Hi biju_john,

Thanks for the suggestion. It answers some of my queries but now opens a new Pandora’s box as well with lot many questions. Nonetheless thanks for this valuable input.

Hi biju_john,

Thanks for the suggestion. It answers some of my queries but now opens a new Pandora’s box as well with lot many questions. Nonetheless thanks for this valuable input.

You can ask the queries, will try to answer, work as an engineer in the shipping sector

How will the current ukraine russia war effect the earnings of the company?

I also read the insurance will go higher for shipping companies as well ,how do shipping companies perform during war and inflation?

The report above talks about container ships.Greast Eastern does not operate container ships and as far as i know does not operate in the black sea area. Anyway will check. They are mainly into the bulk carrier(bulk goods like iron ore) and oil tankers. Bulk rates after hitting a peak in mid 21 was sliding down and is picking up. Oil tankers freight rates are also going up. Since fuel costs make up a large percentage of the opex of a ship, raising fuel costs may nullify any gains in charter rates. Will do more work and find out something specific to great eastern.However in general rising crude prices are not good for shipping sector.

Hi, Does anyone know any free source to track the Baltic Dry Index, Baltic Dirty Tanker Index and Baltic Clean Tanker Index?

Any reason for such a rally? Should one switch from ge shipping to Sci now due to lower valuation and reports saying Q2 will be good for Sci as they have 5 vlcc tankers and i read somewhere that vlcc tanker prices have moved up substainsly in Q2?

tanker rates are up. sci management is sleepy, just compare q1 results of both companies, sci can be bought if you want disinvestment play.

disc - invested in GESHIP.

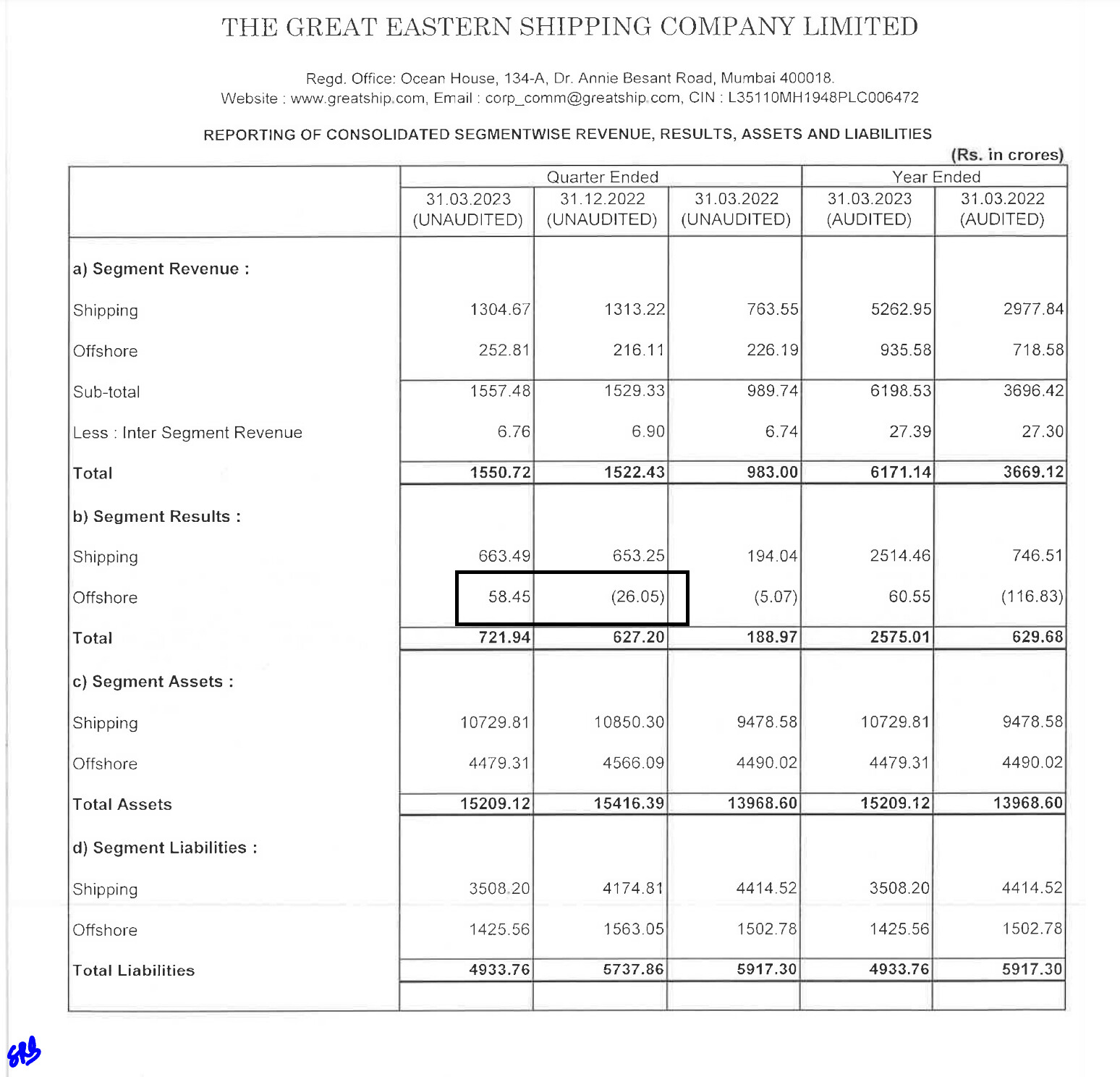

Excellent results ,company made a profit of 769 Cr in this quarter alone which is more then what they made in the whole FY 22.Tanker rates are up due to russia and ukraine war ,tanker rates are expected to rise further as long as europe gets his gas needs from america via ships then from russian pipelines .. I expect the quarter 3 to be more profitable then this quarter .

Disc :Invested as a cyclical bet due to shipping shoratge that might have happened in 2026 to 2030 but i believe i got lucky with it this time .

Guys any idea what would be a great time to exit i feel like it will give a breakout of it’s all time high of 625 rs?

Historically it Trades between 0.5 and 1.25 of its Avg NAV ( which is around 550 )

Occasionally in extreme markets it can exceed the ranges on both sides

Nav currently stands at 800 rs due to high dollar rate and even at pessimistic case scenario we perceive the value to be 700 rs ,the stock curently trades at fair price.

But this should change as :-

2)In the con-call mangament has quoted that rate of tankers have gone up significantly compared to quarter 2 which was the highest profit the company ever made in the history of the company ,for the half quarter the ships have been on time charter and they will be for another 2 months so i am pretty optimistic about the quarter 3 and quarter 4 as well .As a person in con-call asked the managment that are these tanker rates we see right now sustainable which we are seeing because of the war? ,to which the management replied anything can happen and this business is very uncertain but what they believe is even if war is over it takes time for wounds to heal and for europe going back to russia for there energy needs.

Currently the business is seeing great tailwinds and the only thing that can go wrong for the buisness is a recession which might lead to demand destruction even in that case the mangament has said they huge cash balance will be used to acquire newer ships as they have ageing fleet .

Disc:Invested at very low levels will avaerge up if the opportunity present it self .

Global situation has lot of tailwinds for this company.

Tidewater’s ( a global giant in the same sector) recent results are a good indicator.

One can read here .

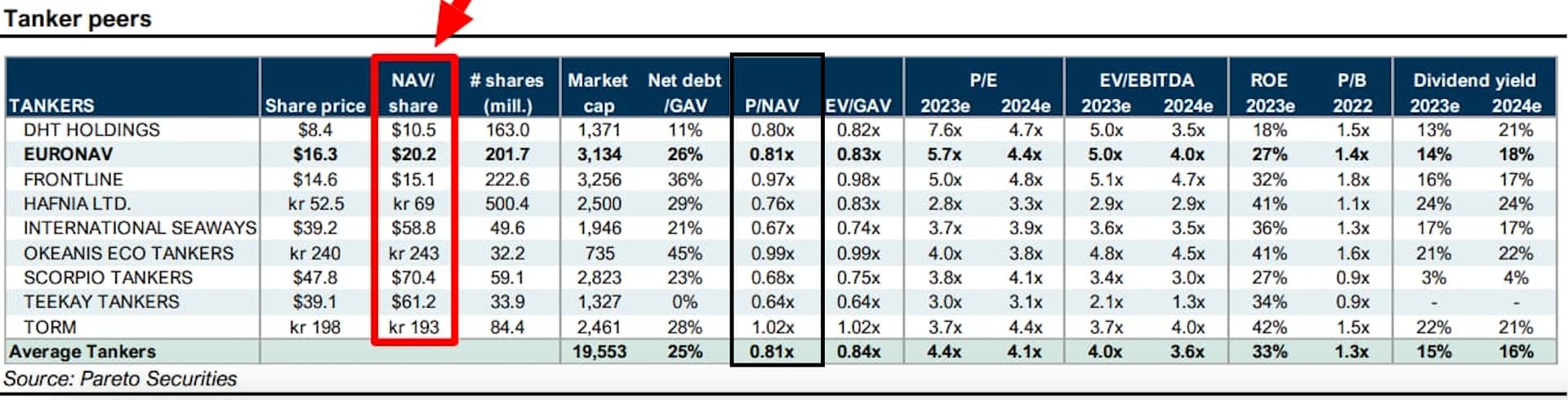

Amazing results from GE Shipping. From what I saw on various forums, everyone was expecting a fall in profitability. Even most of its US-listed pure tanker companies have seen a fall in their profits (Scorpio Tankers and Euronav are the ones that I track).

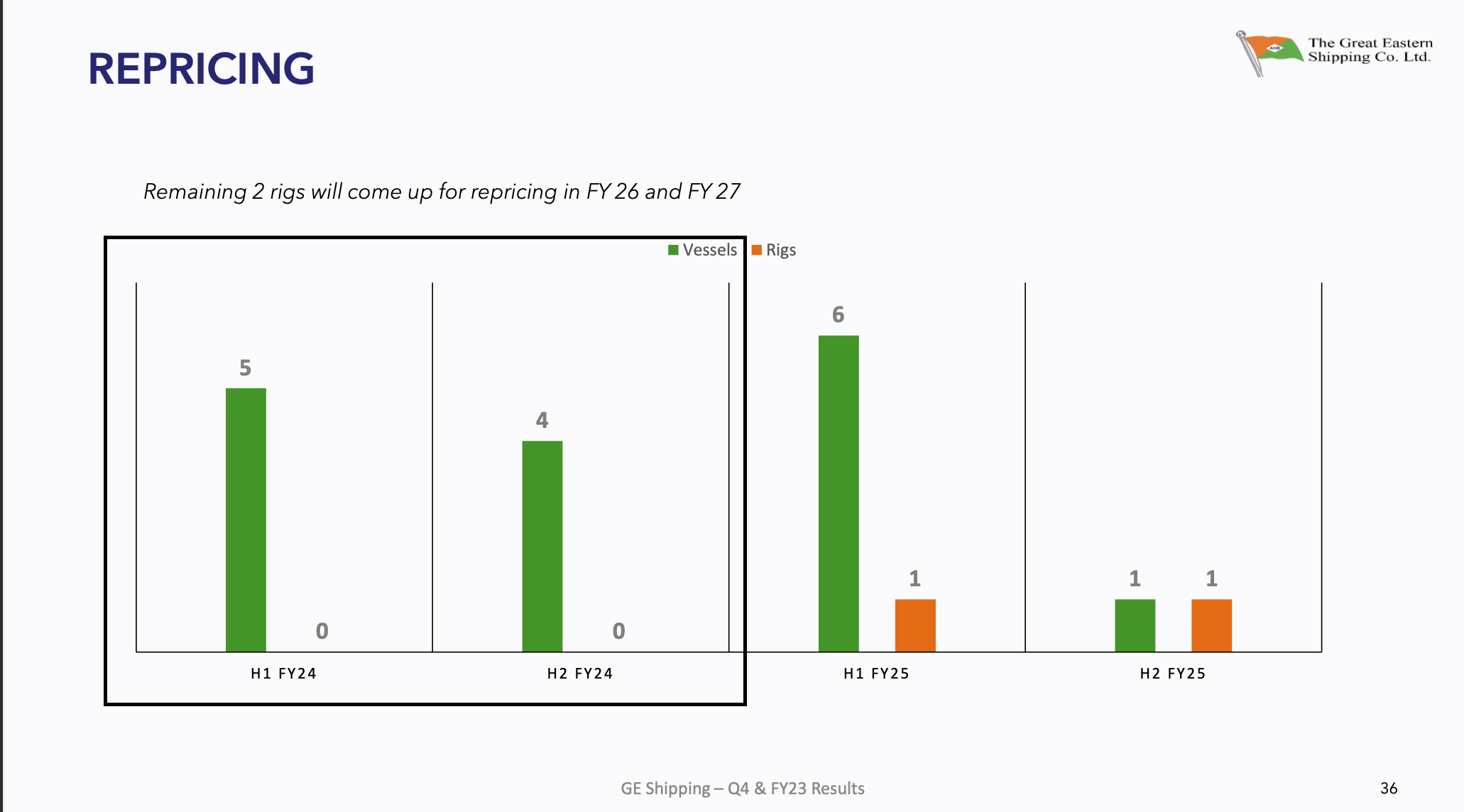

This quarter, even the offshore business became EBIT-positive due to the repricing of one of their rigs.

They currently own 19 offshore vessels and 5 are going to be repriced in H1FY24 and another 4 in H2FY24.

Another trigger will be the repricing of one of their VLGCs. The spot rates are USD 50000- 60000.a day. Currently, it is priced at USD 30000/ day. This will result in an approximate increase of 60-90 crores of revenue annually that will directly flow down to the PBT.

It is still trading at 0.58 its NAV whereas even its cheapest peers in the US market are trading far above it. Just for reference:

This divergence is probably because of the niche of this sector.

Both the future of the tanker market and the valuations seem very juicy.

Hi can anyone suggest as to

A detailed explainer on this company

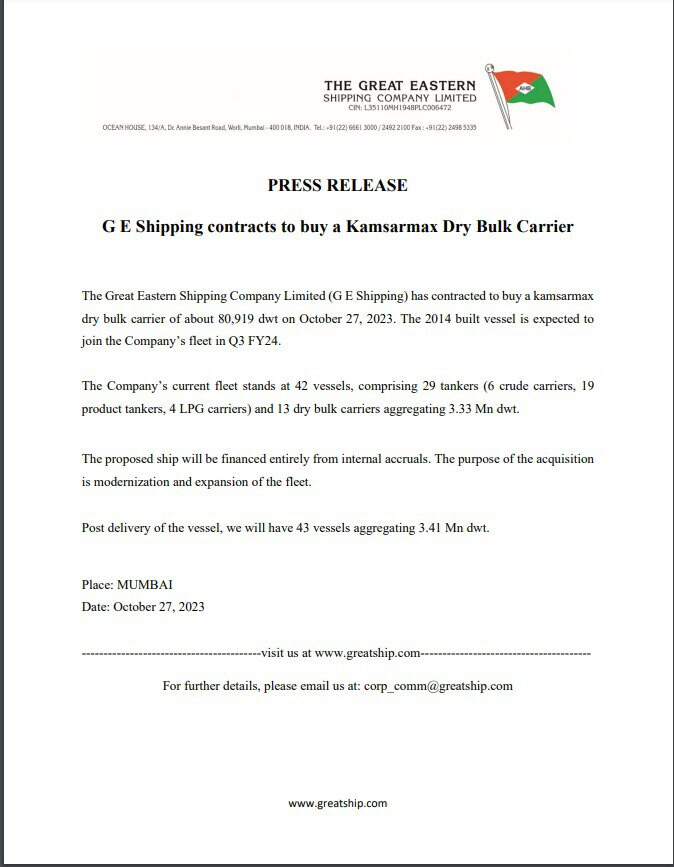

GE Shipping Company have decided to:

The company currently has 42 ships in its fleet. These include 29 tankers (which carry things like crude oil, product tankers, and LPG) and 13 dry bulk carriers (which transport things like grains and minerals), with a total capacity of 3.33 million tons.

Company used their own profits (internal accruals) to pay for these acquisitions/expansions, and the main reason for getting it is to expand their fleet.

There is a theory that you should buy down and out stocks. It is they that make the real money.

P/E of 4.61, and ROE of 26.8 % along with ROCE 20.9% should support keeping faith in the share? The PE also compares favourably with Industry PE of 10.5.

I have a smail investment.

With shipping logistics company in stress globally and red sea route having challenges, India shiping will be in a bit of demand