This is a very interesting conversation with some fantastic inputs in this thread.

I’ve always been fascinated with shipping. It’s one of those industries that has a very long cycle - and it’s been battered for a long time now, and still shows no signs of revival, despite some of the promising numbers thrown around here. It’s one of those sectors whose valuations are screamingly low. But is it worth it at current levels?

I don’t know. There’s no doubt it looks very attractive from price standpoint.

However, the biggest concern in the industry is lack of talent. Being a merchant navy used to be a posh career choice – a captain used to earn enough to buy a house on a single shipping assignment (of course, this depends on the contract) now typically earns a pittance, barely just enough to make EMIs and put food on the table. Several of my shipping friends have switched careers.

Also, the fixed cost of running a fleet of ships now cost more than the freight in some cases, depending on the fleet allocation (smaller ships are easier to maintain, but fetch less income, etc). Insurance cost is also higher (thanks to increased piracy!).

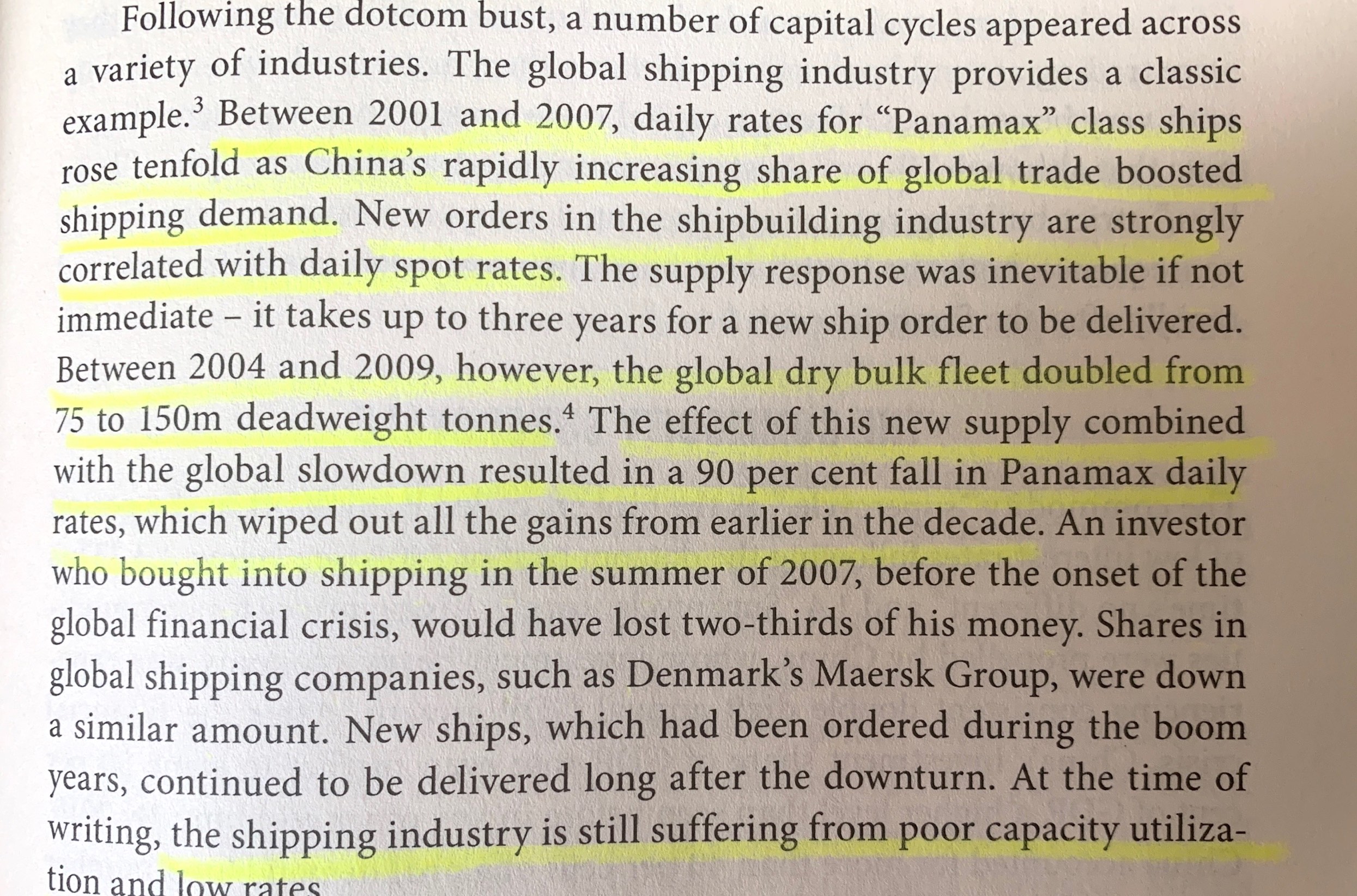

Besides, the competition is just brutal. Significant over-investment in capacity during the 2000s practically killed the industry. Maersk, for instance, hedged their bets on supersized tankers, in anticipation of burgeoning demand for oil. Obviously, in hindsight, this backfired. Some large shipping carriers have gone bust. There are many other factors – mis-allocation of capital by ship manufacturers and shipping companies, global warming (shipping is one of the bigger polluters from what I’ve read, though not as much as air transport), climate change, among other things.

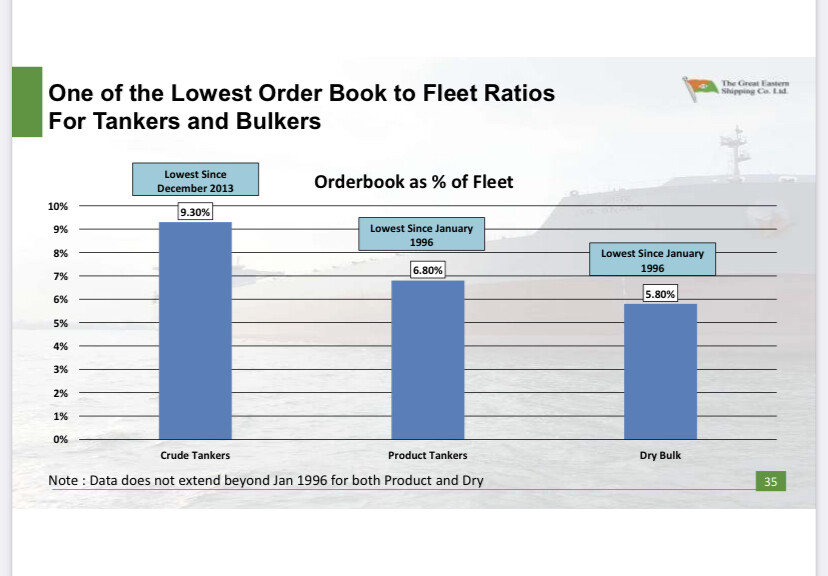

IMHO, the future of shipping lies in dry bulk and inland waterways (i.e. smaller ships which can cater to local economies). Margins for dry bulk is lower than oil but offers more “stability” than oil. I reckon oil demand will last for around 20-30 years more before “green energy” takes over. Inland waterways is a massive opportunity as far as India is concerned. Unfortunately, we’re still stuck in blueprint phase and it’s not showing any signs of life.

In a nutshell – too much headwind, lots of waves. Only super-strong balance sheets will be able to ride out this prolonged recession in the industry. I don’t know if we have any. I see good numbers from GE Shipping, but they aren’t consistent quarter after quarter to give me confidence to invest. It makes sense to do position sizing, build a small position, just to see where it goes.

Sure, one can do some momentum investing, but it’s ridiculously hard to pick entry/exit points as stock market prices tends to be super-cyclical and volatile in the short- and medium-term.

From value investing standpoint, shipping is at its inflection point. Is it ripe to invest with a 10-15 year horizon? I’m very intrigued how this plays out.

Just my two cents.

Disclosure: Tracking.