Current domestic demand is high. IMHO, it’s expected to remain high for for next few years if not this decade.

2 Likes

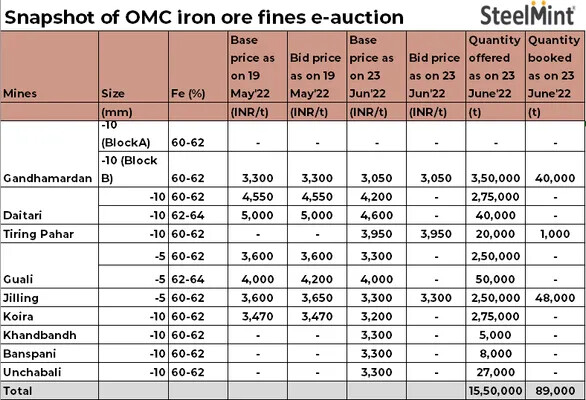

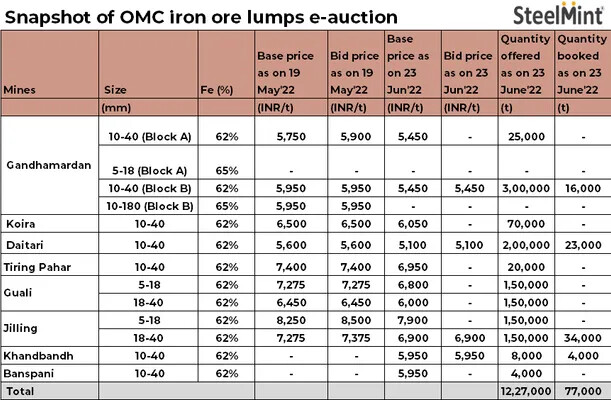

Only 10% fall in iron ore price in Odisha before and after iron ore export duty.

Though the quantity booked is low, but the OMC, state govt co is not lowering the price.

Now, you can’t really accuse private cos to profiteer- since this is a govt co ![]()

Is this the reason?

3 Likes

Hira ferro alloys holds 3.41% equity of GPIL.

However, GPIL has increased stake in HFAL to 91% now, and may soon increase to 100%.

That means, this 3.41% equity will be extinguished, since here GPIL will be holding its own shares.

It implies total number of shares will reduce by 3.4%, and EPS will increase by 3.4% permanently at same level of earnings!

7 Likes

@Kumar_manas - Thank you for the extensive coverage of this stock.

Here is some analysis.

- P&L Analysis

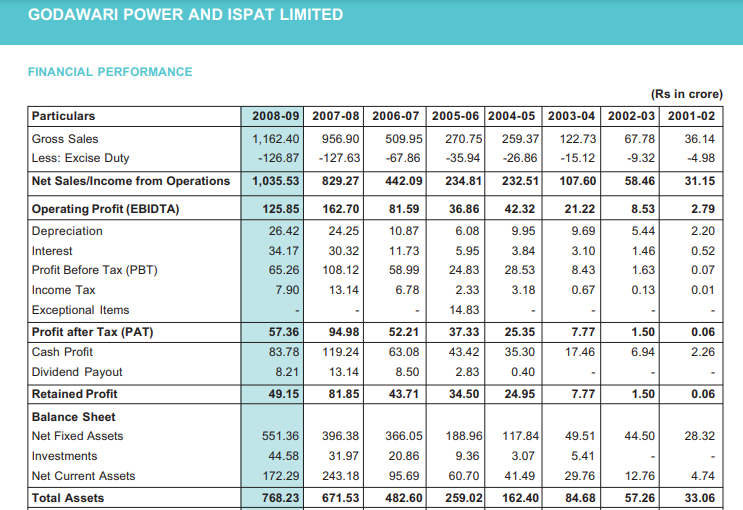

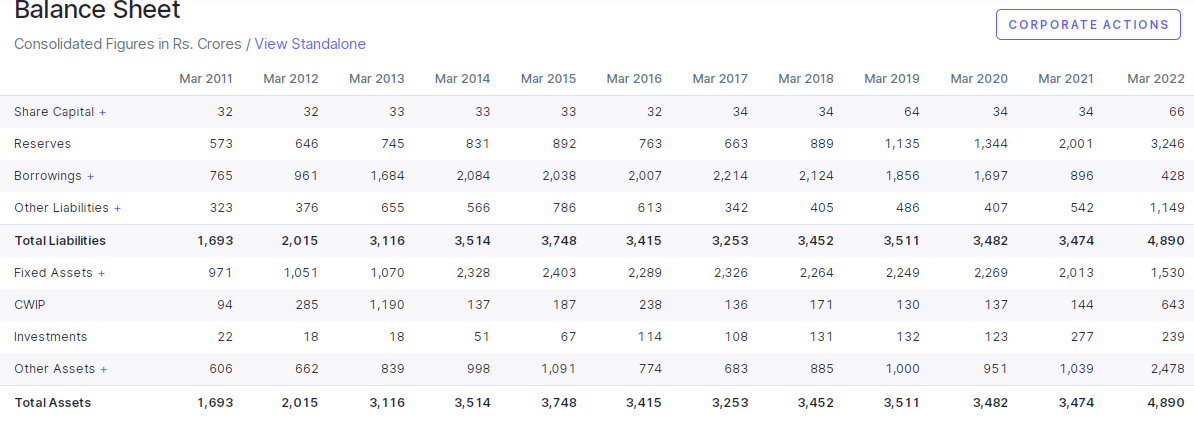

In last few years , GPIL never made loss at operating income level. Sales are always higher than expenses. In 2016 and 2017, Net Profit is negative due to interest cost incurred for the debt of ~2000 Cr. Now that the debt is almost reduced, it is very much likely that Net Profit will be positive.

-

The company is having debt of 428 Cr and Cash Equivalents of 575 Cr. The Capex is estimated to be 500 Cr and management guided that it will be taken care by way of internal accruals(No debt). Traditionally, cyclical industries struggle due to interest expense during downtime but it is not the case with GPIL this time.

-

Company is focusing only on core business and as mentioned by @VALUE2017, the management seems to be share-holder friendly and continues till today.

-

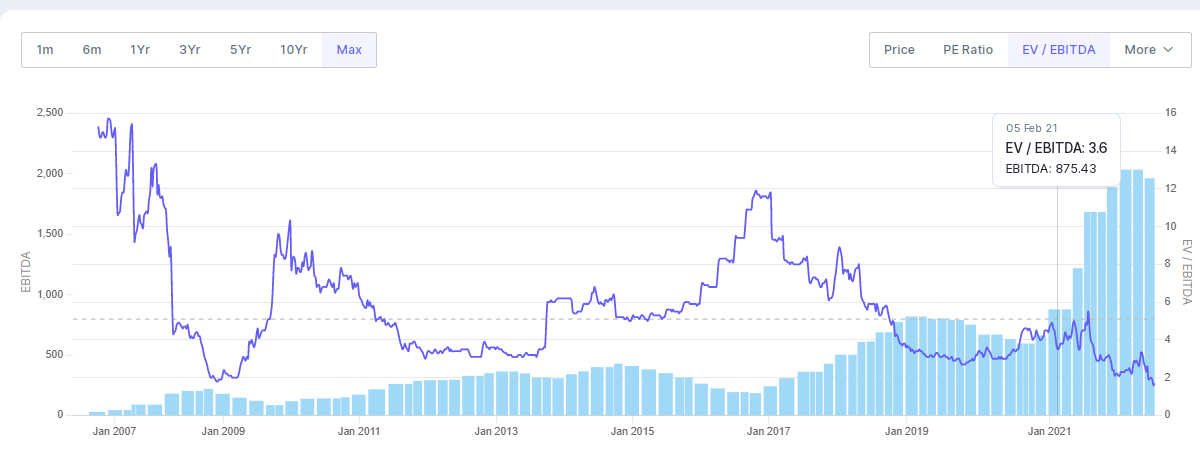

At EV/EBITDA < 1.6, it is at its cheapest valuation.

-

In last 5 years, GPIL increased its market share from 0.58% to 0.8%. Got this from ticket tape but not sure.

-

The tax rate is reduced to 25% by government which was not there earlier and positive for GPIL

Now, what is it that market is discounting for this stock?

- Is it that the target addressable market is saturated for GPIL or going to reduce?

- Are there any mandatory expenses for the company even if there are no sales? Something similar to graphite electrode companies like HEG/Graphite India

- Is there any impending law suit GPIL or one of its subsidiaries are involved with?

- As mentioned in this thread about merchant miners not able to afford the captive mines, will there be any change of policy from government to favour the economy/general public?

Request the esteemed members who are tracking GPIL with the answers. Thanks.

Disc - Invested in last few days at EV/EBITDA of ~1.6. PF.

4 Likes

As of date, cash should be 1000 crores.

Policy is very transparent. It is an open auction. Anyone can buy any mine, No discrimination or favor to anyone. (You want govt to give special favours to some companies?)

Many companies bid at 120-140% premium- it is their choice. No one has forced them to bid at such high prices.

4 Likes

Iron ore can follow this path.

I expect royalties on iron ore to be increased by Australia sooner or later.

Meanwhile, prices continue to surge!

2 Likes

GPIL acquired 37,79,220 equity share of Alok Ferro Alloys Limited @ Rs. 336/- per share. Total value of deals comes to at around Rs. 126 Cr.

The Promoters and promoter/ promoter group/ group companies are holding interest in AFAL.

The transaction is said to be done at Arms’ length price at fair value.

Total turnover of the company in 2019-20, 2020-21 and 2021-22 has been Rs. 76.59 Crores, Rs.78.60 Crores and 134.65 Crores respectively.

GPIL is having turnover of Rs. 5400 Cr. for 3600 Cr. valuation. GPIL also having advantage of long term mining license.

Keeping in view of valuation of GPIL the deals seems to be on costlier side.

Disc: Invested

GPIL.pdf (461.1 KB)

5 Likes

GPIL is trading cheap because of market reaction. Just 2 months back, GPIL was at double the valuations.

One should also look at valuations of other commodity cos like MOIL, HEG, Rain ind etc to see the comparison and not compare with depressed valuations of GPIL. (sarda energy which is very similar to GPIL is at 60-70% higher valuations compared to GPIL)

Also, note that Alok ferro is holding 1.36% shares of GPIL- so this buy price includes buying 1% of GPIL equity too.

Both Alok and Hira acquisitions will reduce GPIL equity base by 5%, and EPS will permanently increase by 5% at same level of earnings.

Anyways, coking coal is up 8% today, and thermal coal also making new highs- both these things favour high grade pellets a lot.

Also, these small acquisitions like alok ferro etc- keep adding to topline and bottom-line, in small ways.

Adding solar plants (which will reduce energy costs despite soaring coal prices), the addition to EBITDA on annual basis may be substantial.

The growth story continues.

11 Likes

@Kumar_manas , Sir I couldn’t find the FS of AFAL but the company’s ROE during FY21 was around 2% so, 1.2 X sales seems a bit expensive isn’t it? Are Ferro Alloys immune to cyclicality? Will GPIL merge HFAL and AFAL if they acquire both completely and if they do, will GPIL benefit from economies of scale?

1 Like

FY 21 was covid year, with 6 months in lockdown

Have you checked FY 22 ROE?

Also, AFAL holds 1.3% of GPIL shares. Actually, that alone is worth the acquisition cost if you know GPIL’s real value!

you can participate on the concall or write to the company about the same.

4 Likes

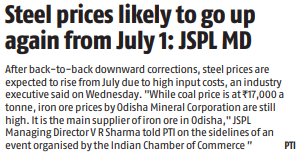

Thanks, yes had mentioned this earlier that Odisha mining corp hasn’t reduced iron ore prices (only small reduction). (everyone needs profits, even govt mining companies)

Semi-steel prices- like billets, wire rod- are already higher than average Q4 prices. (which was the highest average quarterly price for semi-steel prices).

If you follow steelmint daily updates on billets, wire-rod, sponge iron- you will realize there is shortage and very good demand on the ground!

I guess markets need another year to realize that GPIL profits aren’t going to fall off the cliff like other steel companies- it doesn’t have high depreciation and high interest costs- very unlike regular steel companies.

4 Likes

Couldn’t find the FY22 ROE.

Just compared GPIL with Maithan alloys- different sectors.

No export duty on maithan alloys.

GPIL increasing capacity 4x in 6 yrs, but Maithan is not, not even 2x.

Yet, the past 8 months returns and stock price movement is just exactly the same.

Infact, most stocks have moved similarly.

This implies that market has given zero weightage to huge upcoming increase in mining capacity of GPIL.

7 Likes

Semi-steel prices were supposed to crash because of export duties.

But, that ain’t happening even 1 month after the duty imposition.

Why is that so?

It is big green on all time frames-

8 Likes

Finally the 5000 cr investment for 2.2MTPA additional capacity has been filed for environmental clearance. Land identified and transferred. just environmental clearance awaited now. Hopefully it should come soon and then work will start… my wild guess is that the work will be completed in 2-3 years in phases. but on the news GPIL can get rerated.

5 Likes

Thank you for the link. Pl refer Pg 144 If the environmental clearances is taken as the zero date, then Phase-1 completion is expected to be in 3-4 years. Not sure how long environment clearance takes, if it happens let’s say on Oct 1 2022, we can assume at least partial commissioning of Phase-1 to happen 3-4 years from then.

A prev Godawari MoEF application from 2009 was dated June 2009 and conditionally approved in August 2009. But that might have been at an existing site.

I’m not sure how this ties with their Plan to enhance Iron Ore Mining Capacity to 5MnT over next 2-3 years and then to 9MnT over next 5-7 years. I was thinking probably the 5 MT mining will sync with Phase-1 and the 9 MT with Phase-2 But looks like (from Q4 FY22 earnings call transcript), the new plant is on hold though EC application has been submitted mid last year, and there won’t be any investment for new greenfield plant in FY23.

3 Likes

Appreciate your response. True - Anyone can buy mine but what if government come up with a policy to put a cap on mining quantity per year. My intention here is to find the anti-thesis points.

@Rakesh_Arora @ayushmit and other long-term holders/trackers of this stock - Can you please provide your view on anti-thesis pointers here? Thanks.

1 Like

Yes, this was true in Indira Gandhi times when there was waiting time of 5 years for Bajaj scooter, because govt put a cap on how many scooters Bajaj can produce every year.

I hope India doesn’t see such times again!

There were production quotas on how much you can produce in your factory.

Indira Gandhi also nationalized many banks overnight. Many PSU banks today were private banks at that time.

Hope HDFC bank doesn’t become a PSU bank this time!

6 Likes