Gravita India- Master document.pdf (1.5 MB)

Gravita India ltd - Initiating Coverage

3 Likes

Price is moving perfectly in a long term channel. Has formed a cup and handle pattern and might break the long term channel resistance to go into price discovery mode.

Need some good earnings trigger otherwise stock might start correcting from the channel top.

1 Like

I am worried about the cyclicity of this business. It has been growing fast but won’t the cycle turn around? Won’t the slow down in the metal rally affect Gravita?

1 Like

Metal prices have no impact on Gravita. They hedge their metal exposure and focus on only conversion margin.

12 Likes

My 2 cents on Gravita:

Opportunity and Supply Chain Dynamics

The Extended Producer Responsibility and Battery Management Rules 2021 impose strict regulations on OEMs and recyclers to get more raw material and supply better output. For instance, automotive and industrial manufacturers are expected to reuse 35-40% of lead used in batteries. (source - CPCB)

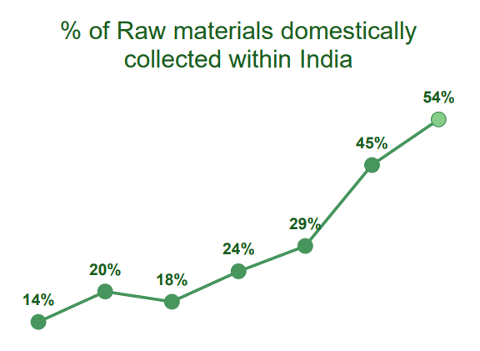

These rules were there since 2001, but apparently very poorly implemented. This has directly resulted in Gravita getting more raw material (batteries) from India:

This has triggered Gravita to increase their capacity from currently 200,000 MTPA to almost 400,000 MTPA by 2026. This will correspond to ~25% volume growth for the next 3 years.

Demand Trends

This is where things arent really blooming for them. The primary use (~80%) of Lead is in Lead Acid Batteries (LAB) which is a sunset industry. With Li-ion batteries getting affordable and much more sustainable, the shift could be imminent.

For now, the commentary of battery manufacturers and recyclers suggest that LAB are here for another decade with industrial growth (28% as per Amara Raja), use of LABs in Solar and Wind energy and small % of LABs still being used in EVs. But this evolution could be really quick.

Competition

In India where LABs are still relevant and showing some minor growth YoY, there are mainly just 2 competitors - Nile and Pondy. Though management has talked about a private Pilot industries as third major competitor. I also saw POCL (which somehow feels like a spinoff from Pondy itself), but it’s too small and in many other metal recycling solutions

One edge Gravita has over its domestic competitors is its raw material sourcing. Gravita collects almost 48% of batteries from Africa where the raw material prices are far less. For instance they have a 26% GM from their Ghana plant (there are other benefits as well like no import duty into Europe and tax benefits).

Although Pondy is a much smaller company with the same market opportunity, I feel they are at a higher risk due to being concentrated in Andhra and not able to import from Africa (shows in margins too).

Management

The management is as enigmatic as I have seen. They have made some sound capital allocation decisions to reach this spot. They have invested smartly by establishing plants in locations that help the business. Africa, Sri Lanka, and Mundra plants have relatively higher gross margins and some enjor special tax benefits (like Kathua and Ghana).

But on the other hand, management keeps looking for many other avenues. For instance, they have in the last 10 years:

-

Started a power company and closed it in a year

-

Started an IT company that has suffered a loss in every year since its inception

-

Invested in Real Estate business in a London associate of a family member

Although these things could be regular for companies of it’s size and there aren’t any glaring red flags as such!

One thing I loved about Gravita and its management is its employee friendliness. The increase in headcount and ESOP strategy is very transparent and fair.

Risks

No analysis is complete without this section. These are some risks I think the business faces:

-

Although their entire Lead inventory is hedged, the fall in Lead prices causes a corresponding loss in revenues. I consider this as deeply cyclical

-

Somewhat unpredictable future of LABs. Although the company has already grown to be a generic recycler than a Lead recycler (almunium and plastic). And more recycling products are coming up

-

Competition from unorganized sector and OEMs setting up their own recycling plants in future

-

Low capacity utilization - historically the Lead recyclers operate at ~50% capacity utilization. And since Gravita is doing a 500cr capex in setting up recycling plants, if the raw material supply isnt strong, they will operate at much less utilization level

Valuation

Although the valuations arent steep now, the stock had a strong run in the last 2 years. And with cyclicality coming in, it could make sense to wait for a down cycle.

Disc - tracking but don’t own. Investing learner, don’t take anything as gospel. Do your own research ![]()

23 Likes

Agree, at this valuation can’t rely on managements word for 25% volume CAGR. FY23 done at 17% volume growth. Which is still good, but far from the commitment. And stock is at historical high valuations if we look at non-pe metrics too. Exit multiples won’t be more that 1 mcap/sales. However there are structural changes in the balance sheet. @basumallick sir, how do you approach valuation of such companies, just want to understand your thought process and learn

Saviour in Q4 result were gains from hedging.

5 Likes

Something that I’m failing to understand here is that, why is Gravita India considered a deeply cyclical business considering that all it’s inventory is hedged?

1 Like

I can atleast tell you that their Aluminium inventory is not hedged. Also, they aren’t able to withstand substantial Lead price fall/hike on their margins even after the hedging. When Lead prices appreciates, they lose some of their margin advantage if I understand that correctly.

1 Like

add other income to margins and see the trend. hedging income sits there. Margins are pretty stable post that

5 Likes

Can you please shed some more light on how this hedging mechanism works? Or point me to some reliable source for understanding the same

Why was there no ‘Other Income’ in years before considering they started hedging in 2015 for Metal and 2019 for all it’s core inventory?

Just want to caution you guys they gave guidance in FY14 AR to achieve 1 billion revenue in 5-7 years.which they haven’t achieved it yet

Plus exclude 88 cr hedging income from 204 cr PAT to see the valuation

PE- 4337/116= 37

Not cheap on TTM PE

Plus do you think they can surpass the PAT of FY23 in FY24 assuming no other income of 88cr.

Thanks

I think we need to look at the macro changes taking place and the shift from unorganised to organised sector especially in the recycling space.

Maybe they had given those estimates in 2014 on same grounds but the story didn’t reflect in numbers.

The vehicle scrapping policy announcement was delayed.

Now this e waste policy etc, ESG norms at global level are all growth drivers. The pace at which India is now producing gadgets and we are consuming electronic devices is unprecedented.

It’s good to be cautious and see the past follies but being optimistic about future based on current trends is more important.

Please watch the link below for estimates on the recycling space.

5 Likes

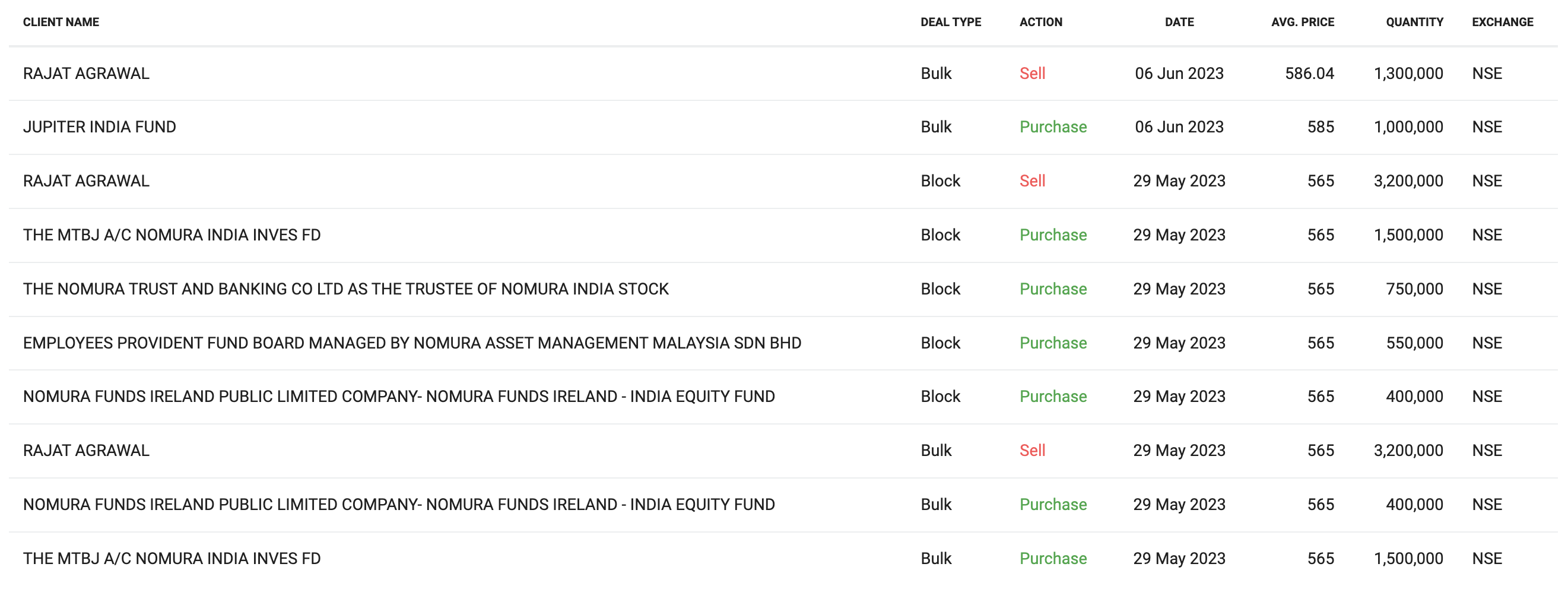

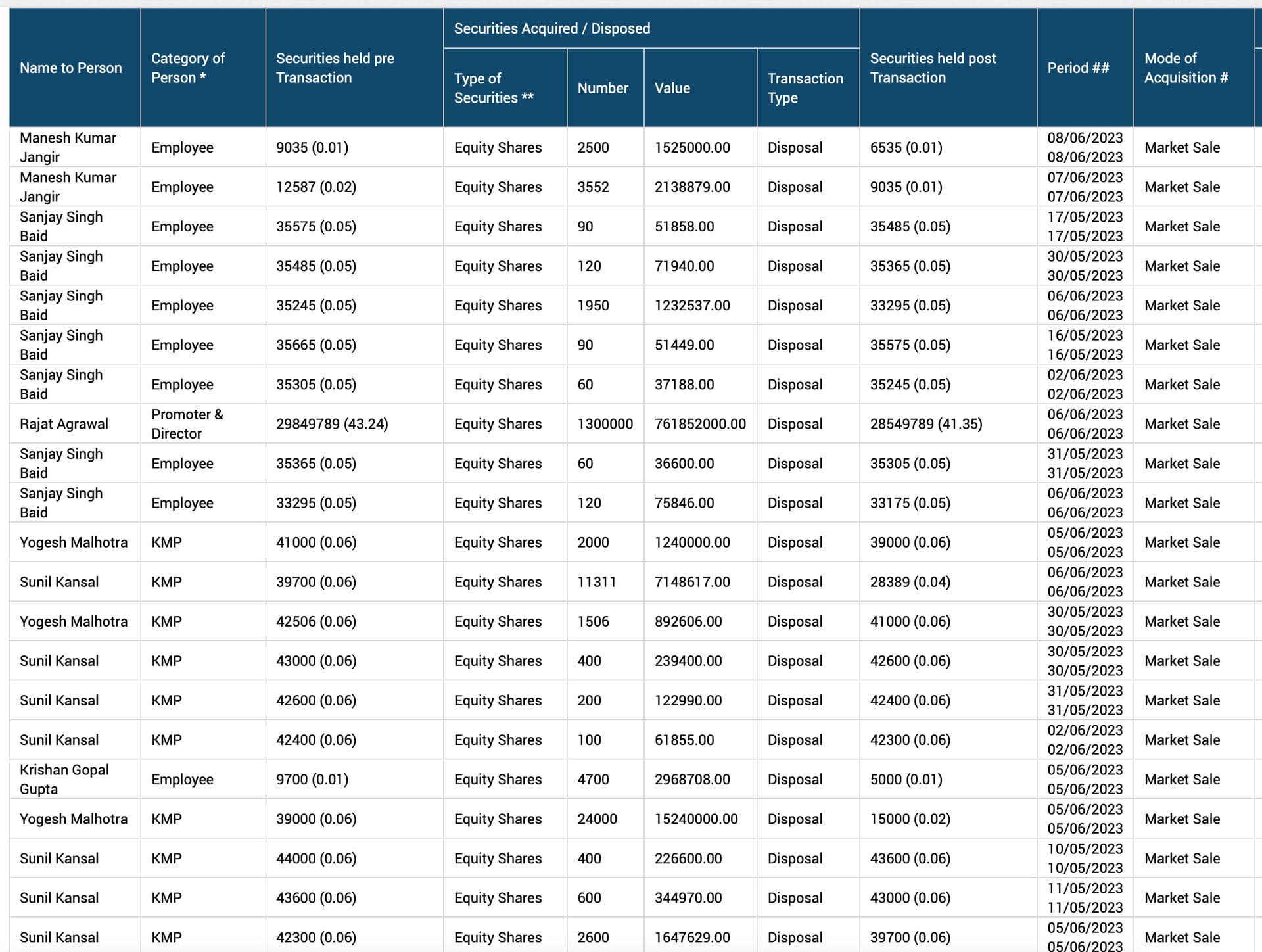

Nothing. Promoter selling can have multiple meanings and the true answer lies only with the promoters. In this particular case looks like Rajat Agrawal sold for Jupiter India fund. Maybe they wanted in and approached the management? As usually in small cap companies their isn’t much float for fund houses to buy from open market. Also some good promoters sell a percentage of stake to fund fast growth. Hope that’s the case here.

6 Likes

I am also concerned about this. Are they kind of transferring to institutions?

Can someone explain?

Regards,

dr.vikas

Don’t know why traders/investors not seeing the other side of deal. There should not be much of concern. Rather new institution entering should be taken as positive factor

3 Likes

Employees when they get ESOPs vested, they sell a part to cover the income tax payments. If u see the sale by employees is a very small qty.

2 Likes

You cant ignore "other income " for gravita since they are fully hedged on Lead

Had few questions based on the management commentary from FY23Q4 Concall. I reached out to the management for the same and sharing the conversation here.

Question 1: As per the management even in EV we require a lead acid battery to do starting, lighting, ignitions and auxiliary functions. However a lot of EV’s already exist without a lead acid battery and many have plans to completely get rid of lead acid battery going forward

Source:

- Tesla's new Model S and Model X get rid of lead-acid 12v battery, move to Li-ion | Electrek

- https://www.power.com/community/green-room/blog/why-do-evs-still-need-12-v-lead-acid-batteries

Reply from management: “Lead acid batteries will be a part of the EV’s majorly as Lithium is a scarce metal.”

This makes sense as lithium is in fact a rare metal but we will have to track going forward if majority of EV’s continue to use lead acid batteries for SLI functions or they switch completely to to lithium ion. And if they do switch completely then success with lithium ion recycling plays a key role here.

Question 2: Management said that raw material for lithium ion will not be available for next six to seven years in India. So does that mean that it is going to take Gravita at least six to seven years before it can start with lithium ion recycling? Also management says that for lithium ion recycling there is no proven technology whereas a quick Google search gives multiple companies which have been doing lithium ion recycling since a long time. Why Gravita is lagging behind in lithium ion recycling technology when it already exists?

Source:

- Lithium-ion Battery Recycling Technology | Fortum

- Lithium-ion battery recycling Escaid™ diluents for solvent extraction | ExxonMobil Product Solutions

Reply from management: "Li-ion battery recycling will take some time, as the life of Lithium ion batteries are 7-8 yrs. Also, in case of Lithium ion batteries also we would be buying the scrap from same vendors (Like Airtel, Vodafone, Amara Raja, Luminous etc) and at the same time we will be supplying to same customers (like Amara Raja, Luminous etc), so for us our eco system remains same. "

As per the concall, we have set up a pilot plant for lithium ion recycling. Does it mean that we already have the technology to recycle lithium ion batteries and just working out the fine details and processes on the plant and to set up the whole value chain will take 6 to 8 years? Or it will take 6-8 years to have enough lithium ion scrap to be recycled? Have asked these further questions to the management and waiting for the reply.

Disclaimer: Invested & Biased.

8 Likes

-

I am not a believer in a full scale EV-only thing. This is a bit of new-age hype. EVs also are not green as they claim. At best, vehicles may become hybrid. Even considering china, the nev leader, 100% nev conversation is still decade at least. longer in us and Europe, longer still in india, Africa and the rest. So plenty of Pb recycling still remains. LAB also have non Vehicle markets. Besides company is broadening it’s recycle base and will have enough time to course correct.

-

Li ion recycling chemistry is well known. Questions are about economic viability as well as waster volume threshold to ensure profitability. They have talked about this many times. In india, Li recycling will lag EV adoption. Here also plenty of time. Remember, the biz is more about reducing costs around collection which remains a moat. Recycling tech can be licensed.

-

I am a bit concerned about too fast rise in price. Many insiders probably sense this and taking this chance to offload a bit. I have pared down my holding and will add back once the prices stabilize.

3 Likes