2 Likes

Goldiam | Concall

a. Plans to open 150-200 stores in 5 years

b. Business expected to double in ~4 years

c. Strong LGD adoption in the US; India yet to catch up

9 Likes

Goldiam International’s Anmol Bhansali On Expansion Plans, US Business & More

5 Likes

4 Likes

Any idea why are they granting ESOPs at less than 1/6th the current market price (Rs. 389)

The Nomination and Remuneration Committee

has approved the grant of 83,333 employee

stock options to the eligible employee under

Goldiam Employee Stock Option Scheme 2024,

within the shareholders approved limit of

10,00,000 options

Exercise price per option shall be Rs. 60/-

(Rupees Sixty Only).

Ref: Intimation of grant of ESOS by Nomination and Remuneration Committee | 7 Mar 2025

1 Like

This perhaps is the first ESOP grant in the company’s history. This now when the company is very much confident of it’s future and clear road map laid ahead, they may want eligible emplyees to be part of this journey and get rewarded.

IMO, this is an enouraging step for the employees and somewhat for investors too (somewhat refers ‘increase in no. of shares which could dilute EPS’).

All in all a good step.

Disc - Invested

5 Likes

Vivek Oberoi LGD compny Solitario going for IPO… interesting development…

They also secured pre ipo funding..

4 Likes

The ongoing geopolitical tensions impacting jewellery demand in key export markets like the US, China and the G7 nations.

Exports of polished lab-grown diamonds in February 2025 dipped by 19.58% to ₹975 Cr. against ₹1,155 Cr. in the same period of the previous year.

4 Likes

Goldiam do not export loose lab grown diamond…they export lab grown diamond studded jewellery…article talks about Gems And Jewellery export decline but silent about lab grown diamond jewellery…also in terms of value decline because downward trend in natural diamond prices also.

7 Likes

This company seems proactive and knows the USA market apparently better than any LGD player from India. Let’s see if they set up manufacturing in the USA, if they do then big positive.

2 Likes

Suprised to see little correction despite the news on tariffs. What could be the reason for the same? It does seem like this move would impact margins adversely. What am I missing?

You jinxed it. But I think today was collateral damage to all the stocks.

Plus goldiam is diversifying into india with all the LGD stores

3 Likes

there’s a catch though, the management plan was to fund India store expansion from the money made through selling LGDs to US. That will be impacted. They may have to look at additional avenues for fundraising now.

6 Likes

IMO this should be seen in the context of.. firstly, decline in prices of natural diamonds as well as LGDs during the reporting period and secondly… considerable increase in Gold and Silver prices..

netting off .. the volume might have increased a bit with reasonable margin stability..below article is interesting..

2 Likes

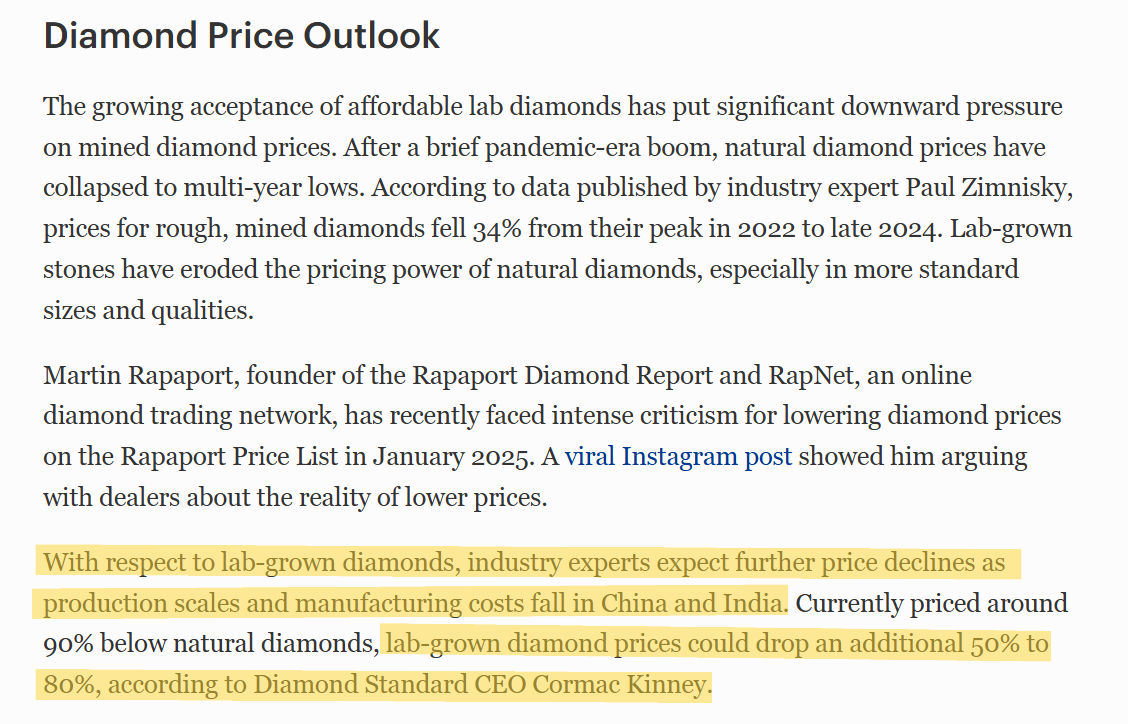

The management continues to insist that LDG prices have already bottomed out. However, the CEO of Diamond Standard anticipates that lab-grown diamond (LGD) prices could fall another 50–80% before reaching stability.

As with other technological innovations, LGDs are likely to follow the trajectory of the three A’s — Availability, Affordability, and Aspiration — to drive widespread adoption. It is entirely plausible that prices will decline to the point where LGDs are perceived primarily as fashion accessories, and there’s no strong argument against this happening.

However, I highly recommend reading this article to understand the unit economics around LGDs and the reasons why the prices might be at the bottom too.

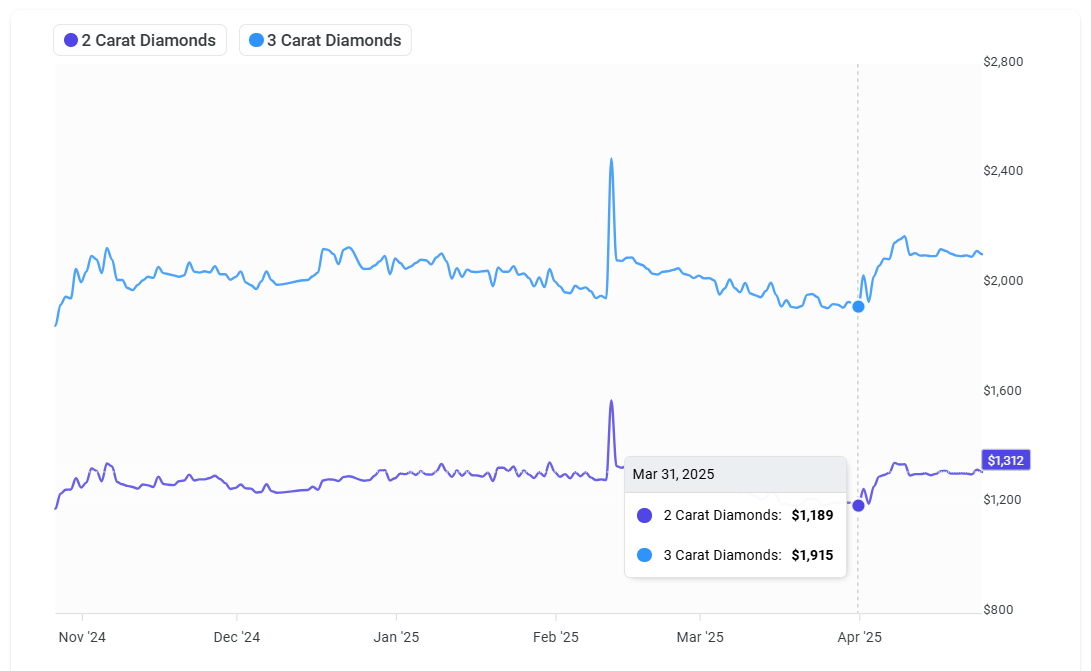

Also, LGD prices have been rising after (possibly) bottoming out in March.

4 Likes

Interesting to know that LGD prices have started rising again.

I always thought if something had unlimited supply (in the case of LGDs) then the prices would fall.

But maybe there’s more to the story. I intend to be an investor in Goldiam regardless off how prices for LGDs move.

Funnily enough De Beers recently started advertising real Diamonds - makes me think have LGDs given them competition?!

3 Likes

LGDs giving competition to De Beers would be to say the least…

- Anglo American has written down the value of its diamond business, De Beers, by $2.9 billion, dragging its 2024 results to a $3.1 billion net loss.

- De Beers, once dominating 90% of the global diamond market, is now valued at just $4 billion.

- Plans to spin off or sell De Beers — part of Anglo’s wider restructuring to fend off a £34 billion takeover attempt by BHP — may be delayed, with no significant progress expected in the first half of 2025.

However, Goldiam’s strategy to establish retail outlets in India appears fundamentally misaligned to me. There is a stark divergence between American and Indian consumers when it comes to purchasing jewelry. In the U.S., buyers prioritize design, brand value, and ethical considerations over the intrinsic value of materials, leading to rapid adoption of lab-grown diamonds (LGDs — with LGDs accounting for 36% of engagement rings in 2023, up from 17% in 2022). Jewelry in America is largely viewed as an accessory rather than an investment.

In contrast, Indian consumers traditionally view jewelry as a store of value, placing a premium on purity and material worth. Gold, deeply ingrained in cultural and financial traditions, remains the cornerstone of jewelry purchases. As highlighted by Titan Company’s Managing Director, C.K. Venkataraman, Indian consumers show minimal interest in LGDs, with a strong preference for natural diamonds backed by authenticity and lasting value.

This is simply because Indian consumer is not aware about the LGDs at the moment. But as awareness about LGDs increases, there is a significant risk that Indian consumers may not only resist paying premiums for lab-grown diamonds but may even reject LGD jewelry entirely unless it is sold along with the substantial intrinsic value of gold.

I would have invested in Goldiam had they not started operating retail outlets already, and this has always bugged me. I think they’re too much in a hurry when there is not a single positive sign of Indian consumers accepting LGDs, and I highly doubt we will. Unless of course, the prices decline so much that even Indians can start considering LGDs as an accessory.

5 Likes

I’ve been invested since the 200 levels primarily because of their buy-back strategy.

But your points about the general Indian consumer mentality makes sense, however if you notice where they’re opening stores, those places house top 0.5% of Indian population (or even less).

Mumbai is really rich. People there would definitely consider jewellery as an accessory rather than investment, this is not for the general audience.

Opening up a store in Mumbai airport, wow, so not like Indian mentality right?

but if you travel to the Middle East, you see so many jewellery stores in the airports - it’s a very flashy thing for people to do.

Of course you and I from a middle class mentality might struggle to understand, lol but it’s very real.

Like always, I could be wrong.

3 Likes

Hi Naval,

My 2 cents to your last para-

-

Like in every business, backward or forward intergration on most ocassions enhances the margins after Capex is done at the most probable time. Goldiam getting into forward integration where they wouldn’t depend on others for the finished product and established supply chain has only helped them to swiftly reach to the end consumers.

-

Being probably the only listed LGD company who does it’s own production and has maximum revenue from exports has thought to diversify into domestic market to enhance margins (tariffs not taken into account)

-

Their 1st store at Borivali West broke even with first month of it’s operations only increases the confidence and therefore attests the demand too.

-

Like everything in the universe, the LGD prices too going through cycliality. How far it would drop and for how long is anyone’s guess.

IMO the LGD market is here to stay and since this only will be a sort of fast fashion, it’s going to be volume game and pure execution skill, whosoever cracks it will be frontrunner and Goldiam is in this business since decades.

Disc- Invested and can be biased

9 Likes