Gravita India - A very promising company

Q2 highlights -

Sales -836 vs 683 cr, up 22 pc

EBITDA -73 vs 59 cr (margins stable @ 9 pc), up 23 pc

PAT - 59 vs 45 cr, up 30 pc

Volume growth @ 14 pc

Last 5 yr CAGR growth rates -

Sales - 22 pc CAGR, from 1242 to 2800 cr (percentage of export sales from 25 to 37 pc)

PAT - 35 pc CAGR, from 15 to 201 cr ( PAT margins expanded from 1.25 to 7.18 pc )

Project updates -

Started lead recycling plant in Togo, expanded lead recycling capacity in Chittor, started rubber recycling in Tanzania, Set up a battery recycling plant in Oman ( via JV ), started Aluminium recycling in Senegal

Vision 2027 -

35 pc + PAT growth

25 pc + revenue CAGR

New recycling verticals - steel, Lithium, Paper

50 pc + value added products

Biggest entry barriers -

Deep rooted procurement network

Diversified customer networks

Customised and value added products

Currently - company has 4 recycling verticals across - lead, rubber, plastic and aluminium spread across 11 recycling plants

Current capacity utilisation @ 55 pc

Current scrap collection capacity @ 2.05 lakh MT

Current capacity @ 2.84 lakh MT/yr - across 4 verticals

Capex lined up for next 4 yrs @ 600 cr for brownfield + Greenfield capex

Slowdown is Aluminium segment in Q2 should reverse by Q4 or Q1 next yr. Lead business leading from the front in Q2. Flatfish business performance in plastic, rubber segments as well. Management expects all the segments to start firing by Q4, Q1 next yr

Company plans to set up Li-Ion recycling plant near Mundra. Have applied for necessary permissions. To start the pilot project first and then scale it up

As lead usage falls due reduced usage of Lead-Acid vs Li-Ion batteries, it may dent the company’s lead business to some extent. However, lead - acid batteries do have applications in various other areas. Also, because of conversion of ICE engine to Li-Ion battery, only the size requirement of lead acid battery is gonna shrink (by 30-40 pc) and won’t lead to their replacement. Lead metal has various other upcoming applications as well like in Nuclear power plants etc. This however remains a key monitorable - IMO

However, the company’s global Mkt share is only 2 pc. Therefore has a long runway to grow

Energy cost in smelting vs recycling of lead is aprox 4:1

Energy cost in smelting vs recycling of Aluminium is aprox 20:1

Also, Gravita India uses pyrolysis oil ( Bio-crude) vs fossil fuel for recycling processes to minimise the carbon footprint

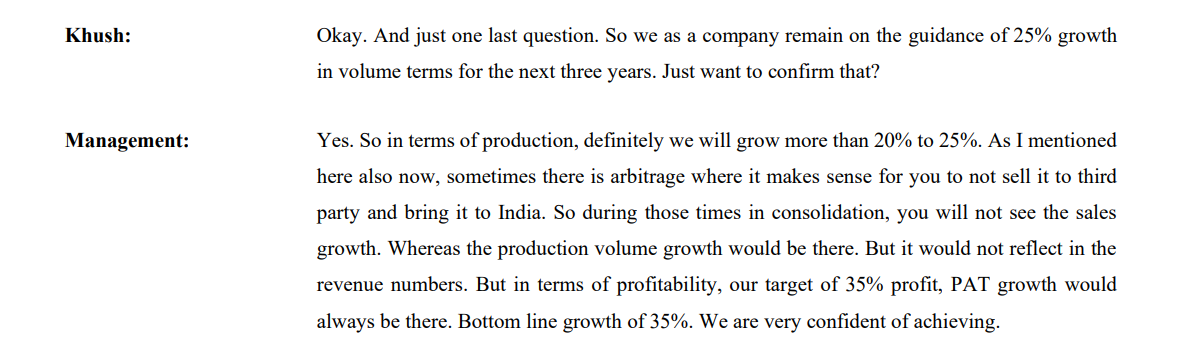

Management insisted that 25 pc CAGR growth in topline should not be a problem in near future

Management also gave a volume growth guidance of 25 pc for medium term !!!

Min ROCE tgt for the company is also 25 pc !!!

H1 capex @ 65 cr. H2 capex tgt @ 100 cr

Next yr onwards, will be spending 100 cr/annum on new verticals - like Li-Ion, Paper and steel recycling

Only 10 pc of Plastic recycling in India is done by the organised sector - a huge tailwind

Current EBITDA contribution from Aluminium + Plastic segment is around 11-12 pc of the total EBITDA

Rubber - these days is also being used as fuel. Should help improve company’s margins as the company’s rubber capacities increase

Disc: holding, may add more, biased, not SEBI registered