Blogpost on greaves cotton

During a recent Bloomberg-Alpha Ideas Investment meet, I covered this stock for discussion purpose only.

Shared here for review and perusal of Valuepickr visitors. Greaves Cotton.pptx (3.0 MB)

10 Likes

How will the share reclassification affects retail investor. I could not understand much. As of now we have 24,42,06,795 shares of face value 2.00 each.

BSE filing.

Buyback:

The last update I am seeing is below

"This is in furtherance to our intimation June 27, 2019, wherein we had submitted a copy of the Public Announcement dated June 26, 2019 pertaining to the Buyback.

The Company has received interim observations from SEBI in regard to the draft letter of offer filed by the Company on July 4, 2019 and is in the process of addressing them.

In light of the proposal to introduce a tax on distributed income by listed companies undertaking buyback of shares, vide the Finance (No. 2) Bill 2019 (introduced in Parliament on July 5, 2019), it is hereby submitted that the Company has filed before the Ministry of Finance and SEBI seeking clarifications and certain relaxations with respect to the Buyback."

Now buyback tax for those buy back announced earlier withdrawn, I am interested to know the fate of this buyback. Any one knows?

Date of opening of Greaves Cotton buyback is Oct 18, 2019 and date of closing is Nov 1, 2019.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/19a3c25b-f227-4501-bc2a-300c57da828b.pdf

The eligible buyback candidates who can participate are ONLY those shareholders of the Company which are on the books as on the Record Date, July 12, 2019

Disc: Not invested

Recently Ampere vehicles has partnered with Bounce(App based bike service in few cities) to provide electric scooters at metro stations. The scooters come with battery swapping facility and bounce has tied up with some kirana stores where charged batteries will be available for swap. It has started in Bangalore and Hyderabad, plans are to start in 5 more cities in November.

See the tweets:

If ampere supplies more scooters to bounce, it will provide them good volumes and also give visibility on streets to people.

Disc: Invested small amount.

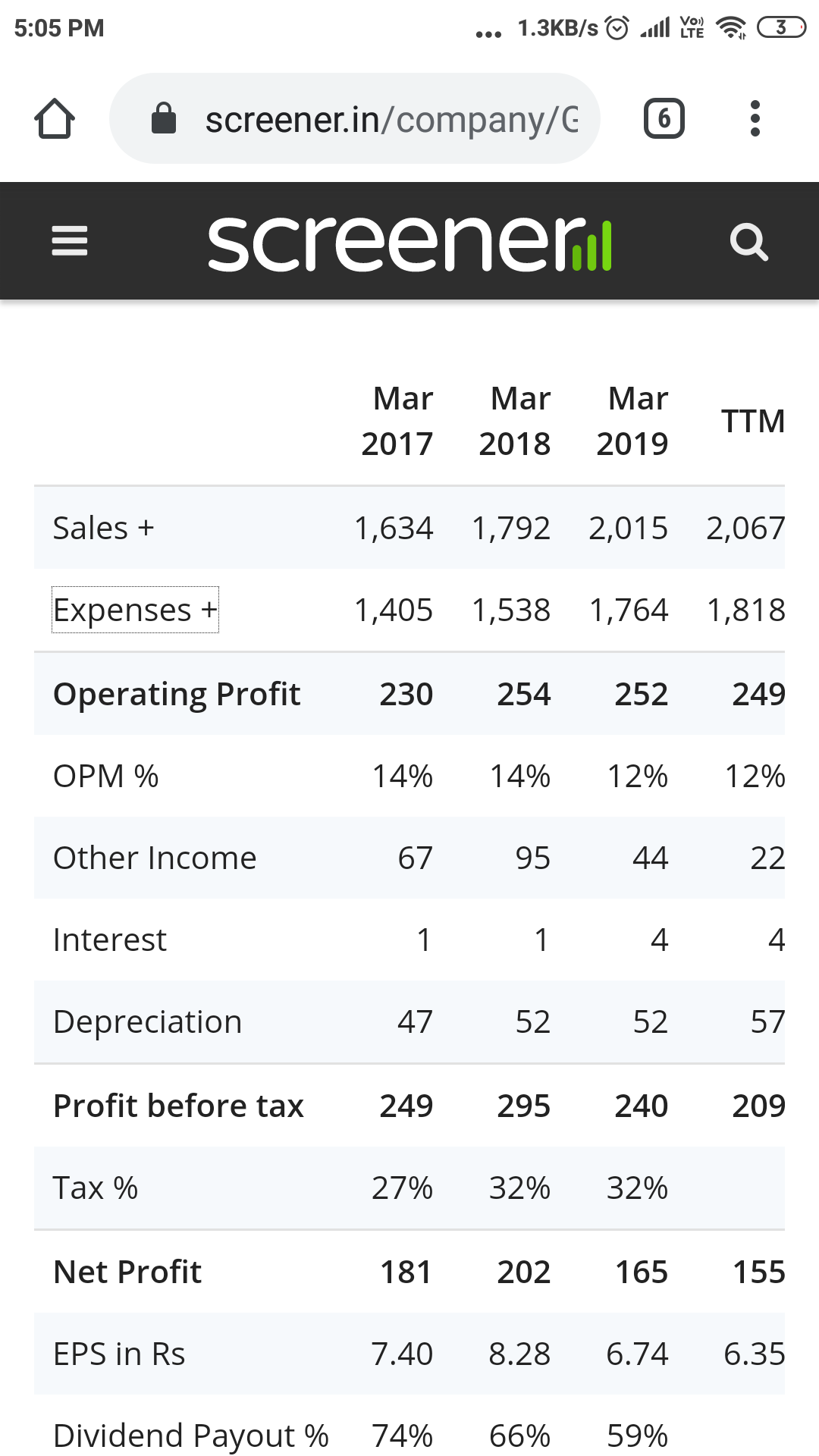

the sales for the last few years have been absolutely flat, Q2 FY 20 results are also in same line. Flat revenues but increased working capital cycle, lower ROCE and poorer in all ratio’s compared to last year as well with Q1 FY 20 results. Ampere is posting EBITDA loss which i feel with more penetration they will be able to make up. what is worrying is after change in management in the last couple of years and lots of effort in trying to improve the products as well as entering in newer segments, results are not that attractive. The only positive seems to be the effective tax rate is now ~24% compared to ~31% .

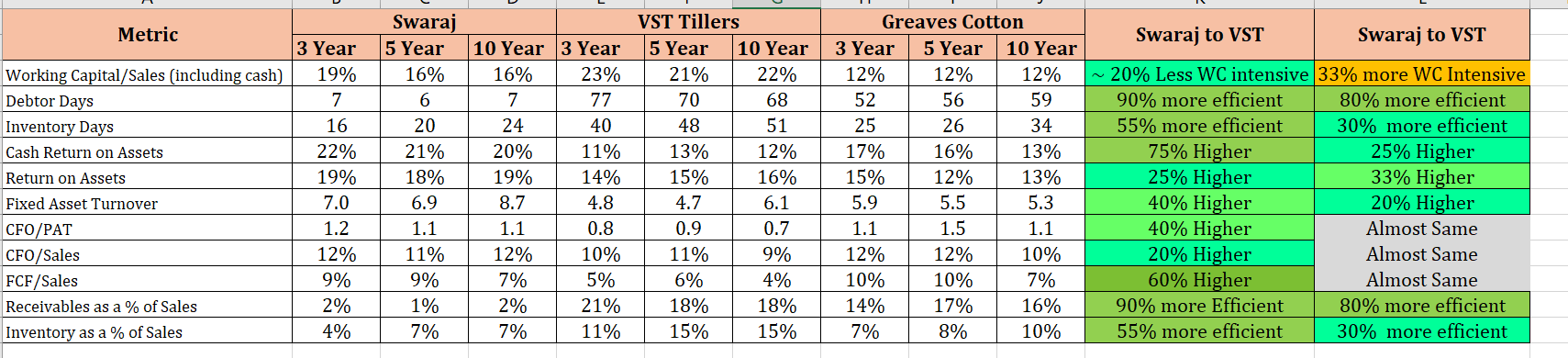

Can you put some numbers to substantiate the same ? At least on operational efficiency front n sales growth front, last time i analysed an year back, it looked relatively improving. Profitability had many other complications . Attaching some data below which i had analysed to compare few companies including this one (though these r not exactly in same business but similar ) n saw Greaves improving in last 2-3 years since new mgmt took over.

Sales is also up from 1600 to 2000 in last 2-3 years after a long stagnation. Of course, m not measuring things quarter to quarter n even if doing that , we should look how whole industry has done with the cyclic auto slowdown for last 1 year.

Hi i just went by the companies presentation. and there seems to be no great growth in any of their product categories whether its in Engines or Agri business segments. So they seem to be focussing on E-Vehicle. we need to see how it pans out.

54.81% is the promoter holding now after buy back, up by another ~ 3 %.

Before buy back the promoter holding as below on Sept 30th.

Disc: Tended shares for buyback and exited remaining holding for better opportunities.

Does the Government push towards EV have any positive impact on the company?

Greaves Cotton Q3FY21 Concall notes

- New business contribution has led an overall increase of 25% of the overall business, and we continue to evolve through these measures to become a future-ready organization.

- We did see growth rebound despite sustained weakness in the 3-wheeler shared mobility industry. Our overall engine portfolio, which is, of course, both auto plus nonauto, did see an upward momentum. Obviously, auto was down. We have invested heavily in creating robust EV ecosystem in terms of people, process, technology and the scaling up.

- Automotive business

- In the auto business, the cargo segment did see relatively good growth due to the last-mile mobility, pickup in economic activity and e-commerce. We see a revival coming – in the coming quarters, and we see good growth potential in the balance part of the year. We aim to drive profitable growth.

- We have a strong product offering to our OE partners. Our BS-VI engine has performed very well in the market. We have secured long-term contracts with some of the major OEMs. We have also signed up with some international OEM and will announce it at the appropriate time.

- Structurally, we have talked about cost reset. We have looked at 2 plants. We’ve gone down in terms of the plants, and that is a permanent structural 10% cost reduction. We have closed the manufacturing facility in Ranipet, and we have started moving our engine operations to Aurangabad from Pune. All this will lead to optimization of resources, cutting off unnecessary expenses and making our operations much more efficient.

- We have signed an MOU with both the domestic and international OEM. And we will make the announcement at an appropriate period of – appropriate time. But the sales of these vehicles will start in a year, 1.5 years’ time. So that is what we can announce at this point of time.

- CREST, as I mentioned, the CREST engine, the basic principle of the engine is still valid. It gives us a new technology, and the technology itself is much more efficient than the conventional engines. One thing also I would like to mention to you, yes, the waiting period has been long, but the engine is a little bit ahead of its time. And therefore, when the fuel efficiency norms – or stringent fuel efficiency norms come into play, this engine will take a lot of traction. And that is the reason why you are seeing a little bit of a delay in the certification of this engine. But we are very, very optimistic about the capability of this engine.

- Yes, we have been hit by the material cost by – because of aluminum and steel price increases. But all our contracts with our key customers are indexed with the commodity pricing. And therefore, any increase or decrease in the commodity price is automatically addressed.

- In the genset segment, while the industry grew somewhere around 3%, our business grew almost 17% in Q3 over corresponding period last year. And our focus on the smart genset is helping us gain significant traction with the customer base.

- On the nonauto side, the other 2 important growth levers around the nonauto engines, which we have been talking about as an important diversification to our single-application 3-wheeler engines, has been growing fairly well. The nonauto engines grew almost 44% in Q3. On the light equipment side, the business grew more than 26%.

- In the aftermarket segment, we have experienced the volume has come back to pre-COVID levels, and we foresee a robust growth.

- Electric Mobility

- On the electric mobility side under Ampere, the business continued its strong performance and delivered almost 2.25x growth over quarter 3 last year. In terms of absolute numbers, the business has achieved, in 9 months the 12-month performance last year, and this is despite the impact due to lockdowns.

- Ampere today has over 300-plus dealerships. And like Nagesh mentioned earlier, almost 80 of them have been opened since the unlock process.

- So the traction remains very strong. The demand remains very strong. Our product range, which was refreshed during the festive season and including the new product launch on Magnus Pro, has been giving very good results, and there’s a very strong and positive customer feedback in these areas.

- Also, to prepare for the future, we are also looking at creating an EV mega site in Southern India, which will help us meet the accelerating demand in the market.

- So we did INR 60 crores of revenue in the third quarter for the e-mobility as a group – Ampere group, that’s including 3w. first half revenue was around INR 42 crores. compared to last year, there has been 126% revenue growth in e-mobility, and that is going to continue as we move in the next financial year.

- if I may also add, the product mix is also helping as Ampere moves towards higher technology, lithium-ion-based products as well as higher-speed portfolio. Especially with the launch of Magnus Pro high-speed scooter, that positioning in the high-speed segment has improved considerably so – which is helping Ampere.

- the high-speed mix is now gradually inching closer to almost 50% of our portfolio. This was – and it was only last year when we started entering the high-speed segment, and it’s already close to 50%. And similar is the story on lithium-ion, where Ampere steadily has moved beyond the lead acid-based products into the lithium-ion products. And we expect this trend to continue, with Magnus Pro gaining more strength in the market.

- So today, if we look at it, I would say that close to 20%, 25% of the sales would be coming from the Greaves Care network, and the remaining sales are coming from the Ampere-dedicated network. And going ahead, we will continue to leverage our complete mobility ecosystems and work on it.

- As the battery prices are reducing, what we have done is, a, we have partnered with certain strategic partners in India so that the battery is locally sourced. That is point number one. Point number two is while maintaining the prices, we are also focusing on localization and better-quality partner for the nonbattery-related products and components and improving the product value proposition in terms of giving a higher range. So at the same price, now the products are giving 10% higher range. So that’s how we have been approaching this segment.

- So the vehicles, the Magnus Pro and some of the higher-end vehicles are configured for taking faster charge. Having said that, 2-wheelers as a segment is not constrained by the charging infrastructure because it can be charged through conventional charging points in 4 to 5 hours for a lithium-ion battery. So it is not a constraint. But for customer segments who want a faster charge, our products are configured for faster charging as well as swapping as the case may be.

- Now another customer segment is the entire B2B customer segment, where people are using electric mobility for the total cost of ownership advantage. In that segment, we have now 50-plus B2B customers, and there are regular repeat orders from customers where the vehicles run in a fairly heavy use conditions of 100 kilometers plus a day. So the vehicles are able to withstand the use and abuse in the B2B segment, and the horizontal deployment on the retail products also in terms of reliability is helping. Now today, we have almost 75,000-plus retail customers, and the number is growing fairly rapidly.

- Software Capability of E vehicles.

- The software capability becomes important as the products – the next-generation products, which will start coming in, will have smarter connectivity features. And Ampere is also working on building that capability, both in-house as well as through smart ecosystem partnerships.

- And there are certain critical technology areas which we would be investing behind and building significant capabilities.

- And as we go ahead in the next-generation products, we will add more software and connectivity features on our scooters as well.

- If you see with Magnus Pro, we started some initial features around – we had certain software control features like hill assist, which were relatively new in the industry. We came up with a renew feature, which – limp home mode, which was in the last – a few percentage of the battery, the product goes into a power save mode so that it can give additional 10 kilometers of range to the customer, which addresses the range anxiety concerns that the vehicle should not stop in the middle of the road.

- So some of these, we have already started building in, and we’re actively working towards further improving the customer experience through software and connectivity features.

- The cash and cash equivalents, we had INR 212 crores of cash and cash equivalents as on the 31st December 2020. And the strong working capital management has worked very well in the COVID times for the company. Our net working capital days have reduced to 26 days. That is almost 7 days of reduction in the last 9 months.

- CapEx, run rate continues to be on the same rate of around INR 12 crores to INR 15 crores a quarter. So that’s going to continue on our CapEx front.

- So as we are restructuring the group and consolidating at central locations, there are exceptional costs incurred for the moment. So in the quarter, we had a total exceptional cost of around INR 9 crore on the cost side, and we had a gain of around INR 4 crores. So net impact in the quarter was INR 5 crore. in terms of next financial year, there will be some exceptional costs, which will come until maybe early part of the next financial year when we shift our – one of the plants that we are consolidating in the Aurangabad further. So most probably by the first half of the next financial year, we will – after that, we will not see any exceptional items

Regards

Harshit Goel

13 Likes

At what % do you guys see this business growing in the next 3-5 years?

Ola plans to invest $2 billion in TN two-wheeler factory - The Hindu BusinessLine

Seems like there are too many players entering the market as it has been touted as the next big opportunity. Ather, Hero, and now Ola with other smaller players also in the fray. Even though Ola’s hopes of selling 10 million vehicles is really amusing and is more like a desperate attempt to pivot from their loss-making aggregator business and justify their high valuations to VC’s. Still, Ampere can be at a disadvantage compared to both of them as both the companies are flush with cash. Hero makes a lot of cash every year(3500 cr approx) and also is a leading investor in Ather. Meanwhile, Ola has a lot of cash available to burn and can probably raise money again from VCs. Also, Hero has a stronger brand name, distribution network, supplier trust, etc which has come from being in the business for many decades. This gives them some advantage over Ampere.

But the good thing is that it is not a winner takes all market and being at worst the 5th or 6th biggest player in the country can most likely rake in good profits for the firm in addition to profits from their old businesses. The thing that can work for them is the huge addressable market despite being insanely competitive. But, Predictions are difficult at this juncture.

What do you guys think about the competitive landscape of this industry?

Disclosure: Hold tracking amount. Interested

1 Like

I agree completely with your assessment. This reminds me of California gold rush analogy. Someone would find gold, but would everyone find gold? Such competitive intensity can make it a race to the bottom (pricing wise). Without any edge and large marketting budgets, it’s difficult to see profitability. I did study greaves cotton last few concalls and the latest annual report, it’s a great business with innovative nature (look at their latest 30% improved efficiency engine CREST. They are clearly innovative. But are they innovative enough to create a differentiated product where they do not compete on price? If not, value creation might not happen despite high growth.

Continuing the California gold rush analogy I think important way investors can benefit is by tracking the value chain and understanding competitive advantages if any. From the ola announcement, it looks like they would make their own motors. So looks like greaves cotton cannot provide value in that value chain. Would greaves be providing engines to hero, ather or any other large players? I think these are the key questions to understand future value creation potential.

Reference video on California gold rush analogy and how it appllies to investing :

5 Likes

Totally agree with you. This gold rush reminds me of what happened in the Indian paper industry a decade ago. Almost every company put up huge capacities in anticipation of growing demand. Everyone was doing CAPEX because everyone else was doing it. Many things went south, as they usually do, and many players were forced to shut down or bear huge losses. I don’t think the same thing is going to happen in this sector at that scale as both industries are structurally different but there is a strong possibility of similar oversupply and price wars which may force some competitors out.

India sold around 17 million 2W vehicles sales last year out of which Hero sold around 6.7 million with Honda and TVS at 4.7 and 2.4 million each. Ola plans to make 10 million at their plant annually. While not expecting them to have this capacity in a few years, but Hero, Bajaj, TVS, Honda, Ather, and other players are also going to come up with good capacities pretty soon when demand starts to rise. But the older players seem a little more cautious considering they are probably waiting for electric infrastructure to be set up which may spur up demand.

Understanding the value chain and seeing where they will have an advantage if any, will be key. I think it comes to more speculation territory when analyzing where competitive advantages of Greaves will lie as the market hasn’t developed yet and the future can go either way. Greaves can use Greave’s retail and Greave’s care centers to provide additional value to consumers but most competitors have a wider reach on these fronts than them.

I guess in the end, a lot of how it plays out may come down to the management and their execution skills. The previous couple of con calls were impressive and management does seem innovative and efficient capital allocators. But sometimes, even the smartest of managements fail due to unfavorable industry dynamics. It will be interesting to see how this plays out. This is a kind of company which in addition to value creation, it can get also get a huge PE rerating and become extremely overvalued for a long period of time as it has all the elements of a growth stock story. Having said that, It may take some time for a clearer picture but the price of clarity is expensive in the markets.

4 Likes

- EV 2W set to be cheaper than petrol 2W.

- GST on EV 2W is 5% vs 28% on petrol

- Running cost of 100 km EV is ₹9 vs ₹250 for petrol bike

- Incentive increased from Rs 10,000 per KW to Rs 15,000

- Ampere from GREAVESCOT gained Market share in FY21

https://twitter.com/amitabhvatsya/status/1404102428916523008

Adhiraj, AS you said old and Hero have lot of cash to burn on this segment , to add to this Greaves also generating cash from the core business, Believing the core business will one day come to an end as the whole engine making sector will come to end when All become electric.

GReaves is also investing and there complete focus on EV what I feel.

very well said that what market share the topper will take , Greaves will be part of it, Recently there have been 70 % growth from this segment of there business, Read an article on this , Google it you can find this.

Over all I remain bullish on this Stock.

Yup, both of them generate cash. But the cash generated by Hero is higher(by multiples) than one generated by Greaves. Hero earns around 3000-3500 Cr per year whereas Greaves earns 150-200 Cr per year. There is simply no comparison. Hero has a better brand name, distribution network, customer recognition and trust. Also has a huge stake in Ather. Also, it seems oil driven two wheelers will take at least a decade to go out of trend, and demand for electrics won’t likely go up exponentially as most people envision.

I don’t mean to say that the company won’t do well. But for it to do well, management has to do extremely well.

The growth rate as of now is of little significance. The market is in its infancy and volumes are low(in a few thousands, it seems). Its easier to have high growth QoQ at low volumes. Much harder to do at scale and especially when competitors come to have a share of the pie.

And It would be safe to say that it is financially weakest (by miles) compared to the giants it is taking on. Every other day I read news about some other competitor(Yamaha, Honda, Bajaj, Ola, TVS, etc) entering this market. Not everyone will do well as there is too much competition. Odds are stacked against it and will be a hell of an achievement if they are standing in the market after a decade.

Betting on the asymmetry provided by this investment should not make one blind to the risks from it.

Disclosure: Not invested but tracking keenly

1 Like