This will be a big negative for strong players in the steel industry.

Export duties will kill the small players, and will help in reducing long term supply in steel industry in India and will lead to steel shortage.

And, thus export duties are very beneficial for the strong players in steel industry.

Also, I don’t think govt will remove export duties just like that. This is just a rumor.

Current govt doesn’t allow any information on any decision to leak in the market before declaring it.

P.S- This is long term view. In short term picture, export duties would look harmful, obviously.

look like i have an exact opposit reading of situation…we are coming out of long slump in steel…bhushan going bust…consolidation in industry as Tata bought up bhushan… NINL bought by tata… JSW buying welspun etc

finally they were making money…and gov slapped duty on thier exports are grabbed food from their mouth… removing duties is for sure a positivee for large steel players…

Do you mean the small players who either have no long-term iron-ore linkage or captive mines, like KIOCL ?

Almost every player who were leveraged (and also have captive mines) have cleaned up their balance sheet in the last 2 years, with a large help from exports. So yeah export duties will benefit them in the long term, but in the short term might less profits for them.

Wouldn’t any additional levy on mines that were recently auctioned make the ore even more expensive ?

A levy is in a way a backdoor for the government to tax players who got old iron ore mines on long lease (like Godawari) who are paying less levy/royalty now. In effect it might increase their cost of ore, and hence decrease the margin long term too.

Literally, there are only 3-4 companies who have captive mines at old rates.

I don’t think govt even cares about them.

The export duty was due to high steel prices in domestic mkt. Not because of GPIL making good money.

Actual number of steel cos in India- 100-200 steel cos- most are unlisted- many are small steel mills.

Many have bank loans too.

Many of these small steel mills having bank loans- will shut down, stop doing capex.

KIOCL has already shut the pellet plant.

Many more will shut down.

GPIL will continue to make big profits- because high grade pellets have big premium and bought by tata steel etc.

Also, note that only 500 cr out of 1400 cr sales is from pellets. Not that big contributor.

Export duty is positive for GPIL- because small leveraged steel mills will shutdown and/OR stop doing NEW CAPEX for future- so Long term, steel supply in Indian market will REDUCE.

While, GPIL will increase its capacity many fold in next 5 yrs- because it is a very cash rich company.

Anyway, if some-one sees today’s semi-steel prices (65-70% of GPIL revenue), he will tell you that govt of India has imposed 10% import duty (not export)

Motilal Oswal latest report on Metals Sector - Light At The End of The Tunnel…China is planning a stimulus of $220 billion (RMB 1.5 trillion) to jump start its slowing economy by preponing bond sales due in January 2023. This should help improve the sentiment for commodities. Motilal_Oswa.pdf (1.0 MB)

These reports are meant for large steel cos- cos like SAIL, Tata steel, JSPL- are very asset heavy companies.

They have high interest cost and depreciation (regular maintenance).

A 20% dip in EBITDA will lead to 40-50% fall in net profits for these large companies because of negative operating leverage (due to interest and depreciation).

On the other hand, a 20% dip in EBITDA for GPIL will lead to only 15-16% dip in net profits due to positive other income from cash balance, and minimal depreciation cost.

These large brokerage cos have never covered GPIL in their research reports and I don’t think they understand GPIL business in depth too.

Also, these large cos will take 10 years to double capacity.

GPIL plans to increase mining capacity by 4x in 6 years and will remain debt free.

Ideally, GPIL should trade at 2-3x valuations vs normal mid-sized steel cos because of debt free status and huge upcoming growth.

Despite govts best efforts, semi-steel prices are rising.

I am sure that govt can’t control prices in a free market.

Otherwise, USA inflation would not be 9.1% today, with the most powerful govt and currency in the world.

“Iron ore concentrate prices have increased despite NMDC’s price reduction mainly due to the recent hike in pellet prices”, a western India-based buyer told SteelMint.

They are exporting HRC by mixing it with Boron- and escaping the export duties.

Also, JSPL net profit for Q1 FY 23 is double the expectations. Results declared today and s̶u̶r̶p̶r̶i̶s̶e̶d̶ shocked all the bearish analysts on steel.

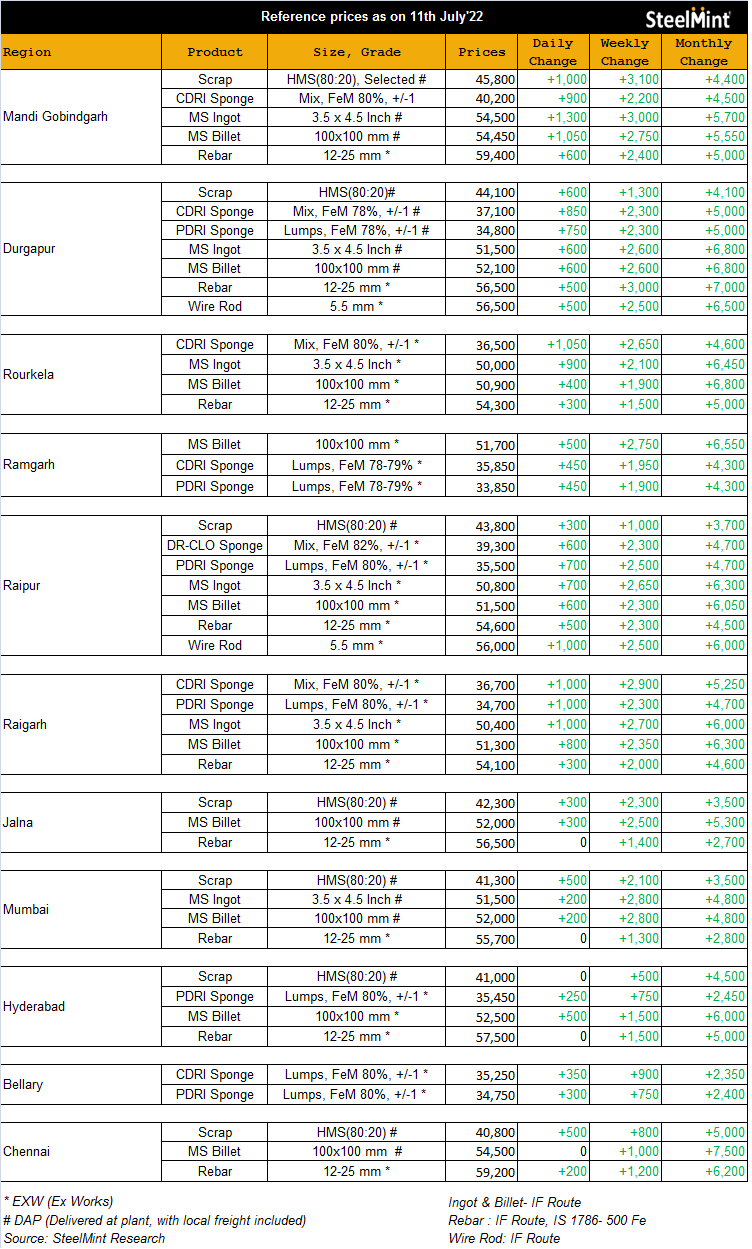

Q3 FY 22 avg billet sale price was Rs. 45,611

Q4 FY 22 avg billet sale price was Rs. 47,252

Q4 FY 21 avg billet sale price was Rs. 38,386

(Source: latest quarter investor presentation)

After export duty, and huge slump in billet prices.

Today’s Billet price is Rs. 48,700

This is higher than all previous quarters avg billet sale price.

(This also applies on wire rod, sponge iron etc, except pellets- which is 30-35% of total revenues)

Markets are indeed funny!

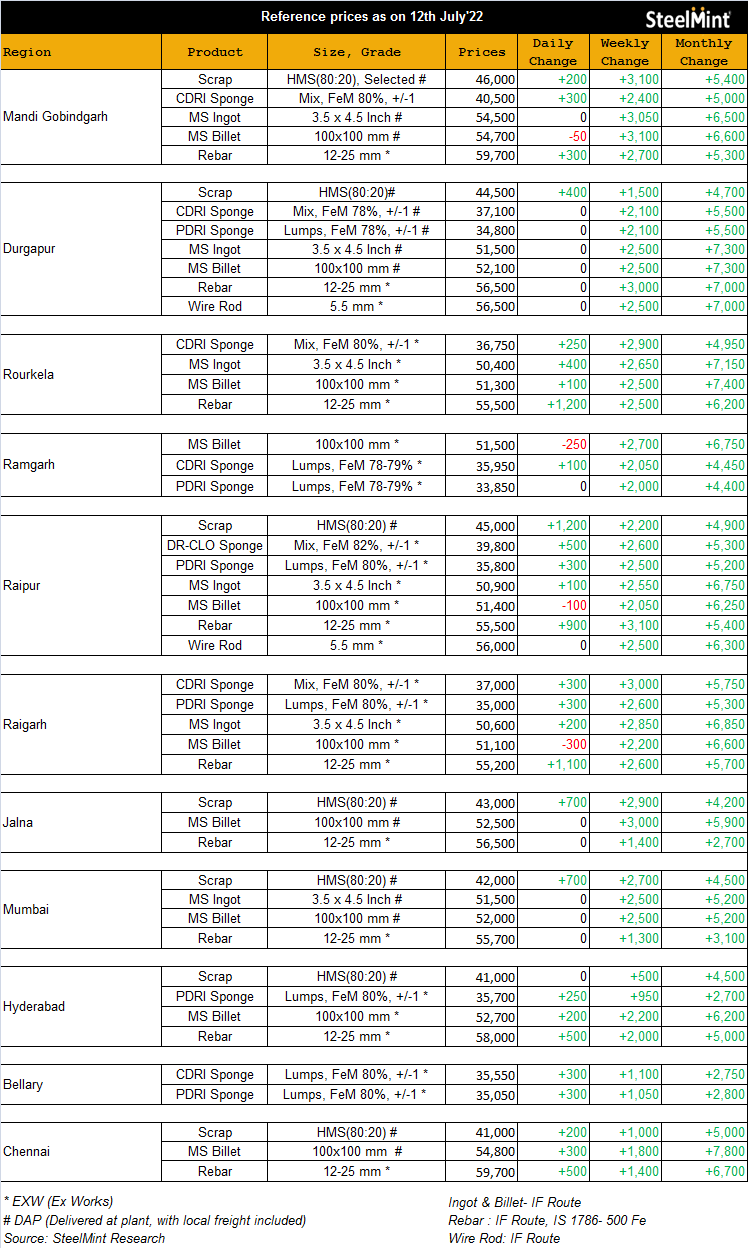

Billets avg price for Q1 FY23 looks ~50,000, while NMDC latest iron ore lumps price is Rs.3900 ! Royalty and all local taxes/levies + transport for iron ore might add another Rs.2000/ton !

Is the industry (atleast post-levy) favoring the downstream products vs a relatively raw-material skewed company like Godawari ? I’m not sure if Godawari has enough Billet/TMT capacity to go for value-add/downstream products, with the billet expansion only ready in Q4.

The existing 0.4MT billet capacity was utilized at 80% in FY22.

except pellets, all other prices are higher or same as last quarters avg prices.

Even pellets are at 8800 per tonne, so high grade pellets are 10,000+/tonne.

This is looking like normal EBITDA of 400-500 cr per quarter even as of today’s prices.

Following APL Apollo too, HRC prices have contracted to 60,000/ton from highs of 75,000+ and are expected to stay in the 60-65 range. The whole profit in the industry value-chain seldom reduces (unless there’s a cyclic down-turn), so whose profit is getting disturbed here ?

companies like KIOCL have shut-down their pellet plants, the employees are not getting salary.

KIOCL was a pretty big pellet plant of 3 million pellet capacity.

Similar story with many other small mills.

They are the losers.

So the govt expected the levy to retain the industry capacity, but discourage raw material exports - hence increased domestic supply and lower prices.

What it ended up doing was reducing industry capacity (of atleast upstream materials) and if demand stays the same, supply is reduced so prices stay the same/increase.

This is what happens in free markets.

Due to export duty, the marginal players will make losses and shut down.

No new capex will happen (atleast by the weaker players).

Result- both medium term and long term reduction in supply.

Demand will keep on increasing gradually due to increasing GDP and population.

And, as a result there will be shortage of steel and increase in prices.

This doesn’t happen in agriculture because govt buys agri produce at MSP from farmers and gives them lots of subsidies, so farmers keep on producing more and more even if no exports are allowed.

The key reason steel is called cyclical (vs cement/oil refinery) is because of steel dumping by China in 2015-16, which was once in 20-30 yrs event due to huge excess capacity in China. This should not be happening again.