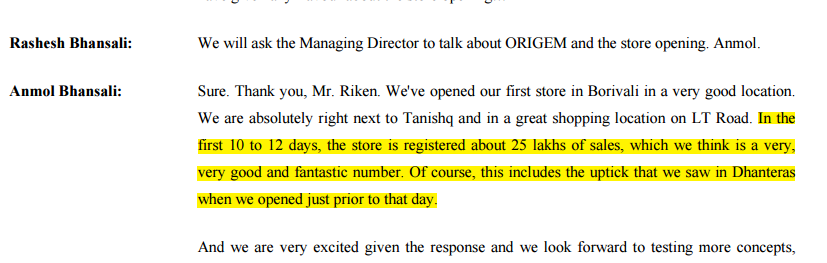

I would consider it as a case of exceptionalism and the management is also aware of it. Diwali is the best time of the year for all the jewelers, and their first store was launched just before the day of Dhanteras. Perfect location as well to launch the first brand outlet, but wouldn’t consider it as the evidence of acceptance and high demand from Indian consumers.

Breakeven level of revenue is around INR30 lakhs to INR35 lakhs per month per

store. Q4 concall will give a much more realistic understanding of the demand.

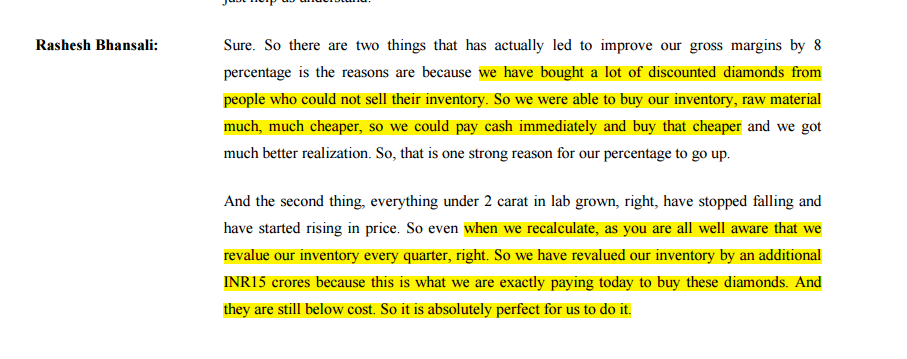

They’re also buying LGDs from manufacturers who are unable to sell. Not only this but they’re also inflating their inventory after buying LGDs on discount.

3.Regarding storing of wealth is concerned…both LGD and Natural diamonds jewellery use same gold and once the market stabilizes, prices of LGD will always be at a particular discount to natural diamond…

Also , Goldiam has life time buy back guarantee

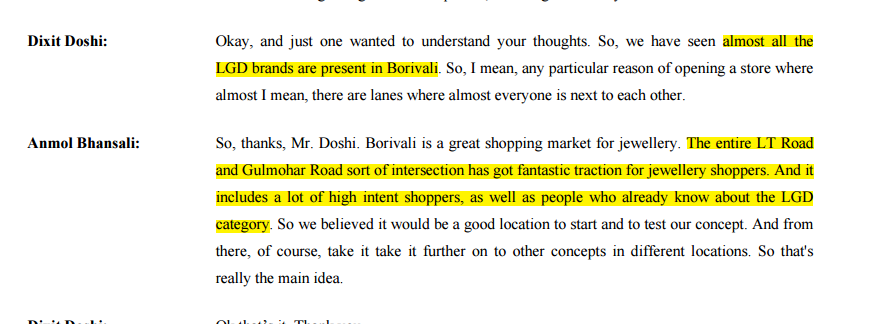

Goldiam is into fashion jewellery , their target customer must be young high earners who are knowledgeable also…anything western get most of the time acceptability here…

De Beers ad flashing on electronics and print media shows they are feeling the heat…

Lets consider Goldiam LGD retail venture as startup only…they have around 300 cr cash on the books and what a better way to start a venture than spending money on dividend or buyback?(LGD business has gross margin of 40 to 45%)if they succeed…company will step on the next level …better thing is they are going slow in expansion…will spread only after getting positive response for sure…we cann’t be sure of success or utter failure…let the data of a few quarters come and then we can be sure…

The Company is raising funds, possibly to expand Origem’s retail presence much faster than it is right now.

42 companies have emerged in the LGD retailing space—5-10 seem to be funded. Maybe the company is raising money to capture good retail spaces since so many have emerged. That said, the company had ~Rs. 275 crores of cash and investments in September 2024 —so they don’t really need a lot of cash!!

Can anyone please elaborate the Moat side of Goldiam

Since last few days i have been seeing ads on my instagram account of jewellery brands selling LGD jewellery with high discounts and all. A few days back I saw an interview on cnbctv18 where Anmol Bhansali, MD of Goldiam told that the approx cost to setup CVD diamond growing plant is 1-1.2 crores per reactor. This cost is very less so what if this LGD jewellery industry gets crowded with many LGD jewellery players.

Also over 80% LGDs which Goldiam uses for manufacturing their LGD Jewellery are purchased from third party so they only grow around 20% LGDs In-house.

so, I just wanted to understand how will they survive the B2C market if large players enter this segment aggressively. What if others start manufacturing LGD Jewellery for export after buying LGDs from third party sellers.

In their traditional core B2B business, they have a strong MOAT. AS per the company, it’s the design and distribution which sets them apart from peers. So whatever the diamond prices, they would get the sort of same margins while exporting Gold jewellery to mainly USA. So far, so good.

Now, in B2C, declining LGD prices are a problem. Not only it encourages competition, it would be lower the realisation and hence absorption of fixed cost. But in one of concalls, they said that they were buying most LGDs from the market than manufacturing themselves as the wholesale price was same as their cost of production. Now, I suppose Goldiam, being an established and strong player, will have low cost structure in manufacturing LGDs. If the wholesale price is the same, it means LGDs prices are very close to their cost of production. Which should mean prices won’t decline much from here, otherwise many LGDs growers would have to shut shops because it would become unsustainable. So, I feel Goldiam will keep getting LGDs at rock bottom prices for medium term atleast, and then it’s upto the demand side of the story in B2C whether they can sell at good prices basis their attractive designs, or the competition becomes too much and they feel the pain.

Clarification on the backward integration via EDL vs procuring from others – The larger caratage diamonds which go into fine jewellery and are drivers of higher profitability & margins – come from in-house, via EDL. This is roughly 30% as per a recent call. What they procure from outside is basically addressing the commoditized side of the business – (smaller diamonds or accessory diamonds).

What sets them apart - Strong product development & design skills: Almost all of their products that are sold in US are in jewellery format and not in loose LGD. A new player cannot manufacture LGD jewellery but will have to make substantial investments in product development & design before exporting to US markets. Goldiam has a first mover advantage.

Distribution network (with large retail partners in USA and other markets):

Omnichannel presence – Around 25 to 30% revenue comes from online / ecommerce – almost double that of industry benchmark. Negative working capital business; where they get paid in 7 to 30 days whereas their purchase of diamonds has a longer credit period.

B2C business – Need to monitor how the story unfolds; watch where the prices tend to stabilize and the impact due to declining prices..

Website (while its early days still) gives a good snapshot of variety of jewellery and wide range of designs that they are offering– By Style, by stone shape, by price-point, etc.

This blog posted a year earlier perhaps in this topic - has some good insights for a new investor looking to study this company ..