivatives and Edible Oils we had been bestowed upon with a great sense of responsibility to operate amidst these difficult times to supply these essential commodities across the globe.

since the Company is a major supplier of food, feed and nutritional ingredients, the demand is estimated to get its normal levels sooner than Industry in general.

As per the AR, the great monsoon season turned out to be ‘too good’, reducing crop yields, reducing maize qualities, disrupting the maize market, increasing the maize prices to Rs 24/KG and thereby reducing the company’s sales volumes. This demonstrates the importance of weather on the company’s fortunes. The capex plans for the malda plant are going as per plans. The company reduced debt due to lower WC utilization and also using internal accruals.

Disc: Invested a small amount, full portfolio here.

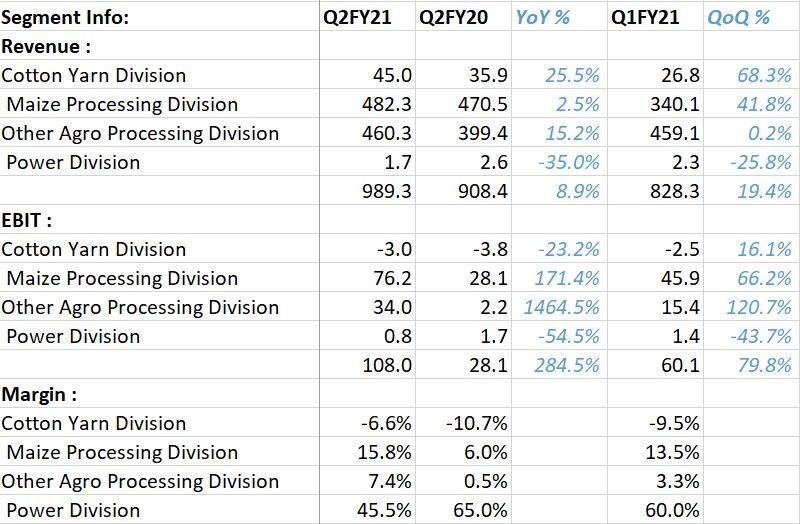

[Operational highlights] The Maize processing business contributes 85% share in the overall margin of the company. Over the last 5 years, Margin has remained above 15% except this year when it fell due to an unprecedented rise in maize prices. Achieved capacity utilization of 69% in FY20. 40% of all starch output is value-added products and 60% is commoditized products.

[Malda Capex] Implementation of Malda Capex (Additional 1000 TPD Maize processing plant) is on track for completion in 18 months. We expect to increase top-line by 600cr when Malda capex comes online.

[HFCS] FSSAI standards for production of HFCS are expected soon this year. Post that, the company will take up 100 TPD HDFC plant at chalisgaon plant.

[Future Guidance] Pre-covid, Capacity utilization was 80%. Now it is 70%. Expect it to come back to 80% in Q3 and 90% in Q4 FY21. Value addition plants have commenced operations in Chalisgaon. Full effects will be seen in Q3,Q4. Will double the Polyol capacity in next 12-18 months to 600 TPD. Maize prices have been 13-14 Rs this year. Expect them to continue to be stable (13-16 Rs) due to bumper Kharif crop. 90% power requirements are fulfilled through captive power generation. Expect to go up to 95% by FY22Q3. Soybean crop output will increase by 40-50% this year. Agro division should do much better this year. Post Malda plant, company will have 28-30% market share in maize processing. Will keep setting up new plants to increase capacity. Plan to expand outside current geographies. Will spend 500cr capex in next 2 years, majority in Maize segment. Including setting up new solar power plants.

[Share splitting] Company board decided to split shares so as to make trading easier due to requests by share-holders: Volumes were less so it would be ideal to split it to make trading easier.

[Industry picture]: GAEL’s gross margins are 4-5% higher than Competitors like Surjit and Riddhi Siddhi in spite of locations not being so different and competitors also having value added products. Margins are higher because the company is the most cost effective producer in the country. Raw material purchase planning is much more effective. 50% of all such products which are exported outside of India are done by the Company (export to 75 countries). Percent of starch converted to derivatives and sold is much higher for GAEL versus competitors. Contracts with clients are not always L1 since these are global FMCG and Pharma giants who require backup suppliers. These are not tenders either. Contract consists of a negotiated price. Export demand across the world has increased due to the China effort (global supply chain trying to diversify away from China). With maize prices coming down, avenues to export improve dramatically. GAEL is largest sorbitol, dextrose anhydrous, dextrose monohydrate, Maltodextrine producer in India. There is huge demand for Indian soybean because it is non-GMO.

[Cotton yarn business]: Company is in Final stages of evaluating how they can turn it around and whether they even want to continue in this business. Haven’t done any Capex in the Agro sector since 2012.

I found point 5 to be a little concerning. It is not clear why investors would ask GAEL to split a 200 rupees stock into 2 100 rupees stock. It certainly can improve trading volumes. But why would investors care about trading volumes? Would be happy to hear what other boarders think.

As per the management the biggest risk to the business is Raw Material prices, which is my own assessment as well. GAEL is definitely executing very well. Would be reasonable to call it the most efficient/profitable maize processing company in India. The long gestation period contracts with oral care, FMCG and pharma companies act as some sort of a Moat for the company. However, the RM price should would always remain.

I had attended the AGM last time in person and have seen many “old timers” asking for bonus shares - makes no sense to me but that’s how some investors think…

In their latest filing

“Company has acquired I00% Equity shares of Mohit Agro Commodities Processing Private Limited on 9th September, 2020, making it a wholly owned subsidiary of the Company”

Couple of things on this .

The promoter of MACPPL is also of promoter of Gujarat Ambuja Exports Limited and the acquisition would fall within the related party transaction.

Cost of acquisition or the price at 16,00,000 Equity Shares @INR 79/- =12.6 Crore

The acquired company could have fixed assets on which it may or may not be earning rental income. Wonder why this has not been clarified in the filing. Does anyone have some more understanding on this acquisition?

I also come from the same school of thought… a stock split adds virtually no value to the fundamentals of a company. That said, even the greatest investor os our times, Warren Buffet, had to succumb to whatever pressures he might have had to face, to finally allow his company Berkshire Hathway split the face value of its share. Warren Buffet too was strictly against splitting and on the theory of ‘a stock split will make a stock more affordable to retail investors’, he always believed that high share prices attract like-minded investors who are focused on long-term profits as opposed to short-term price movements.

While a company technically should not be interested in factors like trading volumes and stock prices etc., rarely do entrepreneur promoters be able to strictly follow that principle. And there’s nothing wrong even if they show interest, as long as they don’t resort to fraudulent practices in the interest of market cap gains. And this doesn’t seem to be the case with GAEL, in my opinion, and hence it shouldn’t bother investors a lot.

As much as i get to understand, the company has got the assets valued by an independent valuation company and done the transaction at arms length pricing. Mohit Agro, the group company which it has purchased 100%, owned some warehouses which was leased out to GAEL. So while the debate on ‘Own vs Lease’ could continue, especially given the sub optimal yields on owned properties (commercial or residential), a warehouse remains a strategic asset to a business like GAEL’s which may have prompted them to buy out the asset completely. So unless the value paid for acquiring Mohit Agro is significantly bigger than the actual value of the property, it shouldn’t bother us as much.

Great Results !!

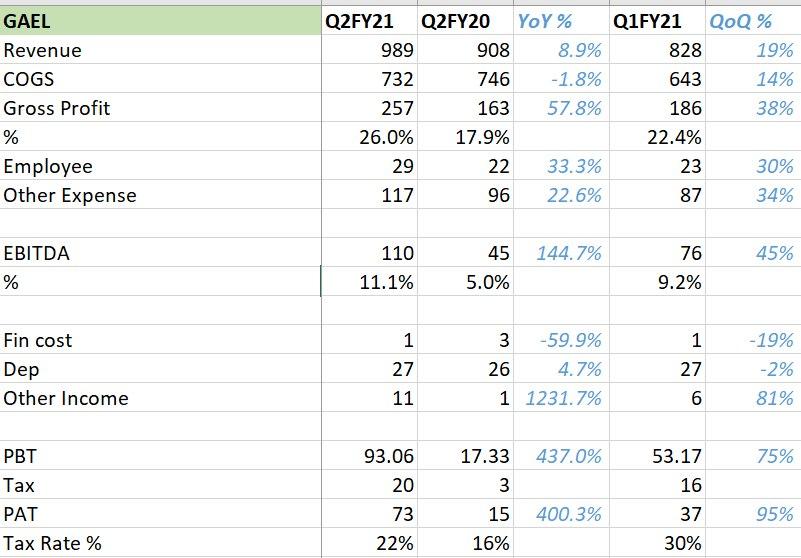

The Company has come out with probably best Q2 nos. in many years. Expecting equally good Q3 & Q4 nos. and Net Profit to cross Rs. 200 Cr in FY 2020-21.

9 months profit is already 50% above 12 months profit of 146 cr. in 2020.

Improvement in margins by ~3%.

Expecting at least 75 cr. net profit in Q4, will double the EPS to 12 v/s 6 in 2020.

At PE of 15, the share price should cross at least 180 by results in May.21, a 40% jump in 4 months.

At this stage, stock price down probably indicates signs of desperation by traders for not accumulating enough !

It is a fundamentally stable business and will grow with new plants in newer areas / expansions from internal accruals.

EBIT has doubled in Maize processing division - with good margin expansion.

New plant for maize processing, in Malda once completed should further increase mkt share.

Q4 Results for GAEL declared:

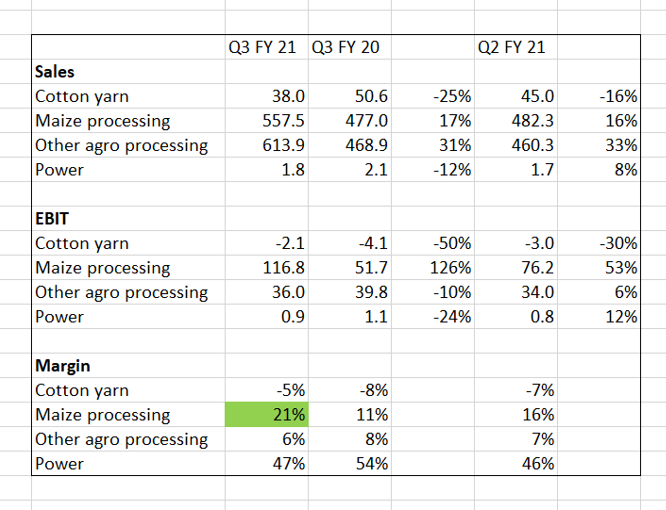

Maize segment’s EBIT margin at healthy 18.4% (though dropped from 20.9% QoQ)

Agro Processing has generated an EBIT of 80 Cr and textile has turned back into green.

Revenue flat, EBIT has doubled. (Maize price hike issue in last FY). Margins at 18% - highest in last 5 years. Business back on track after a blip last year. Planned capex in Malda (likely completion by year end); should increase revenue by 600 cr, as per guidance given by mgmt. CWIP of 106 Cr vs 12 Cr.

AGRO PROCESSING

2016

2017

2018

2019

2020

2021

Revenue

1488

1847

1760

1901

1667

2578

Rev growth

10%

24%

-5%

8%

-12%

55%

EBIT

10

81

130

72

69

165.2

EBIT growth

-371%

672%

60%

-45%

-4%

139%

EBIT margin

0.7%

4.4%

7.4%

3.8%

4.1%

6.4%

Segment has sprung a positive surprise, surpassing maize with higher contribution to overall revenue. Healthy growth in revenue and EBIT.

Cotton Yarn

2016

2017

2018

2019

2020

2021

Revenue

172

220

258

240

169

162

Rev growth

-4%

28%

17%

-7%

-30%

-4%

EBIT

-14

7

-7

-8

-13.4

0.71

growth

-12%

-150%

-200%

14%

68%

-105%

EBIT margin

-8.14%

3.18%

-2.71%

-3.33%

-7.93%

0.44%

Muted numbers, though EBIT has turned into green after 3 years