A wonderful summary of the investment thesis has been provided by rupaniamit. I was unable to post on that thread probably since it was categorized as “collaborators corner”. If there is any way to merge with that thread, kindly let me know. Also, its my first time trying to initiate a thread so if there are any mistake, kindly guide.

I have gone through the summary and want to update based on what rupaniamit said were the key monitorables.

The following were mentioned as key risks to Godfrey Philips

Risks:

1 Declining cigarette volume trend in India

2 Current EBITDA margins not sustaining and reverses to older/lower levels

3 Any sudden increase in taxes on cigarette impacting demand

4 Any irrational capital allocation where good money is thrown after bad

5Hostile takeover/sell-off of GPIL due to ongoing family feud which may impact market’s perception of business’ true value.

6 Current retail foray continues to burn money at higher rate.

7 Any other unknown unknowns.

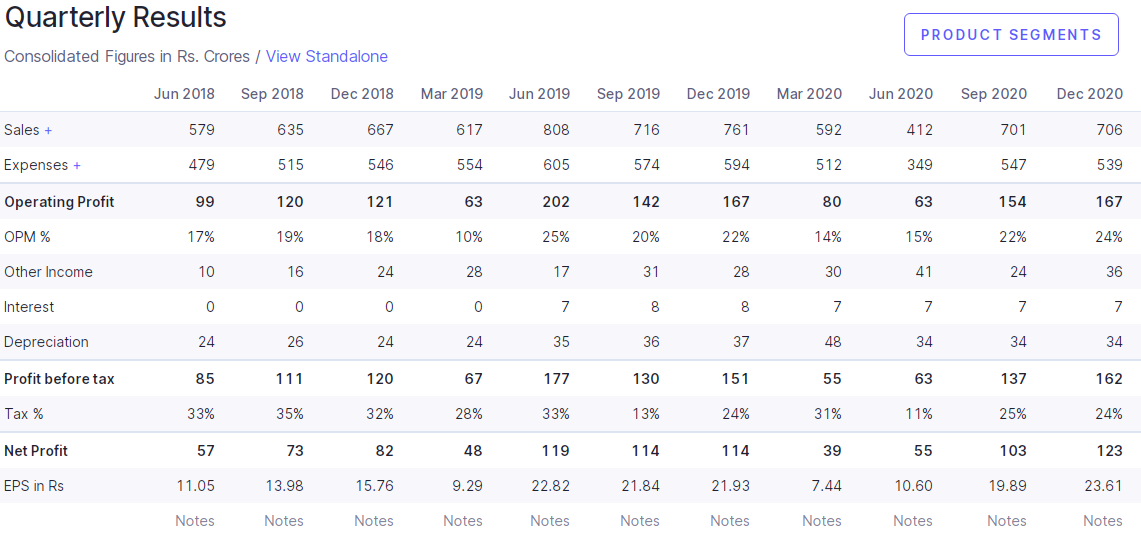

No.2 - The company has been able to maintain its margins in the latest quarter.

No.3 - Favourable action (no increase in taxes in budget and unlikely in GST meet)

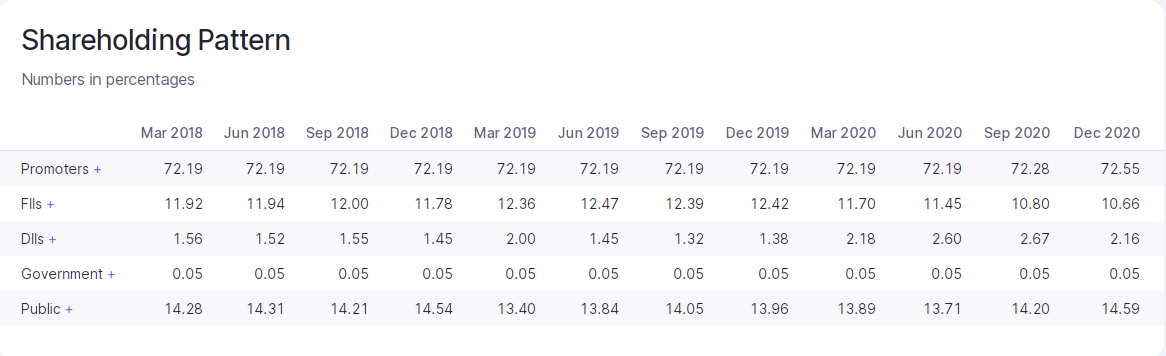

Additionally, promoters have increased stake in December quarter after a long time.

Plus the low FII shareholding means a selloff in the US market may not affect Godfrey Phillips too violently.

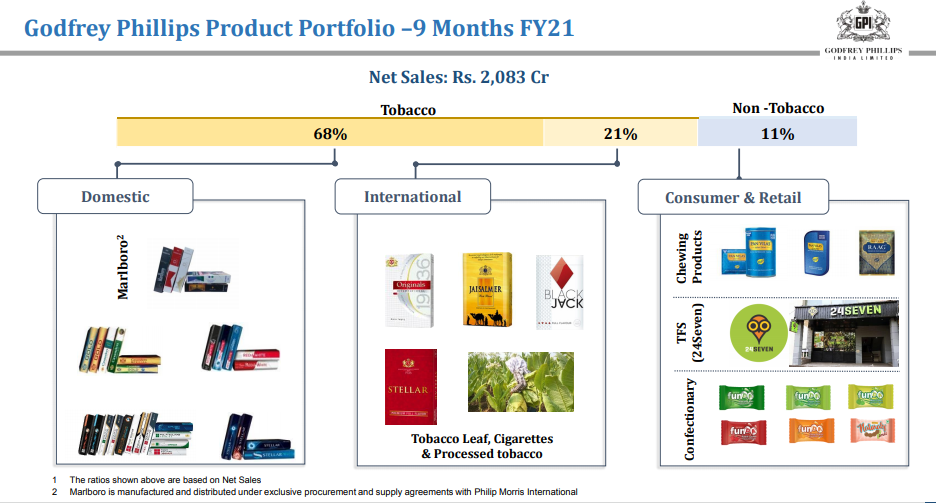

Based on latest investor presentation, GPIL derives 21% of its sales from international markets (tobacco leaf, cigarettes and processed tobacoo).

And exporting cigarettes is one of the growth priorities of the company.

Based on this, I feel that even if the domestic regulatory environment turns unfavourable, the company can make up some part in the export market.

Inspite of Covid, the company was able to maintain same operating profit in Dec, 2020 as Dec, 2019 (167 crores). So even if you take the consensus that “value investing is dead” to be true, the company could still make it as its earnings are growing. And if you like to bet against the consensus, I think it’s one of the best bets in the market currently.

Disclosure - Invested and looking for counter views to temper my enthusiasm.