India suspends palm oil import license

3 Likes

can you pls elaborate how this can impact Godrej Agrovet? Also is gov regulation good or bad for the company? Thanks

Godrej Agrovet is the largest palm oil producer in India with 35% market share. It has 68400 Ha of oil palm plantation which is equivalent to ~20% of India’s oil palm plantation area. The company is in the midst of developing additional 4 mandals of area consisting 10000 Ha that was allotted last year in Chittoor (Andhra Pradesh).

So, cancellation of import licenses is beneficial for the company.

P.S. The above data is from the initiating coverage review by Prabhudas Lilladher.

4 Likes

Godrej Agrovet partners with Zomato and Swiggy for uninterrupted supplies

Under this partnership, Creamline Dairy, subsidiary of Godrej Agrovet, will deliver essential food items under their brand Godrej Jersey which includes – milk, ghee, curd, paneer and buttermilk.

While these products were already available on e-commerce sites such as Big Basket and Flipkart, consumers in Hyderabad, Chennai and Visakhapatnam can now place their orders for Jersey products through Zomato and Swiggy that are connected to the nearby retail points.

Delivery through these applications is operational in Chennai and Visakhapatnam.

Their services in Hyderabad will commence once the restriction on food delivery through Swiggy and Zomato is lifted in Telangana.

3 Likes

Moneycontrol article on Agrovet

Transcript of Conference call with Investors & Analysts held on May 12, 202068c4d8dc-7d25-43ee-8ccb-133c60ce0bb8.pdf (791.2 KB)

2 Likes

Now that the government has allowed contract farming, Godrej Agrovet wants a big play in oil palm cultivation. According to company’s Managing Director, Balram Singh Yadav, the company could “build a very good system for contract farming for oil palm cultivation.” Funds, he added, are not a problem. Yadav observed that there are about two million hectares of land in India on which oil palm can be grown; in contrast, only 300,000 hectares are being used now. He said that oil palm gave the biggest bang for the buck compared with other edible oils, yielding four tonnes per hectare, compared with 300-400 kg of others.

1 Like

Biggest questions is are they going to be cost competitive compared to indonesian , malaysian palm oil ? If yes why ?

We have been surviving on the basis of import duty etc, one cannot invest thinking all these protection going to stay forever.

Palm oil has been and continues to be a major driver of deforestation of some of the world’s most biodiverse forests, destroying the habitat of already endangered species like the Orangutan, pygmy elephant and Sumatran rhino. This forest loss coupled with conversion of carbon rich peat soils are throwing out millions of tonnes of greenhouse gases into the atmosphere and contributing to climate change.

For this reason there has been a continuous resistance towards expansion of oil palm plantations.

Palm oil can be produced more sustainably, however it will remain to be seen whether the cost competitiveness remains even then. With the import duties our country may just become future-ready sooner.

1 Like

Has anybody evaluated Astec Life sciences? Q4 investor call and Annual report presents an optimistic picture (snippets below). Promoter holding (i.e. through Godrej Agrovet) has increased from 58% to 62% in the last 1 year. Stock price action has been strong with the stock touching all time highs.

PS. Pls let me know if you want me to move this to a separate thread.

FY 20 Annual Report

The Company’s contract manufacturing business also performed well and we saw strong demand for our products. We commissioned two new products for multinationals. We also have several projects in the pipeline which will be rolled out over the next few years.

Construction of a new herbicide plant is expected to be completed by the end of the year and we propose to introduce two new products this year. We will also continue our programme of backward integration to reduce our dependence on China.

We have completed the design of our new state-of-the-art Research & Development (R&D) Centre, which will result in a quantum jump in our R&D capabilities. We hope to commission this facility by the end of the next year.

Agrochemical Industry and Implications for the Company

Opportunity for Indian agrochemical players remains high , both in the domestic and the international markets. Increasing usage of agrochemicals is needed in India, given the high focus on increasing the yield per hectare, limited arable land, rising labour costs and increase in growth of herbicides and fungicides.

Globally, disruption of Chinese agrochemical supply chain has shifted the focus on India, thereby increasing the opportunity for contract manufacturing business for Indian players. Also, as large number of molecules are going off-patent in the next 3 to 5 years, it further augments the opportunity for Indian players.

Your Company is one of the leading players in triazoles fungicide and is well-placed to capitalize on opportunities arising in the domestic and the international markets. While in India, large number of companies are dependent for their raw material supplies from China, your Company is continuously investing in backward integration projects to reduce its dependence on Chinese raw material. This is not only helping the Company in reducing its reliance on China, but is also aiding in margin expansion.

Godrej Agrovet Limited, Holding Company has also increased its stake in your Company during the year and holds 62.37% stake in the Company as on 31st March, 2020 as compared to 57.67% stake as on 31st March, 2019

Opportunities

50% of the Indian agrochemical industry’s value is derived from exports and therefore, exports are expected to grow at a faster pace in the coming years as compared to the domestic market. As global companies look for alternate manufacturing locations outside China, the opportunity available to Indian manufacturers including your Company will be huge. Organizations with deep technical capabilities of technical or intermediate chemistries are likely to gain from this shift / diversification of the manufacturing base.

Outlook: The global as well as the domestic demand for triazole fungicide is showing a strong demand. The Company is also working on enhancing the offering within the triazole fungicide products and developing a robust pipeline for Contract Manufacturing business. International companies are considering India as an alternate to China for contract manufacturing business. This poses a huge opportunity for domestic players like your Company, which have strong technical capabilities.

Going forward, your Company will continue to focus on both the markets and develop manufacturing capabilities which should cater to the key changes emerging in agrochemical industry. Your Company will keep on working towards adding new multinational customers for ensuring sustained business growth.

Q4 call snippets

In the fourth quarter we had both advantages of one, entirely across the globe, there was a disruption from Chinese supply side because the Chinese problem with COVID started during December, which aggravated like by middle of January, which coincided with the New Year. So, that was one of the advantages. Because we re-positioned ourselves, major purchases shifted from China to us. We captured a lot of Southeast Asian market, Russia, CIS market opened up very strongly. That has been one of the good and that will be a permanent good, plus the US, Europe markets remain. These changes will be to some extent permanent because most of the multinationals will be now actively looking for de-risking. This one change in terms of enterprises will be there. Second changes which will happen is or which we are also experiencing is shifted to the CMO businesses because if you see most of the multinationals are working in asset sale. So they do not produce much actives within themselves. They just procure it either from China or India, and majority almost 70-75% is working from China only. So, that is a shift. Almost this year, we have launched two new products. So, that is actually a shift from China because they used to procure from China and it has shifted to Astec. So these two changes will more or less remain permanent. You will see more of Japanese projects coming to Astec as well as to other companies. And enterprise businesses derisking will go on. So, coming year also we think this type of growth, we will be able to maintain.

Sir, a short question on Astec. What I wanted to know is that the confidence that we are getting in terms of the sales that we have received in the previous quarter continue in the times ahead, is that based on a commercial inertia trend or have we signed some long-term or rolling contracts with new customers? Arijit Mukherjee: A combination of both. One is a long term agreement also we have made that is covering both CMO businesses as well as the normal generic businesses. Plus, as our output has increased, the spot market has also improved.

9 Likes

I am holding Astec shares for last 3 years and pretty optimistic about their future, more so after last quarter’s result and concall. I see them developing into next PI Industries. PI was in similar position around 10 years back. One positive for Astec is that they are backed by large group like Godrej so market does not have to worry about corp governance issues. So if Astec can repeat Q4 performance in next 2 quarters, stock has potential to get good leg up. Re-rating can follow in next few years if earning performance continues.

Disc : Astec forms more than 10% of my portfolio

5 Likes

So you don’t think merger will not happen soon? Have you been trimming your position from more than 10% of PF or has it always been 10%?

1 Like

Merger was called off last year.

1 Like

If I recall correctly, as per Mr. Balram Yadav, it was postponed and will be done at the appropriate time… They had received lot of pushback from minority shareholders,even I had written to the investor communications about cancelling the merger.

Considering the fact that Godrej Agrovet is also a listed entity, the risk of merger always remains for Astec. In my opinion, this is the biggest risk which can cap the upside of the stock. But based on my last experience, I have decided to sell my holding if and when the merger gets declared. This is not against Godrej Agrovet as a company but I personally do not like diversified portfolio companies where there are too many moving pieces of the puzzle.

6 Likes

Highlights from management commentary

In the Palm Oil segment, volumes are not at risk as imports are likely to decrease if demand starts to increase; however, price decline stands as a key risk.

CWIP of INR1.5b as of FY20 pertains to: a) INR1.2b injected in the Animal Feed segment and b) INR220m put toward the Astec herbicide plant, which would commence operations in 3QFY21. Guided for consolidated capex of INR2–2.5b for FY21.

4QFY20 conference call highlights

Animal Feed

In India, broiler production averages at 75–80m per week, which has dropped to 35–40m per week due to the COVID-19 crisis. Similarly, India usually produces 2.2b eggs in a single week v/s 1.4b per week reported currently.

Cost of production of feeds for broiler has dropped to INR77/kg currently, from INR84–85/kg in March, on RM prices declining due to the rabi maize crop set to enter the market.

Maize prices in the pre-COVID-19 era stood at INR22–24/kg v/s 12–14/kg currently. Prices have fallen due to decline in poultry demand and rabi maize set to enter the market.

Out-of-home consumption accounts for 50% of demand for chicken. Even if 15–20% of this demand is revived, this would aid a price rise.

Consolidation is unlikely in the Animal Feed segment as barriers to entry are low.

Aqua (shrimp and fish) prices have been remunerative for farmers. Cattle feed sales have been impacted due to lower milk prices.

Crop Protection:

The company has been cutting credit to distributors to avoid bad debts, which have impacted sales. Collections have taken a hit as these usually happen toward the end of March.

The CP plant, which has been running at 60–70% utilization, is expected to run at 100% utilization from 17th May; lost production would be recovered by working on holidays.

In Dec’19, the company launched Hanabi, a Nissan product, which has received an excellent response.

The company is lagging behind on placement for the kharif season, which should ideally have happened by this time, as production processes are running slower than usual.

A drop in labor availability would aid in increasing the consumption of herbicides.

Astec’s growth during the quarter was led by two main factors. A) An increase in enterprise sales, on disruption in China’s supply chain, led to growth in order inflows from Southeast Asia, Russia, the US, and Europe. B) Moreover, Contract Manufacturing launched two new products, which customers earlier acquired from Chinese manufacturers.

The prices of certain Astec products are competitive with those of Chinese products. Three to four molecules under the registration would be launched in the Standalone Crop Protection segment over FY21–22.

Palm Oil

55–60% of sales are usually conducted in the July–Oct season.

The company has two mills, each with a processing capacity of 1,200MT per day. It is also refurbishing another mill with a 600MT per day processing capacity.

Currently, the price of CPO is INR58–59kMT; prices have dropped as demand from bakeries, restaurants, and other institutions has been impacted. Previous-year prices were a little lower, reaching as high as INR60–68kMT in Mar’20.

Palm kernel oil finds use in industrial oils, FMCG products, and beauty products, among others; prices have been impacted due to lower demand from end user industries

In Palm Oil, volumes are not at risk as imports would decrease if demand starts to increase; however, price decline stands as a key risk.

In FY20, the company processed FFB of 568k MT, sold CPO of 98.6kMT, and supplied palm kernel oil of 12kMT.

Dairy

The company is attempting to lower procurement from agents, which would not only control the price of milk but also quality.

Over the next couple of quarters, share of revenue from value-added products would be higher than liquid milk sales.

Milk production in India is 180m MT, 45–50mn MT of which is procured by organized players; of this, 33% goes to value-added products (VAP) and institutions.

Others:

The Aqua Feed and Crop Protection businesses face credit risk.

The company reported exceptional loss of INR99m in its subsidiary Godrej Tyson Foods as demand and prices of poultry and related products plummeted toward the end of fiscal. Accordingly, the company had to recognize inventory loss of INR30m and loss of INR69m with reference to the fair valuation of biological assets.

3 Likes

I need an overall idea about Indian feed market in terms of companies and market shares

If someone can share any link it will be of great help

On today’s Astec AGM, one shareholder did ask about whether Astec would merge with Godrej Agrovet in future. Nadir Godrej responded that there are no immediate plans of merger but if minority shareholder wants it, they can suggest and board can consider that

6 Likes

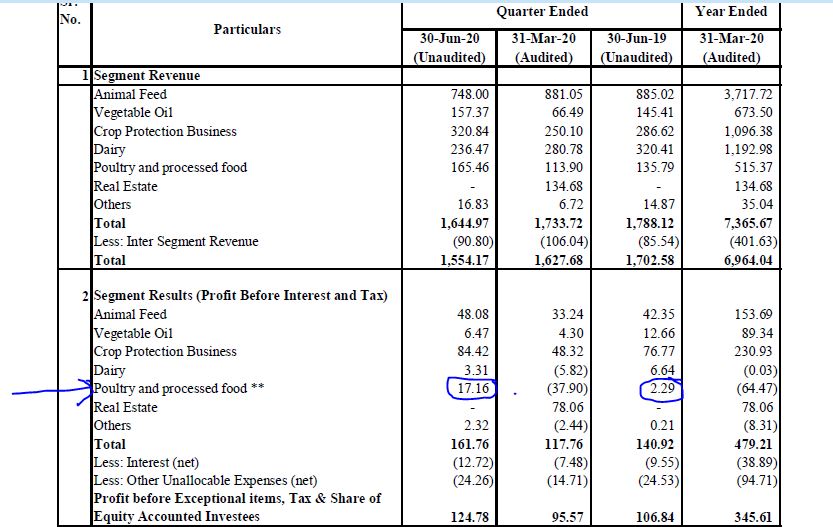

Hi,

The quarterly results are out and it is better comparing YOY.PBT stands at 124.78 compared to 106.84 crore earlier.An increase of 17%.And PAT stands at 100.59 crores compared to 77.58 crores.An increase of almost 30% yoy.EPS stands at 4.61 compared to 3.96.

And if we look at segment wise performance the poultry and processed food part’s bottomline contribution has increased sharply.

Kindly see the below screenshot.

vegetable oil part segment’s performance is not that good.

Full results can be viewed in the below link.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/2feae334-73dc-42ec-9afb-dfccea43a6df.pdf

Thanks,

Deb

2 Likes

From Godrej Agrovet report

Astec Lifesciences

Astec continued to grow strongly, recording ~45% YoY growth in revenues (volume growth was ~20%). Management stated that high

growth was witnessed across both CRAMS and enterprise sales.

Astec’s Ebitda margins surprised this quarter, expanding ~1,700bps YoY. While 1Q is traditionally the weakest quarter in terms of margins, Astec’s Ebitda margin this quarter is even higher than that reported for

4QFY20 (its strongest quarter last year).

Expansion of margins during the quarter was largely driven by better realisations from triazole fungicides and cost optimisation. Management believe that the company can deliver >20% annual Ebitda margins going forward.

Management expect the new R&D centre to be a game-changer for Astec. They stated that Astec currently is in an enviable position,wherein demand for its products is outstripping supply. While there is no limitation on infrastructure, the company currently does not have the R&D bandwidth to cater to the overall demand. Benefits provided by the new R&D centre include:

• Increase in bandwidth to handle multiple projects at a time.

• Help in development of new chemistries: management alluded to their desire to enter areas such as fluorine chemistry, flow

chemistry, high-pressure reactors and hydrogenation.

• Building pilot plants, etc., for scale-up of molecules.Management believe that offering such services to the customer is essential to scale up the CRAMS business.

The CRAMS business currently generates ~20% of the company’s revenues, but management is hopeful that rapid growth can take this

up to ~50%, over time.

Management pointed out that PI Industries

currently generates ~US$300-400m of revenue via CRAMS, while Astec is currently a much smaller vendor and is poised to benefit, as global

customers seek to de-risk their supplies from China as well as larger Indian companies.

Management said that the triazole chemistries are currently performing well and witnessing positive trends in the North American and European markets. Management also said that exports have grown faster than domestic sales.

Astec plans to launch two new products this year and another two next year. Pharma sales have fallen to ~5% of total revenues due to the

strong growth witnessed in agrochemicals. While there are multiple opportunities available, pharma growth has been limited due to low

bandwidth at the company.

Management guided to a peak asset turnover of ~1.5-1.7x in the long term, which is at par with industry. The company is investing ~Rs1bn

on its new herbicides unit.

5 Likes