if successful debt will reduce by 46mn $. It is a tender offer to buyback their bond issued 3 or 4 years back, the bond maturity is in 2022 mid of the year.

1 Like

The news seemed pretty significant to me but did not get any reaction from the stock. In the last concall, management said that they had shelved API business monetization plans but maybe due to delay in Ichnos fundraising, they are thinking of listing API business. This should help in bringing down debt (Is my thinking along correct lines?).

Another news

I’m not sure how significant this is.

Just trying to understand the potential for Ryaltris. The total market for allergic rhinitis is 17 bn usd and expected to move to 25 bn by 2025.

The principal treatment are corticosteroids, histamine and one more class of drugs. Ryaltris is a combination of a corticosteroid and histamine. Its efficacy and safety is much superior to a standalone drug. While there are other combinations of combination drugs available. But ryaltris efficacy is at par with most of them.

Usa is 50% of the market in term of geography and combination drugs are 50% of market and quickly gaining mkt share.

Ryaltris is currently approved in s africa, australia ukraine and russia. And application pending in 30 eu countries, usa, china, canada and middle east.

The mktg tie up for front end sales is in place with reputed names in each mkt.

I find this better than a generic sales as innovator

You get better margins and lower competition.

If they get a 1% market share that translates to 170 mn usd of sales .

1 Like

Just an update as there has been lot of buzz about this company in last few days

If news are to be believed, Glenmark is planning to raise 1500 crores through GLS IPO which will result into valuation of around 6K crore if 25% is diluted for that and good news is Glenmark plans to use the proceeds into reducing debt levels as we know that there is no huge capex planned as of now… Looking at IPO frenzy since few months… GLENMARK won’t face any issues raising the money and I think raising through equity is best decision to pare debt. Looking for some shareholder quota in it though.

Ichnos fund raising remains on plan for this year for Glenmark and it will take mcap of Glenmark to all together a new levels as market has till now not factored in any investments made in Ichnos by Glenmark (I am saying this looking at 15K mcap of GLENMARK)

Technically

Stock had been consolidating in strict price range between 490-440 since last 5 months and it has broken the downward trending line with huge volumes

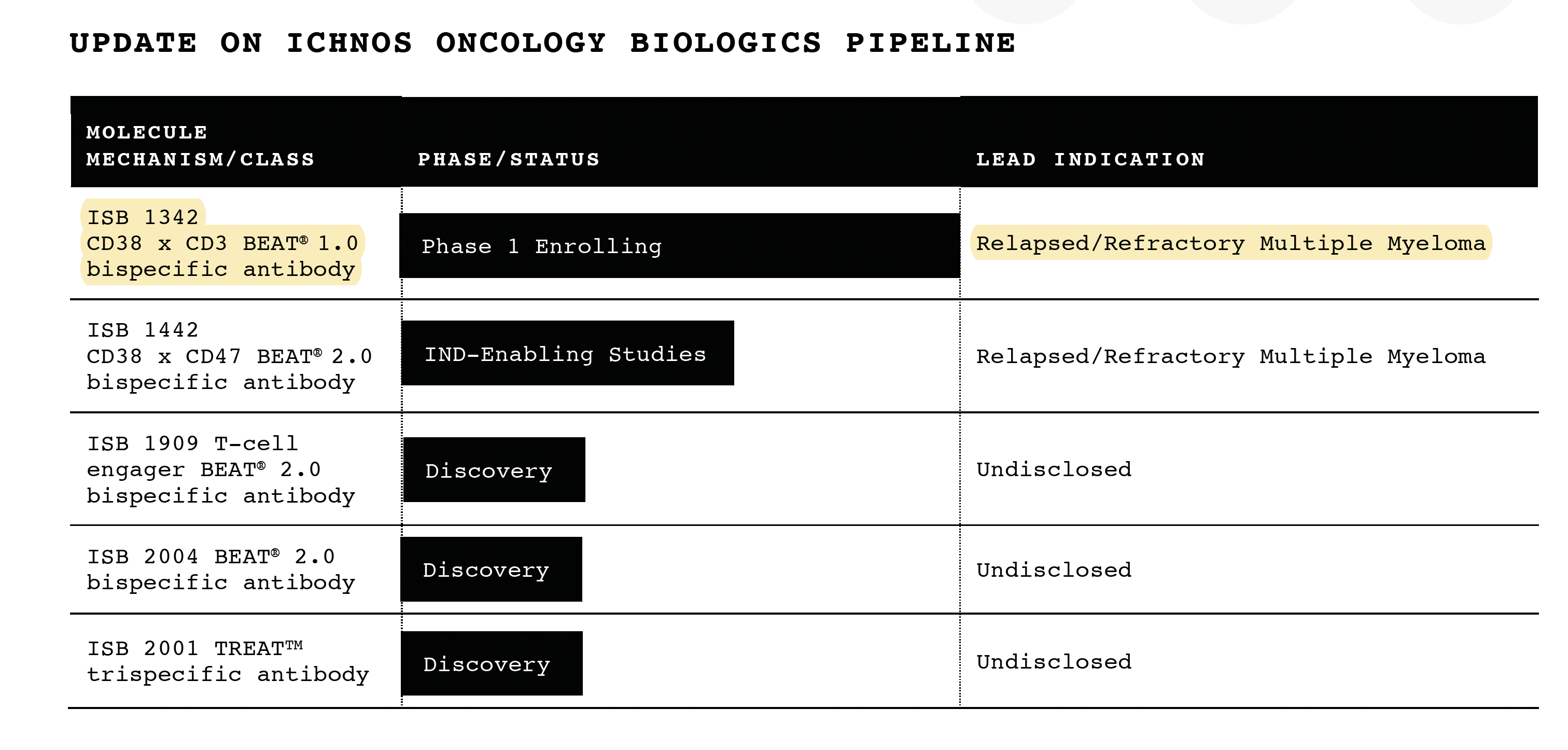

Ichnos pipeline on its website had 2 biologics in phase 1 isb 1342 and isb 1302 till last month.

Now only 1342 is there. Does that mean 1302 has been outlicensed? Can anybody check on this.

1342 and 1302 are in the same universe as trastazumab and dartamumab and are more effective as per ichnos. The current mkt size of these drugs are 10 bn usd pa and 4 bn usd pa.

1 Like

No mention of 1302 on pipeline slide as well. It was there until Q3FY21

Below image is for Q4FY21

Below image is for Q3FY21

They mentioned in todays concall that they have put it on hold to prioritise 1342.

The main points of the call revenue guidance of 10%. With uptick in all key markets and launch pipeline of 10 in usa. Europe they are already selling generic of advair post settlement with innovator. Spiriva is getting launched this qtr. Ryaltris response better than expected in mkts where it has been launched.

Filing in usa to pick up this yr. 40 are pending out of which 20 are ftf/ para iv.

Ichnos fund raise is stuck for proof of concept. Hence they have prioritised 1342 over 1302 as they wanted to control spends as well. 2 oulicensing deal in works, likely in fy 22. Equity raise probably after proof of concept. 1342 data expected in 6 month time to give proof of concept. Ceo departure a concern as per me.

Capex down , r and d up, debt to be down by 1000- 1200 cr depending on ipo price and free cash flow of 400 cr.

Spiriva and advair were positive surprises, ichnos updates were not so much.

2 Likes

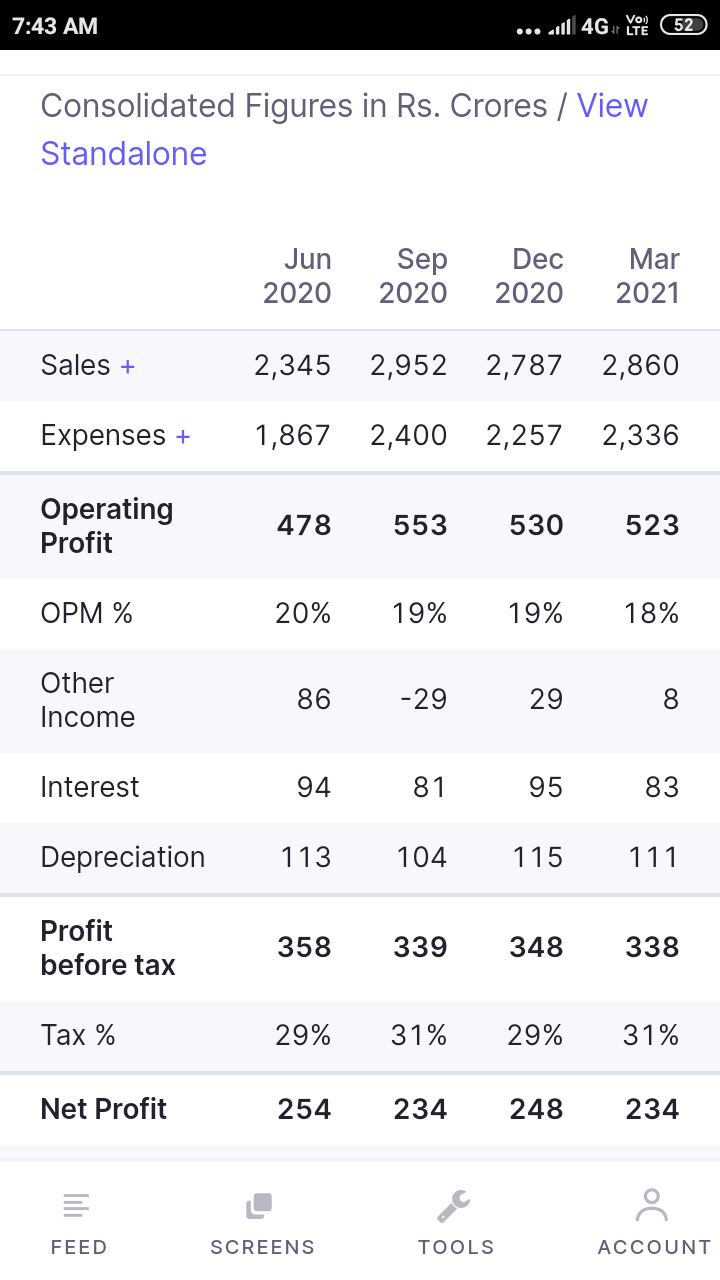

*Glenmark Pharma – Q4FY21 Concall Update –

Glenmark Lifescience’s (API company) IPO is near term trigger which would unlock value for shareholders as well as help in reducing the parent’s company’s debt as well

The stock is trading at 17.2xFY22E consensus earnings

• For FY22 – the company plan to file 18-20 ANDAs including 5-6 filings which got delayed in FY21 due to the pandemic. This includes 4-5 filings from Monroe.

• Ryaltris will be commercialized in Russia in Q1 FY22.

• The company is witnessing recovery in Russia (which de-grew by 7.7% in FY21) on sequential basis

• Europe - For the financial year, the European region signed 21 major contracts for in-licensing products in the region. The region is expected to benefit from significant product launches including products like Tiotropium Bromide Dry Powder Inhaler and Ryaltris in FY22

• Ryaltris - Glenmark submitted responses to European agency queries, which enabled Glenmark to conclude the Decentralized procedure paving the way for potential approval of the product and expected launch of RyaltrisTM in the EU in FY22.

• Forex loss – Rs 5.8 cr in other exps; Rs 75 cr forex loss in FY21

• Gross Debt – Rs 4687cr

• Ichnos – can see some partnerships in FY22

• R&D in FY22 – should be similar to FY21 in absolute terms – it was 11% of sales in FY21 – likely to be 10-11% in FY22

• Tax – likely to be 29-30%

• In US - 3 launches are lined up in Q1 – for FY22 targeting 8-10 launches

• Topline is expected to grow at 10-12% in FY22

2 Likes

1)As per the above ipo proceeds will largely be used to pay the promoter for api spin off-- approx 900 cr

2)150 cr for capex

3)And balance to general corporate purpose which i presume will largely be debt payment. Approx 300 to 400 cr.

Does the point no.1 mean existing shareholders will get a payout out of the IPO.

@Donald @sarthakkumar19_ @harsh.beria93 @kanvgarg123 and others following the stock.

It means Glenmark will get payout as it is existing shareholder. Glenmark may chose to give a special dividend and/or reduce debt.

1 Like

I hope Glenmark pays off some debt as debt has been a major overhang on the stock. Management has also guided for substantial debt reduction within 1 year. If debt isn’t reduced significantly even after receiving IPO proceeds, that would be a major negative in my limited understanding.

Isb 1342 effective in patients where other prevalent medications have failed. Currently in phase 1. Which indicates it is a better line of treatment.

2 Likes

After spiriva and advair glenmark gets approval for brovana as well. If we take ryaltris as well their inhalation portfolio is at par with cipla, if not better.

1 Like

Glenmark pharma

Highlights from the management commentary

-

GNP guided at overall sales growth of 10-12% YoY in FY22, with US sales growth of 10%.

-

The company is guiding at 19-20% EBITDA margin in FY22.

-

Other expense to be ~27% of sales in FY22 v/s 25% in FY21.

-

Absolute R&D spend to remain at FY21 levels in FY22 (10-11% of sales).

-

It had a net debt of INR35b at the end of FY21.

-

GNP indicated a net debt reduction of INR10b-12b, considering: a) free cash flow to be generated from core operations, and b) receipt of money from the upcoming Glenmark Life Science IPO.

3 Likes

I fail to understand why Glenmark Life’s IPO shares got listed flat. Considering the euphoria in the market any tom, dick and harry company too gets oversubscribed.

2 Likes

IMHO glenmark is going through a time correction after a good upmove in last few months and now it seems going through a consolidating correction without much volumes on current fall which itself signals strong accumulation at lower levels by shaking off weaker hands, besides Q1 results being declared on upcoming weekend will surely give good support between 560-580 levels . Company had given good guidance on growth for FY22 and additionally the latest development on license agreement with Canadian firm Sanotize for nitric oxide based nasal spray which eleminates covid19 virus by 80 to 90 percent in upper respiratory tract within a matter of 72 hours can be a real booster for sales if it gets approval in clinical trials already being run in India currently. glenmark has the license to sell this product under fabispray brand which it plans to do so in Q4 of FY22 not only in India but quite a few other Asian countries affected by Covid19. All of the above can further help it drastically reduce its debt exposure and can give analyst a good opportunity to re rate its PE which is running near its lower bottom to rise faster and further high levels.

Discl: Invested for medium to long term in Glenmark Pharmaceuticals

1 Like

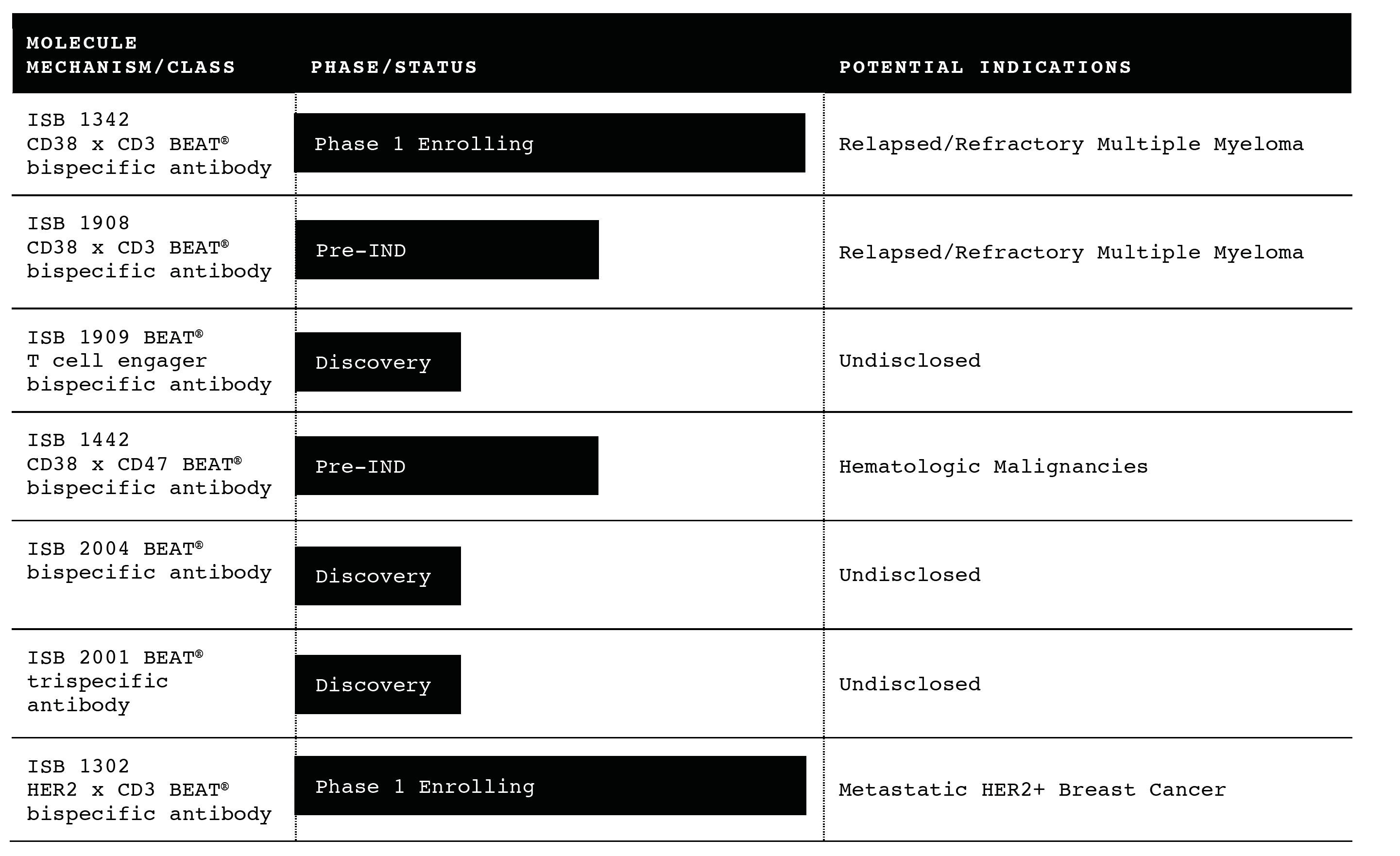

Isb 1442 going in phase 1 in ichnos

Glenmark Q1 beat on all parameters

India formulations are up whopping 48% and are already creating high base…would be difficult to sustain this I suppose

Debt reduction of 1600 crore is being planned this year with ipo proceeds and free cash flows

FaviSpray will be latest addition in CoVID portfolio already into Phase 3 trials

Net Profit At Rs 306.5 Cr Vs CNBC-TV18 Poll Of Rs 261.3 Cr

Revenue At Rs 2,965 Cr Vs CNBC-TV18 Poll Of Rs 2,970.9 Cr

EBITDA At Rs 573.6 Cr Vs CNBC-TV18 Poll Of Rs 554 Cr

EBITDA Margin At 19.3% Vs CNBC-TV18 Poll Of 18.6%

3 Likes

Updates from the concall

Q2 to be strong on the basis of growth in us and ROW, india to belower over last yr

india to grow by 12% to 13% in fy 22. Some good launches expected in 3 months

US launches to 8 to 10 pa including fy 22

At least one outlicensing deal expected this year

Focus on reduction of debt. Capex and r&d to be reigned in for next 2 yr. While free cash flow and outlicensing will help in reducing debt

Ryaltris performing better than expected in all mkts.

Brovana mkt share 28%

Ichnos focus on 1342 data read out,1442 ind enabling studies and phase1

2 Likes