@Gautam_Chopra how to get these research reports? do you have account with centrum broking?

Thanks

telegram channel. And some “internet ki shaqtiyan”

Success depends on the company’s ability to develop marketable, effective drugs and manage associated risks effectively.

1 Like

3 Likes

Glenmark has cultivated inlicensing ( also outlicensing) into a strength where they target therapy and geography where they are weak and inlicense products to close the gaps…they did it in Europe with several respiratory assets followed by deals with Pfizer, beigene,cosmo etc

For me the standout point in the conall was isb 2001, being described as transformational, once in a lifetime opportunity etc…

ISB 2001 outlicen will reduce R&D spend by 60 mn USD pa apart from future payoff

3 Likes

Appreciate your updates on Glenmark.

But Glenmark hasn’t had much success in out licensing till date. I don’t think management calling their own asset as transformational or once in a lifetime in itself has as much significance. Although Ichnos has been discussed in every concall since a number of years, there hasn’t yet been anything concrete. Even if we agree that these things take time, if the assets were truly valuable, there could atleast have been some progress on raising money at Ichnos.

Views invited as to if/when Ichnos will actually amount to something.

Thanks.

1 Like

Evolution - Glenmark Pharmaceuticals. The above links has details of 7 outlicensing deals done till date apart from 2 by IGI in last 3 years

2 Likes

Glenmark Pharma -

Q2 FY 25 concall and results updates -

Revenues - 3434 vs 3207 cr, up 7 pc

EBITDA - 602 vs 462 cr, up 30 pc ( margins @ 18 vs 14 pc, significant margin improvement )

PAT - 354 vs (-) 62 cr ( not comparable because LY, the company had to bear a one time exceptional loss of 205 cr )

R&D expenses - 227 cr @ 6.6 pc of revenues

Geography wise sales performance -

India - 1281 cr, up 14 pc ( @ 37 pc of sales ). Significantly outgrew the IPM which grew @ 7.6 pc. Cardiac, Respiratory and Derma therapies grew strongly. Company’s OTC business also grew strongly @ 15 pc. Company is ranked no 2 in Derma and Respiratory therapies and no 5 in cardiac therapy in India

Company already has some unique / differentiated products in IPM. These are - LIRAFIT ( Liraglutide - GLP-1 drug ), JABRYUS ( to treat atopic dermatitis, in-licensed from Pfizer ), TISLEIZUMAB and ZANUBRUTINIB ( in-licensed from BeiGene )

North America - 740 cr, down 1 pc ( @ 22 pc of sales ). Company has commercialised 8 injectable products in US. Launched 04 products in US in Q2. Slated to launch another 3-4 products in Q3. Have a strong filing pipeline - 02 Nasal sprays and gFlovent awaiting approval

Europe - 687 cr, 15 pc ( @ 20 pc of sales ). Branded respiratory portfolio led by Riyaltris continues to lead the growth in EU. Awaiting approval for 4 more respiratory products in EU ( were filed in Q4 LY ). Expected to launch WINLEVI ( derma drug for severe acne ) in selected EU mkts in next FY. Has in-licensed WINLEVI for 15 European mkts + South Africa

RoW - 704 cr, down 4 pc ( @ 20 pc of sales ). Reported 19 pc growth in Russia. Launched Riyaltris in Mexico, Kenya and some Asia-Pacific mkts

Till date, company has commercialised RIYALTRIS in 41 markets. They have filed for approval for RIYALTRIS in 90 markets. Should be launching it in 10-11 mkts in next 2-3 Qtrs

Company has partnered with Hikma ( has out-licensed RIYALTRIS to them ) for US market. Seeing good demand traction for the same

Expect to launch RIYALTRIS in China in FY 26. Has out-licensed it to Grand Pharma in China

Company has in-licensed ENVAFOLIMAB ( Onco Drug ) from Jiangsu Biopharma ( China ) for commercialisation in over 20 markets across the globe

Guiding for a full yr EBITDA margin of 19 pc ( that means they should do 20 pc kind of margins in H2 vs 18 pc in H1 )

Company believes, RIYALTRIS has the potential to do a $ 200 million sales / yr in next 3-4 yrs time. This year, it should cross the $ 100 million sales mark

The pipeline of respiratory products lined up for approvals / launches in US + EU should support growth in next 6-12 months

Company is now ranked 13 in IPM with 9 brands in top 300 brands in India

Company is the first one to launch Liraglutide in India under the brand name LIRAFIT. Had launched JABRYUS in India in Jan 24. Company is currently engaged in a lot of marketing, educational, promotional activities across dermatologists across India. TISLEIZUMAB and ZUNUBRUTINIB are expected to be launched in next 9-12 months

Company expects a significant growth pickup in RoW mkts in H2 after a flattish H1. Expects to end the year with high single digit growth in RoW mkts

Company is now ranked no 2 in the Kenyan Pharma mkt

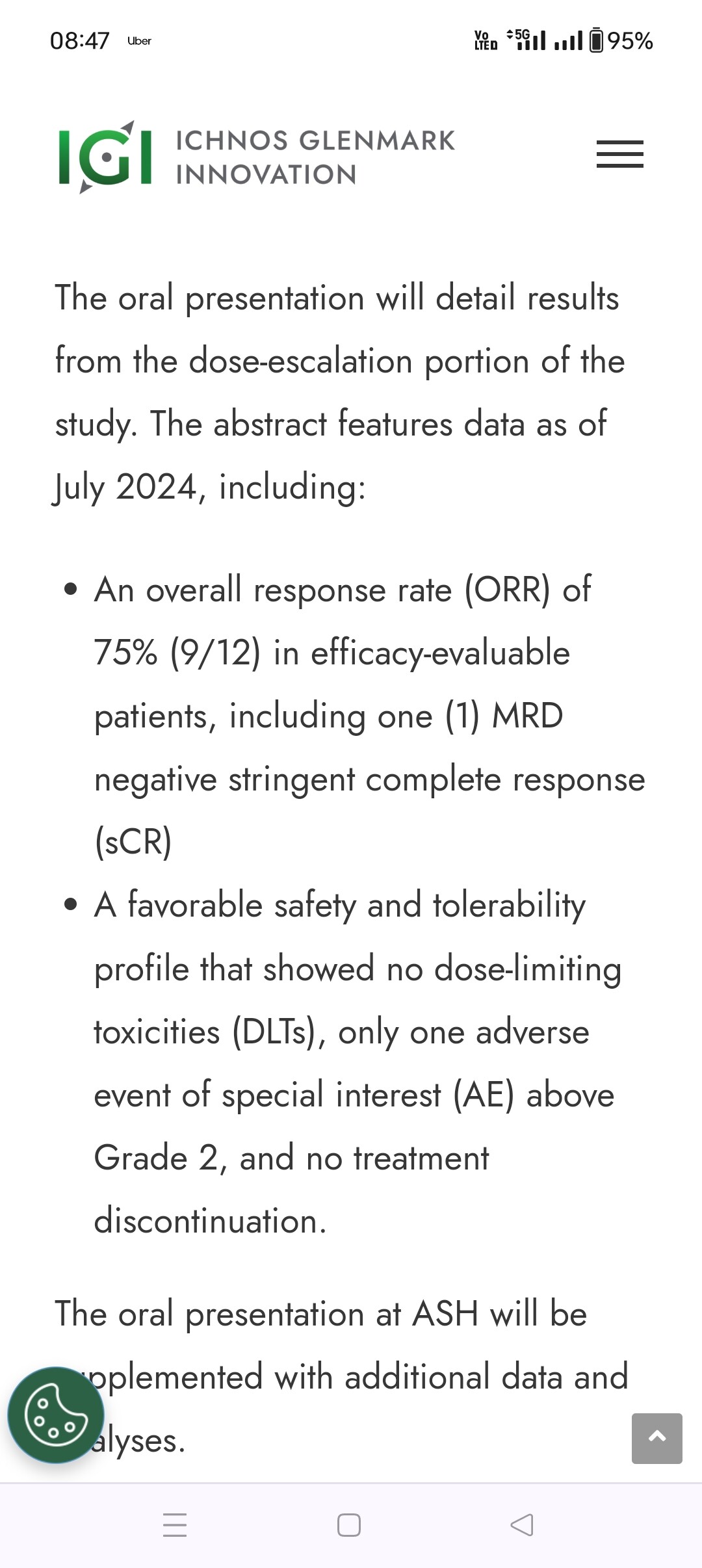

Company’s developmental drug - ISB 2001 - to treat Multiple Myeloma ( a type of blood cancer ) is undergoing Phase - 1 trials in US. The initial data is very encouraging. Hence the company is currently curtailing its expenditure behind other novel assets and focussing primarily on ISB 2001. Likely to keep spending aprox 450-500 cr / yr on the R&D effort at Ichionis ( company’s Innovation led subsidiary )

Company is looking to find a partner for further funding @ Ichionis after raising money by out-licensing ISB 2001. This should take some time and also depends on the safety and efficacy data of ISB 2001. At present, company seems confident of being able to do so in FY 26/27

Company’s Plant in US at Munroe is Serving a USFDA warning letter. Once that is lifted ( should happen in FY 26 ) and company starts launching products from there, it should result in significant operational leverage for the company. Currently, company ends up spending 150-200 cr / yr on the Munroe plant with no revenues

Should be able to commercialise WINLEVI in next 9-12 months. Should be able to start launching ENVAFOLIMAB in next 3-6 months. Should achieve descent scale in both these assets in about 2-3 yr’s time

Disc: holding, biased, not SEBI registered, not a buy/sell recommendation

4 Likes

2 Likes

Ichnos Glenmark Innovation (IGI) Presents First Clinical Data from Phase 1 Study of Trispecific TREAT™ Antibody, ISB 2001, Showing High Overall Response Rate (ORR) with Durable Responses and Favorable Safety Profile in Patients with Heavily Pretreated Multiple Myeloma

1 Like

Sir,

What is your view on the counter as per the latest updates and concall.

Regards

I sold Glenmark Pharma about 2-3 months back. Not updated wrt Q3 and Q4 FY 25’s developments

Hello @ranvir

Would it be possible to know the reason for your selling.

Thanks

General anxiety and uncertainty wrt Tarrifs, possible fall in USD were the only reasons. We ll only know if these were just fears or there was substance in these assumptions only by next yr ( I guess ![]() )

)

2 Likes

In your view, how significant is the favourable data that came for ISB 2001 recently.

Thanks

1 Like

Deal with abbvie done for 700 mn usd upfront and 1.25 bn usd in development… Balance revenue sharing details awaited

2 Likes

Tiered double digit royalty of net sales

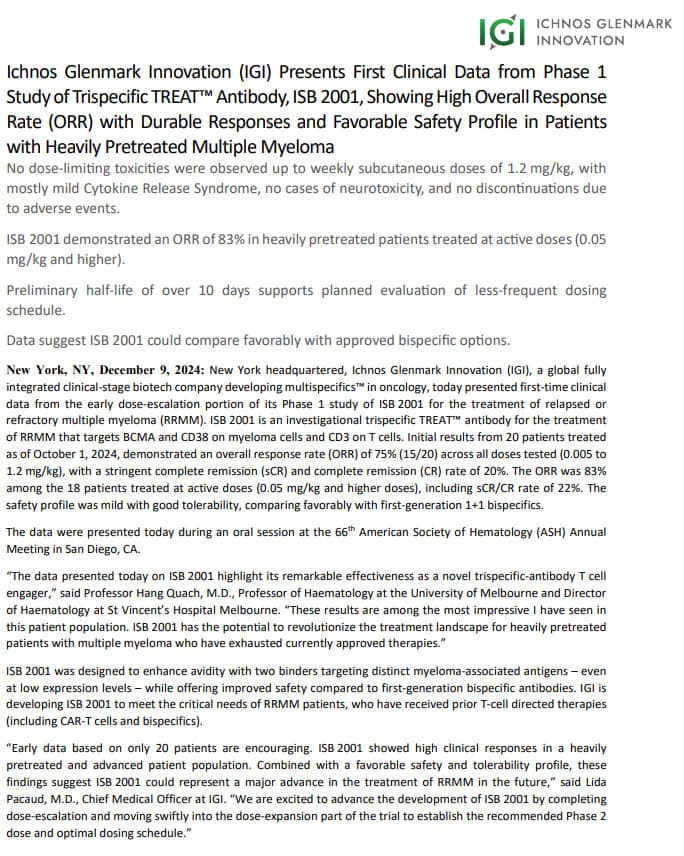

| ISB 2001 | Linvoseltamab | Teclistamab | Elranatamab | Ciltacabtagene Autoleucel | Anitocabtagene Autoleucel | Belantamab Mafodotin | Talquetamab | |

|---|---|---|---|---|---|---|---|---|

| Efficacy (ORR) | 79 | 71 | 63 | 61 | 98 | 70 | 60 | 74 |

| Complete Response (CR/sCR) | 30 | 50 | 30 | 30 | 83 | 30 | 30 | 30 |

| Safety (Low Toxicity) | 90 | 70 | 60 | 65 | 40 | 40 | 50 | 55 |

| Ease of Administration | 80 | 70 | 70 | 70 | 30 | 30 | 60 | 70 |

| Development Stage | 20 | 80 | 100 | 100 | 100 | 60 | 90 | 100 |

The chart focuses on key parameters: developer, mechanism, clinical efficacy (ORR and CR/sCR), safety profile, administration, and development status, highlighting ISB 2001’s unique features and competitive positioning.

- Efficacy (ORR): Overall response rate (partial response or better) in R/R MM patients with ≥3–4 prior lines. Scores are based on reported ORR percentages (e.g., ISB 2001: 79, ciltacabtagene: 98). Anitocabtagene and belantamab lack precise ORR, so estimates (70 and 60) are based on partial data and trends.

- Complete Response (CR/sCR): Complete or stringent complete response rate, reflecting deep responses. ISB 2001, teclistamab, elranatamab, anitocabtagene, belantamab, and talquetamab have ~30% CR/sCR or less specific data, while linvoseltamab (50%) and ciltacabtagene (83%) score higher.

- Safety (Low Toxicity): Based on reported adverse events, particularly cytokine release syndrome (CRS) and immune effector cell-associated neurotoxicity syndrome (ICANS). ISB 2001 scores high (90) due to no ICANS and 71.4% low-grade CRS. CAR T-cell therapies score lower (40) due to high CRS/ICANS. Belantamab’s ocular toxicity lowers its score (50).

- Ease of Administration: Subcutaneous (SC) or intravenous (IV) dosing (e.g., ISB 2001’s weekly SC, 80) scores higher than complex CAR T-cell therapies (30) requiring hospitalization. Belantamab’s IV dosing (60) is less convenient than SC bispecifics (70–80).

- Development Stage: Approved therapies (teclistamab, elranatamab, ciltacabtagene, talquetamab) score 100, near-approval (linvoseltamab, belantamab) 80–90, Phase II/III (anitocabtagene) 60, and Phase 1 (ISB 2001) 20.

Notes on Competitors

- ISB 2001 (IGI/AbbVie): Phase 1, trispecific (BCMA×CD38×CD3), 79% ORR, 30% CR/sCR, no ICANS, low-grade CRS, weekly SC dosing. Excels in BCMA/CD38-refractory patients (86% ORR).

- Linvoseltamab (Regeneron): Phase I/II, BCMA×CD3 bispecific, 71% ORR, 50% ≥CR, nearing FDA approval (2024), SC/IV dosing.

- Teclistamab (Janssen): Approved 2022, BCMA×CD3 bispecific, 63% ORR, moderate CRS/ICANS, SC dosing.

- Elranatamab (Pfizer): Approved 2023, BCMA×CD3 bispecific, 61% ORR, moderate CRS/ICANS, SC dosing.

- Ciltacabtagene Autoleucel (Janssen/Legend): Approved 2022, BCMA CAR-T, 98% ORR, 83% CR, high CRS/ICANS, complex infusion.

- Anitocabtagene Autoleucel (Arcellx): Phase II/III, BCMA CAR-T, durable responses, high toxicity, complex infusion.

- Belantamab Mafodotin (GSK): ADC, BCMA-targeted, ~60% ORR in combination, ocular toxicity, IV dosing, seeking re-approval.

- Talquetamab (Janssen): Approved 2023, GPRC5D×CD3 bispecific, 74% ORR, CRS and GPRC5D-specific AEs, SC dosing.

Additional Context

- Data Sources: The chart uses data from the provided links (Targeted Oncology, Cancer Network, IGI press release, ASH publication) and web/X sources up to July 13, 2025, including trial updates (e.g., NCT05862012 for ISB 2001, CARTITUDE-1 for ciltacabtagene).

- Estimates: Anitocabtagene and belantamab’s ORR/CR values are estimated due to limited 2025 data, based on trial trends (e.g., iMMagine-1, DREAMM-8).

- ISB 2001’s Edge: Its trispecific design and efficacy in BCMA/CD38-refractory patients (86% ORR) make it uniquely positioned for resistant R/R MM, though its early-stage development (Phase 1) lags behind approved competitors.

- Limitations: Direct comparisons are limited by trial population differences (e.g., prior lines, refractoriness) and incomplete 2025 data for some molecules (e.g., anitocabtagene).

2 Likes

Intresting presentation by Glenmark on their investor day. Some pointers

In licensing - they have been using inlicensing aggressively since last 5 years. Earlier some respiratory assets in Europe and now oncology in emerging markets. This allows them access to novel products increasing their value in eyes of distributors, hospitals etc and better use their distribution network . With their experience in inlicensing now they are becoming partner of choice for innovators for launching products in emerging markets

Igi- sufficiently funded now for developing their pipeline and IPO will be at a time when more assets are validated to get proper value of ichnos.

Usa- large dependency on munroe likely to be resolved in fy 26. several injectable/ respiratory launches likely in inext 2 years

Isb 830 and 880 progressing and addressing a large market, both in phase 1 so will take time

4 Likes