AR Link of Greaves Cotton https://www.bseindia.com/xml-data/corpfiling/AttachLive/b0567953-d9f2-453c-8c9b-2c95fbcd2a4c.pdf

Some Management discussion points

Financial Performance In FY 2018-19, there was exceptional expense of 17.9 Crore against the exception income of 47.5 Crore in FY 2017-18. FY 2018-19 exceptional expense was for provision made towards losses which may be suffered on account of a fixed deposit of ` 20.50 Crore placed in IL&FS.

Greaves Cotton Limited is a diversified engineering company with over 160 years of strong presence. The company manufactures world-class products and solutions under various business units - Engines, Power, Farm, Aftermarket, Care and Global, backed by comprehensive support from 325+ big 3S (Sales, Service and Spares) retail centres and 5,000+ smaller spare parts retail outlets.In the mobility segment, the Company provides affordable mobility solutions manufacturing 4 lakh plus engines annually, almost 1 engine per minute. This translates to moving over 1 Crore passengers and 5 lakh tonnes of cargo daily. In all, the Company has crossed 5 million engines, 3 million pumpsets and 1 million gensets. Greaves Cotton augmented its Clean Technology portfolio with entry in the last-mile affordable 2W personal Mobility segment with Ampere Electric Vehicles and e-rickshaws in last-mile people transportation segment.

Outlook for E-Mobility The outlook in the affordable mobility is exciting as the Company is witnessing demand in the lower speed as well as the optimal speed of the higher speed EV versions. The Company believes that the market size for affordable mobility is large at the bottom of the pyramid and more than 200 million households can benefit with these vehicles.

Outlook of AUXILIARY POWER BUSINESS: With robust economic growth and development, strong growth in the private sector capex cycle and higher budgetary allocations to infrastructure, the genset industry is poised for a good growth

Outlook on FARM EQUIPMENT BUSINESS : The Government’s continued thrust in the agricultural areas, higher MSP for certain crops and reforms to ensure farmers get a better price hold promise for the Company. Mechanisation is also aided by the higher labour prices and unavailability of labour during particular season. The Company is looking to expand product range based on the feedback received from farming communities. The Company is also working on digital revolution to increase productivity by providing timely information about rainfall and price quoted in various mandis and outlook

Outlook AfterMaket Business: Leveraging its strong brand name assiduously built over the decades, the Company hopes to become a dominant player in the After sales and service market.

Greaves Retail By building Greaves Retail, the Company is well poised to support customer with EV charging infrastructure and thus accelerate India’s mission of growing Electric Vehicles as a clean last-mile solution.

International Business : India with its competitive advantages is likely to witness healthy growth in engineering exports in FY 2019-20. Despite the much-feared tariff wars, the global recovery is expected to stay on course. The Company is well-placed to explore the emerging opportunities in the export market.

HR The payroll count of Company’s permanent employees was 1,675 on March 31, 2019.

Dividend: The Company paid an interim dividend of 4 per share on face value of 2 each in compliance with the Dividend Distribution Policy. The Board has not recommended any final dividend for the Financial Year 2018-19. Thus, the interim dividend of ` 4 paid during the financial year shall be considered as final dividend.

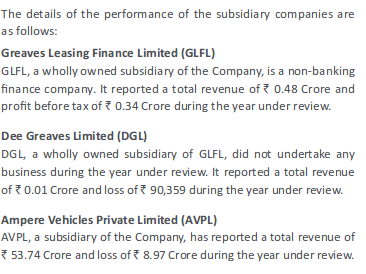

Subsidiaries:

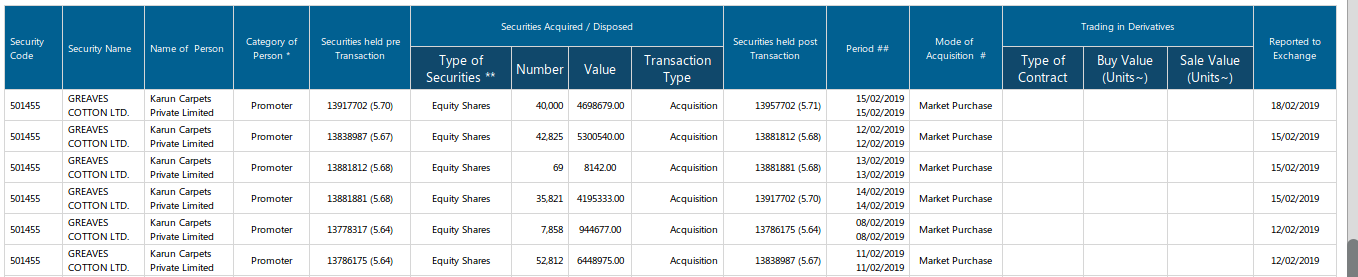

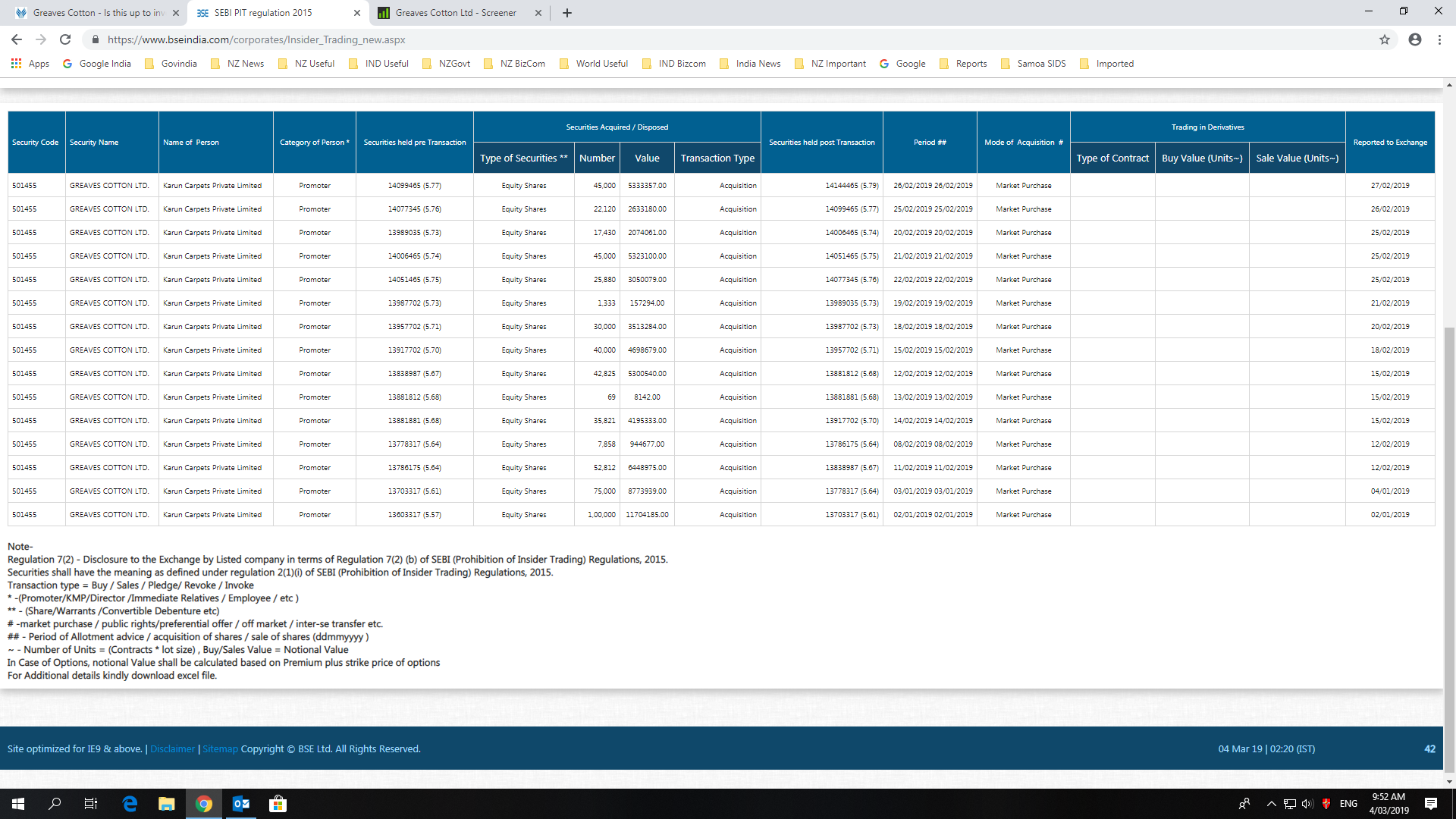

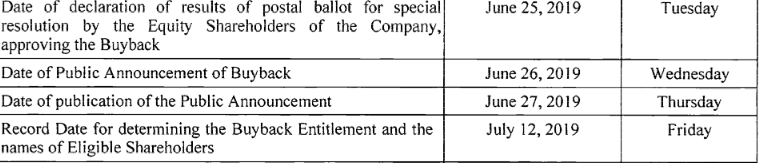

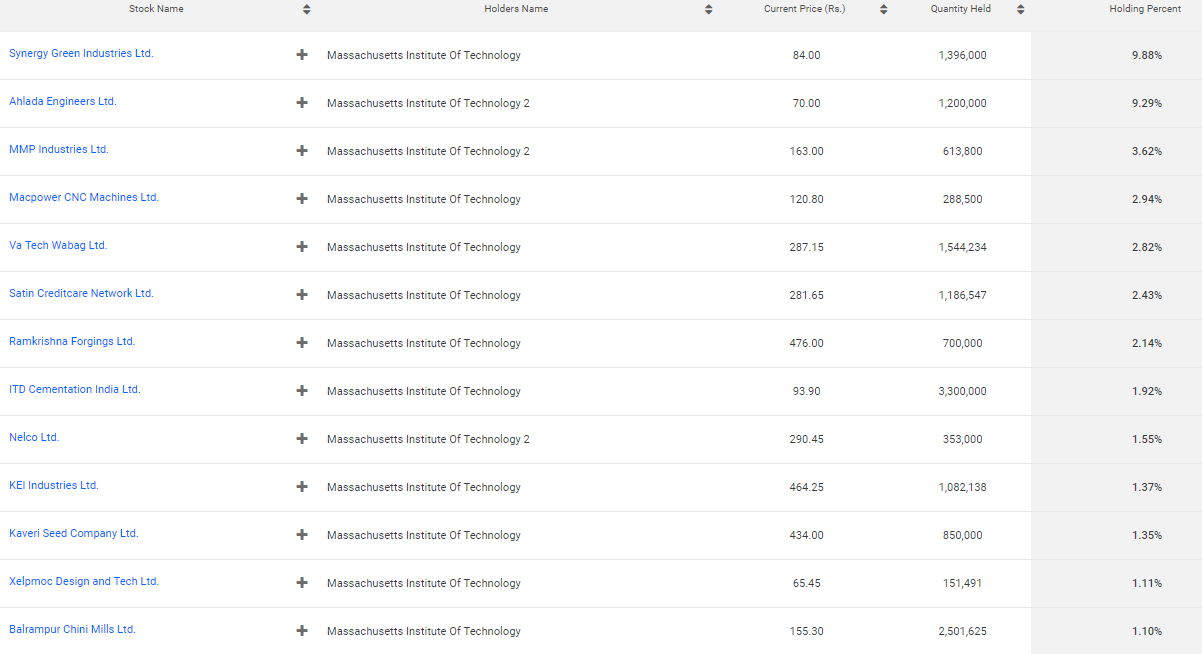

Top 10 share holders(with the exception of LIC, GIC and OIC -all GOI) and Promoters bought shares during last FY. Interestingly one of the top 10 share holder is “Massachusetts Institute of Technology”. Do they hold any other shares in India ? If any one can throw more light it will be great. As a result holding on non-institutions came down by 4.86 %. (-2.80% up to 1 Lakh). So here retail did not hold on to shares. After Buy back promoter holding will increase further.

Disc: Invested