Adhiraj- I tried to have a ground check for Ampher EV, There are two showrooms in Hyderabad and Secundrabad , Sales guys said there are lot of demand from the Wholesaler , They are buying and renting to Flipkart amazon and Pizzahut ( they bough in big ) , Just to make a note to everyone who invested in Greaves, FAME II benefits are only for Registered Bike not for un Registered.

Recently I saw a Tweet ,where a person showing images on a Vendor BOUNCE using Ampher EV bike. Earlier they used TCS scooty for city riding services. IF this click this can be big , Mostly in Gujrat the top modal is the cheapest when compare to other state, FAMEII is also welcomed in Haranya and Bihar Gujrat, where state govt giving additional benefits.

I neither bullish nor bearish , IF this clicked the market and have some percentage of market share, at least 1000 CRS Revenue from EV and make Balance sheet stronger + they have multiple business as well. Ofcourse it cant be compare with OLA or Ather, this is premium segments and upper middle class will target the affordable where I can only see Ampher and Ipluto EV.

Thanks for sharing your scuttlebutt. I think this sort of work is invaluable for a consumer facing brand like Ampere. If anyone else has any scuttlebutt specially on the pricing, performance, comparison to peers (ather, joy ride etc) please do share.

I test drove an Ampere Magnus Pro (their top end model) last week in Pune

The vehicle itself drives well and the final on road price was around 72,000 post all taxes and insurance and 3 free services in thr first year. Personally I felt like the quality was a little on the lower end and might not be as well finished as the price would ask for (exposed wires in the storage and the cover for the battery was flimsy looking)

The sales lady said there has been a massive growth in the order booking with around 30-35 orders a month compared to 10-12 a year ago which is very visible in the vahan numbers as well

The showrooms are financing upto 80% of the cost and buying back any petrol two wheelers to offset the cost of a new purchase.

Currently they were backordered because of lockdowns in Coimbatore.

I also think the pricing and specs of those Ola scooters will be a key factor in the success for Ampere moving forward

OLA uses AC Motor while Ampere goes with BLDC.

Difference can be seen in Motor Power, Obviously AC will provide higher power.

But That wont be a efficient system. BLDC is much more efficient.

Ultimately it will be game of Charging and Range for City commuters.

Speed people can compromise(Considering Indian Traffic)

Hi Imran, Wonderful written with good insights, appreciate all your efforts. Greaves could be a great stock for the investor. Recently said sold 1,00,000 EV in India, that is a great number. Let see what ola can do when compare to these, Investor will sure compare the market cap and give fair value to Greaves value as well.

Can you please post the link where they said anything about 1,00,000 EV ?

Last I read they mentioned 45 Cr Revenue from Ampere then they have bestway as well for E-Rickshaw.

if I take your data and Multiply with 50K(Considering Avg value of each unit) Revenue becomes 500 Cr.

Or MAy be they might have said Till date they sold 1,00,000 Historical data

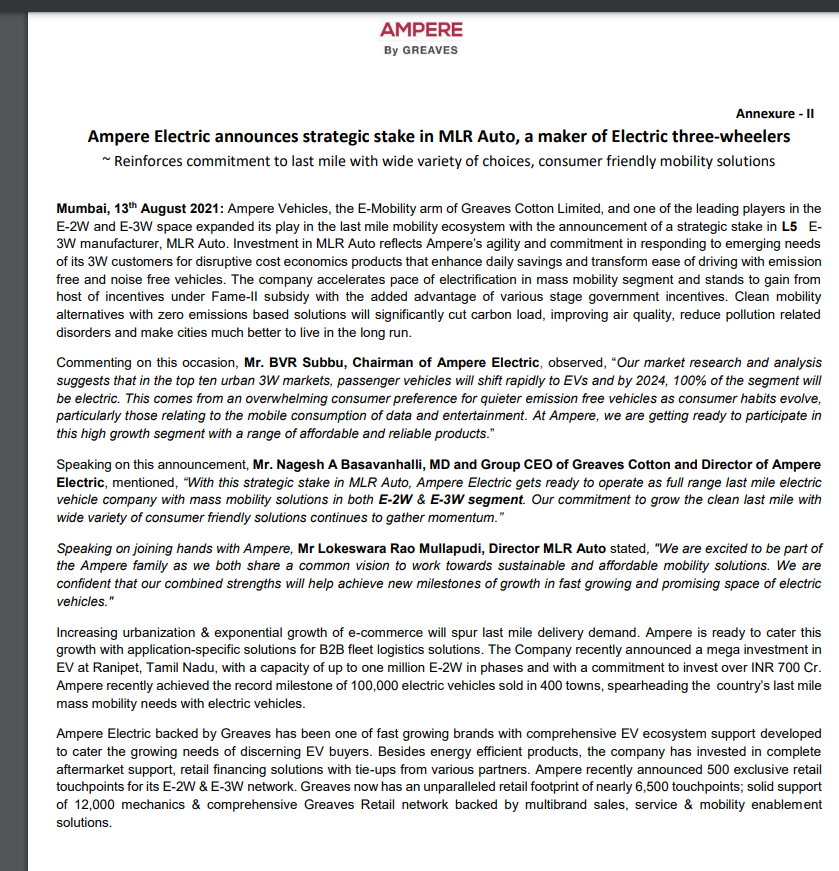

Wow. They are acquiring 26% of the company for 18 crores, and have an option to take another 25% in 12 months.

If they exercise this option, they will have controlling stake.

Looks like a good diversification play. Could not find much info about MLR auto, but their total average revenue for past 3 years is hovering around 15 crores.

Considering average net margins of about 10% (Very optimistic), they are paying almost 75 times yearly profit.

So, MLR has some very good tech / facilities / Processes or they are basically acquiring the factory.

HI VP Folks,

I am tracking greaves for sometime and I hold some positions in it, As a investor I think the company is making all the right moves in terms of scale, size and right acquisitions, however one area which I feel there could be a significant improvement is it’s marketing spends, comparing it’s competition I seldom see Ampher ads, It must be a very miniscule comparing the competition.

What do you guys think about this? Am I missing something?

• New business which is e-mobility business, Retail solutions, Fin-tech and Technologies are contributing 40% of revenue share in overall business

• Due to festive seasons and various discounts, there is good traction in 2w ( Ampere )and 3w (Ele)

• There are short term challenges in 2w as well 3w due to supply chain disruptions, while to eliminate the issue they start procuring all the ancillaries from India itself. There is only non-availability of lithium cells which is still needed to be imported from china or else all the products are procured and developed in Indian markets.

• Mega site at ranipet is been prepared and all the fulfillment of orders will be done here within on which commercialisation will follow slowly and can see the impact in revenue from Q3-Q4 FY22 itself.

• The company bought 26% of stake in MLR auto in consideration of 18.81 Crores which has now increased to 51%

• High-speed vehicles in the mobility space are getting traction and make 30% in the total volume of 10,000 per qtr sales.

• Magnum ( 2w) has the highest demand and a long waitlist in our product portfolio.

• There is an increase in cost due to various reasons

• 1. They are heavily investing in procuring people to fulfil the demand

• 2. Commodity price has increased a lot which impacted our sales ( Why they can’t pass, will justify later)

• High speed 2 wheeler scooter has reached the demand at 40% in Q4FY21 while it was a slowdown in Q1FY21 at 15-20% due to lockdown now the demand is 30% and still growing and management is bullish to reach its previous peak

• 70% of mobility sales are coming from urban sales while 30% come from rural areas.

• Overall CAPEX planned is 700 crores in which 300 crores has already been deployed and while other will be required for front-ended cost.

• The highest traction of E-rickshaw (Ele) is been shown in northern and eastern India, As many of the people drive handcarts or cycle cart which now shifted to e rickshaw for earning more revenue.

• In Organised markets, E- Rickshaw there are only 3-4 major players while financing plays a pivotal role in these markets.

• 95% of the E rickshaw are run of Lid batteries while in scooter 50% of the battery are of lithium batteries and 50% are lid based batteries. ( While there is a few bps margin difference between the lid and lithium batteries on the operation side)

• In E- Rickshaw space 90% of the market was from the unorganised sector which drawdown to 62%. While in organised space greaves cotton have a double-digit market share.

• There will 7-8% of the reduction in next qtr as well as 16-17% reduction on cost will be seen compared to the previous year as the contract is been made with B2B on YOY basis, so it’s 1 December or 1st October while we can hike the rates and passed on to the dealers

• Diesel engines sales had been gone down but the CNG and crest model has been picking up the demand which helps to offset or hamper the growth in engine segment.

• On average there is an average waiting time of 8 weeks for e- mobility scooters.

• There were 500+ sales of magnum scooters in a day and while it’s is contributing a significant share in our product portfolio.

• One out of two users is under 34 years of age and a lot of gen- Z buying coming up for 2 wheeler segments.