Here is a very old discussion (1999) between Chetan Parikh and Utpal Sheth on Goldiam International.

Goldiam – Adding value to the Invaluable, the no.2 studded diamond jewelry exporter

Mr. CHETAN PARIKH: Utpal, can we come to some specific picks that you have identified. Can you tell us something about Goldiam International, a stock you have been recommending lately?

Mr. UTPAL SHETH: Goldiam is an obscure B-group company on the Bombay Stock Exchange. It is into the business of jewelry, which is a very recent business, just 8-9 years old. When I say jewelry business, I mean the standardized automated jewelry design making as opposed to the traditional hand set jewelry. Goldiam is the no.2 jewelry exporter from India. No.1 is a company called Intergold. Goldiam has had a fairly impressive compound annual rate of growth from jewelry sales. Although the sales growth rate visible in the Profit and Loss Account is nowhere as impressive. That is because Goldiam cannibalized its traditional business which is diamond processing.

Jewelry is a high value added, fashion product for the western markets.

Five years ago, Goldiam sales had a very large component of diamond sales. In FY00, it has a zero component of diamond sales. Given that it is such an obscure company, everybody thought that the management might not be honest & transparent. Being in the diamond business inherently leads to such lack of credibility, since the business as a whole has had many mal-practices in the past. Also, investors do not realize the true difference between diamonds, that is a low value added cyclical business, and jewelry, which is a high value added, stable service business. Jewelry is a fashion product for the western markets.

Better growth, better margins in the jewelry business as compared to the diamonds business

Goldiam designs 70-80% of its aggregate sales output. So, it is not a contract manufacturer. The quantum of value addition is very significant as compared to diamonds. The operating margins for the diamond business would be in the vicinity of 6-7% whereas, the operating margin in the jewelry business is twice that number. Jewelry exports from India are growing at a very fast pace. I mean we are talking of over 20% compound growth rate in dollar terms against a 6% compounded growth in diamonds. India has an inherent labor cost advantage in jewelry making, but then so do many other countries.

With own designs, diamond studded jewelry in India has significant competitive advantages . . .

What is so special about India in the field of jewelry making? In the studded jewelry field, India has a huge advantage. This is not just labor cost advantage but another advantage is sourcing of diamonds since it has an existing base of ancillary diamond producers, diamond-polishers, which is not the case, for example, in China. So although China can be a great center for pure gold jewelry making, China can never be a great source of studded diamond jewelry because the sourcing costs will be high & the sourcing skills are absent. Further, sourcing hurdles lead to larger lead times.

The order processing time for Goldiam for diamond studded jewelry is in the vicinity of 1 month while it would take a Chinese studded gold jewelry producer approximately 20 days just to source the diamonds. Even if he stocks them then he is talking of far greater investments in his working capital combined with the risk of diamond price fluctuations, which will render him non-competitive in this business. Therefore, I believe that studded gold jewelry in India has a big competitive advantage, which is borne out by the fact that this segment has grown at a compounded rate of 20% for the last 5 years. Given the strength of the business model, we believe that the external opportunities are large making it an attractive business. The number of domestic players are so few that we believe the sustainable competitive advantage of Goldiam both from an international perspective as well as domestic perspective will last for quite some time to come.

. . . but still far from owning brands

Having talked about the business dynamics, Indian jewelers are far from branding. I don\’t think that this is going to happen anytime in the next decade. They do not have the critical mass to do this. Goldiam\’s FY00 sales are just Rs.1 billion and a branding exercise cannot be sustained unless we are talking of a size of Rs.5-6 billion in the jewelry business.

The key strength in this business is the ability to continuously compress delivery times, avoid exposure to gold & diamond price volatility, travel up the value chain by selling first to the wholesalers, distributors internationally, then to the large retail chain stores internationally & finally to launch your own brand.

Goldiam is moving up the value chain – Selling to J C Penney . . .

Has Goldiam made any efforts in traveling up that value chain? We think so. Goldiam started out tying up with an intermediary in international diamond jewelry business and is now selling to several international wholesalers & distributors.

Has Goldiam been able to move beyond these distributors? Yes, Goldiam has struck a tripartite agreement between itself, an intermediary and J C Penney, a very large and well known US retail chain. J C Penney buys $1 billion plus of jewelry per annum. As of today, close to 40% of Goldiam\’s output goes to J C Penney via this tripartite arrangement but that amounts to only 1% of J C Penney\’s aggregate annual gold jewelry purchase. It also sells to Sears, and hopes to sell to Wal-Mart in the near future. In the latest collection of “Hint of the Holidays”, the latest catalogue by Hezelberg, a leading jewelry chain in the US, 4 out of the 5 displays on the cover page are Goldiam\’s designs.

We believe Goldiam can significantly expand its market share. We also believe that Goldiam will be able to sell to several other retail chains over the next few years. So we think the external opportunities are large. This is a product which can be marketed only to the US and not to the European segments, as the European segment is far more up-market and far more fashion conscious.

To get into some detail, Goldiam has expertise in what is known as invisible settings. The traditional jewelry has gold to hold the diamond in place so that the setting of the diamond is visible. What Goldiam does is invisible setting which is a higher plane of jewelry making wherein it cuts the diamond with a laser and then welds the diamond with a laser so you cannot see any gold holding the diamond which enhances the visual impact of such jewelry.

. . . Selling Platinum jewelry

Besides this particular skill, Goldiam is now planning to move into platinum jewelry. As of now in the global market platinum jewelry is a fraction of the gold jewelry market. But, the future clearly is in platinum. Platinum jewelry has the potential to grow at a far greater pace over the next 4-5 years. The largest market for platinum jewelry incidentally is Japan and not the US. Therefore, if Goldiam can make a successful transition into platinum jewelry for which it has already made the necessary investments, then the growth rates will only accelerate.

De-risking the business model

In the process, Goldiam will have de-risked its business dramatically both in terms of geographical, product and customer diversification. Platinum is a harder metal as compared to gold. It is far more difficult to stud on platinum and it is much more difficult to achieve invisible setting on platinum. Goldiam claims that it will be able to do invisible diamond setting on platinum. If Goldiam can do that, this will put it in a different league. Goldiam has spent no more than Rs.25 million for the platinum jewelry plant and the first full year\’s turnover from this project is anticipated to be in the vicinity of Rs.200-250 million.

Mr. CHETAN PARIKH: Do you think that Goldiam has the skill set to go ahead and make this change to platinum jewelry? It is a different market, it is not a market to which they have been traditionally exposed and so what would be the marketing strategies?

Mr. UTPAL SHETH: Initially, Goldiam will enter the existing markets, mainly US, through the existing distributors while it will have to appoint new distributors to enter new markets like Japan. Effectively, Goldaim will, to some extent, leverage on its existing distribution channels. And to that extent Goldiam will have lesser entry barriers. Tapping other specialist distributors will not be very difficult given the track record Goldiam has. But over a period of time Goldiam should pass the acid test of being able to sell directly to the retail shops. And when it does that, it goes into a different plane of operating margins.

Objective evidence of focussed management

Mr. CHETAN PARIKH: Couple of other questions that I have. Can you give us just a brief background on the management? You said that there is not much to distinguish many Indian managements in the jewelry business. So what would be your assessment of the management?

Mr. UTPAL SHETH: There is not much to distinguish between the Indian managements in the diamond business. In the jewelry business, strictly speaking, there have been only 2 or 3 successful players. As I told you, the no.1, Intergold; is owned by B. Arunkumar and the no.2 is Goldiam. Goldiam is run by a young guy called Rashesh Bhanshali. His father Mr. M.R.Bhanshali is in the diamond business and was among the top 5 at one point of time. However, Rashesh has always focussed on jewelry business & not on diamonds. Our degree of comfort with this management is not very high, but when we passed them through the test of objective evidence, we found that this management has over $7 million lying in its EFC account (External foreign currency a/c).

Historically, all managements who played truant, have not held cash in the balance sheet. These guys have held cash on the balance sheet. The lead manager for the IPO was DSP Merill Lynch. Goldiam had announced a buy back few months ago and this scheme is shortly closing. Even for the buy back, DSP ML is the lead manager and we believe they would have done their due diligence.

Insight Asset Management has got certified reports from SEEPZ which state that Goldiam is the second largest jewelry exporter from SEEPZ. There have been no custom infringements at SEEPZ by this company, which leads us to believe that there is no objective evidence of any malpractice. However, as of now the stock markets have tarred this company with the same brush as the diamond business.

Goldiam\’s management is focussed on consistently moving up the value chain and de-risking its business. We find all this to be quite impressive. Even the financials are excellent.

Compelling valuations – less than 2x prospective FCF, and less than 1x FY01 EPS, net of cash

Mr. CHETAN PARIKH: Can you highlight the financials and the valuation of the company?

Mr. UTPAL SHETH: Ok, presently this company has sales in the vicinity of Rs.1 billion for FY00, a growth of 25% over the previous year. Goldiam has quite a bit of extra space at its existing location and can expand capacities at very low incremental costs. The kind of profitability it achieves has been constantly improving, from an operating profit margin of mid-single digits a few years ago to 12% now. This vindicates our contention of their moving up the value chain.

When they enter platinum jewelry, the margins will move up further. Apart from the raw material costs, the overheads of Goldiam are under control. So while there is a labor cost arbitrage in one sense, it is not a labor-intensive operation. If you see the manufacturing facilities of Goldiam, you can clearly observe that they are using the state of the art machinery. They are on the skill-intensive part of the business and not the labor-intensive part. The bottom line for the company has been growing and it has consistently generated substantial sums of free cash flow. At the current price of Rs.58, the stock is available at less than 2x prospective free cash flow in FY01.

Mr. CHETAN PARIKH: In fact, I went over you notes on the company. I fully agree with you that even if you take the price of Rs.58 and you take out the cash of Rs.44 per share that is on the balance sheet, the effective price that you pay for the business is just Rs.18, which is less than the forecast EPS for the next year. It is generating large free cash flows, zero debt and is growing rapidly.

Mr. UTPAL SHETH: Yes and I am certain that this company will go in for dividend pay out exceeding 20-25% and if they do that I am getting a 8-10% tax-free dividend yield.

Valentines, Marriage anniversaries, Birthdays & Christmas will keep coming

Mr. CHETAN PARIKH: A concern here is that would Goldiam be able to withstand a downturn in the US caused by a stock market crash or any other factor?

Mr. UTPAL SHETH: Goldiam\’s jewelry is not targeted to be on the high end. It is a mass market item used by working Americans. While one cannot rule out some impact of a crash on the US market, I do not think that it would be severely affected by any such downturn. Importantly, Valentines, Marriage anniversaries, Birthdays & Christmas will keep coming.

Incomparable with comparables

Mr. CHETAN PARIKH: Milleniums too, at least this year. Utpal, I wanted to ask you something about the valuation of this whole sector. You know I was just looking at it. PE ratios for the whole sector are quite low and this includes the jewelry manufacturing cos. Goldiam\’s OPM while higher than most peers, it is lower than Shantivijay and the valuation case for Shantivijay looks more compelling. You know anything of Shantivijay?

Mr. UTPAL SHETH: Yes, Shantivijay is probably the highest value added jeweler in the country. But all of it is hand made studded jewelry. Over the last two years, Shantivijay has had an exceptional deal on an emerald sale. If you exclude that, then the profitability and the valuation of Shantivijay is actually higher than Goldiam. Also the scaleability of Goldiam is far superior to that of Shantivijay. Shantivijay will always remain a small niche company. The kind of growth rate that will be visible in Goldiam will be far superior.

Goldiam is not exposed to any commodity price risk at all

Mr. CHETAN PARIKH: Utpal, gold and diamonds form a very significant portion of the total cost and inventory of Goldiam. Does it not run any risk on price variation in these commodities?

Mr. UTPAL SHETH: Goldiam carries a negligible inventory and all the inventory is against booked orders. As soon as Goldiam gets an order for jewelry, it hedges itself by booking gold and diamonds immediately. Any way, the processing cycle is less than a month. Effectively, Goldiam is not exposed to any commodity price risk at all.

Mr. CHETAN PARIKH: What about debtors?

Mr. UTPAL SHETH: All debtors are backed by irrevocable LCs, so there is no credit risk. Sales under the tripartite arrangement that we talked about earlier are Cash-on-Delivery and hence, debtors are likely to remain quite low even in the future.

Diversion of funds not likely

Mr. CHETAN PARIKH: There are some investments that are there in the company. They are not very large or material. But the interesting point is that there is an investment of 10 shares of Goldiam Information Technology ltd. That is not much. It is 100 bucks but does this signal that the company is planning to make forays into software field & would the company\’s funds be ever diverted for that and do the promoters have any prior knowledge of IT?

Mr. UTPAL SHETH: We specifically asked this question to the management and the management has assured us that there will be no transfer of funds from this company into any other business venture. Also, given that the management has Rs.350 million lying in the bank account, if at all they were to fall to such temptations, I am sure there were many opportunities in the last 3 years. The management has committed to us that even the small quantum of investment in the balance sheet will be divested off as the company is very clear that it will focus only on jewelry.

Jewelry is a business of credibility

Mr. CHETAN PARIKH: Does the company have any Internet strategy?

Mr. UTPAL SHETH: No, for having an Internet strategy, the company will have to ensure a brand image first. Secondly, the logistics of managing this will be very difficult. The company might create a web site wherein it will display its designs, which will open it up to other customers. But I think the company is far, far away from selling on the Net.

Mr. CHETAN PARIKH: Utpal, I know you have sort of answered this but I want to highlight this because it appeared in the 26th Oct\’99 issue of “Think Tank” of The Financial Express and they have a report on the diamond industry. This is a paragraph I would like to quote “What is even more worrisome for India is a fact that through the joint ventures, which have been set up, the Chinese would first utilize the Indian marketing expertise and then break-off. Another major cause of concern is that Chinese are also venturing in to jewelry. India with a miniscule presence in the global $70 billion industry is even more vulnerable here. Remember the Chinese don\’t have to depend solely on import of gold. China is one of the top gold mining country annually producing about 150 tons of gold”. Any comments?

Mr. UTPAL SHETH: As I told you China has a great lead on India in terms of pure gold jewelry, but they are far, far behind in terms of studded diamond jewelry since sourcing diamonds will remain a large competitive edge for India.

Mr. CHETAN PARIKH: Ok fine. Are there any moats in this business? What would prevent somebody else in the diamond market from making a transition into this area?

Mr. UTPAL SHETH: Actually speaking, jewelry is a business of credibility. There is nothing preventing anybody else except the fact that the credibility of all Indian diamond players is extremely poor. Secondly, the cream in this business lies in ensuring that you can compress the delivery time or your working cycle times. Most diamond jewelers are unable to do that. They are not capital conscious and they are not cost conscious. They have been working for years in a very highly manned, labor intensive diamond polishing environment, which I think does not provide the right mind set. Shrenuj & Su-raj both have tried making this transition and failed. Goldiam has an in-house design team which is headed by a lady who has been adjudged the Designer of the Year award for gold jewelry studded with diamonds by De Beer\’s for 3 years in a row.

High margin of safety

Mr. CHETAN PARIKH: What could make this investment into a mistake? Can you visualize any sort of conditions making this investment at this price into a mistake at Rs.58?

Mr. UTPAL SHETH: Any significant indiscretion by the management or a catastrophe in the US markets will threaten this investment idea. But even then I think the margin of safety is so large that . . .

Mr. CHETAN PARIKH: Do you have any projected price target?

Mr. UTPAL SHETH: I only know that it is a multi-bagger, I don\’t know how many times. Even at a measly 6x 2001 conservative earnings estimate of Rs.33 per share, we are talking of a 3 bagger plus.

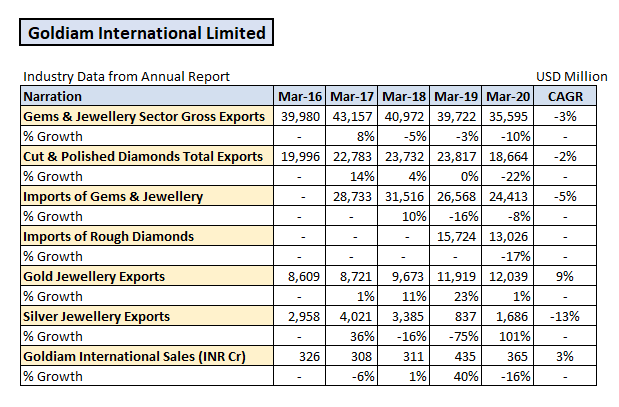

Company’s last five year growth seems to slower than the Gold Jewellery Exports. Promoter has been buying regularly. Company also acquired Eco Friendly Diamonds LLP recently in Nov-2020, which is Lab Grown Diamond business. Very high EBITDA margin profile. FY20: Sales: 27 Cr. EBITDA: 11 Cr.

Company’s last five year growth seems to slower than the Gold Jewellery Exports. Promoter has been buying regularly. Company also acquired Eco Friendly Diamonds LLP recently in Nov-2020, which is Lab Grown Diamond business. Very high EBITDA margin profile. FY20: Sales: 27 Cr. EBITDA: 11 Cr.