Gravita India Q3 – 2022 concall notes:

Quarter Highlights-

Operational revenue at 557cr up 49% YOY

Indian business 63%, overseas 37%

Lead revenue up 43% YOY

Aluminium Revenue up 112% YOY

Plastics revenue up 51% YOY

Revenue growth is supported bay both growth in volume and prices

Volume growth 14% YOY to 32K MT, margin expansion on all 3 segments.

Value added products contribution - 44%

EBIDTA 54cr, 69% up YOY, EBIDTA margins at 9.7%

PAT 39cr, declared interim dividend of Rs. 3 per share

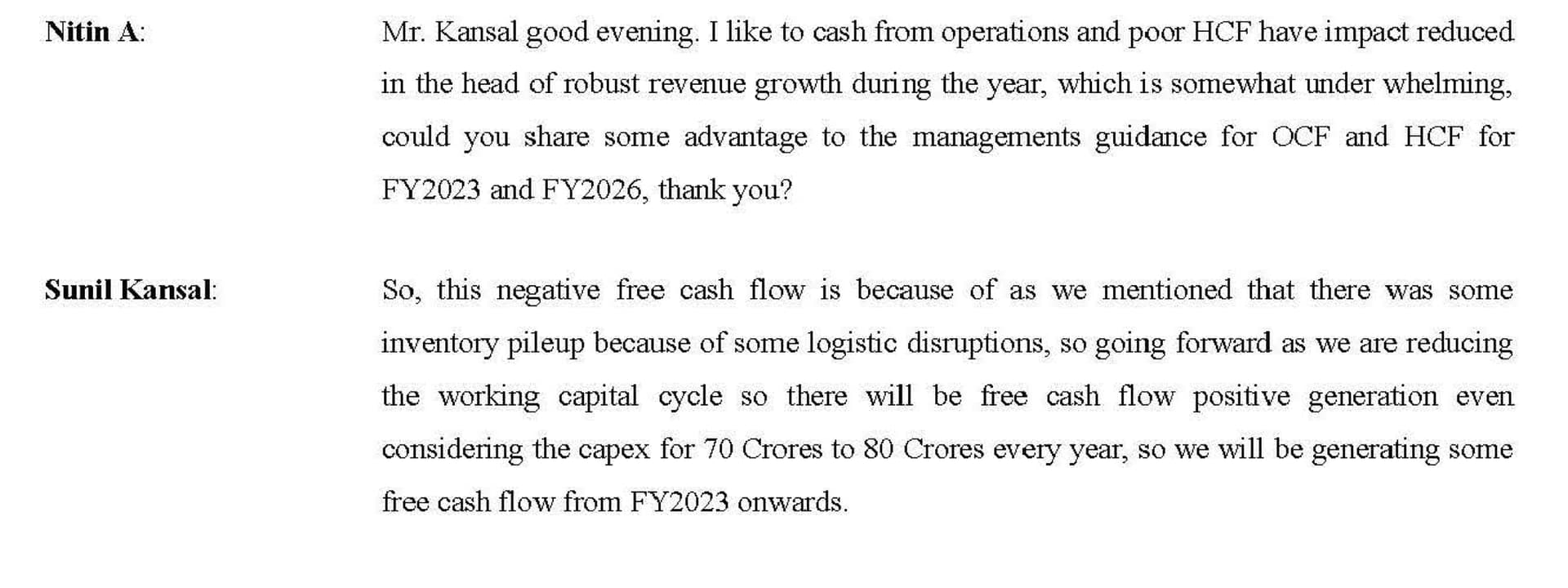

Operating cash flow in this quarter is 45cr.

QOQ volume degrowth in lead from 26.6K MT to 25.3K MT due to logistical issues in December.

Planning to increate overseas revenue, which have higher margins

Planning pilot projects in rubber and copper recycling at overseas locations

Planning to raise 300cr by QIP

On Guaidance –

Sustainable EBIDTA margin will be 8-9%, This quarter margins increased due to higher aluminium prices

Lead volume will increase up to 10K MT per month next year

Aluminium & plastics volume will remain at 3K to 3.5K MT per month next year

Volume growth shall be 10% next quarter and 30-35% next year

Target is in next 2 years to increase total capacity by 1.2L MT, which is more than 50% of current capacity

Expected operating cash flows for FY23 will be in the range of 250-300cr

Expected EBIDTA margins Rs. 20-22 per ton in long terms for aluminium

Plastics EBIDTA per ton will be around Rs. 12-13.

Capex per annum - 70-80 cr for next 2 years

ROCE is currently 20% by 2025 will try to increase ROCE to 25%, by reducing working capital cycle, using localised scrap processing, more value-added products

Debt-

Current gross debt is 375Cr including long term and short term

Long term debt will be paid in 3-4 years, short term debt will be there for working capital requirement

Indian operations-

Raw material which is scrap is increasing in India. Earlier there was 10-12% from India, in FY 2018-19 it was 25%, now it’s about 50-55%, that’s why need to expand capacity in India and overseas.

Tie ups with Amara raja, Reliance, Indus Towers, Asian Paints for collections of scraps

Plastic scraps procurement is a challenge in India.

Mundra Plant –

Started operation in December.

Mainly will do lead recycling from imported scraps.

Spent 32 cr on plant, current capacity is 19K MT, further expansions are planned at 30 cr to increase capacity up to 48K MT, which will be operational by H2-FY23.

Mundra plant will reduce working capital by 10 working days due to its strategic location.

Expected ROCE 30-35%

Chittoor-

Chittoor plant planned expansion 38K MT at 30 cr, will start operation by H2-FY23.

Expected ROCE 30-35%

East India-

Planning to put up a plant in east India by next year.

Capacity will be around 12K MT. Cost will be around 20 cr.

America –

In America there is regulation to use minimum 25% recycled plastics, gravita has expertise in food grade recycled pet, there is huge demand for food grade recycled plastics in America and prices of recycled pet is increasing every month. There is tailwind coming in this counter

Food grade recycling process cost is higher than non-food grade recycled pet

Currently there is one plastic recycling plant of 10K MT capacity, planning for one more plant of 10K MT capacity.

Africa-

Planning capacity expansion in both Ghana and Senegal, will be operational by Q1-2023.

Senegal plant currently doing lead recycling, planning to put up aluminium recycling also.

Ghana and Senegal have zero tax for 10 years, plants started recently.