Can someone help me with current capacity of Goldiam per annum in terms of carats and how many reactors do they have ?

The promoter is continuously selling. Sold yesterday as well. He knows what the public doesn’t know. So if the business is so good why has he been continuously selling over the past year? Thoughts?

1 Like

Promoter buying is always positive but promoter selling can never be always negative…he has right to reap fruits of hardwork…better than manipulating…

5 Likes

They have an order book of 270cr executable in 3-4 months - Strong for H2

1 Like

A very Important point made.

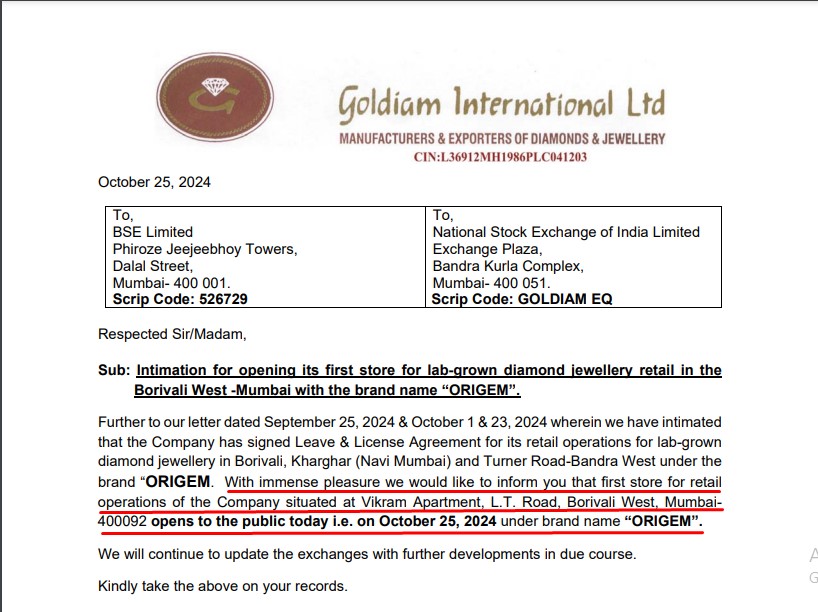

Retail initiative of lab-grown diamond jewellery in India. Marking Goldiam’s entry into our own country into retail

On Trent LGD entry

8 Likes

Goldiam: Intimation for Opening of Third Store for Lab-Grown Diamond Jewellery Retail at Turner Road, Bandra West, Mumbai Under The Brand Name ‘ORIGEM’.

6 Likes

Good set of Q3 nos. from Goldiam:

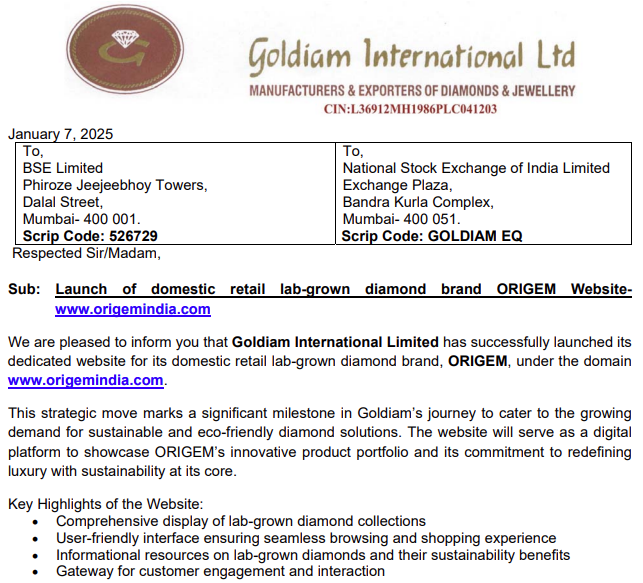

3 retail stores ‘ORIGEM’ started operation in Mumbai…3 more to open before March 25.Going to target Delhi NCR post that…Co. recently established its online sales channel with the launch of

Q3 Topline up 41%…Also order book size is ₹ 1750 mn as on December 31, 2024 compare to ₹ 1150 mn as on December 31, 2023…Hence expecting good Q4 growth.

Discl. inested…5% of portfolio.

8 Likes

Q3 FY 25 CONCALL SNAPSHOT…

B2C: 3 stores stared in Mumbai, 3 more to open before 31st Mar 2025.Post that, going to target Delhi NCR and Bengalore market.

All the three stores opened in mumbai has good response and already achieved break even at store level.Retail gross margin northward of 40% and comfortably well above some LGD start ups due to 100% backward integrated such as LGD manufacturing, jewellery design and manufacturing.Also online channel www.origemindia.com has good response and already getting one or two online orders per day…also many customers first visit website and then visit store for actual purchase.

Geographical Expansion: Three orders already dispatched to Australia.Also, shipped some samples to gulf region but not any significant orders yet.

One question was about stock exchange doubtful/negative perception about diamond company’s balance sheet…Management said they do not sell even a single loose diamond and no shipping to Dubai or Hong kong…so no question of round tripping or something fishy…they have highest standard of governance and generated as well as distributed real cash in the form of dividend or buy back over last many years…

Futuristic guidance: Hope to double topline in next four years…

Digging existing US customers(One is US based largest diamond jewellery retailer) and trend is customers shifting upward in terms of diamond caratage from 3 / 4 carat to up to 10 carat…

Wrote as per memory…will edit once transcript out…

Overall positive personal view…

Discl. : Invested 10% pf portfolio…biased.

8 Likes

As per recent commentary both US business and India retail venture currently witnessing good tail winds.

Only thing that didn’t add up is growth projection for combined entity.

India retail venture expected to do 150-200 stores in next 3-5 years which implies 700-1000cr sales.

US business they are saying expected to penetrate deeper per store with higher carats being sold.

Current sales 800 cr.

So in next 3-4 yrs sales doubling (as per their commentary) with India retail contribution means very subdued growth for US business which is not in sync with commentary around LGD and higher sales per store.

Evaluating growth to assess valuation at 40 PE.

Would be interesting to hear others comments

4 Likes

Conservtive guidance is always good.

4 Likes

Priyanka Gill quits Kalaari Capital to launch lab-grown diamond brand

3 Likes

Did they mention about how much Sales is every store adding ?

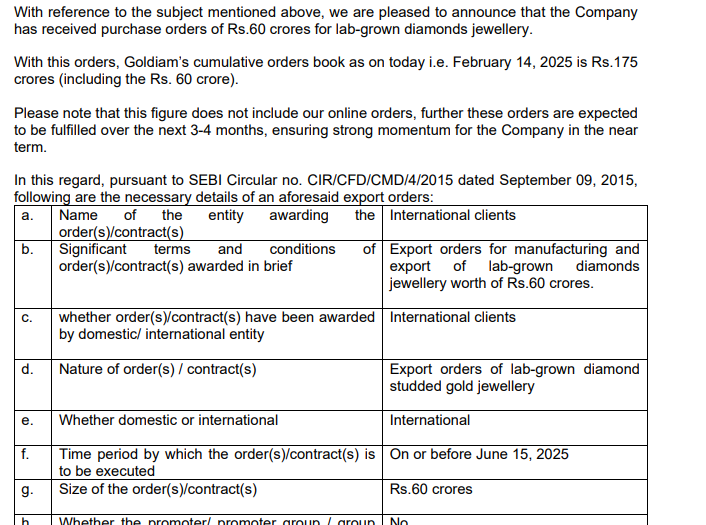

Goldiam International received export orders worth Rs.60 crores for lab-grown diamond jewelry, with a cumulative order book of Rs.175 crores.

2 Likes

Guidance

![]() Aims for 10-15% export revenue growth and to double total revenue in 4 years including ORIGEM retail expansion.

Aims for 10-15% export revenue growth and to double total revenue in 4 years including ORIGEM retail expansion.

Lab grown diamond jewellery market

![]() Demand shifting from natural diamonds to LGDs due to cost-effectiveness & identical properties.

Demand shifting from natural diamonds to LGDs due to cost-effectiveness & identical properties.

![]() Lower carat LGD prices are stable, no price drop in last two quarters for <3 carat stones.

Lower carat LGD prices are stable, no price drop in last two quarters for <3 carat stones.

![]() Customers now prefer larger LGDs (5-10 carats vs. earlier 1-5 carats).

Customers now prefer larger LGDs (5-10 carats vs. earlier 1-5 carats).

India Retail Venture – ORIGEM

![]() Crossed Rs.20 Mn in topline with 3 stores in 2.5-3 months itself

Crossed Rs.20 Mn in topline with 3 stores in 2.5-3 months itself

![]() Launched B2C brand ORIGEM, with 3 stores in Mumbai, including a flagship in Bandra.

Launched B2C brand ORIGEM, with 3 stores in Mumbai, including a flagship in Bandra.

![]() 3 more Mumbai stores by March 2025; aiming to be the largest LGD retailer in Mumbai.

3 more Mumbai stores by March 2025; aiming to be the largest LGD retailer in Mumbai.

![]() Post-Mumbai, expansion planned in Delhi NCR & Bangalore.

Post-Mumbai, expansion planned in Delhi NCR & Bangalore.

![]() E-commerce website launched: www.origemindia.com.

E-commerce website launched: www.origemindia.com.

![]() Targeting total of ~20-25 stores by Dec 2025.

Targeting total of ~20-25 stores by Dec 2025.

![]() Expansion model: company-owned, company-operated.

Expansion model: company-owned, company-operated.

![]() Monthly breakeven per store <Rs 30 lakhs per month.

Monthly breakeven per store <Rs 30 lakhs per month.

![]() Gross margin expected >40% post-discounts.

Gross margin expected >40% post-discounts.

![]() Store operations already breaking even for 3 stores which are operational (excluding HO expenses).

Store operations already breaking even for 3 stores which are operational (excluding HO expenses).

![]() ORIGEM offers buyback policy, aligned with major Indian jewelers.

ORIGEM offers buyback policy, aligned with major Indian jewelers.

US - B2B Business

![]() Presence in large retailers & independent stores via wholesale partners.

Presence in large retailers & independent stores via wholesale partners.

![]() Estimated >3,000-3,500 stores carrying Goldiam’s products (vs. 1,500-2,000 two years ago).

Estimated >3,000-3,500 stores carrying Goldiam’s products (vs. 1,500-2,000 two years ago).

![]() Focus on increasing per-store sales via high-end fashion & larger LGDs. On the B2B side, GIL has already fulfilled an order for an Australian retailer & aims to get more orders going forward.

Focus on increasing per-store sales via high-end fashion & larger LGDs. On the B2B side, GIL has already fulfilled an order for an Australian retailer & aims to get more orders going forward.

Other KTAs

![]() Certification: Driven by customer demand; lower certification on entry-level products. Costs passed to customers.

Certification: Driven by customer demand; lower certification on entry-level products. Costs passed to customers.

![]() Geographic Expansion: Initial shipments made to Australia, samples sent to Middle East.

Geographic Expansion: Initial shipments made to Australia, samples sent to Middle East.

![]() Inventory: 74% of finished jewelry stock is with customers; focus on inventory turnover.

Inventory: 74% of finished jewelry stock is with customers; focus on inventory turnover.

![]() Credit Terms: Wholesalers: 150-180 days ; Large retailers: 60-120 days ; Online (customer websites): 7-30 days

Credit Terms: Wholesalers: 150-180 days ; Large retailers: 60-120 days ; Online (customer websites): 7-30 days

![]() E-commerce: 20-25% of B2B sales from online, operating on negative working capital.

E-commerce: 20-25% of B2B sales from online, operating on negative working capital.

![]() No celebrity brand ambassador planned currently; may consider after reaching 15-25 stores

No celebrity brand ambassador planned currently; may consider after reaching 15-25 stores

3 Likes

Its derived… basically expected 3 yr payback for store capex of 3.5cr-this implies yearly pat of 1.2cr which implies PBT of 1.6cr yearly…, Assuming 10% depreciation of 50lac store refurbishing capex, implies 5lac depn…EBITDA required is roughly 1.7cr…12 lac monthly operational expenses (derived from 30lac revenue with 40% Gross margins currently allowing store to break even). Gross profit roughly required is 1.8cr… At 40% gross margins revenue required per store yearly is 4.5-5cr.

at 50k avg ticket size, this requires on an avg 1000 pieces to be sold yearly implying 80-100 per month (3 per day)… with weekend probably deriving 40-50% of weekly sales… means 8-10 pieces on weekend…

6 Likes

Are there any numbers of how much the other retailers generate from one store, would be a good variable for comparative advantage , it would be great if you can share the numbers if any.

Odd that there were no questions in the concall around the impending Tariffs by Trump. Or did I miss it ?

Edit: There was a question, they didn’t clearly answer the Tariff part.

1 Like