The following is an article in Bloomberg in relation to the steep decline in prices of rough natural diamonds and the growing volume of lab grown diamonds in the diamond export from India. There are multiple indications now (IMO) that LGDs are going to take away significant volume from natural diamonds. How much of that shift benefits goldiam considering the immense competition from Gujarat belt, only time will tell.

The article:

Diamond prices are in free fall in one key corner of the market

One of the world’s most popular types of rough diamonds has plunged into a pricing free fall, as a growing number of Americans choose engagement rings made from lab-grown stones instead.

Diamond demand across the board has weakened after the pandemic, as consumers splash out again on travel and experiences, while economic headwinds eat into luxury spending. However, the kinds of stones that go into the cheaper one- or two-carat solitaire bridal rings popular in the US have experienced far sharper price drops than the rest of the market.

The reason, according to industry insiders, is soaring demand for lab-grown stones. The synthetic diamond industry has paid special attention to this category, where consumers are especially price sensitive, and the efforts are now paying off in the world’s biggest diamond buyer.

The shift doesn’t mean engagement rings are about to go on deep discount — the impact is limited to the rough-diamond market, an opaque world of miners, merchants and tradespeople that is several steps removed from the price tags in a jewelry store.

However, the scale and speed of the pricing collapse of one of the diamond industry’s most important products has left the market reeling. Now, the question is whether the plunging demand for natural diamonds in this category represents a permanent change, and — crucially — if the inroads made by lab-grown gems will eventually spread to the more expensive diamonds that are typically dominated by Asian buying.

Industry leader De Beers insists the current weakness is a natural downswing in demand, after stuck-at-home shoppers sent prices soaring during the pandemic, with cheaper engagement rings having been particularly vulnerable. The company concedes that there has been some penetration into the category from synthetic stones, but doesn’t see it as a structural shift.

“There has been a little bit of cannibalization. That has happened, I don’t think we should deny that,” said Paul Rowley, who heads De Beers’ diamond trading business. “We see the real issue as a macroeconomic issue.”

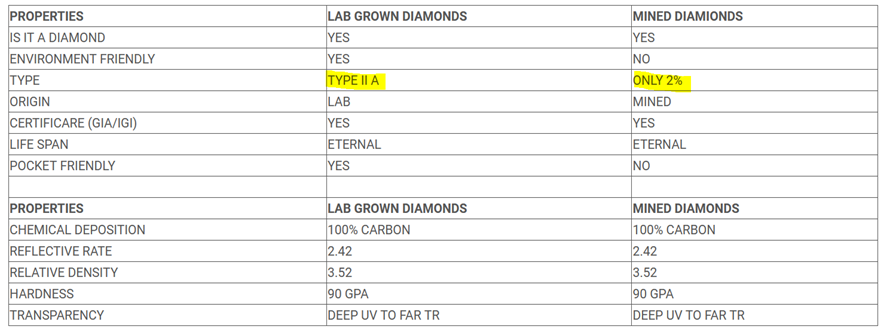

Lab grown diamonds — physically identical stones that can be made in matter of weeks in a microwave chamber — have long been seen as an existential threat to the natural mining industry, with proponents saying they can offer a cheaper alternative without many of the environmental or social downsides sometimes attached to mined diamonds.

For much of the last decade the risk remained unrealized, with synthetics eating away at cheaper gift-giving segments but making limited headway otherwise. That is now changing, with lab-grown products starting to take a much bigger bite of the crucial US bridal market.

De Beers has cut prices in the category by more than 40% in the past year, including one cut of more than 15% in July, according to people familiar with the matter.

The one-time monopoly still wields considerable power in the rough diamond market, selling its gems through 10 sales each year in which the buyers — known as sightholders — generally have to accept the price and the quantities offered.

De Beers typically reserves aggressive cuts as a last resort, and the scale of the recent price falls for a benchmark product is unprecedented outside of a speculative bubble crash, traders said.

In June 2022, De Beers was charging about $1,400 a carat for the select makeable diamonds. By July this year, that had dropped to about $850 a carat. And there may be more room to fall: the diamonds are still 10% more expensive than in the “secondary” market, where traders and manufacturers sell among themselves.

De Beers declined to comment on its diamond pricing.

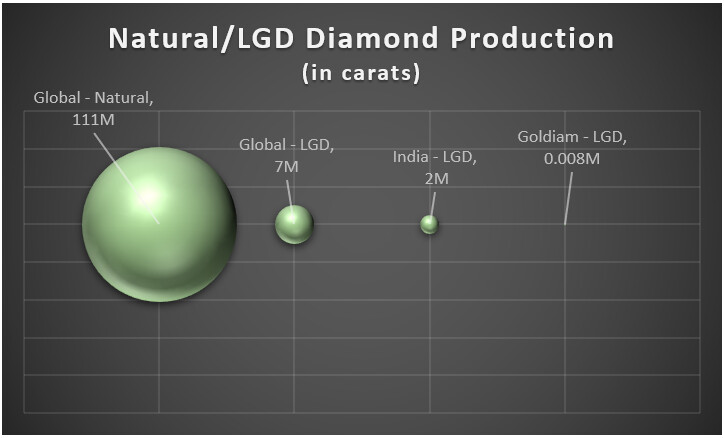

One of the clearest signs of the traction being made by lab-grown diamonds is their share of diamond exports from India, where about 90% of global supply is cut and polished. Lab grown accounted for about 9% of diamond exports from the country in June, compared with about 1% five years ago. Given the steep discount that they sell for, that means about 25% to 35% of volume is now lab grown, according to Liberum Capital Markets.

The impact on De Beers was clear in the first half. The Anglo American Plc (AAL)’s unit’s first half profits plunged more than 60% to just $347 million, with its average selling price falling from $213 per carat to $163 per carat. Its August sale was the smallest of the year so far.

De Beers has responded by giving its buyers additional flexibility. It’s allowed them to defer contracted purchases for the rest of the year of up to 50% of the diamonds bigger than 1 carat, according to people familiar with the situation.

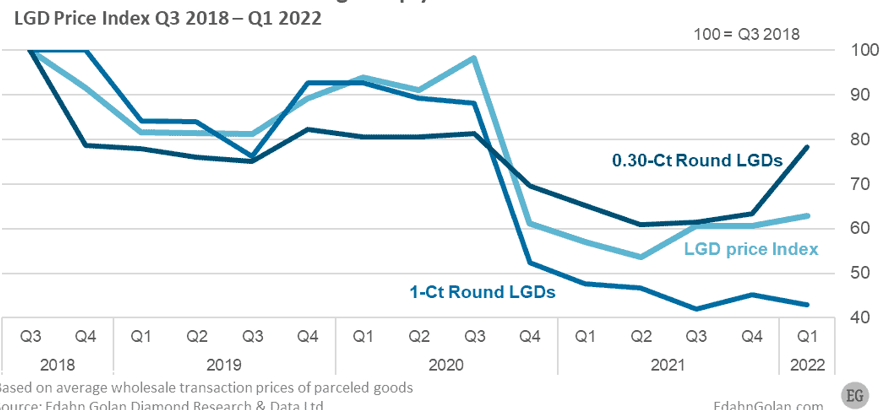

While lab grown diamonds are currently hurting demand for natural stones, the upstart industry is also suffering. The price of synthetic diamonds has plunged even more steeply than that of natural stones, and are selling at a bigger discount than ever before.

About five years ago, lab grown gems sold at about a 20% discount to natural diamonds, but that has now blown out to around 80% as the retailers push them at increasingly lower prices and the cost of making them falls. The price of polished stones in the wholesale market has fallen by more than half this year alone.

De Beers started selling its own lab-grown diamonds in 2018 at a steep discount to the going price, in an attempt to differentiate between the two categories. The company expects lab-grown prices to continue to tumble, in what it sees as a tsunami of more supply coming on to the market, Rowley said. That should create an even bigger delta in prices between natural diamonds and lab grown, helping differentiate the two products, he said.

“With the increase in supply we’ll see prices fall through the price point and reach a level where, long term, it does not compete with bridal because it comes too cheap,” said Rowley. “Ultimately they are different products and the finite and rarity of natural diamonds is a different proposition.”

(Bloomberg)

https://www.bloomberg.com/news/articles/2023-09-03/lab-grown-gems-are-crashing-prices-for-one-key-type-of-diamond?utm_source=newsshowcase&utm_medium=discover&utm_campaign=CCwqGQgwKhAIACoHCAow4uzwCjCF3bsCMJyV3QEwv5_4AQ&utm_content=bullets