Can you please let me know from where do you get their plants utilization level details .

in public domain https://www.ambujagroup.com/wp-content/uploads/2018/12/Green_Field_Plant_Update-14.12.2018.pdf

Any idea how Sukhjit Starch was able to improve margins last quarter inspite of high maize prices which impacted GAEL?

Tracking QoQ margins for these businesses might not make sense as I think they have to book inventory loss and gain. Over the FY it usually averages out but QoQ there should be volatility depending on inventory gain/loss.

1 Like

Hi

This is my understanding of their business model

They buy RM in bulk , so get it at a better price compared to competitors. This gives a good advantage for Gael. What I don’t understand is why is the competition not following the same sort of process

What are they doing differently compared to its competition. I believe other companies in the same industry is highly leveraged

They are able to buy large amounts in one shot due to their balance sheet strength.

They have pan india plants that are close to maize producing regions this further decreases their logistics costs both inward and outward to customers.

They are setting up a new plant in Malda and this should help cater to the eastern part of India. They are managing to do all this without resorting to long-term debt. All debt is mostly backed by inventory as they purchase bulk at once.

They have gone from 0 to to what they are in maize in 10 years and have done it only with internal accruals. This has occurred in an industry where all big competitors are mostly struggling.

The starch derivatives industry is sticky in nature. Since they form a part of critical items like infant food, usage in pharma etc: quality is a big deal for their clients. And this forms less than 1 or 2% of the cost of the product so customers may not want to switch even if a competitor offers the product slightly cheaper. Further it takes a long time for a new vendor to get approved by such clients is my understanding.

As a business they seem to be way ahead of the rest in the industry.

8 Likes

Poor Results it seems…

Commodity as raw material could bite seriously unless company has pricing power.

If raw material jumps by some 80% in such a short period of time (as per SBIs report) it is impossible for even a company like asian paints to pass on costs in two quarters let alone 4 quarters!

Gradually it should be passed on. However, if it is not passed on then I think the entire starch derivatives industry is a commodity business. As of now I do not believe so due to the nature of the product and historical margins maintained in maize. (same can be found on Stalwart’s reports)

1 Like

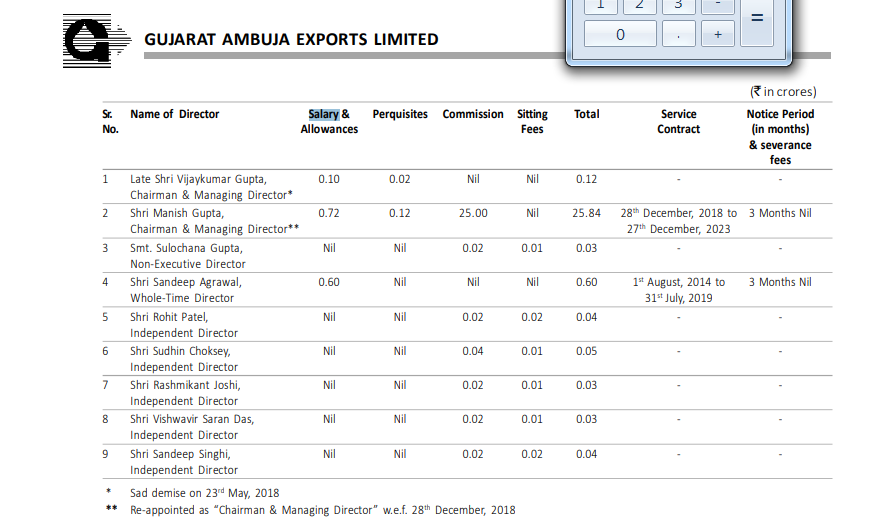

In 2018, Promoter Father & Son were drawing Salary of 6 Cr and 18 Cr respectively.

In 2019, as father is no more, son(Manish Gupta) simply adds all father income into his income and now stands at 26 Cr.

Here is the screenshot of the Annual Report:

1 Like

| 2016 | 2017 | 2018 | 2019 | |

|---|---|---|---|---|

| NPAT (in Cr) | 100.00 | 159.00 | 180.00 | 198.00 |

| Commission to MD (in Cr) | 12.00 | 18.00 | 23.00 | 25.00 |

| Commission as % of NPAT | 12% | 11% | 13% | 13% |

Just did a rough calculation and you can see that the percentage of commission to Net profit after tax is constant atleast for past 4 years. Therefore not a big negative I would say. Although it is on a higher side, the remuneration seems to be linked to his efforts.

2 Likes

1 Like

Had attended Gujarat Ambuja Exports Limited’s AGM held earlier this month. Here are my rough notes:

- Corn prices were stable till October 2018 and then started rising due to early reports of crop failure in Andhra Pradesh due to infestation of army worm

- MSP of Maize was increased to Rs 17 from Rs 14 last year by government

- GAEL was able to import because of the license – 100,000 tonnes were imported

- Sowing was 59 million hectares last year and it remains the same this year (sowing in Karnataka is down 10%). MP was the largest producer last year and there has been increase of 10-15% sowing this year.

- Company believes that this level of pricing (Rs 23-24) is not sustainable as the poultry industry will be unable to afford the same.

- Government has opened a separate HS code for corn, pop corn and feed corn. Starch industry would be allowed to import (for export).

- If import prices remain at Rs 17-18, GAEL would be competitive based on current prices of starch in international markets.

- Soya bean – 11-12 MT expected this year – good crop expected based on sowing.

- Soya - India would continue to benefit from US and Iran tensions as food items are allowed under rupee trade agreement.

- Starch/Starch derivatives - First half the exports would be subdued and in the second half of the year, they are expected to go full steam clocking in at least what was done last fiscal (Rs 1,200 cr).

- Challisgaon Plant Utilization is 70-80% and derivatives production would start in October 2019

- Rationale for putting up plant in the eastern part of the country (Malda):

- Water supply (ample supply of water)

- Raw material availability (very close to corn producing states)

- Sales in the region

This plant would act as a hedge in case there is a problem in any of the points mentioned above in other regions. Gujarat and Maharashtra were heading towards lesser availability of water until the rains picked up.

- Corn Steep Liquor (CSL) is a big source of pollution for the industry. Now, GAEL has started to generate fiber from this liquor; plant had started 3 years back. Earlier CSL was being used to produce power – now, fiber would be sold in the market which has better realization. Last year 40% conversion was achieved and this year 80% of CSL would be converted in the next two years across plants; this would reduce load at effluent treatment plants. GAEL has been a pioneer in adopting this practice.

- FMCG – supplying to all top tier players. Every contract has age of 6 months to one year. GAEL’s share in FMCG market is 30-40%.

- Glucose - Either demand has gone up or capacities have closed down. Not seeing any capacity expansion is next 2 years because of increase in maize prices.

- Water consumption is a big risk for the industry and the company keeps a close watch on the source of water; water requirement for glucose is higher than that of starch.

- HFCS – It is in final stage of approval. However, the product would still not be viable vis-à-vis sugar because of the price difference. In 2-3 years, it should become a reality; sugarcane consumes 5 times more water. Maize production to increase to 80 million hectares (against 60) replacing land for cotton/soya/pulses/sugarcane. Therefore, availability of corn would not be a challenge. The plant is flexible wherein last mile equipment can be added to this unit to convert sorbitol plant into HFCS.

- Malda Plant plan

- First phase: Starch and Glucose

- Second phase: Derivatives (till this plant is commissioned Chalisgaon plant would take care of derivatives)

- Capacity: 750 Million Tonnes

- Company has sufficient land to double the capacity at existing locations

- If corn prices continue to remain high, there would be lot of closures

- Starch prices were Rs 20 last year and it would be difficult to ask for Rs 30 straight-away this year and therefore a temporary hit would need to be taken; this would go a long way in creating a sticky customer base

- Long Term Plans

- Looking at M&A opportunity outside India where corn can be sourced at a lower price

- Like to preserve cash to get through the difficult times

- Forward integration – starch and soya

- Branded products

- Import Duty and International sourcing

- Import duty in India for corn is ~55%

- International corn prices are $230 while the prices are trading at $320 in India. If prices in India continue to inch up then the duties will have to be reduced (otherwise the output prices would become unsustainable and would hit industry hard). Going forward the import duty might be reduced.

- Last year, under the export scheme the company imported 100,000 Tonnes of the total 140,000 allowed.

- The reason for getting high prices for derivatives is that only few players are approved by customers

- Textile segment: No sentiments not to dispose off the asset; Company is also evaluating whether employees can be given VRS and the unit is closed down instead of burning cash year on year. No incremental capex on textile planned.

Disc: Have a tracking position on the stock

20 Likes

Due to excess rain and flooding, farmer lost their crop. How much impact will be on Maize and Soya which is the main raw material for GAEL and Avanti Feeds?

GAEL 2QFY20 Results is attached.

2019 Nov. - Q2 Results GAEL.pdf (2.0 MB)

Half Year 2019 - 2018 comparison (% of revenue)

-

Revenue increase Rs. Cr. (1923 vs 1587 ~ +21%)

-

PBT - net impact is -5%

a) Expenses : -5% (increase)

(Inc in cost of material consumed 5% & inc.in stock in trade 6% compensated by decrease in emp.

cost by 1%, dec. in finance cost by 0.5%, dec. in other cost by 4.5%)

b) Tax impact : +1.5% (decrease) -

Net Profit : -3.5% (decrease)

Key take away

a) Cost of procurement has gone up only marginally.

b) Availability of raw material Maize should not be constraint as good sowing & no threat of Fall Army Worm.

c) H2 sales is normally 20-25% above H1.

3 Likes

Quarter December 2019 results.

Hi,

What’s the view on company prospects as maize prices have corrected to Rs 13 - 14 level. Company is generating cash, has strong balance sheet and is moving towards building brands as well.

Disclosure - Invested since 2014 and adding slowly

2 Likes

The valuation looks mouth-watering to me:

The Current Market Cap of the GAEL is INR 1,350 Cr when the Company has 600 Cr worth of inventory, 100 Cr cash and 20 Cr of Net Receivables. Adjusting 150 Cr of ST Borrowing, the Net Current Assets of the Company are itself at 570 Cr. So, the company is available at an Effective Market Cap of less than 800 Cr with about 400 Cr of EBITDA in a normal operating year and has no long term borrowings.

The Company has healthy balance sheet and would hopefully be able to gain market share in the maize segment when at least some of the competition might not be able to survive this downturn.

Disclosure: Invested

6 Likes

GAEL stock split announced -

GAEL - Stock split.pdf (59.0 KB)