Gravita is leading Indian multinational company having state-of-the-art nonferrous metals (Lead and Aluminium) processing unit at Jaipur (Rajasthan), India. We carry out smelting of Lead Ore / Lead Concentrate / Lead Battery Scrap and Aluminium scrap to produce Secondary Lead Metal and Aluminium Ingots.

The Existing production Capacity of 3600 MTPA of Gravita Metal Inc. has been increase to 6000 MTPA w.e.f 28th December 2016. The reason behind capacity addition is due to potential raw material availability and rising demand of orders.

Gravita commenced commercial production of Lead metal from its new recycling plant situated at Chittoor, Andhra Pradeh. This plant is having production capacity of 12000 MTPA and will grab the opportunity of domestic scrap available with the large telecom players, UPS batteries from I.T. offices in and around southern markets by having long term contracts to collect their PAN India scrap in cost effective manner and by exporting the finished goods using the nearest Chennai port, being near to the port will help in reducing cost

“Gravita has commenced commercial production of pet recycling by setting up plant through its step down subsidiary Gravita Nicaragua SA in Nicaragua (a part of Central American Nation),”

Increase in lead demand and price hike: The lead prices which have suddenly shot up in the last two months and particularly in the last one week or ten days. The major reason is the demand from the Chinese market because there are a lot of supply side reforms going in China where they have closed a few of the mines because of some safety issues and add to that because of heavy winters there is a shortage of mine products from Chinese mine.

With all above fact “gravita india” made not only turn around but made new new height in their production and profits. Its now at top performance of their life time and story will not end here. Look at appreciated in share price in one year together with financial performance:

8 Likes

Please mention disclosure and interest .

There are more positive; however please also see key risks/negatives :

Scrapping import duty on metal waste, giving industry status.import duty, presently the levy varies from 2.5%-5% depending upon the scrap metal," "In the global market, we cannot stand as a competitive market due to duties levied in India. Secondly, having PSIC and other document procedures to import metal scrap are totally impractical,"

Any change in scrapping metal policy impact on performance of Gravita Ind.

Plastic recycle business is new and at USA, change in environmental policy in US can’t be predicted.

**

CMP: Rs 70.60.

**

Disclosure: I am heavily invested at Avg. cost of Rs 20.

5 Likes

@ajay1979 The company had posted losses in Dec 15 and Mar 16 quarter. Can I know what prompted you to buy the share during that period when the company was posting losses. There might be some strong reason or conviction from you side. Will be happy if you can let us know.

2 Likes

Thanks for asking justification, you catch the right point. Actually after march '16 result it was trading at 52 week low ~15-17 and was stabilizing and getting support. Points what triggers me are :

- even in march '16 was loss but there was good increase in revenue from 83 in dec’15 to 118 Crore in march’16 and reduce losses from -1.5 to -0.21 …this losses was temporary as it was bad time of metal(specially lead) which was improving.

- when it start moving from 52 week low , I get the news that there are now coming in aluminum recycle business so I was expecting a increase in revenue and that time aluminum bad time was over.

- later when they announce to commission expand unit at Andhra I have added more

- They also announce to start plastic recycle business which is good in environmental friendly county like US.

- increase in metal price also supported the company .

- there was stable increase in revenue and profit.

CMP: Rs 71.65 (52 week high).

**

Disclosure: I am heavily invested at Avg. cost of Rs 20 and expected to continue for further 2 more year.

2 Likes

I understand this would turn out to be a cyclical metal business in the long run. However, without factoring the price fluctuations, do you know what would be a steady state margins for conversion of scrap lead to finished lead?

1 Like

You will get the perfect answer on 15th may with Q4 and annual result.

1 Like

I went through the last few months results and it seems that there is a growth in revenue which is steady but the profit is not growing - It seems that the margin is very low (check expend with each revenue line) and plus this is cyclical too.Fundamentally its just fairly priced but cyclical business needs to be looked differently.Could a long term tracker of this stock give a margin breakage and also the demand so to say the growth driver in future.

Disc - not invested

1 Like

Dears thanks to evaluate Gravuta india,

I agree that margin is low due to type of business however revenue increasing continues since dew quater which is coming from its added new unit after expansion and also added new segments in current business I.e. added new lead recycle unit for expansion and started aluminum recycling unit last year and started plastic recycling unit this year. Since new business have just started I except that will continue to add more revenue and add more profibility . things will be more clear on anuual result on 15 may…

1 Like

thanks ajay - will wait and check the results.

2 Likes

pe just 17; vs peers avg. of 32

Significant increase in revenue from lead business expansion and new aluminium recycle buduuness…plastic recycle yet to perform in coming quarters as recently started.

4 Likes

Must watch vedio…gravita has good vision of expansion…

Supported by analysts:

4 Likes

Thanks for sharing. Appears to have a very exciting future with about 50%

increase in topline in FY 18.

Disc : Invested recently

3 Likes

Of late all the names in the Non-Ferrous Metals are delivering great results, is that because of

- Tailwinds provided by cyclical uptrend?

- IF yes, what factors provide tailwinds and how long are they likely to support?

- Is there anything special about the specific companies like

a) Gravita India

b) Nile

c) Pondy Oxides

- Recent quarter results by Gravita seem to be phenomenal, how much one should attribute its success to Gravita’s operational excellence and how much to cyclical up trend?

Any insight on above points would be very helpful to juniors like me.

3 Likes

Massage from Gravita chairman( from annual report):

It has been a stupendous year under review

for your Company and it gives me pleasure

to write you again. While the financial

numbers were historic and reached record

levels, our operations and strategies formed

the bedrock of growth. This was achieved at

the backdrop of volatile economic scenario,

both at global and national levels. Even

as demonetisation pulled the economic

growth back at 7.1% for FY 17, our country

continues to outpace growth of major

developed economies. On a global scale,

the commodity prices remained volatile, as

several macro-economic and geo-political

factors continued to overshadow overall

global economic growth.

Amidst these circumstances, your Company

outperformed industry growth and has

created a platform for sustainable growth.

We took several initiatives that helped us

scale ahead, One, we actively increased our

price control mechanism, mitigating price

volatility risks. In the last two years, the metal

prices had gone down, which led to fall inour margins as we were unable to pass the

fluctuations to our customers. As a strategic

step, we enhanced our internal team, and

consciously made efforts towards locking in

prices at London Metal Exchange (LME).

Two, we gave incentives to our team for

operational improvements. The incentives

were given to ensure we see tangible results

for increase in volumes and procurement

levels in a cost-effective manner. The result:

volumes increased by 63% in all the plants

and capacity utilisation increased by 10%.

We also saw a significant improvement in

the collection ratio improving our margins.

The Company’s profitability increased from

H4.5 crore to H30 crore – registering our

highest ever profitability.

Three, we entered into new countries

in terms of procurement and market

expansion. Our team focused on grass

root level for procurement, reaching out

to every possible level of Lead secondary

sale, thereby strengthening our position as

market leaders.

Leveraging our recycling experience, we

diversified into aluminium recycling in

April 2016 and performed reasonably well

in first full year of operations. Similarly we

also penetrated the PET recycle business. I

would like to assure the stakeholders that as

an organisation we are leveraging our core

competencies of more than two decades

and expanding into new businesses only to

derive greater operational efficiencies and

higher profitability levels.

Coming back to our Lead recycle business,

we commenced commercial production of

Lead metal from our new recycling plant

situated at Chittoor, Andhra Pradesh. The

plant has a production capacity of 12000

MTPA and will help us enhance domestic

The Chittoor plant has a production capacity of 12,000 MTPA

and will help us enhance domestic procurement in the

southern region on one hand, and make it easy for us to

export the Lead Metal/Alloys through nearest Chennai Port

to our major customers across South East Asian Region.

procurement in the southern region on one

hand, and make it easy for us to export the

Lead Metal/Alloys through nearest Chennai

Port to our major customers across South

East Asian Region.

We are quite optimistic about the progress

of our business as the global and Indian

industry for Lead and Aluminium are

performing well. There has been a significant

growth in the automobile industry by 12-

13%, which is advantageous for us, as the

automobile sector is one of the biggest

growth driver of our business.

As I mentioned earlier, we also started plastic

recycling production by setting up plant

through our step-down subsidiary Gravita

Nicaragua SA in Nicaragua. The plant was

set-up with internal accruals of around USD

1 million. We have a two-stage model for

PET recycling: waste collection and flex

formation; and we will continue to expand

PET recycling facilities in South America. We

are expecting a revenue of H100 crore in

FY18 with 12-15 percent profit margin. The

current annual production capacity of this

plant is 3600 MTPA.

The engineering and Lead recycling Turnkey

solution arm of your Company has bagged

an order worth H150 million from the Middle

East region in early 2017. As the oil driven-

economy of Middle East continues to face

challenges, the Government now focuses on

giving thrust to manufacturing and recycling

sector. Your Company, a leading recycler of

Lead has a niche offering in Lead recycling

turnkey solutions have executed over 50

turnkey projects in last few years. This move

will help us further in penetrating markets in

the emerging countries.

As we march along the road towards

growth, globalisation and sustainability, we

remain rooted to our ethos and values. Our

CSR initiatives extend well beyond our core

business objectives, and our commitment

and concerns for the society are evident

from the various initiatives it has taken in

different fields in such short period of time.

In our endeavor to create a green and

sustainable environment we showed true

spirit and ran a campaign “Mission Green” to

plant 5000 trees engaging students, women,

clients and community at large and making

a commitment to the community around it.

Going ahead, we are expecting better

growth in FY18. With implementation of

GST, we expect the shift from the informal

sector of Lead recycling to formal sector.

With a diversified business model in

place, we expect to expand our revenues

and profitability levels and emerge as a

recognised recycled business conglomerate

with a vast global and national network.

I also take this opportunity to thank the

Board and the team for their continued

support and trust to drive the Company

ahead.

Warm Regards

Dr. Mahavir Prasad Agarwal

1 Like

EPS and PAT should be same unless equity is diluted.

Why is pat 29% CAGR and EPS 4% CAGR ?

2 Likes

@ishandutta2007 - The graphic says its 10 year CAGR and in 10 years, there has been a lot of dilution, hence the difference.

1 Like

I went through the annual report and have the below mentioned doubts. I wrote to the Investor department at the company and await a reply. Meanwhile I’m posting the doubts here and would appreciate if somebody can answer them for me.

-

As per page 12 of the report we have a lead capacity of 113,419 MTPA but our production for the year was only 32,619 MTPA for Lead. Why is there such huge under utilisation and in the year we have added capacity of 24,270 MTPA of which 6,000 MTPA is for Aluminium. I assume the rest majorly belongs to Lead. Again when the existing capacity is so under utilised why do we need to add new capacity?

-

What is the reason for loss in Ghana subsidiary despite having relatively high realisation per MT of lead sold?

-

Pg 52 mentions investment in efforts to utilise alternate sources for oxyfuel combustion system for its smelting section. As drawn from P&L our power and fuel cost is 0.77% of our lead revenue. How significant will be these efforts in terms of cost saving?

-

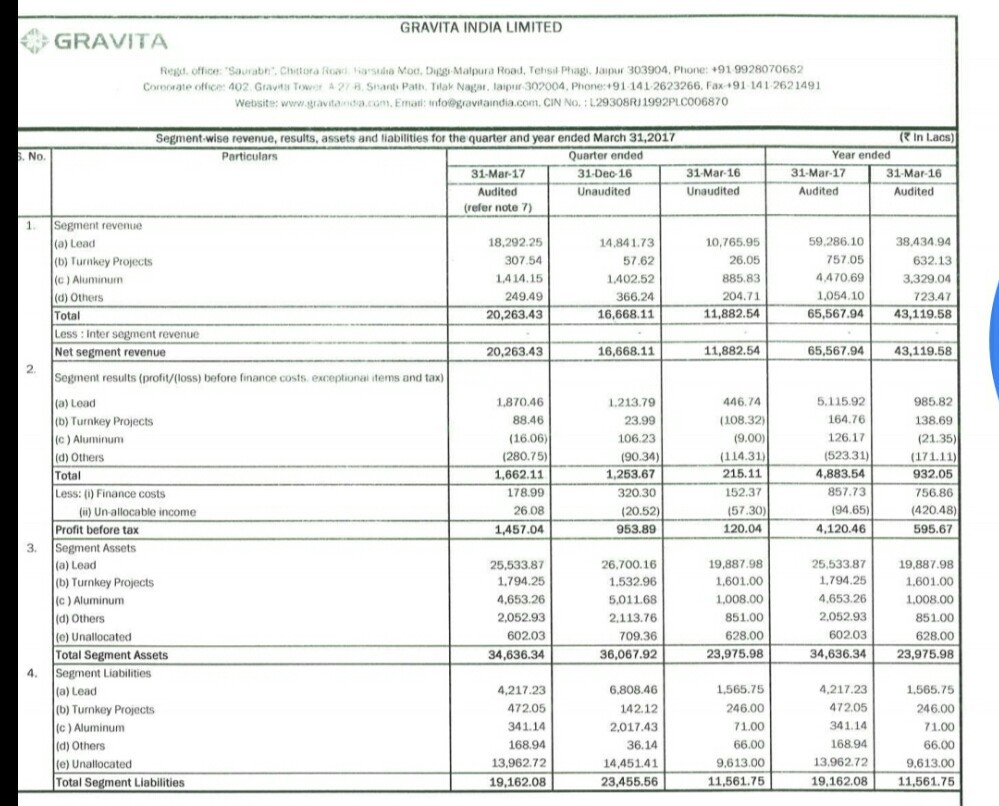

As per 145 Segmental disclosure our margins in lead business have increased from 2.5% to 8.63%. Was this increase abnormal or is it sustainable? Also turnkey projects offer a good margin of roughly 21-22%. Are there any chances of becoming a major turkey projects service provider so that we earn higher margins? What is the business outlook for the same segment?

Please pardon me if any questions above seem irrelevant as I’m new to reading annual reports and asking meaningful questions out of the same.

5 Likes

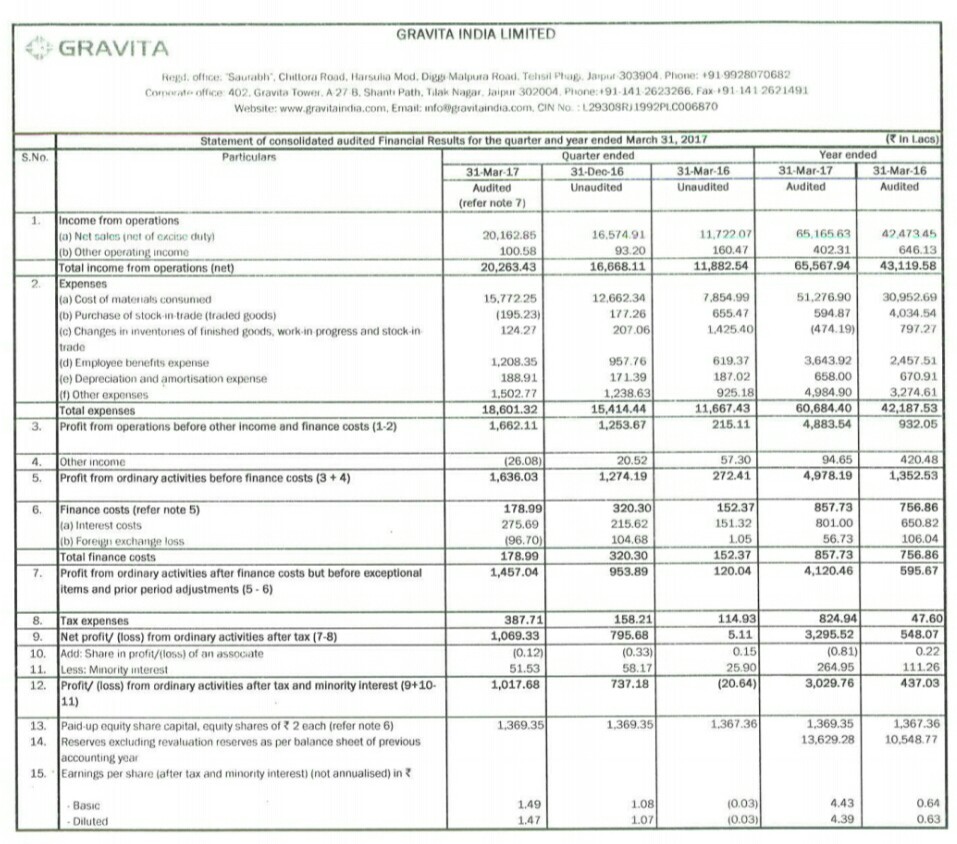

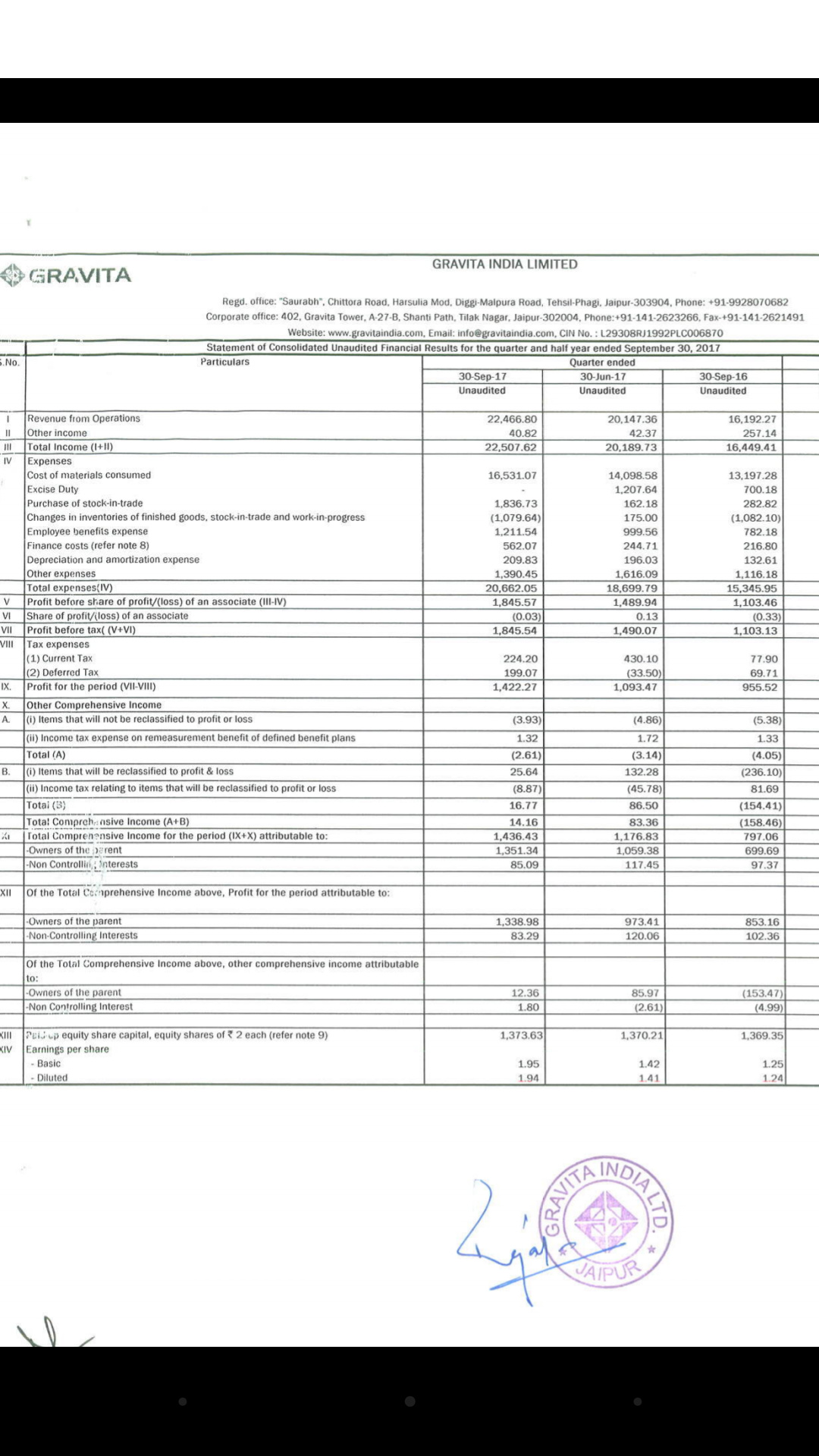

Good performance continues in Q2 as well.

Revenues up 39%, EBITDA up 116% and PAT up 57%. EPS Rs.1.95 vs Rs.1.25 YoY. QoQ as well performance is very good. Q1 EPS was only Rs.1.42 so that’s a great improvement even QoQ.

Segment-wise. Lead revenues have improved 35%, Aluminium 110% and Others (PET) up 154%. Clearly Lead and Aluminium commodity cycle is in favour and should remain so for awhile helping the numbers.

4 Likes

As expacted…One more bumper result from Gavita India… Quater to quarter growth continued…1.39x sales and 1.56x profit in Q2-2018 vs. Q2 2017 and 1.12x sales & 1.37x profit against Q1-2018…