Glenmark Pharma -

H1 and Q2 FY 24 highlights -

Adjusted financials ( adjusted for Glenmark Life’s slump sale ) -

Consolidated Sales @ 3207 cr, up 6.3 pc ( growth drivers - Europe, RoW business which were up 58, 19 pc YoY )

EBITDA - 505 cr ( adjusted for a forex life of 43 cr ), Margins @ 16 pc

R&D expenses @ 305 cr ( almost 10 pc of sales - a very promising indicator, out of this - aprox 195 cr spent towards NCE discovery program at Ichnos ( GPL’s subsidiary )

Geography wise sales breakup -

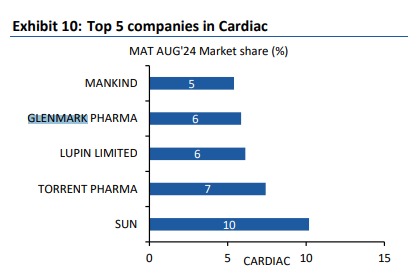

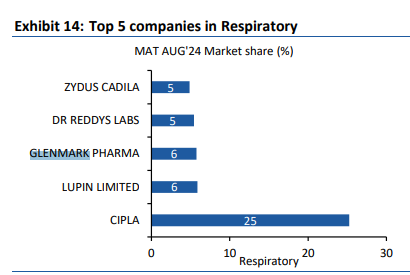

India - 1121 vs 1091 cr, up 3 pc ( however, the consumer care business was up 15 pc. Slowdown in acute therapies and divestment of some brands to Eris Life affected overall growth. Scalp and Candid continue to do really well ). Glenmark Pharma has a strong Respiratory and Derma portfolios in India

( ranked no-2 in both ). Company ranks no-5 in Cardiac market. IPM overall rank @ 14. Company has 9 brands in top 300 brands.

North America - 740 vs 753 cr, down 2 pc ( sales expected to pick up in Q3 as some important launches like - gTaytulla are lined up ). Currently, the company has a product portfolio of 165 generics in US

Europe - 599 vs 378 cr, up 58 pc ( key brands like - RYALTRIS - nasal spray , Salmex - anti asthma inhaler - continue to do well )

RoW - 732 vs 615 cr, up 19 pc ( GPL - ranks no 8 in Derma, No-2 in expectorants (cough medicines ) in Russia. Launched RIYALTRIS in Malaysia, Saudi Arabia - receiving great response. Also witnesses strong growth in Brazil, Mexico

Brand RIYALTRIS -

Currently being marketed in over 70 countries. Enjoys double digit mkt share in a lot of countries like - Czech, Poland, Australia, RSA, Italy

Glenmark’s commercial parter for RIYALTRIS is US is Hikma ( British major ). Seeing strong demand in US

Brand has completed phase-3 trials in China. NDA application to be submitted by Dec 23

Other comments -

Intend to strike at least one out licensing deal wrt the Ichnos portfolio

Intend to further enhance cash generation to reach debt free status

Entered into an agreement with Nirma Pvt Ltd to sell 75 stake in GLS ( will continue to retain 7.5 pc stake ) for a total consideration of Rs 5600 cr. Company currently has a gross debt of around 4700 cr and a net debt of around 3300 cr

GLS sale likely to be reflected in the Q3 numbers

GPL expects operating leverage to kick in across LatAm and Europe by next FY leading to expansion in EBITDA margins. Also expecting reduced intensity of R&D going forward

India business expected to pick up from Q3 onwards. In Oct, India business grew 20 pc YoY

In Q3, three injectable products are lined up for launch in US. US business should pick up pace in Q3

Aim to hit and maintain EBITDA margins in the 18-19 pc range wef H2 FY 24

Continue to see price erosion in mid single digits in US business

Company is buoyant on the branded and OTC India business going forward. Company remains on a very strong footing in Respiratory, Derma and Cardiac space. Diabetic portfolio is also doing well. Should be able to grow the topline at 12-14 pc for next 3 odd years

Company’s Muroe facility in US should go live by next year. This should also aid margins going forward

Europe business’s margins have reached corporate avg with scope for further improvement. LatAm should reach there in next 1-2 yrs. RoW is already there

My Take ( biased ) - company can report a revenue of aprox 14000 cr and EBITDA of aprox 2500 cr next year. PAT may come in the range of 1300 - 1400 cr. That may lead to significant value unlocking for the company’s stock

Disc: holding, biased, may add more, not SEBI registered