Quick Snapshot

CMP: 100.85 as of 27th June ( vs Average Buyback price of 154 on 26/2/2020)

Market Cap: 223Cr

P/E : 4.77

Div Yield: 6.45%

ROE: 11.58%

52W H-L: 184.8/72.2

Website:

India: http://www.goldiam.com/

International: https://www.goldiamint.com/

History

-1986: Started export of cut and polished diamond and studded gold jewelry

-1994: Company was converted into a Public limited company

-2007: Company entered into JV with Russian major retailers with its subsidiary Diagold

-2008: Company retail brand in silver jewelry segment “OLA” entered into a tie-up with leading groups like Total mall, Bengaluru, DLF Group for Kiosks, Aditya Birla more, etc

-2015: Reported Net profit > 20Cr for the first time and has been able to maintain that ever since.

-2019: Company introduced its first line of Lab-grown diamond jewelry in the US market. They were among the first exporting company to driven in this segment.

Lab-grown jewelry is almost 50% cheaper than the same quality mined diamond and has a better operating profit margin.

Segment

The company mainly operates on two-segment

(1) Jewel Manufacturing which contributes 95% roughly of company revenue and

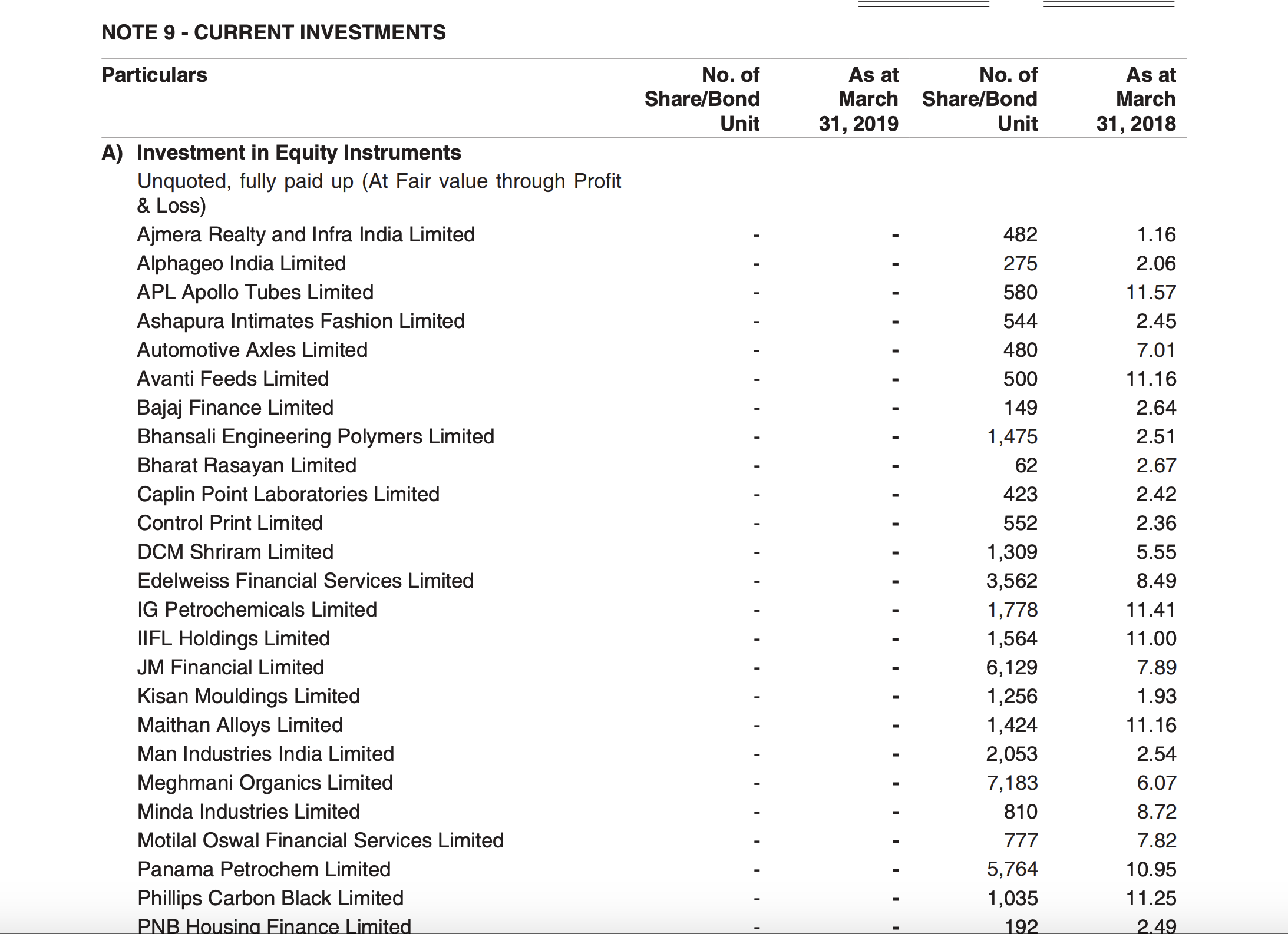

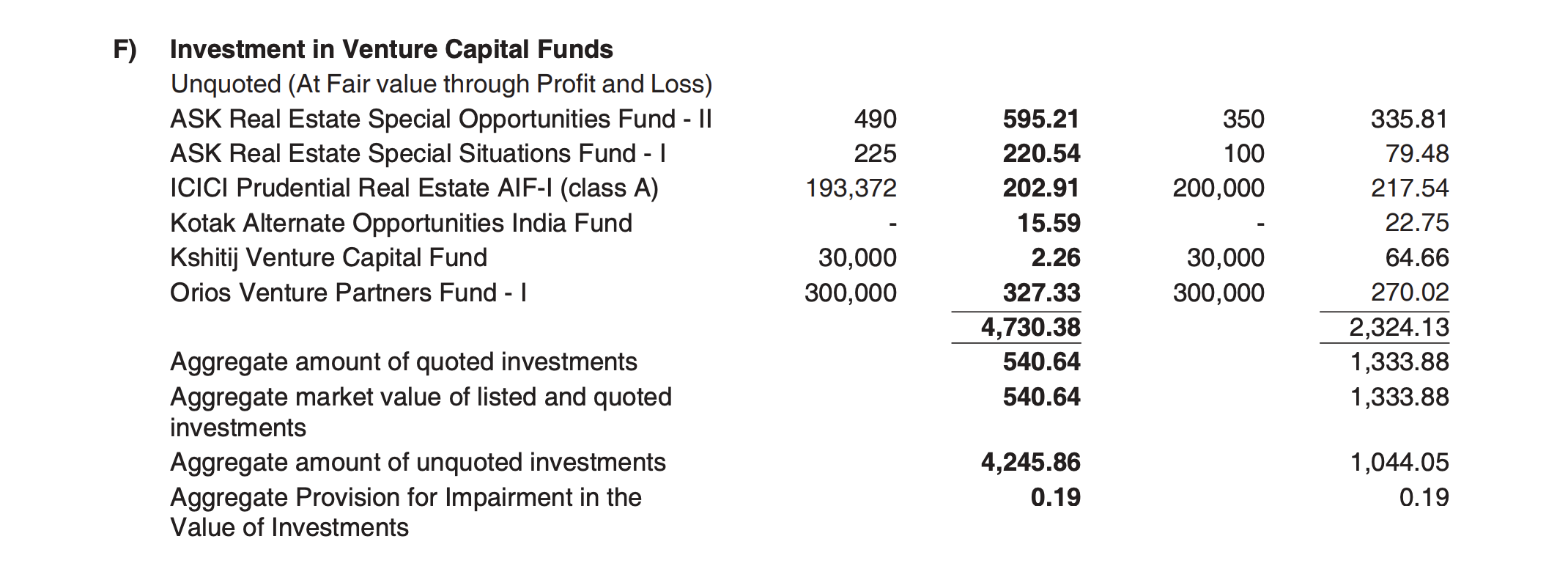

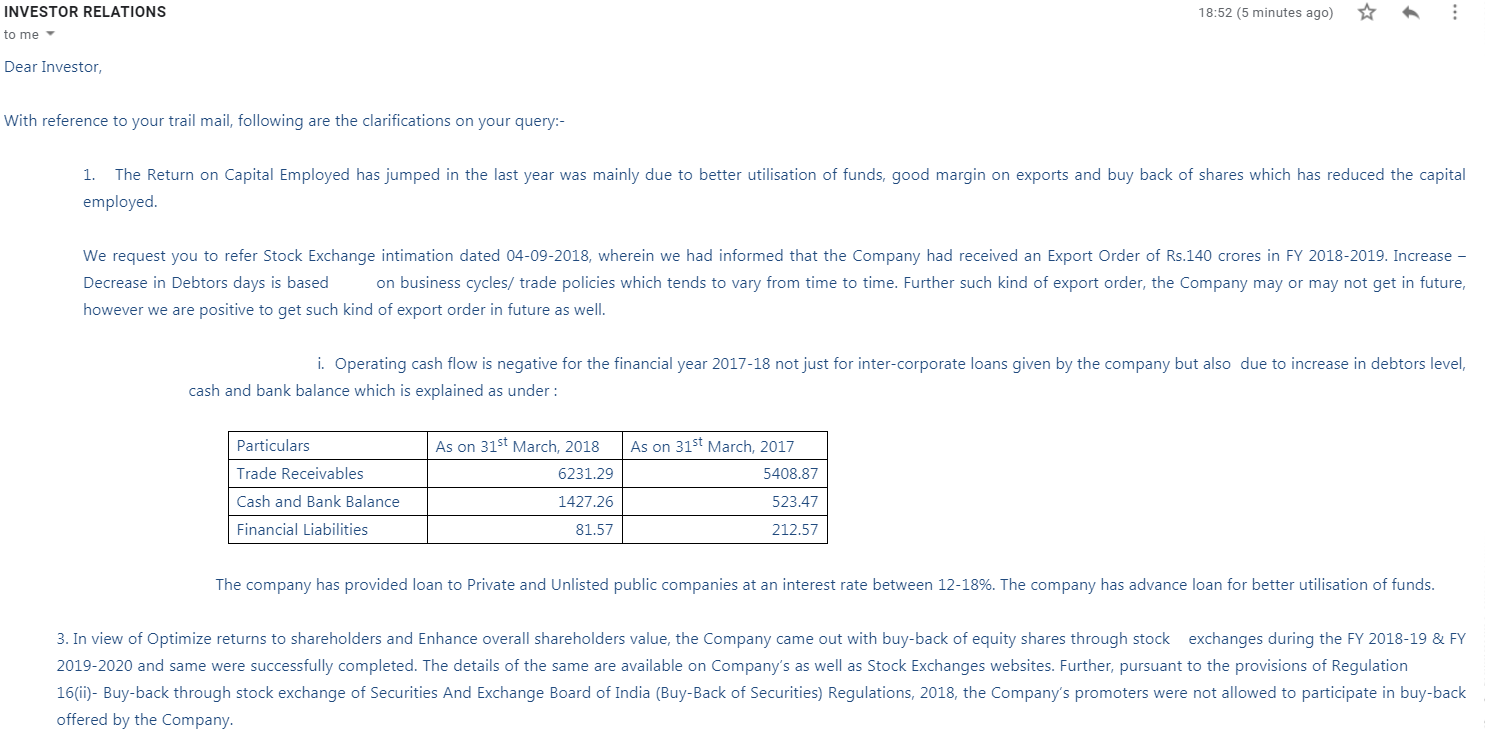

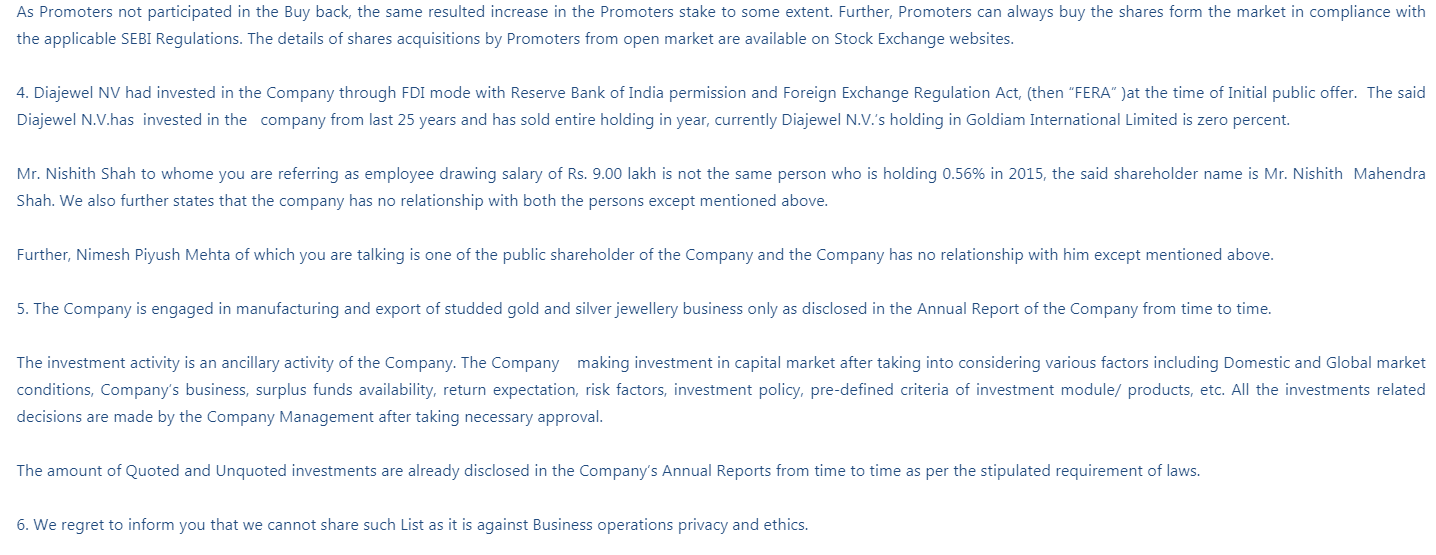

(2) Investment activity

The Company is manufacturing high quality, luxurious and creative diamond jewelry and exporting to USA, Europe, and other countries. The Government of India and several other trade bodies have awarded the Company for its contribution to jewelry trade and being a pioneer and a role model in this industry.

Following are the achievements:-

• Outstanding Export Performance for studded Jewelry from EPZ for the years 1992; 1993; 1994;1996;1997;1998 and 1999 by Gem & Jewellery Export Promotion Council.

• Late Mr.Manhar R. Bhansali, Chairman of The company was awarded “PIONEER OF THE YEAR” award by IDCA (Indian Diamond & Colorstone Association) on June 5, 2010.

Below are some of the Jewelry company specialize in:

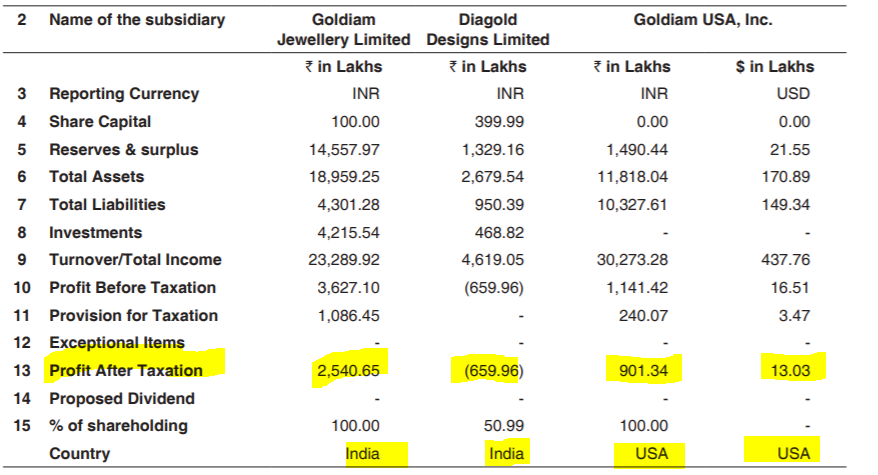

The company operates via below subsidiary mainly

In terms of a subsidiary, we can see that its subsidiary has a strong performance, particularly it’s USA business whereby it’s generating almost 9Cr out of its 43cr total revenue thereby supporting its diversified model quite well.

Its Indian business generates the majority of its revenue via Export and the USA continues to be a prime export market. This was the major reason for this stock being picked up as given the global pandemic, I do believe sectors like jewelry will take time to recover and companies which are the majority in the export market like the USA will be able to recover first.

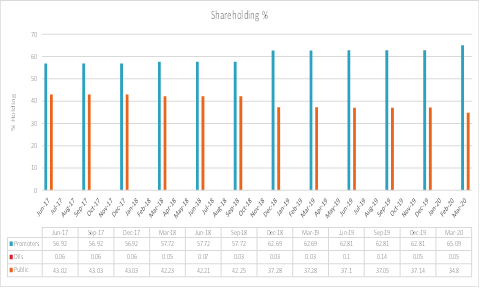

Promoter Holding

-

Promoter holdings have increased by 2.2% in the last one quarter and promoter holding is quite good at 65.09% as of March-20 at average buyback price of ¬155.

-

Promoters have taken a very good shareholder-friendly approach of paying good dividends and doing continuous buyback giving faith to people on its model.

- In last 3yrs, it has increased its shareholding by >8% through consistent buyback in the markets.

- Star Investor Ramesh Damani has a holding of ¬1.3% on this company at an average price of 85.

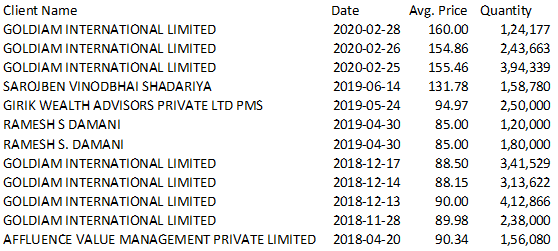

Buyback history

The company has adopted an extremely consistent shareholder-friendly approach to buyback the shares throughout the last few yrs.

As we can see the the average buyback price of the company has been in the range of 90-155 which gives strong support to the current market price esp a decent buyback in Feb around 155 levels.

Financials

-

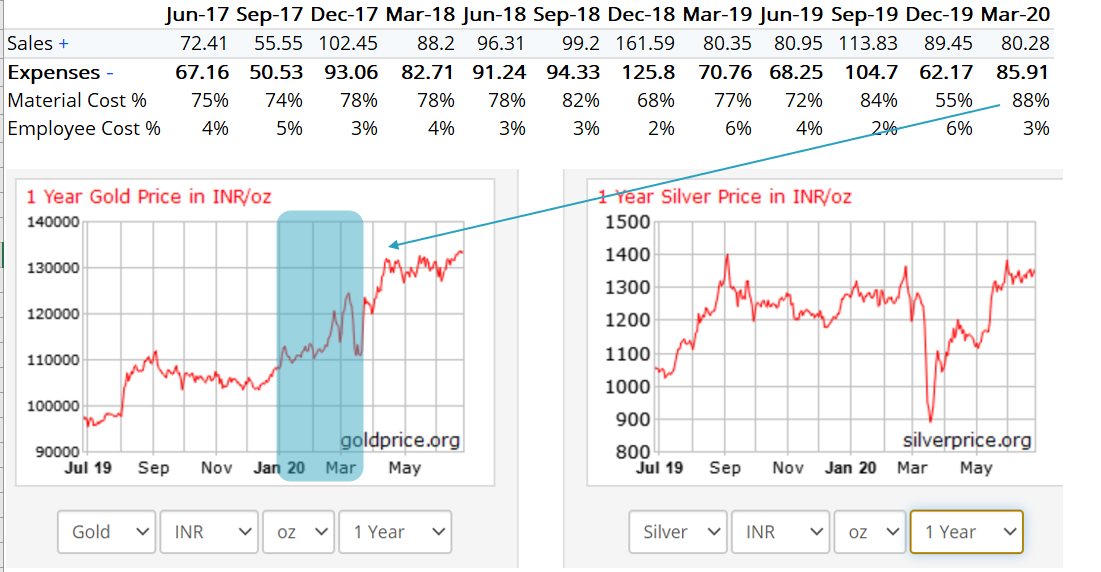

Company profit was under pressure from COVID this year and rise in Gold prices in the Q4 where it resulted a poor result. In spite of that YoY profit is the highest ever

-

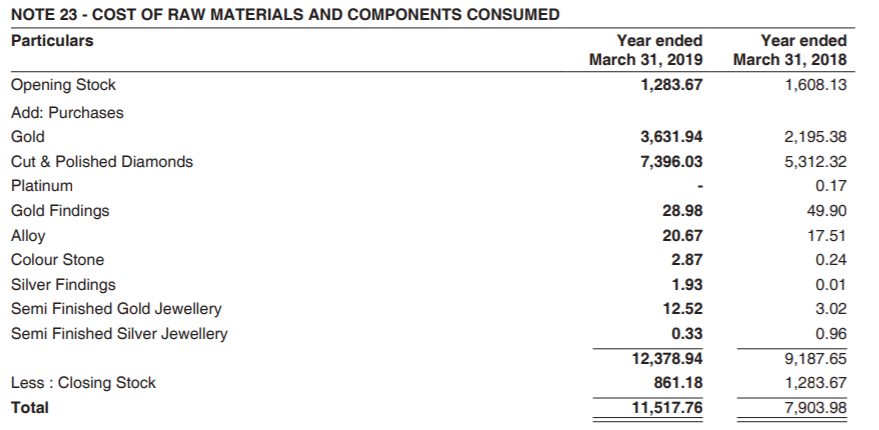

Raw material cost breakdown as we can see from the company annual report of 2019 is mainly driven by Gold which accounts for roughly 64% of the cost while Diamonds accounts for roughly 32%

We can clearly see the impact of high gold prices due to pandemic on the cost of the company. I expect the company to report similar Profit in Q1 of the year as compared to Q4 recently due to COVID situation and gold price still being high however as compared to other companies this company is well placed to capitalize on the growth.

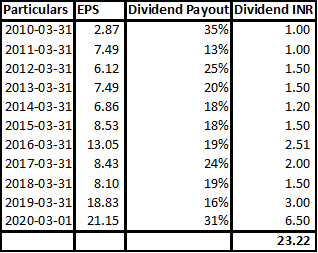

The company has also paid a good dividend of 23.22 in the last 9yrs. It’s currently trading at a Dividend yield of 6.5%. These dividend payments are expected to continue given the growth of the company and consistent positive cash flow.

It must be noted that company is Debt-free and it has managed to do so by repaying its loan every year from internal accrual. This is so important in times like this whereby fixed cost has killed so many sectors and business models.

As highlighted below, you can see the company has managed to use its strong internal accrual to

(1) repay debt and get debt free

(2) do buyback in both the years to increase shareholding

(3) Pay generous dividends to shareholders

Future growth drivers :

-

Increasing range of products like Lab diamonds which makes it one of the first export-oriented company to enter this segment. Given strong margin and cheaper than mined diamond, it will be interesting to see how the company further grow in this space

-

The development of a new export is key. The company has heavily relied on USA model for its growth. It’s now making progress in domestic India retail market and also the European market

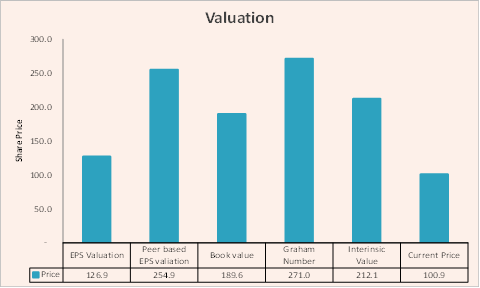

Valuation as per different methods:

Looking at the valuation right now, we do have a chance of more than 50 to 100% upside. These evaluations are made under certain assumptions which are given below

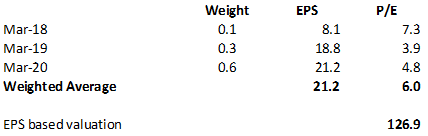

- EPS based valuation:

Goldiam International has been historically been trading at a P/E of 6 as an average over the last 2-3 yrs. Lowest P/E has been 2.9 vs 4.8 its currently trading at and highest has been around 15.

We have a fairly good upside of ~25% on this stock-based upon EPS remaining the same over the next few yrs ( which is quite a conservative assumption) and P/E reverting back to somewhat normal of 6 times instead of 4.8 times currently more inline with the past historical average. This also takes into account the COVID impact of the last quarter which is the same as COVID impact in Q1 this year.

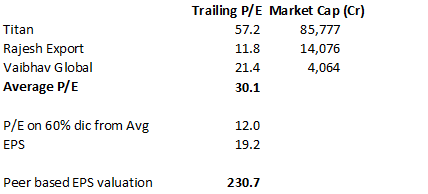

- Peer-Based Valuation

Again we have got a 130% upside against Peer-Based valuation under a conservative 60% discounting to average P/E of the Peers. This I have done as I have highlighted risk earlier of COVID impacting consumption

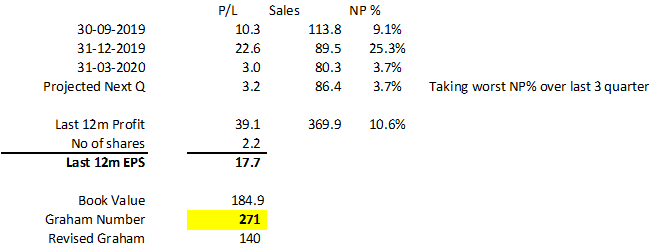

- Graham

Looking at the Graham, we will come up with a much higher valuation of INR 271. However, the Graham formula has certain flaws like P.E of 15 and P.B of 1.5 is assumed

this is obviously going to show the stock as massively undervalued. However, the core concept of Graham is still relevant, blind usage of the formula without understanding will not yield a correct result like below its yielding 271

In the below, I have modified the Graham formula to take a P/E of 6 which given the historical range of 2.6-15 and Median of ~6 P/E looks to be a much more reasonable and conservative P/E and P/B is assumed to be 1 given a growing company should always trade at least equal to its book value.

Given the modified Graham formula, I get a price of 140 which already takes into account next quarter Q1 company will just report 3.2cr P&L. It still shows an upside of 40% in relation to the current stock price.

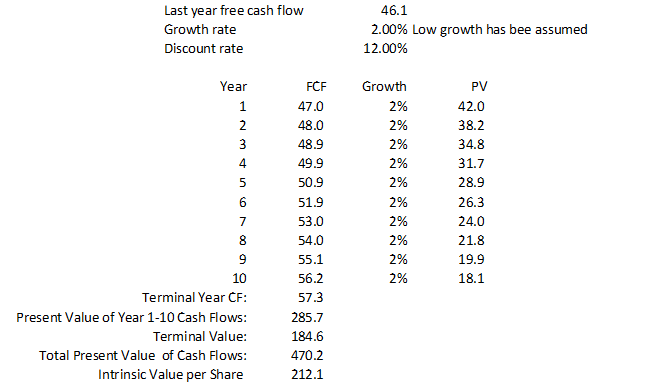

- Intrinsic value

Intrinsic value also is very good given a very conservative assumption of 2% growth in Cashflow and 12% discount.

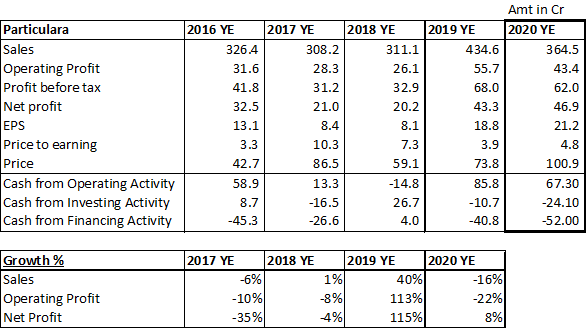

Below is the historical growth rates in Sales and Profit of Goldiam. Given the impact on this year due to COVID it hasn’t been able to register growth we witnessed in FY 2019

- Book value approach

Looking at the book value, this stock is trading much lower than its book value as compared to its peers. In this sector, a normal trend is to see P/B of ¬4-10 times. Due to the recent fall in price, its P/B has plunged to 0.55 times which is very cheap.

Risk:

-

High Input prices like Gold always make things challenging for the company given its size to pass the effect of that to its customer. This was clearly visible in the Q4 result where it actually reported a loss for the first time in the last few yrs in a quarter. Times are unprecedented and will be interesting on how soon the company can come out of COVID. However given its large focus to export market i.e. the USA where it derive its revenue, it is well placed in my view to recovering quickly as compared to local players

-

Currency risk arises from exposure to foreign currencies and the volatility associated with therewith. While the Company hedges majority of its receivables, any sharp fluctuation in currency is likely to affect the cash flow of the Company as well as its profitability

-

Since the company mainly operates in the USA market, it faces challenges of a slowdown in the economy and risk of government policy changes.

Overall its a company with good historical growth, strong brand, and presence in the USA market with which it has benefited massively. With its past growth and recent crash in price from 180 levels to just 100 currently, it has now gone to become one of the lowest P/E in the Jewel Industry. Also, it must be noted that being a Debt-free and Cash rich company is very important during these COVID times and this company is a rare company with perfect parameters. Company new initiative of Lab Diamond is exciting and need to be seen how consumer takes it. Lastly, it’s rare to find a company that is consistent and shareholder-friendly esp in the micro-cap sector. With its consistent buyback and good dividend along with now it being debt-free, it’s expected to continue.

I have invested in this at the current market price of 100 for long term purposes given the above.

Disclosure:

-

I have an investment in this stock so my views might be biased. I request you to take your own judgment call before you make any investment in this name.

-

I am not a SEBI registered analyst so don’t have any recommendation service/Paid service. It’s an educational website that is just meant to share the analysis I do before I invest.