In my view very good results. The only concern in the past so many years has been cyclicality of business. Ethanol production from crops other than sugar cane can be one more set back (not sure how this will play out) as Maize availability and pricing drives the profitability for GAEL.

Company should organize quarterly con calls as very little information is available outside the ARs or few brokerage reports. Annual report for FY21 is still not uploaded on website. The website itself needs new age designing.

My rough notes of AGM for FY21 (there may be some mistakes!):

Maize processing Capacity – 3000 TPD; after Malda – 4000 TPD. Current Market share – 22%; After Malda, expected Market Share – 28%.

Current installed capacity for Sorbitol – 100,000 TPA; CUF = 75%.

Exports

Exports not led by a specific product but generally from a large array of products.

Low RM Prices – Corn prices have been moving in India against the international market due to pandemic and because of bumper crop. Generally, India corn prices are higher than internationally; in the last year, it has been in tandem.

Rupee depreciation has also helped in better realization.

GAEL is the largest exports of corn and derivatives from India. Competitors in International markets for exports – Cargill, Rocket, ADL, etc

International corn prices have increased significantly and now India is at par on FOB basis with all other countries.

Why are other countries cost competitive in edible oil - India is a net importer of edible oil (15 MT) and climatic conditions better in Brazil, Argentina, US for oil seed production.

Don’t expect any stoppage of exports (while there can be volatility) – we are well spread out internationally for exports market and are supplying to 75 countries.

Value added Products form 25% of the Maize division sales.

Margins

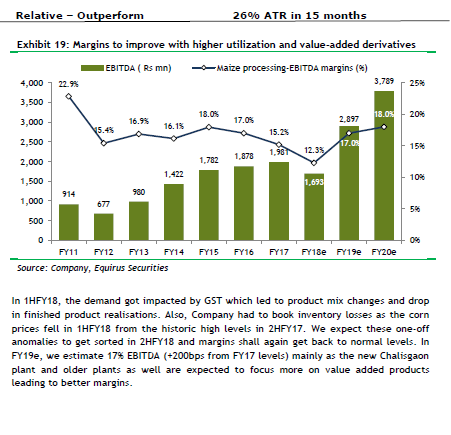

Maize spread increase – a) unprecedented demand from overseas leading to higher margin b) share of value added products has increased.

Maize EBITDA have varied between Rs 3.6 to Rs 6.3/kg and can be expected to be at mean of these numbers.

ROCE /IRR for Greenfield capex – Generally consider 20% return on capital for implementation of new projects.

Maize outlook – Had a good Rabi crop and expect good Kharif crop also. India should harvest good crop inspite of lower monsoon as corn is spread across in many states.

Production of derivatives has started in Chalisgaon.

Maize division – 85% operational efficiency (scope to increase to 95%)

Update on HFCS – We are in the last stage of approval from FSSAI. With sugar mills’ more emphasis on Ethanol, HFCS looks very promising product and expect to start production in first half of 2022.

Guidance for next 3 Quarters – poised to increase CUF.

Soya bean crop is good – Sales and profitability to increase. Demand for Soya bean (no-GMO) meal is very high.

Quarterly concalls – few investors have requested. Will look into this.

Ethanol – Company has already applied for 3 licenses for Ethanol; it would be much cheaper cost compared to grass-root ethanol manufacturer (and therefore competition would be less). It would be a forward integration for us. Company has applied for licenses (Chalisgaon license expected in Q2 and other two in FY22). Three plants of 420 KL (120, 180, 120) in next two years.

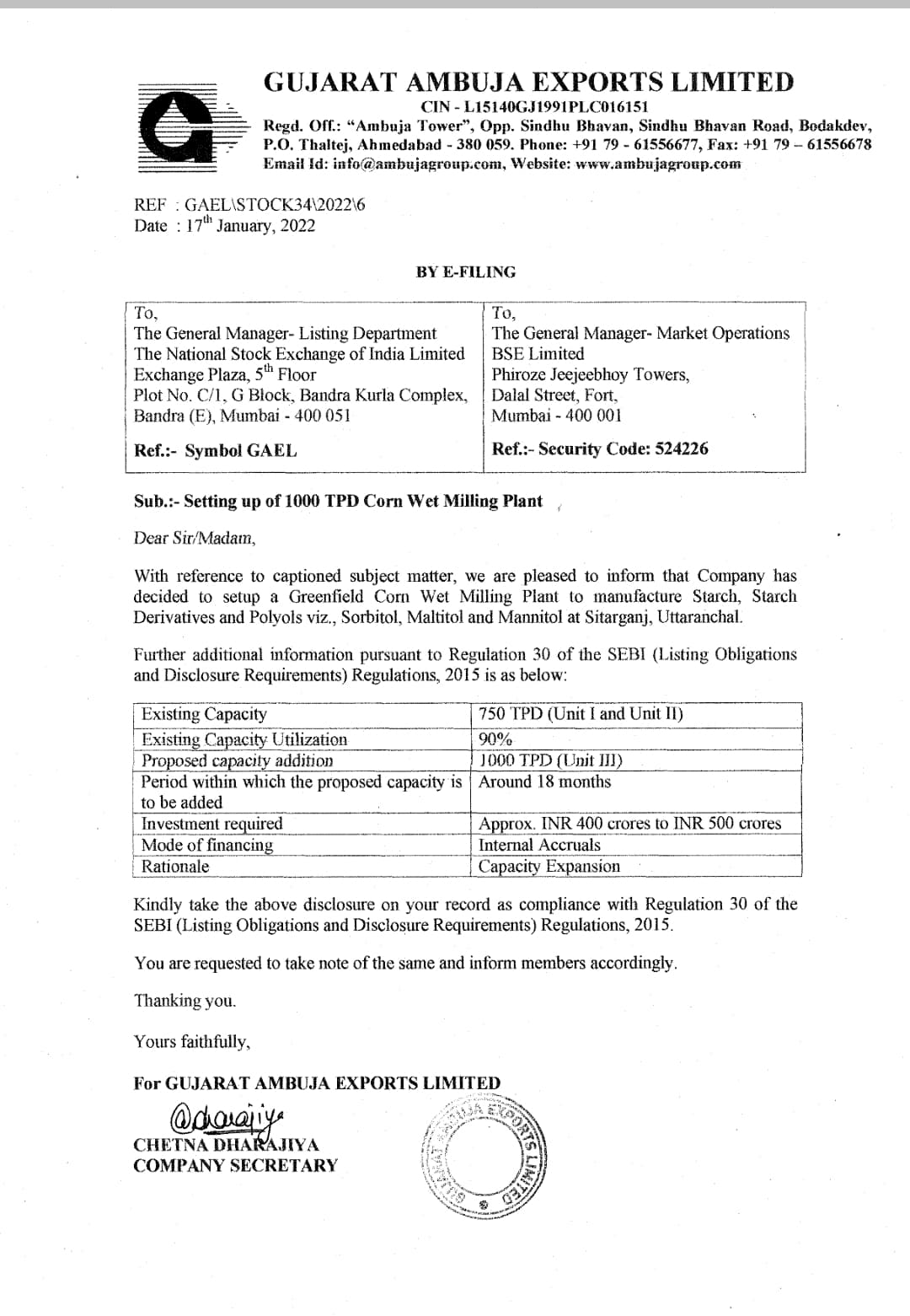

Malda project delayed due to pandemic – expected commissioning in first half of 2022. No further delays expected.

Expansion

Aim to reach to 6000 TPD in maize in next three year (2024) through Brownfield and Greenfield projects.

Adding two more sorbitol plants in next one year – Hoogli and Sitarganj, which will take the capacity to 160,000 TPA and will be sufficient for next 5 years.

HFCS

Ethanol

Pollution issues – there is no problem (some news articles had cropped up in the past due to vested interests).

We will look to absorb all the incremental growth till 2025.

Raising equity capital is only an enabling provision for expansion (6000 TPD maize, Three ethanol plant, HFCS at one location initially and then at other locations) and there are no concrete plans to raise capital. We would try to remain debt free and try to grow through internal accruals.

Although they mentioned that raising equity is just kept as an option, however, their current capital allocation seems strange. With so many expansion plans planned ahead

Why are they investing such a huge amount in Bonds ? Found below snapshot in Annual Report 2021

Doesn’t it require approval from Shareholders when your salary as %PAT is increasing every year?

Please let me know in case my understanding is incorrect

True…as a percentage of profits, his salary is indeed high. However, and this is just my two cents…

GAEL was not present in maize processing about 15 yrs. ago. Once Malda comes on stream, they’ll probably own more than a quarter of the market. Even today, they have no option but to go for value addition. Incremental growth is unlikely to yield results as a “pure play” maize processor. Most of this transformation is thanks to Mr. Gupta.

This, of course, is key man risk…and so on. That’s the beauty of investing in smaller companies.

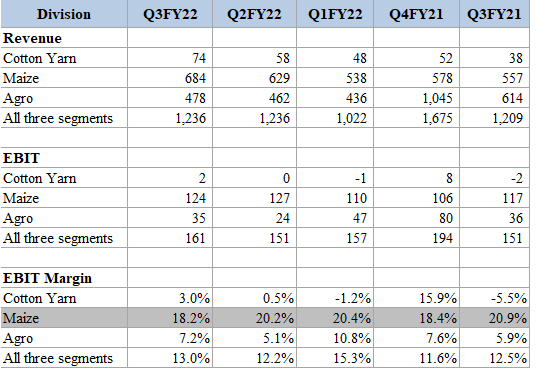

But if you notice the maize processing has grown 1850 cr in 2019 to 2600 cr in closing of fy 22 and margin improvement on ebit basis from 13 to 18.

Also the agro sales has reduced with 7 percent ebit margin yarn has slightly turnaround.

important thing is free cash flow of three years at 780 cr and operating cash flow for three years around 1100 cr cash in hand 450 cr investment around 170 cr nil debt.

At fy 22 net profit 440 cr an roe of 21/22 percent on a approx reserve of 2100 cr. With an eps around 19 even at earing yield of 7 percent price comes to 271 so the present price gives ample discount.

Overseas investor MIT has consistently increased it stake upto 1.52 percent

If gulshan poly can trade at 18/19 Pe there is a scope for pe expansion

Not a bad entry point even on technical chart even though I don’t consider it

hello anupam

since you have been tracking gael for a long time can you please throw some light on the corn price movement and the opm margin since 2021 has shown above average margin is it related to sudden jump in corn price now in 21/22 we can see margins decreasing in maize due you feel ebitda 18% margin in maize is sustaintable or i should work with 13/15 ebitda margin. your reply would be highly helpfull thanking in advance

regards

kumaresh

Thank you very much any idea on the capacity utilisation levels and since there is always a doubt about HFCS usage because of the health problems will it be of any meaningful addition

Fssai has listed sucrose as an approved additive for sweetner

Is the corn price movement and margin has a historic co relationship

I am not aware of the CUF - Management had indicated that they are poised to increase the utilization factor in the next 3 quarters. Insofar as HFCS usage is concerned, do not understand what are the incremental health issues between HFCS and sugar.

Have been tracking this stock for ~3 years and had started purchasing in 2019 & 2020 when there was severe shortage of maize driving down the margins substantially but I understand that this was an extreme situation. The margins in the Maize business have steadily increased.

I tried to summarise and explain the GAEL business in a One-pager note. Try to collect from various sources and try to make to simplify the business in layman terms so that someone gets a jist of the company.

Taken some points from this thread, some from Starwart Advisors and whatever is available in the public domain, Hope this will contribute to your thesis and develop a broad understanding of the business.