There is no disclosure on what is the deal amount… I read the article saying deal can be work 150-200 crores…

Any one did a rough valuations on VWash?

There is no disclosure on what is the deal amount… I read the article saying deal can be work 150-200 crores…

Any one did a rough valuations on VWash?

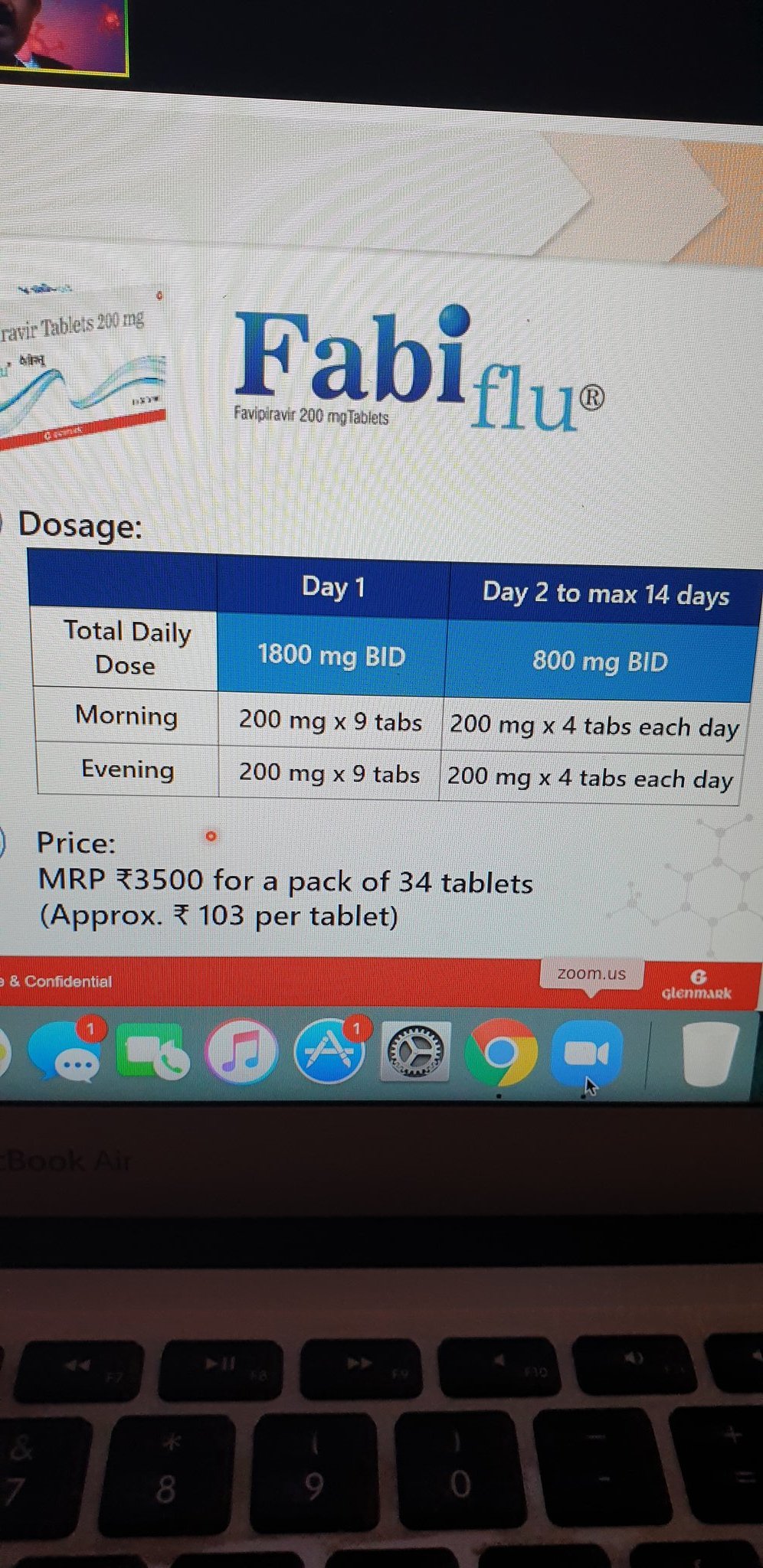

When contacted, Glenmark confirmed it has submitted its application to tbe Drugs Controller General of India (DCGI) for marketing approval of Favipiravir (API)

the company may become the first Indian company to develop an anti-retroviral (ARV) used for the treatment for coronavirus.

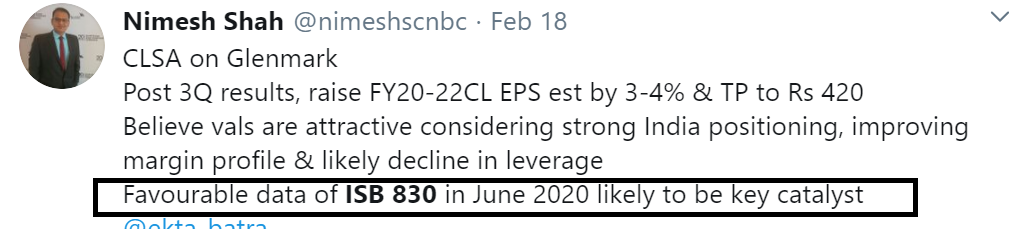

when is ISB 830 particles (an OX40 antagonist monoclonal antibody) final outcome is expected?

as per some reports Glenmark should clear picture by end of April 2020

Last few weeks developments are very positive for the company

Some links on Favipiravir results

http://www.bseindia.com/xml-data/corpfiling/AttachLive/a1d984fc-382f-4be1-97d1-cd5fe8ae8e2b.pdf

Disclosure : Views mentioned are personal with secondary research and hold about 12-15% of my portfolio

Glenmark becomes first company to get approval for launching a drug officially to treat Covid-19 patients with brand (FabiFlu)

vital drugs to treat Covid-19 patients got the drug regulator’s nod on Friday. While Glenmark Pharma got the Drug Controller General of India’s (DCGI’s) approval to launch oral antiviral favipiravir, Maharashtra Health Minister Rajesh Tope claimed Cipla and Hetero also received the nod for Gilead’s repurposed drug remdesivir.

Mumbai-based Glenmark Pharmaceuticals is conducting phase-III clinical trials to assess the drug’s efficacy on Covid-19 patients. The drug may be available as early as next week, claimed sources.

http://www.bseindia.com/xml-data/corpfiling/AttachLive/3989d9b2-8612-4516-a047-7e425796e950.pdf

Disclosure : Holding 10-12% of portfolio

Even though there’s logic in the rationale provided but the target price is too harsh it seems, 257 is like 50% drop from CMP.

Disc:- Not invested (not sure if I’m interested, was looking at screen when price went down to the lowest this march)

Trust me this report has no meaning. All the points are vague here…

All the four points mentioned in relation to CoVID may be correct but that doesn’t warrant share price falling 45% more from today close… because share rose for drug announcement from 400 to 550 odd levels … which is the only gap here…

Share has been in a range of 270-350 since few quarters due to capital allocation, debt and US revenue issues but recent re-rating of Pharma as a sector had caused a rise to 350;400 levels

One side he says eps would only increase by 0.20 in a most optimized scenario for CoVID and then share price down target given is 258 without any basis… It’s weird

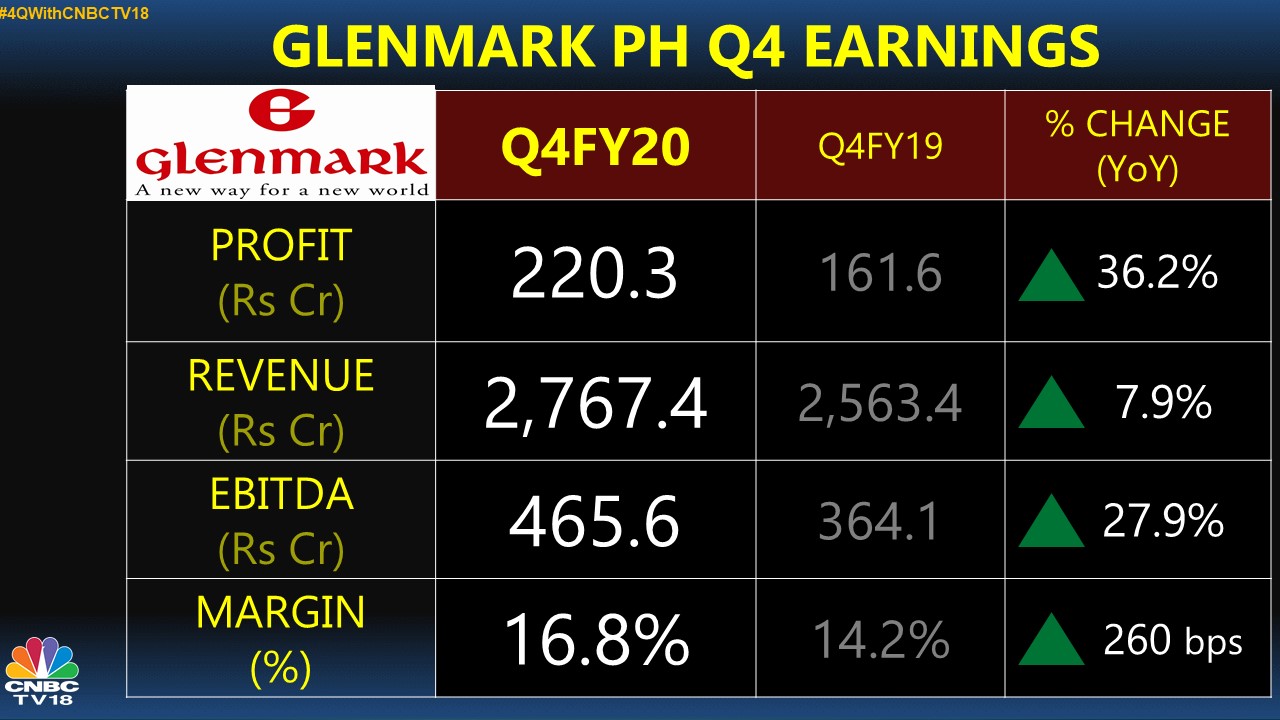

Results are beat again 3rd quarter in a row…

Positives

Negatives

Positive developments

Glenmark.pdf (1.3 MB)

Hello Guys, I did some research on Glenmark Pharma and posting the same here.

Any views on why debt is growing inspite of 30% Gr in cash flows and no addition Expense on ICONHS in Q4

Ichnos had 230 odd crore expense in Q4…

And overall 700-750 crores for year FY19-20

I didn’t get your question. Recently they did CAPEX in Monroe USA and spend over $100M dollars. ICHNOS spend hasn’t stopped. I think they spent some 820 Cr. rupees this year.

Glenmark Pharma share price tumbles 5% on price-fixing allegations in US

Some important points from Annual Report worth knowing

Our manufacturing facility in Monroe was commissioned to manufacture oral solids with injectables expected to follow suit in the near future. The coming months and years will see Glenmark launch more niche generics and injectables in the US and accelerate filings for new products in the market.

As a part of our move from vanilla generics to specialty products, Glenmark’s first proprietary speciality product Ryaltris™ (olapatadine hydrochloride and mometasone furoate) Nasal Spray for seasonal allergic rhinitis is on course to being launched in global markets. During the year, Glenmark’s partner Seqirus Pty. Ltd. received marketing approval for Ryaltris™ from the Therapeutic Goods Administration (TGA), Australia. The launch is planned for the second quarter of FY21 and we have dispatched launch quantities. Glenmark also entered into an exclusive licensing agreement with Hikma to commercialize Ryaltris™ in the US where our product is currently under review.

Glenmark has signed commercialization deals for

Ryaltris™ in China, Australia, New Zealand and South

Korea, and is working to close partnerships in various

other markets, including the European Union where

an application for approval is pending. Clinical trials in

Russia have been concluded and Glenmark’s Russian

subsidiary will shortly seek regulatory approval.

Ryaltris™ has also received marketing approval in

Cambodia, Uzbekistan, Namibia and South Africa.

Glenmark launches NINDANIB, a branded generic drug for treatment of pulmonary fibrosis in India. I have been following Glenmark’s domestic division, it is the best performing among all listed competitors. Although the recent high growth has come from the launch of their COVID drug, even before covid they were very strong in chronic medicines and have managed to grow much faster than IPM rates. I have attached some reports covering glenmark’s domestic business.

Could you please explain this further. I thought glenmark did not have any corporate governance issues.

Thanks

Actually there are no corporate governance issues as such…it’s just that.management has not walked the way they have talked so far in last 2 years of what I have been following…

I have been hearing plans of cutting of debt since last couple of years but there are no major actions

Then they also said that they will sell of some assets, apart from VWash I never saw any such sales too…

So… management has been not able to keep the words many times and fortunately they started doing good since last 9 months so company is better positioned than what it was before 9 months…