Got it, Thank you very much for again clarifying it.

Operational efficiency (Ultimately operating profit only)

Really sorry, Not able to understand in 1st reply

Got it, Thank you very much for again clarifying it.

Operational efficiency (Ultimately operating profit only)

Really sorry, Not able to understand in 1st reply

Returns from equity markets?

If so, not a bad way to use surplus funds.

They are just putting up a pilot plant to test feasibility of Li-Ion recycling. Based on the success of this pilot, they may go for a larger commercial plant. I think this is a good move, albeit cautiously, to be future ready.

Do read below article for a perspective on Li-Ion Battery recycling.

The lead acid battery market will continue to be a significant one despite the growth of Li-Ion batteries for EVs. Lead acid batteries have applications in commercial vehicles, construction equipment, defence equipment, generators etc etc. List is a long one.

Sir, Very good point. Does it vary from industry to industry.

If yes, which all industry has this problem/trait

Q3FY24 Concall Notes

Thank you for sharing the notes. Did they give any guidance going forward? Market has reacted quite violently to the results.

They stuck to FY27 guidance. Said there maybe a quarter up or down, but overall on track to achieve 25%CAGR revenue and 35%PAT CAGR by FY27. Market may have reacted to volume reduction.

The issue is with the Red Sea Crisis, they said that they are looking to supply to customers outside of Europe if the crisis continues. The numbers will be muted on volume side for another quarter likely. They sounded confident over the longer term but short term they were not clear hence i think the reaction.

yes, also thematically, this does seem to be a long term play.

Amara Raja is setting its own 150,000 tons battery recycle facility, which is roughly 35 to 40 per cent of its requirement. How this will impact Gravita, especially to volumes of Chittoor plant which is near Amara Raja facility?

Gravita India FY24 results and conference call:

Consolidated Topline/ Topline growth YoY: 3161Cr / 13%

EBITDA/ EBITDA Margin for FY24: 285Cr / 9%

PAT / PAT GROWTH YoY: 242Crs / 18.6%

Commentary:

Gravitas’s wholly owned subsidiary situated in Tanzania, Gravita Tanzania Limited, has increased the battery recycling capacity by 5,000 metric ton per annum, bringing the total capacity of battery recycling of this unit to 12,000 metric ton per annum.

Gravita has expanded its total capacity to 3 lakhs plus metric tons per annum in Financial Year ‘24 compared to 2.34 lakh metric tons per annum in Financial Year ‘23, which shows an increase of 28%. The company aims to increase our capacity to 5 lakh plus metric tons per annum by Financial Year ‘27.

Volume growth is less in aluminum because there is no hedging mechanism for the same. Alum. alloy contracts are expected to be launched soon on mcx which will help the company hedge the metal.

EBITDA per ton for plastic is Rs. 11,176 per ton, lead is Rs. 19,252 per metric ton and aluminum is Rs. 15,308 per metric ton in Q4 Financial Year ‘24. This is in line with the company’s target.

45% of revenue in Financial Year ‘24 came from value-added products, management aims of achieving 50% revenues from this category. India contributed 62% and the balance contribution of 38% is from overseas business.

Vision 2028. Management has stressed on the following points as a par of their 2028 vision.

Diversifying into new business verticals like lithium-ion, steel and paper.

Aiming for revenue CAGR exceeding 25%, profitability growth surpassing 35%, maintaining an ROCE of 25% plus

Elevating non-lead business to over 30%, using 30% plus renewable power and reducing energy consumption by 10%

Commitment to sustainable development, increasing the proportion of value-added products to 50%

by fy 2028 the company wants revenue from non lead business to contribute 30% to the topline

Management on Aluminum capacity utilization: The company had only capacity utilization of 11% in the case of ADC12. So, this year, they plan to increase it once the contracts are in place on mcx. Management expects that the derivative should list somewhere in next quarter and then brand empanelment will start. So, in Q4, they expect it to have a growing volume. And next year further, the volume growth and capacity utilization to higher levels. The aluminum business will grow at least by 60% to 70% in terms of volumes because they are also adding capacity at a certain location, at Ghana, that should be operational in the beginning of the Q2.

Management on Supply chain issues: Mgt. also mentioned about the logistics delay and macroeconomic challenges they feel by addressing the issue by diverting the volumes to other geographies, as the company has touchpoints all over the world… So, wherever there is an issue like this they encounter it by diverting the volumes to other geographies without affecting the volume growth.

Arbitrage play: The management mentioned that this year, they have not taken as much domestic scrap simply because the overseas scrap was much cheaper compared to the domestic scrap, and there were some arbitrage opportunities. Overseas markets were lower compared to Indian markets.

So, they bought more international scrap as compared to domestic scrap. So, this also contributed to their increased working capital cycles.

Regarding Amararaja putting up a plant: They mentioned that Amara Raja is only putting a plant in the south, but they sell this battery everywhere in India. while Gravita has plants in the North, in central and even in west India. The specific benefit that we have is that we can process it in the northern plants and then we can give the finished products to Amara Raja from the south plant itself. So, that gives us the advantage over the competition

I feel that this is a good time to deep dive in the recycling sector and feel that garvita is in a great space with a huge market potential. I have made some tracking position and would track it as closely as I can.

In addition to this:

Implementation of regulations presents opportunities for smaller battery manufacturers who may lack infrastructure for battery collection and processing.

Smaller players may need partnerships with companies like Gravita to collect and process batteries

Capacity of new plants being set up by other battery manufacturers represents less than 20% of the total capacity in India, considering Exide and Amara Raja.

The recylcing sector does look promising specially after the BWMR and EPR acts being pushed by the government in addition to the concept of circular economy. This will lead to lot of business moving to organised players like Gravita. Moreover, their foray into lithium-ion and steel should start giving results maybe in about 4-5 years time.

Gravita India have shown consistent growth in revenues and profits and mgmt focus to expand capacities gives one confidence of the performance of the company going forward. Interesting times ahead for the sector and the company.

I am invested in Gravita and look to add up going forward.

How should we view the qualified opinion presented by the auditors?

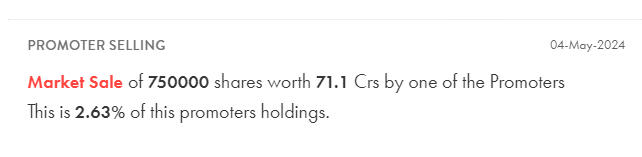

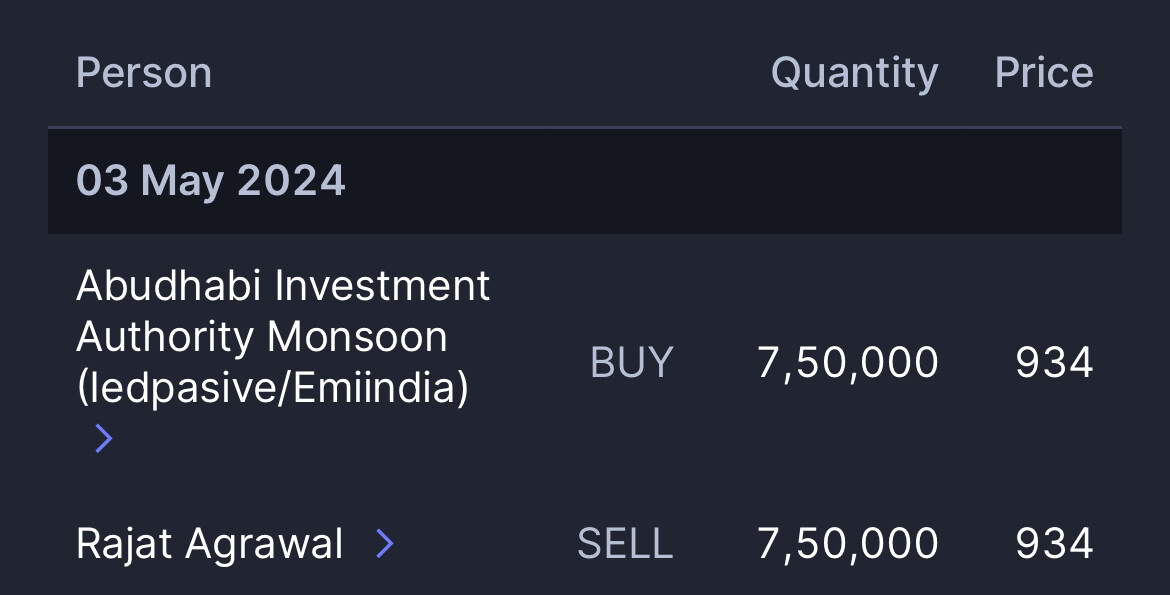

Promoter has sold shares in the open market